Resources

About Us

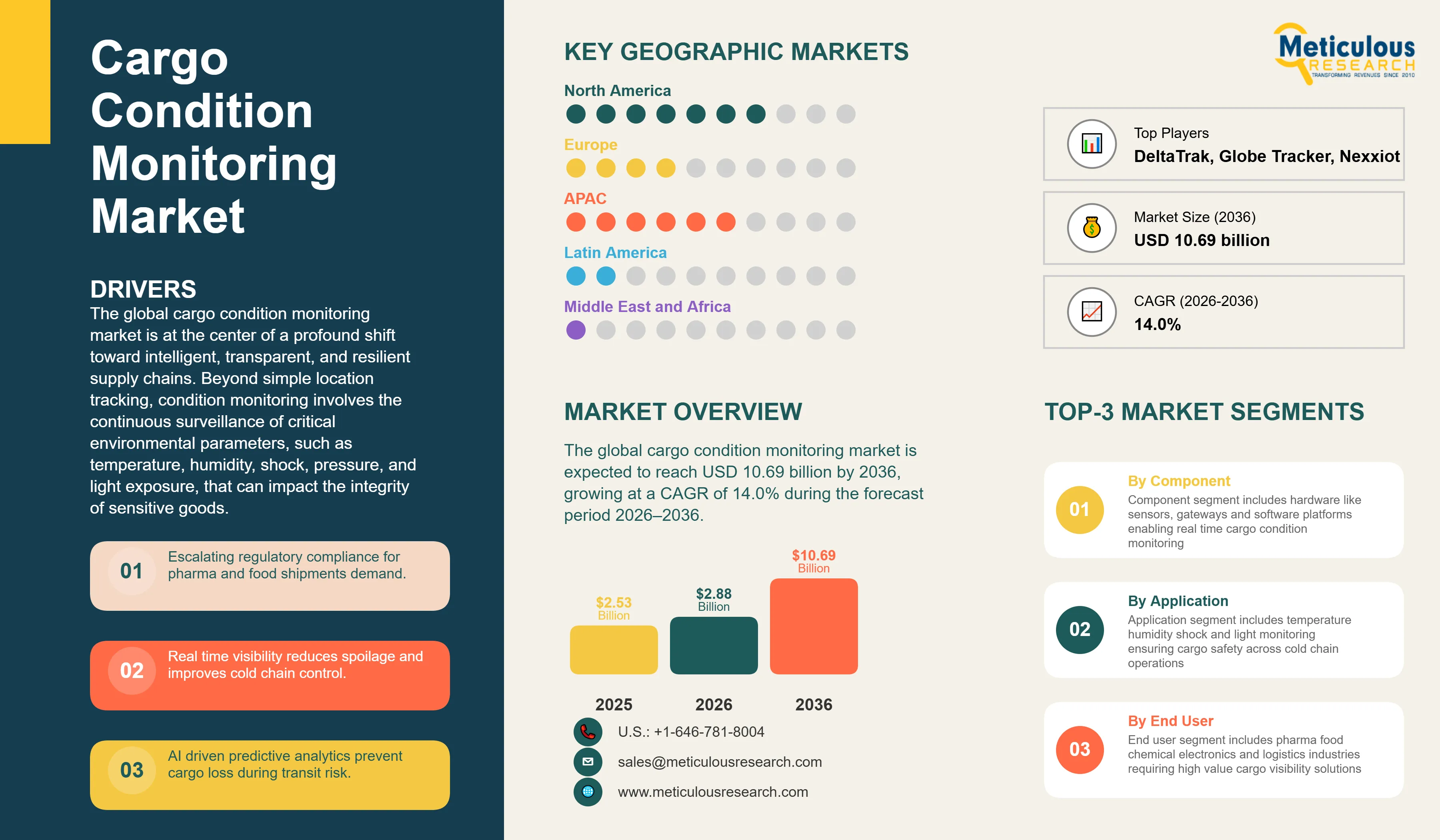

The global cargo condition monitoring market is estimated to be USD 2.88 billion in 2026. This market is expected to reach USD 10.69 billion by 2036, growing at a CAGR of 14.0% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

he global cargo condition monitoring market is at the center of a profound shift toward intelligent, transparent, and resilient supply chains. Beyond simple location tracking, condition monitoring involves the continuous surveillance of critical environmental parameters, such as temperature, humidity, shock, pressure, and light exposure, that can impact the integrity of sensitive goods. According to the International Air Transport Association (IATA), the integration of real-time monitoring technologies is essential for reducing cargo loss and ensuring compliance with global quality standards. As trade networks become increasingly complex and intermodal, the ability to gain situational awareness into the cargo's immediate environment is no longer a luxury but a fundamental requirement for risk mitigation and quality assurance. This market evolution is driven by the convergence of IoT, advanced sensor technology, and low-power connectivity, enabling stakeholders to transform raw data into actionable intelligence for proactive supply chain orchestration.

