Resources

About Us

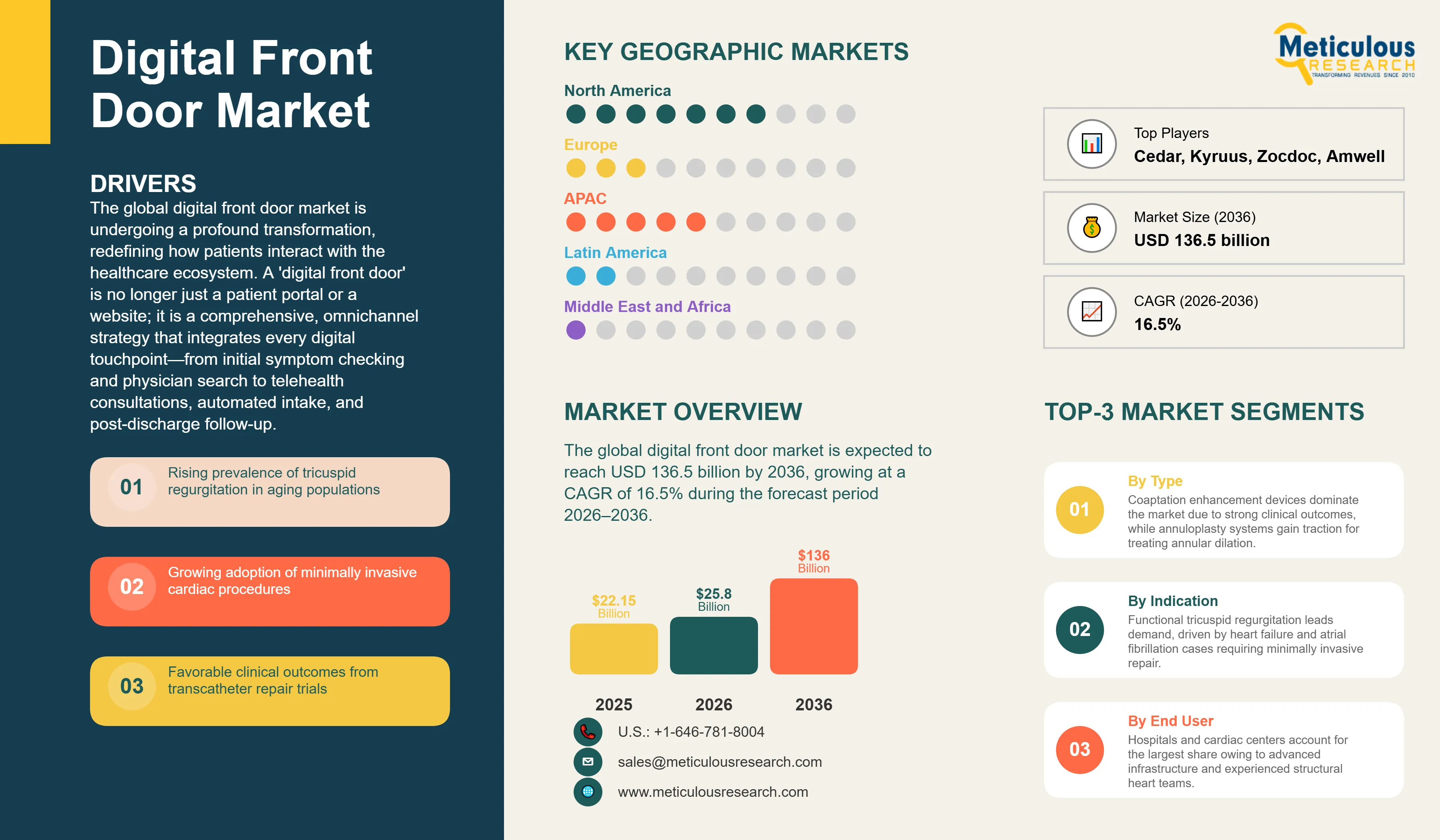

The global digital front door market was valued at USD 25.8 billion in 2026. This market is expected to reach USD 136.5 billion by 2036, growing at a CAGR of 16.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global digital front door market is undergoing a profound transformation, redefining how patients interact with the healthcare ecosystem. A 'digital front door' is no longer just a patient portal or a website; it is a comprehensive, omnichannel strategy that integrates every digital touchpoint—from initial symptom checking and physician search to telehealth consultations, automated intake, and post-discharge follow-up. By 2026, this market has become the cornerstone of 'healthcare consumerism,' as patients increasingly demand digital convenience comparable to retail, banking, and travel. The shift from episodic, reactive care to continuous, proactive engagement is the primary catalyst driving health systems to consolidate their fragmented digital tools into a single, unified entry point.

