Resources

About Us

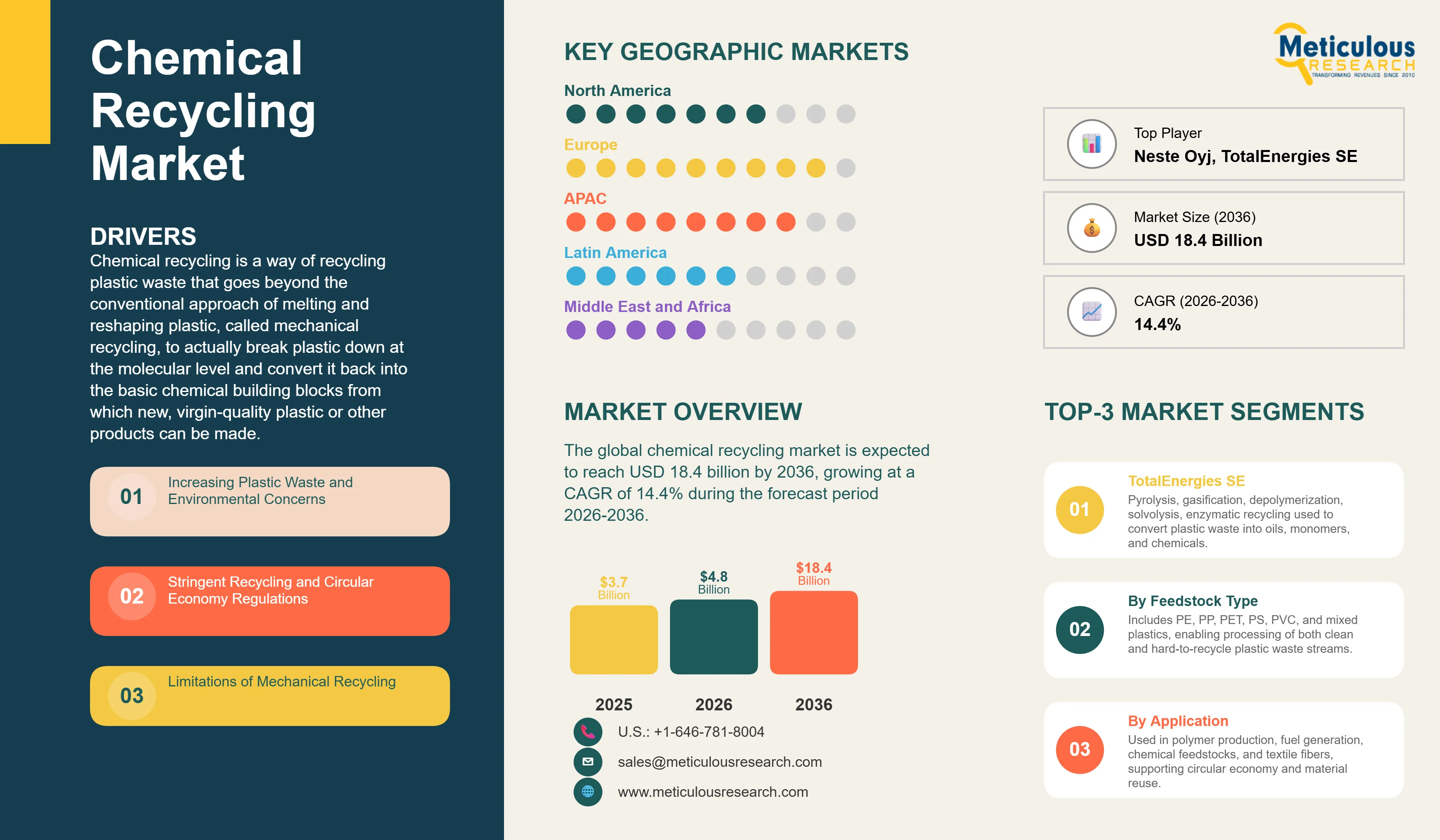

The global chemical recycling market was valued at USD 3.7 billion in 2025. This market is expected to reach USD 18.4 billion by 2036 from an estimated USD 4.8 billion in 2026, growing at a CAGR of 14.4% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Chemical recycling is a way of recycling plastic waste that goes beyond the conventional approach of melting and reshaping plastic, called mechanical recycling, to actually break plastic down at the molecular level and convert it back into the basic chemical building blocks from which new, virgin-quality plastic or other products can be made. When you put a plastic bottle in a recycling bin, it typically goes through mechanical recycling where it is shredded, melted, and reformed into lower-grade plastic products like park benches or fleece clothing. Chemical recycling takes a fundamentally different approach by using heat, chemical reactions, or biological enzymes to break the polymer chains in plastic back down into simpler chemicals called monomers or into liquid oils that can be fed directly into chemical and refinery plants as raw material. The key advantage of this approach is that the output material is functionally identical to virgin plastic derived from fossil fuels, which means it can be used in demanding applications like food packaging that requires the highest purity standards and that mechanical recycling typically cannot meet.

The market is growing strongly because the global plastic waste problem has reached a scale that conventional recycling approaches simply cannot solve. Globally, only about 9% of plastic waste is actually recycled, with the rest going to landfill, incineration, or ending up in the natural environment. The primary reason that mechanical recycling cannot handle more plastic is that most real-world plastic waste is a complex mixture of different plastic types, colors, and contaminants that cannot be cleanly sorted and separately recycled, and many plastic types including flexible packaging and multilayer films cannot be mechanically recycled at all because they are too complex or too contaminated. Chemical recycling can in principle accept this mixed, contaminated, and otherwise unrecyclable plastic waste and convert it into useful outputs, addressing the large fraction of plastic waste that the current recycling system simply cannot handle.