The urgency of this transformation is underscored by changing consumer expectations and operational pressures. A majority of healthcare consumers now expect mobile-first access, including the ability to self-schedule appointments and pay bills online. For healthcare providers, the digital front door is a critical tool for combating staffing shortages and operational inefficiencies. Automated intake and self-scheduling tools can significantly reduce administrative staff workload, allowing personnel to focus on high-value patient care. Furthermore, organizations with a robust digital front door strategy report meaningful improvements in patient retention and reduced appointment no-show rates, directly impacting the financial sustainability of health systems.

Technological convergence is a key theme in 2026. Telehealth, once a standalone service, is now fully integrated into the digital front door, serving as a primary gateway for outpatient care. Virtual visits are projected to account for a significant and growing share of all outpatient encounters globally in 2026. This integration is supported by AI-driven symptom checkers and chatbots that utilize natural language processing (NLP) to triage patients effectively, ensuring they are routed to the right level of care whether it be a virtual consultation, an urgent care visit, or home-based monitoring. The proliferation of mobile health (mHealth) applications, with billions of users worldwide, further cements the digital front door as the primary interface for the modern patient.

Geographically, North America remains the leading market, holding an significant share in 2026, driven by mature healthcare IT infrastructure and high consumer demand for digital access. However, the Asia-Pacific region is emerging as the fastest-growing market, with a projected CAGR exceeding 15–20% through the next decade. This growth is fueled by a 'mobile-first' population and massive government-led digital health transformations in China and India. As healthcare systems globally pivot toward value-based care, the digital front door serves as the essential infrastructure for managing population health and ensuring equitable, convenient access to medical services.

The rise of healthcare consumerism is the most significant driver for the digital front door market. Patients now view themselves as consumers who demand the same level of digital convenience in healthcare as they experience in retail and banking. This includes mobile-first access, real-time communication, and transparent billing. Additionally, the global healthcare staffing crisis is forcing organizations to automate administrative tasks. Digital front doors provide the self-service tools necessary to handle registration, scheduling, and triage without human intervention. The continued proliferation of telehealth also drives demand, as a unified digital entry point is required to manage the transition between virtual and in-person care seamlessly.

Security and data privacy concerns remain a primary restraint, as a centralized digital entry point creates a high-value target for cyberattacks. Protecting sensitive patient health information (PHI) across multiple omnichannel touchpoints requires significant investment in cybersecurity. Furthermore, the high cost and complexity of integrating these modern platforms with legacy Electronic Health Record (EHR) systems can be a major barrier, particularly for smaller health systems. Ensuring a consistent user experience across diverse mobile devices and operating systems also presents a continuous technical challenge for vendors and providers.

The integration of Generative AI in patient triage and communication offers a monumental opportunity. LLM-powered chatbots can provide more natural, empathetic, and accurate symptom checking, significantly improving the patient experience. There is also a substantial opportunity in the expansion of digital front doors into the pharmaceutical sector, particularly for clinical trial recruitment and medication adherence monitoring. In emerging economies, the 'leapfrog' effect—where populations move directly to mobile-first healthcare—presents a vast untapped market for digital front door vendors. Furthermore, the use of predictive analytics within these platforms can help health systems anticipate patient needs and proactively offer wellness services.

Navigating a fragmented vendor landscape is a major challenge for healthcare organizations. Many vendors offer specialized 'point solutions,' making it difficult to build a truly integrated, 'all-in-one' digital front door. Bridging the 'digital divide' is another critical challenge; health systems must ensure that their digital strategies do not exclude elderly patients or those with limited digital literacy or access to technology. Finally, maintaining high levels of user engagement over the long term is difficult; platforms must provide continuous value beyond simple scheduling to remain the patient's primary gateway for all healthcare needs.