Two significant near-term opportunities are driving investment and growth. The European Union's Single-Use Plastics Directive and its packaging regulation require increasingly high levels of recycled content in plastic packaging over the coming years, and companies selling packaged goods in Europe are facing legally binding obligations to include chemically recycled plastic in their packaging if mechanical recycling alone cannot provide sufficient supply of sufficiently high quality recycled material. This regulatory pressure is creating a strong and growing commercial demand signal for chemical recycling output. In addition, the very large food and beverage industry's need for food-grade recycled plastic, which conventional mechanical recycling cannot reliably produce at the required purity level, is creating premium-priced demand for chemically recycled PET and other food-contact plastics that justifies the higher cost of chemical recycling processes compared with mechanical alternatives.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 18.4 Billion |

|

Market Size in 2026 |

USD 4.8 Billion |

|

Market Size in 2025 |

USD 3.7 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 14.4% |

|

Dominating Technology Type |

Pyrolysis |

|

Fastest Growing Technology Type |

Enzymatic Recycling |

|

Dominating Feedstock Type |

Polyethylene Terephthalate (PET) |

|

Fastest Growing Feedstock Type |

Mixed Plastics |

|

Dominating Application |

Polymer and Plastic Production |

|

Fastest Growing Application |

Chemical Feedstock Production |

|

Dominating End-Use Industry |

Packaging Industry |

|

Fastest Growing End-Use Industry |

Automotive Industry |

|

Dominating Product Output |

Recycled Polymers |

|

Fastest Growing Product Output |

Chemical Intermediates |

|

Dominating Process Stage |

Conversion Processes |

|

Fastest Growing Process Stage |

Pre-Treatment and Sorting |

|

Dominating Geography |

Europe |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Major Petrochemical Companies Building Chemical Recycling into Their Core Business

One of the most commercially significant trends in the chemical recycling market is the active entry of the world's largest petrochemical and oil companies into chemical recycling as a strategic business line rather than a peripheral sustainability initiative. BASF's ChemCycling program, which accepts mixed plastic waste and converts it through pyrolysis into pyrolysis oil that is fed into BASF's existing steam cracker facilities to produce virgin-quality polymer feedstocks, is one of the most commercially advanced examples of a major chemical company integrating chemical recycling into its existing production infrastructure. ExxonMobil has announced plans for several large-scale pyrolysis-based chemical recycling facilities in the United States, with individual plant capacities targeting processing of tens of thousands of tonnes of plastic waste annually. TotalEnergies has partnered with Plastic Energy to build pyrolysis-based recycling capacity in Europe. Shell and Neste have announced chemical recycling programs that integrate recycled plastic feedstocks into their existing refinery and petrochemical infrastructure.

The entry of major petrochemical players is commercially significant for several reasons. These companies have existing large-scale chemical processing facilities, established relationships with plastic product manufacturers who are their primary customers for virgin plastic feedstocks, and the financial resources to invest in commercial-scale chemical recycling capacity without needing to wait for the technology to reach cost parity with fossil-based feedstocks. For small and medium specialist chemical recycling technology companies, the large petrochemicals companies represent both potential customers for their technology and credible partners for scaling commercial operations faster than they could achieve independently. The competitive dynamic between specialist technology developers and large industrial players integrating chemical recycling is shaping the commercial structure of the industry as it scales.

Enzymatic Recycling of PET Opening Food-Grade Recycled Plastic at Scale

The commercial development of enzymatic recycling technology by Carbios, a French company that has engineered a biological enzyme called PETase that breaks down PET plastic into its component monomers at commercially relevant speeds and temperatures, represents one of the most technically significant advances in the chemical recycling market. PET is one of the most widely used plastics globally, used in water bottles, beverage containers, food trays, and polyester textiles, and it is also one of the most valuable recycling targets because the recycled PET monomers can be repolymerized into new PET that is functionally identical to virgin PET and meets food-contact safety requirements.

Carbios has signed a licensing agreement with Indorama Ventures, the world's largest PET producer, to build the first commercial-scale enzymatic PET recycling plant, and has secured partnerships with major brands including L'Oreal, Nestle Waters, PepsiCo, and Suntory to supply recycled PET produced through its enzymatic process. The commercial advantage of enzymatic recycling for PET is that it can accept highly contaminated and colored PET waste that other depolymerization methods struggle with, and produces monomer outputs of sufficient purity for food-contact packaging applications. As the enzymatic recycling technology scales up and production costs fall, it is expected to become an important source of food-grade recycled PET for the large food and beverage packaging market that is facing growing regulatory pressure to increase recycled content.

EU Regulation Creating Mandatory Demand for Chemical Recycling Output

The European Union's regulatory framework for plastic packaging and circular economy is creating the most powerful and commercially binding demand signal for chemical recycling output of any regulatory environment globally, effectively mandating the market into existence on a defined timeline. The EU Packaging and Packaging Waste Regulation requires that all plastic packaging placed on the EU market must contain minimum percentages of recycled content by 2030 and 2040, with specific requirements varying by packaging type. For contact-sensitive packaging including food and beverage containers, the required recycled content levels can only be met with high-purity chemically recycled plastic because mechanical recycling cannot consistently deliver the food-safety-compliant material quality required.

The practical effect of the EU regulations is that every major consumer goods company selling packaged products in the EU, including Unilever, Nestle, PepsiCo, Coca-Cola, L'Oreal, and hundreds of others, must either secure supply of chemically recycled plastic or face the inability to sell their products in one of the world's largest consumer markets. This commercial necessity is driving branded consumer goods companies to make long-term offtake commitments with chemical recycling facilities and to invest directly in chemical recycling capacity, providing the demand certainty and sometimes the direct capital that chemical recycling project developers need to justify large facility investments. Similar regulatory pressure is building in the UK, Canada, Japan, South Korea, and several other countries following the EU's lead on plastic recycling mandates.

Limitations of Mechanical Recycling

The fundamental constraint of mechanical recycling, which can only process clean, sorted, single-type plastic waste and produces recycled plastic of lower quality than the original material, means that the majority of real-world plastic waste cannot be recycled through existing infrastructure regardless of how many collection bins are provided or how much consumer participation is achieved. Mixed plastic packaging, multilayer films, contaminated containers, and plastic types that are not commercially viable to sort and mechanically recycle separately collectively represent a very large fraction of all plastic waste generated. Chemical recycling addresses this limitation directly because pyrolysis and gasification processes can accept mixed, contaminated, and otherwise unrecyclable plastic feedstocks and convert them into valuable outputs, and depolymerization processes can produce higher-purity outputs from more homogeneous feedstocks. The recognized inadequacy of mechanical recycling alone to meet the plastic recycling targets mandated by EU and national regulations is creating a policy and commercial consensus that chemical recycling must be deployed at significant scale to complement mechanical recycling, which is the most important structural driver of the chemical recycling market.