Digital front doors are increasingly using AI-enabled healthcare CRM platforms and EHR-integrated data to deliver hyper-personalized patient experiences, including tailored reminders, education, and provider recommendations. This is supported by widespread digital infrastructure. According to ASTP/ONC (2024), 99% of U.S. hospitals enable electronic access to health information, 92% support secure messaging, and 96% allow data download, enabling large-scale personalized engagement. Patient willingness further enables adoption, with HIMSS reporting that 77% of patients are open to sharing health data to improve outcomes. Overall, digital front doors are evolving into AI-driven engagement layers, where CRM and clinical data converge to enable continuous, context-aware personalization across the patient journey.

Digital front doors are increasingly shifting from fragmented point solutions (separate telehealth apps, scheduling tools, bill pay portals, and symptom checkers) toward unified, integrated patient access platforms that centralize the end-to-end care journey. This consolidation is driven by the need to reduce patient friction and improve continuity across access, care delivery, and financial workflows. This trend is reinforced by the scale of digital fragmentation already embedded in healthcare delivery. According to the Office of the National Coordinator for Health IT (ONC, ASTP), while 99% of U.S. hospitals are electronically connected, interoperability and cross-system data exchange remain uneven, with hospitals still relying on multiple disconnected vendor systems for scheduling, messaging, and billing workflows. This structural fragmentation is a key driver for platform unification efforts. Industry adoption patterns further validate this shift. HIMSS surveys consistently highlight that healthcare organizations prioritize platform integration and interoperability as top digital transformation goals, with fragmented patient access systems cited as a major barrier to experience consistency and operational efficiency.

Based on component, the market is segmented into Software and Services. In 2026, the Software segment is expected to hold the largest share. This segment encompasses the core patient-facing applications, including patient portals, mobile apps, AI chatbots, and self-scheduling engines, which are the primary drivers of digital engagement.

The Services segment is projected to witness the fastest growth. As health systems move from simple portals to complex, integrated omnichannel strategies, the demand for consulting, custom implementation, and ongoing support and maintenance services is increasing significantly.

Based on end user, the market is segmented into Healthcare Providers, Healthcare Payers, and Pharmaceutical Companies. In 2026, the Healthcare Providers segment is expected to hold the largest share. Hospitals and physician groups are the primary architects of the digital patient journey, using these platforms to acquire new patients and improve operational efficiency.

The Healthcare Payers segment is projected to witness the fastest growth. Insurance companies are increasingly adopting digital front door strategies to improve member engagement, promote wellness programs, and steer members toward lower-cost, high-quality virtual care options.

North America is expected to hold the largest share of the global Digital Front Door market in 2026, driven by a highly mature healthcare IT ecosystem, strong adoption of EHR-based patient engagement tools, and rising demand for consumer-grade healthcare experiences. The region accounts for roughly 40–50% of global market value across most industry estimates, supported by widespread deployment of platforms such as Epic Systems, Oracle Health (Cerner), and Salesforce.

Europe remains a significant market, supported by regulatory and interoperability initiatives such as the European Health Data Space (EHDS), which is accelerating the standardization of digital health access and patient data exchange. Asia-Pacific is projected to be the fastest-growing region over the forecast period, driven by rapid digital health adoption, expanding healthcare infrastructure, and mobile-first populations in countries such as China and India. Overall, the market is characterized by strong platform consolidation, with major players including Epic Systems, Oracle Health, Microsoft, Salesforce, and Teladoc Health shaping the global competitive landscape

The competitive landscape of the digital front door market is characterized by a mix of established EHR giants, CRM leaders, and specialized 'best-of-breed' patient engagement vendors. Competition is centered on the ability to provide a seamless, omnichannel user experience, deep integration with clinical workflows, and advanced AI-driven triage and communication capabilities. Strategic acquisitions and partnerships are common as vendors seek to build comprehensive, 'all-in-one' platforms.

Key players in the global market include Epic Systems Corporation (U.S.), Oracle Corporation (Cerner) (U.S.), Salesforce, Inc. (U.S.), Microsoft Corporation (U.S.), GE Healthcare (U.S.), Philips Healthcare (Netherlands), GetWellNetwork, Inc. (U.S.), Phreesia, Inc. (U.S.), Cedar (U.S.), Kyruus (U.S.), Zocdoc (U.S.), Amwell (U.S.), Teladoc Health, Inc. (U.S.), Luma Health (U.S.), QliqSOFT, Inc. (U.S.), Notable Health (U.S.), Stericycle, Inc. (Communication Solutions) (U.S.), Wolters Kluwer (U.S.), Religent (U.S.), and Healthgrades (U.S.).