Rising Demand for Recycled Feedstock

The growing commitments of major consumer goods companies, branded packaging manufacturers, and plastic product companies to increase the recycled content in their products is creating genuine commercial demand for chemically recycled plastic feedstocks that goes beyond regulatory compliance to include brand differentiation and customer expectation. Companies including Danone, Unilever, Coca-Cola, PepsiCo, and L'Oreal have made public commitments to increase the recycled plastic content in their packaging to 25%, 50%, or even higher percentages by 2025 or 2030. These commitments, whether driven by regulatory requirements, investor pressure, or customer preference, are translating into active procurement programs for recycled plastic feedstocks and, where sufficient supply is not available from mechanical recycling, direct investment in or offtake agreements with chemical recycling facilities. The combination of regulatory mandates and voluntary corporate commitments is creating a large and growing demand for recycled plastic feedstocks that exceeds what the current recycling infrastructure can supply, making the expansion of chemical recycling capacity a commercially necessary response to this demand gap.

Integration with Petrochemical Value Chain

The most commercially efficient pathway for chemical recycling to scale rapidly is the integration of recycled plastic feedstocks into existing large-scale petrochemical production infrastructure, which eliminates the need to build entirely new processing facilities and allows chemical recyclers to leverage the enormous capital already invested in conventional cracker and refinery plants. When pyrolysis oil produced from plastic waste is fed into a conventional steam cracker alongside naphtha from oil refining, the cracker does not distinguish between the fossil-derived and recycled inputs and produces the same ethylene and propylene outputs that are then used to make new plastic. This mass-balance accounting approach, where the recycled content is tracked through the shared production process, is accepted by certification bodies including the International Sustainability and Carbon Certification plus standard and is used by BASF, ExxonMobil, and others to certify the recycled content of products made using their ChemCycling and comparable programs. The integration opportunity is enormous because it means that the entire existing global petrochemical production capacity could potentially process recycled plastic feedstocks without needing to build equivalent new capacity from scratch, dramatically reducing the capital investment required for the chemical recycling industry to achieve significant scale.

Increasing Demand for Food-Grade Recycled Plastics

The food and beverage packaging market represents the highest-value and most commercially attractive application for chemical recycling output because it requires the highest purity recycled plastic and is willing to pay the highest premium over mechanically recycled material, yet it is precisely the application that mechanical recycling cannot serve reliably due to the food-safety contamination risks associated with mechanically recycled material. PET water bottles and food trays, polypropylene food containers, and polyethylene food film all require recycled plastic that meets strict food-safety regulations governing residual contaminants, and the depolymerization and solvolysis processes used in chemical recycling produce monomer-level outputs that can be repolymerized to full food-grade specification. Carbios's enzymatic PET depolymerization, Loop Industries's low-temperature depolymerization, and the chemical recycling programs of Indorama Ventures, the world's largest PET producer, are all specifically targeting the food-grade recycled PET market where the combination of regulatory obligation and premium pricing creates the most commercially viable business case for chemical recycling technology at current production costs.

By Technology Type: In 2026, Pyrolysis to Dominate

Based on technology type, the global market is segmented into pyrolysis, gasification, depolymerization, solvolysis, and enzymatic recycling. In 2026, the pyrolysis segment is expected to account for the largest share of the global chemical recycling market. Pyrolysis, which heats plastic waste in the absence of oxygen to break it down into a mixture of oils, gases, and char, is the most commercially deployed chemical recycling technology globally, with the largest number of operating commercial facilities and the most mature technology base. Pyrolysis is particularly well-suited to mixed and contaminated plastic waste that other chemical recycling methods struggle to process, making it the most flexible technology for accepting the diverse real-world plastic waste streams that chemical recyclers must work with. Companies including Plastic Energy, Brightmark, Agilyx, and Licella have operated commercial or demonstration pyrolysis plants, and the major oil and petrochemical companies including ExxonMobil, Shell, and TotalEnergies are building large-scale pyrolysis capacity integrated with their existing refinery and petrochemical infrastructure.

However, the enzymatic recycling segment is projected to register the highest CAGR during the forecast period. Carbios's commercial breakthrough with its engineered PETase enzyme, combined with the significant commercial interest from major brands and the licensing agreement with Indorama Ventures for large-scale commercial plant development, is driving rapid investment and development activity in enzymatic recycling. The superior output purity achievable through enzymatic depolymerization compared with thermal processes like pyrolysis, and the specific fit of enzymatic recycling for the high-value food-grade PET recycling application, makes this the highest-growth technology segment in the market.

By Feedstock Type: In 2026, PET to Hold the Largest Share

Based on feedstock type, the global chemical recycling market is segmented into polyethylene, polypropylene, polyethylene terephthalate, polystyrene, polyvinyl chloride, and mixed plastics. In 2026, the PET segment is expected to account for the largest share of the overall market. PET is the most commercially valuable chemical recycling feedstock because it is widely collected through bottle deposit and curbside recycling systems in developed markets, has well-established depolymerization chemistry through both glycolysis and emerging enzymatic routes, and produces monomer outputs that can directly replace virgin PET at full food-grade quality. The large global PET bottle and packaging market, the strong regulatory push for recycled PET content in food and beverage packaging, and the commercial viability of PET depolymerization at current technology costs collectively make PET the dominant feedstock type by revenue.

However, the mixed plastics segment is projected to register the highest CAGR during the forecast period. Mixed plastics represent the largest volume of currently unrecyclable plastic waste that chemical recycling can address, and the pyrolysis and gasification technologies capable of processing mixed plastic waste feedstocks are scaling up rapidly. As the volume of plastic waste that needs to be diverted from landfill and incineration grows and as the chemical recycling capacity to process mixed plastics expands, this feedstock segment is expected to grow very rapidly from its current smaller base.

By Application: In 2026, Polymer and Plastic Production to Hold the Largest Share

Based on application, the global market is segmented into polymer and plastic production, fuel production, chemical feedstock production, textile and fiber production, and other applications. In 2026, the polymer and plastic production segment is expected to account for the largest share of the overall market. Converting chemically recycled plastic back into new polymer materials, particularly for packaging applications where recycled content requirements are most stringent, is the highest-value application for chemical recycling output and the application that drives the most investment and commercial activity. The combination of regulatory mandates requiring recycled content in packaging and the premium pricing achievable for certified recycled polymers makes polymer production the dominant application by revenue value.

However, the chemical feedstock production segment is projected to register the highest CAGR during the forecast period. The conversion of plastic waste into monomers and petrochemical intermediates that can be used as raw materials across the entire chemicals manufacturing value chain, not just for plastic production, represents a larger and more diversified market opportunity than packaging polymer production alone. As the pyrolysis and cracking capacity integrated with large petrochemical complexes scales up, the production of chemical intermediates from recycled plastic feedstocks is expected to grow rapidly.

By End-Use Industry: In 2026, Packaging Industry to Hold the Largest Share

Based on end-use industry, the global chemical recycling market is segmented into packaging, automotive, textile, construction, electronics, consumer goods, and others. In 2026, the packaging industry segment is expected to account for the largest share of the global chemical recycling market. Packaging is both the largest application for plastic globally and the industry facing the most direct and binding regulatory pressure to increase recycled content, making it the primary driver of demand for chemical recycling output. The EU Packaging and Packaging Waste Regulation, the UK Plastic Packaging Tax, Canada's draft recycled content regulations, and similar measures in multiple other markets are creating commercially mandatory demand for recycled content in packaging that is directly translating into procurement commitments and investment in chemical recycling capacity.

However, the automotive industry segment is projected to register the highest CAGR during the forecast period. Automakers are under growing pressure to reduce the carbon footprint of their vehicles and to increase the use of recycled materials in vehicle production, and the automotive sector is increasingly adopting recycled polymer materials for interior components, under-hood parts, and structural applications. The transition to electric vehicles, which use more plastic components per vehicle than conventional vehicles in battery housings, interior trims, and thermal management systems, is expanding the automotive sector's total plastic consumption and its interest in sustainable recycled material sources.

Chemical Recycling Market by Region: Europe Leading by Share, Asia-Pacific by Growth

Based on geography, the global market is segmented into Europe, North America, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, Europe is expected to account for the largest share of the global chemical recycling market. Europe leads the global chemical recycling market because it has the most comprehensive and binding regulatory framework for plastic recycling of any region, creating the strongest and clearest commercial demand signal for recycled plastic that drives investment in chemical recycling capacity at a pace not matched elsewhere. The EU Packaging and Packaging Waste Regulation's mandatory recycled content requirements, the EU's Single-Use Plastics Directive, and the individual national legislation of member states collectively create a regulatory environment where every major consumer goods company and packaging manufacturer operating in the European market must secure supply of high-quality recycled plastic, including chemically recycled material, or face non-compliance. The Netherlands, Belgium, Germany, and France are particularly active chemical recycling development markets, with numerous pilot and commercial-scale facilities operating or under construction. The Netherlands' Rotterdam port area hosts a concentration of chemical and petrochemical infrastructure that makes it a natural hub for chemical recycling facilities integrated with the existing petrochemical value chain. Carbios in France, Plastic Energy in Spain and the UK, and the European programs of BASF, Shell, and TotalEnergies represent the leading commercial chemical recycling activities in the region.