The market is projected to reach USD 136.5 billion by 2036, growing at a CAGR of 16.5% from 2026 to 2036.

Organizations with a robust digital front door strategy report improved patient retention and loyalty.

Telehealth and virtual visits are projected to account for 25-30% of all outpatient encounters globally by 2026.

The Asia-Pacific region is projected to be the fastest-growing market due to its mobile-first population and rapid digital health transformation.

Automated intake and self-scheduling tools can significantly reduce administrative staff workload, allowing personnel to focus on high-value patient care

Patients now demand retail-like digital convenience, including mobile access, real-time communication, and online bill pay.

The market is expected to grow at a CAGR of 16.5% during the forecast period 2026–2036.

The Software segment holds the largest share as it encompasses the core patient-facing applications and engagement tools.

Security and privacy concerns, along with the high cost and complexity of integrating with legacy EHR systems, are major restraints.

Leading players include Epic Systems, Oracle (Cerner), Salesforce, Microsoft, and GE Healthcare.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Component

3.2.2. Market Analysis, by Technology/Application

3.2.3. Market Analysis, by Deployment Mode

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Rise of Healthcare Consumerism (Retail-like Convenience Demand)

4.2.1.2. Need for Operational Efficiency to Combat Staffing Shortages

4.2.1.3. Proliferation of Telehealth as a Primary Care Gateway

4.2.1.4. Increasing Patient Expectations for Mobile-First Omnichannel Access

4.2.2. Restraints

4.2.2.1. Security and Privacy Concerns Regarding Centralized Patient Access

4.2.2.2. High Cost and Complexity of Integration with Legacy EHR Systems

4.2.3. Opportunities

4.2.3.1. Integration of Generative AI for Natural Language Triage and Triage

4.2.3.2. Expansion into Pharmaceutical Clinical Trial Recruitment and Adherence

4.2.3.3. Rapid Digital Health Transformation in Emerging Mobile-First Economies

4.2.4. Challenges

4.2.4.1. Navigating a Fragmented Landscape of Specialized Point Solutions

4.2.4.2. Bridging the Digital Divide for Elderly and Low-Literacy Populations

4.2.5. Trends

4.2.5.1. Hyper-Personalization through Integrated CRM and AI Analytics

4.2.5.2. Consolidation of Disparate Tools into Unified Healthcare 'Super-Apps'

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Digital Front Door Market, by Component

5.1. Overview

5.2. Software

5.3. Services

6. Global Digital Front Door Market, by Technology/Application

6.1. Overview

6.2. Telehealth & Virtual Care Integration

6.3. Patient Intake & Self-Scheduling

6.4. AI-driven Symptom Checkers & Chatbots

6.5. Patient Communication & CRM Platforms

7. Global Digital Front Door Market, by Deployment Mode

7.1. Overview

7.2. Cloud-based Solutions

7.3. On-premise Solutions

8. Global Digital Front Door Market, by End User

8.1. Overview

8.2. Healthcare Providers

8.3. Healthcare Payers

8.4. Pharmaceutical Companies

9. Global Digital Front Door Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. Australia

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Dashboard

10.4. Vendor Market Positioning

10.5. Market Share Analysis, 2025

11. Company Profiles

11.1. Epic Systems Corporation

11.2. Oracle Corporation (Cerner)

11.3. Salesforce, Inc.

11.4. Microsoft Corporation

11.5. GE Healthcare

11.6. Philips Healthcare

11.7. GetWellNetwork, Inc.

11.8. Phreesia, Inc.

11.9. Cedar

11.10. Kyruus

11.11. Zocdoc

11.12. Amwell

11.13. Teladoc Health, Inc.

11.14. Luma Health

11.15. QliqSOFT, Inc.

11.16. Notable Health

11.17. Wolters Kluwer

11.18. Relatient, Inc.

11.19. Healthgrades

12. Appendix

Published Date: May-2026

Published Date: Nov-2025

Published Date: May-2024

Published Date: Jul-2024

Published Date: Jun-2026

Subscribe to get the latest industry updates