However, the Asia-Pacific chemical recycling market is expected to grow at the fastest CAGR during the forecast period. Asia generates the largest volume of plastic waste of any region globally, with China, India, Indonesia, and other developing Asian countries facing severe plastic pollution challenges that are driving national policy action and creating large-scale demand for advanced recycling solutions. China's dual carbon goals and its growing emphasis on circular economy development are driving investment in chemical recycling technology and capacity, with several Chinese companies developing pyrolysis and depolymerization facilities at commercial scale. Japan has a long history of thermal recycling of plastic waste and is now transitioning toward chemical recycling approaches that produce higher-value outputs as the regulatory environment for chemical recycling certification improves. South Korea's government has committed to significant chemical recycling capacity targets as part of its plastic waste management strategy. India's growing awareness of plastic pollution and its expanding regulatory framework for extended producer responsibility is creating the policy foundation for chemical recycling market development, and Indonesia, Thailand, and Vietnam are beginning to invest in chemical recycling infrastructure as international brands pressure their regional packaging suppliers to provide recycled content options.

North America is a large and rapidly growing chemical recycling market, primarily driven by the United States where the combination of state-level recycled content mandates in California, Washington, and other states is creating growing demand for high-quality recycled plastic alongside the large corporate sustainability commitments of major U.S. consumer goods companies. ExxonMobil's large-scale chemical recycling investments at its Baytown Texas facility, which targets processing 500 million pounds of plastic waste annually, represent one of the most ambitious commercial chemical recycling programs in the world. Canada's draft national recycled content standards and British Columbia's extended producer responsibility program for packaging are creating growing policy-driven demand in Canada, and Mexico's growing manufacturing sector is beginning to address plastic waste through chemical recycling initiatives supported by international brand partnerships.

The chemical recycling industry includes specialist technology developers who have built proprietary recycling processes, large petrochemical and oil companies integrating recycling into existing infrastructure, waste management companies providing feedstock supply and logistics, and emerging biotechnology companies developing enzymatic and biological recycling approaches. Competition is based on technology efficiency and output quality, feedstock flexibility and acceptance capability, cost per tonne of processed plastic, integration with existing industrial infrastructure, certification credentials for recycled content claims, and the strength of offtake agreements with consumer brands providing commercial demand certainty.

BASF's ChemCycling program is one of the most commercially established large-scale chemical recycling programs, using pyrolysis oil from plastic waste as feedstock in its existing chemical production infrastructure and certifying recycled content through mass balance accounting. Eastman Chemical Company has built what it describes as the world's largest molecular recycling facility at its Kingsport Tennessee site, using methanolysis to depolymerize PET and other polyesters back to their building blocks for high-value applications. Carbios has developed the most commercially advanced enzymatic PET recycling technology and is scaling toward commercial plant operation through its partnership with Indorama Ventures. Plastic Energy is a leading pyrolysis technology developer and operator with plants in Spain, the UK, and projects in development across Europe and North America. Neste is integrating recycled plastic feedstocks into its renewable products refinery in Finland alongside its biofuel products.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' technology platforms, operating track records, customer relationships, geographic presence, and recent strategic developments. Some of the key players operating in the global chemical recycling market include BASF SE (Germany), Eastman Chemical Company (U.S.), Plastic Energy Ltd. (UK), Agilyx Corporation (U.S.), Neste Oyj (Finland), Loop Industries Inc. (Canada), SABIC (Saudi Arabia), TotalEnergies SE (France), ExxonMobil Corporation (U.S.), Shell plc (UK/Netherlands), Veolia Environnement S.A. (France), Indorama Ventures Public Company Limited (Thailand), Carbios (France), Brightmark LLC (U.S.), and Licella Holdings Ltd. (Australia), among others.

The global chemical recycling market is expected to reach USD 18.4 billion by 2036 from an estimated USD 4.8 billion in 2026, at a CAGR of 14.4% during the forecast period 2026-2036.

In 2026, the pyrolysis segment is expected to hold the largest share of the global chemical recycling market, reflecting pyrolysis being the most commercially deployed and technically mature chemical recycling technology with the largest number of operating commercial facilities and the broadest feedstock acceptance capability.

The enzymatic recycling segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by Carbios's commercial breakthrough with engineered PETase technology, the Indorama Ventures licensing agreement for large-scale commercial plant development, and the strong commercial interest from major food and beverage brands in food-grade recycled PET produced through enzymatic depolymerization.

In 2026, the polymer and plastic production segment is expected to hold the largest share of the global chemical recycling market, driven by the mandatory recycled content requirements for packaging materials in EU and national regulations creating commercially binding demand for high-quality recycled polymers that only chemical recycling can supply at the required purity levels.

Europe is expected to dominate the global market in 2026, driven by the EU's comprehensive and binding plastic recycling regulatory framework creating the strongest commercial demand signal for chemical recycling output of any region globally, and the concentration of leading chemical recycling technology developers and operating facilities in Western Europe.

The market is primarily driven by the fundamental limitations of mechanical recycling that leave the majority of real-world plastic waste unrecyclable, creating a large addressable market for chemical recycling technologies that can process mixed, contaminated, and difficult plastic waste streams, combined with the growing regulatory mandates in Europe and other markets requiring recycled content in packaging that mechanical recycling alone cannot supply in sufficient quantity and quality.

Key players are BASF SE (Germany), Eastman Chemical Company (U.S.), Plastic Energy Ltd. (UK), Agilyx Corporation (U.S.), Neste Oyj (Finland), Loop Industries Inc. (Canada), SABIC (Saudi Arabia), TotalEnergies SE (France), ExxonMobil Corporation (U.S.), Shell plc (UK/Netherlands), Veolia Environnement S.A. (France), Indorama Ventures Public Company Limited (Thailand), Carbios (France), Brightmark LLC (U.S.), and Licella Holdings Ltd. (Australia), among others.

Asia-Pacific is expected to register the highest growth rate in the global chemical recycling market during the forecast period 2026-2036, driven by the very large plastic waste volumes generated across Asia creating urgent demand for advanced recycling solutions, China's circular economy investments, and the growing extended producer responsibility frameworks in South Korea, Japan, and India creating policy-driven demand for chemical recycling capacity.

1. Introduction

1.1 Market Definition

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Approaches for Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.3.3 Growth Forecast

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1 Introduction

4.2 Market Dynamics

4.2.1 Drivers

4.2.1.1 Increasing Plastic Waste and Environmental Concerns

4.2.1.2 Stringent Recycling and Circular Economy Regulations

4.2.1.3 Limitations of Mechanical Recycling

4.2.1.4 Rising Demand for Recycled Feedstock

4.2.2 Restraints

4.2.2.1 High Capital and Operational Costs

4.2.2.2 Limited Commercial Scale Infrastructure

4.2.2.3 Feedstock Quality Variability

4.2.3 Opportunities

4.2.3.1 Development of Advanced Recycling Technologies

4.2.3.2 Integration with Petrochemical Value Chain

4.2.3.3 Increasing Demand for Food-Grade Recycled Plastics

4.2.3.4 Expansion in Emerging Markets

4.2.4 Challenges

4.2.4.1 Regulatory Uncertainty and Certification Issues

4.2.4.2 Energy Intensity of Chemical Recycling Processes

4.3 Technology Landscape

4.3.1 Pyrolysis

4.3.2 Gasification

4.3.3 Depolymerization

4.3.4 Solvolysis (Hydrolysis, Glycolysis, Methanolysis)

4.3.5 Enzymatic Recycling

4.4 Chemical Recycling Value Chain

4.4.1 Waste Collection and Sorting

4.4.2 Feedstock Preparation

4.4.3 Chemical Conversion Processes

4.4.4 Refining and Upgrading

4.4.5 End-Product Manufacturing

4.5 Value Chain Analysis

4.5.1 Waste Management Companies

4.5.2 Technology Providers

4.5.3 Chemical and Petrochemical Companies

4.5.4 Plastic Manufacturers and Converters

4.5.5 End Users

4.6 Regulatory and Standards Landscape

4.6.1 Circular Economy Policies (EU, U.S., Asia)

4.6.2 Recycling Targets and Mandates

4.6.3 Certification Standards (ISCC+, etc.)

4.7 Porter’s Five Forces Analysis

4.8 Investment and Industry Trends

4.8.1 Investments in Recycling Infrastructure

4.8.2 Partnerships between Waste and Chemical Companies

4.8.3 Scaling of Commercial Plants

4.9 Cost and Pricing Analysis

4.9.1 Cost by Recycling Technology

4.9.2 Cost vs Mechanical Recycling

4.9.3 Pricing of Recycled Outputs

5. Chemical Recycling Market, by Technology Type

5.1 Introduction

5.2 Pyrolysis

5.3 Gasification

5.4 Depolymerization

5.5 Solvolysis

5.5.1 Hydrolysis

5.5.2 Glycolysis

5.5.3 Methanolysis

5.6 Enzymatic Recycling

6. Chemical Recycling Market, by Feedstock Type

6.1 Introduction

6.2 Polyethylene (PE)

6.3 Polypropylene (PP)

6.4 Polyethylene Terephthalate (PET)

6.5 Polystyrene (PS)

6.6 Polyvinyl Chloride (PVC)

6.7 Mixed Plastics

7. Chemical Recycling Market, by Application

7.1 Introduction

7.2 Polymer and Plastic Production

7.2.1 Packaging Materials

7.2.2 Consumer Goods Plastics

7.2.3 Automotive Plastics

7.3 Fuel Production

7.3.1 Diesel and Gasoline Alternatives

7.3.2 Synthetic Fuels

7.4 Chemical Feedstock Production

7.4.1 Monomers and Intermediates

7.4.2 Petrochemical Feedstocks

7.5 Textile and Fiber Production

7.5.1 Polyester Fibers

7.5.2 Industrial Textiles

7.6 Other Applications

8. Chemical Recycling Market, by End-Use Industry

8.1 Introduction

8.2 Packaging Industry

8.3 Automotive Industry

8.4 Textile Industry

8.5 Construction Industry

8.6 Electronics Industry

8.7 Consumer Goods Industry

8.8 Others

9. Chemical Recycling Market, by Product Output

9.1 Introduction

9.2 Recycled Polymers

9.3 Fuels

9.4 Chemical Intermediates

10. Chemical Recycling Market, by Process Stage

10.1 Introduction

10.2 Pre-Treatment and Sorting

10.3 Conversion Processes

10.4 Post-Treatment and Refining

11. Chemical Recycling Market, by Geography

11.1 Introduction

11.2 North America

11.2.1 U.S.

11.2.2 Canada

11.2.3 Mexico

11.3 Europe

11.3.1 Germany

11.3.2 U.K.

11.3.3 France

11.3.4 Netherlands

11.3.5 Belgium

11.3.6 Italy

11.3.7 Spain

11.3.8 Sweden

11.3.9 Rest of Europe

11.4 Asia-Pacific

11.4.1 China

11.4.2 India

11.4.3 Japan

11.4.4 South Korea

11.4.5 Indonesia

11.4.6 Thailand

11.4.7 Vietnam

11.4.8 Australia

11.4.9 Rest of Asia-Pacific

11.5 Latin America

11.5.1 Brazil

11.5.2 Mexico

11.5.3 Argentina

11.5.4 Chile

11.5.5 Colombia

11.5.6 Rest of Latin America

11.6 Middle East & Africa

11.6.1 UAE

11.6.2 Saudi Arabia

11.6.3 South Africa

11.6.4 Turkey

11.6.5 Egypt

11.6.6 Rest of Middle East & Africa

12. Competitive Landscape

12.1 Overview

12.2 Key Growth Strategies

12.3 Competitive Benchmarking

12.4 Competitive Dashboard

12.4.1 Industry Leaders

12.4.2 Market Differentiators

12.4.3 Vanguards

12.4.4 Emerging Companies

12.5 Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1 BASF SE

13.2 Eastman Chemical Company

13.3 Plastic Energy Ltd.

13.4 Agilyx Corporation

13.5 Neste Oyj

13.6 Loop Industries, Inc.

13.7 SABIC

13.8 TotalEnergies SE

13.9 ExxonMobil Corporation

13.10 Shell plc

13.11 Veolia Environnement S.A.

13.12 Indorama Ventures Public Company Limited

13.13 Carbios

13.14 Brightmark LLC

13.15 Licella Holdings Ltd.

14. Appendix

14.1 Additional Customization

14.2 Related Reports

Published Date: Apr-2026

Published Date: Feb-2025

Published Date: May-2022

Published Date: Mar-2026

Subscribe to get the latest industry updates