Drivers: Mitigating Spoilage and Meeting Stringent Global Regulatory Mandates

The growth of the global cargo condition monitoring market is primarily driven by the imperative to reduce waste in the cold chain and the increasing rigor of regulatory mandates governing the transport of sensitive goods. Shippers and logistics providers are under immense pressure to guarantee product efficacy and safety, particularly for pharmaceuticals and fresh produce. Telematics and sensor-based monitoring provide the necessary documentation and real-time alerts to address environmental excursions immediately, thereby preventing costly cargo rejections and ensuring consumer safety.

Escalating Regulatory Compliance Requirements for Sensitive Cargo

Regulatory frameworks such as the FDA's Food Safety Modernization Act (FSMA) and the EU's Good Distribution Practice (GDP) guidelines for medicinal products have established strict requirements for environmental monitoring during transit. These regulations mandate that shippers maintain a verifiable 'chain of custody' and 'chain of temperature' for sensitive cargo. Cargo condition monitoring systems provide automated, tamper-proof logs that satisfy these compliance needs, driving widespread adoption among pharmaceutical and food manufacturers who must mitigate the risk of regulatory non-compliance and product recalls.

Urgent Need to Reduce Global Spoilage and Financial Loss in the Cold Chain

The global logistics industry faces multi-billion dollar losses annually due to cargo spoilage, damage, and theft. According to the Food and Agriculture Organization (FAO), a significant portion of food loss occurs during transportation and handling. Cargo condition monitoring systems, equipped with shock, light, and temperature sensors, enable real-time detection of door openings, rough handling, or refrigeration failures. This allows for immediate corrective actions, such as rerouting cargo or adjusting cooling settings, significantly reducing waste and protecting the financial interests of all stakeholders in the supply chain.

Rising Demand for End-to-End Visibility in High-Value Intermodal Logistics

As global trade increasingly relies on intermodal transport, the 'black holes' in supply chain visibility, particularly during port transfers or remote maritime transit, have become unacceptable. Condition monitoring solutions provide continuous visibility across all modes of transport, offering shippers and carriers a unified view of their assets. This transparency is critical for high-value industries like electronics and aerospace, where even minor environmental fluctuations can lead to significant functional damage. The ability to provide real-time status updates and precise ETAs based on actual cargo conditions is a powerful driver for market expansion.

Restraints: Addressing High Hardware Costs and Data Interoperability Barriers

Despite the clear advantages, the widespread adoption of cargo condition monitoring is hindered by the high initial costs of sensor deployment and the complexities of integrating disparate data streams into legacy supply chain platforms. Furthermore, the lack of universal standards for data exchange across different logistics providers and national networks remains a significant barrier to achieving true end-to-end transparency.

Significant Upfront Investment for Large-Scale Sensor Deployment

The cost of equipping thousands of shipping containers or individual pallets with high-precision, multi-parameter sensors and communication gateways is substantial. For many small-to-medium-sized logistics providers, the initial capital expenditure (CAPEX) can be prohibitive. While the long-term return on investment (ROI) from reduced spoilage is clear, the upfront financial burden often leads to phased implementations or the prioritization of only the most high-value cargo, restraining the overall pace of market penetration.

Challenges in Data Interoperability and Cross-Platform Integration

The cargo monitoring ecosystem is characterized by a multitude of hardware vendors and software platforms, often with proprietary data formats and communication protocols. Integrating these diverse data streams into a single, cohesive view for the shipper or carrier is a complex task. The lack of standardized APIs and data models across the industry creates 'data silos,' where information from one leg of the journey cannot be easily shared with stakeholders in the next. This fragmentation complicates the realization of seamless, end-to-end visibility and slows the adoption of integrated monitoring solutions.

Opportunities: Leveraging AI and Blockchain for Autonomous Supply Chain Trust

The future of the cargo condition monitoring market lies in the integration of emerging technologies like Artificial Intelligence (AI) and Blockchain to create self-correcting and highly transparent logistics networks. AI-driven predictive models can anticipate potential spoilage events before they occur, while Blockchain provides an immutable record of cargo conditions, fostering unprecedented levels of trust and accountability among supply chain partners.

AI-Driven Predictive Analytics for Proactive Spoilage Prevention

The massive volume of data generated by condition monitoring sensors provides a rich foundation for AI and machine learning. These technologies can analyze historical patterns and real-time data to predict when a refrigeration unit is likely to fail or when cargo is at risk of spoilage due to external conditions. By providing 'predictive alerts,' AI enables logistics providers to take proactive measures, such as scheduling emergency maintenance or accelerating delivery, to save at-risk cargo. The development of these autonomous risk management platforms represents a significant growth opportunity for telematics vendors.

Integration with Blockchain for Immutable Chain-of-Custody Records

Blockchain technology offers a powerful solution for the challenges of supply chain trust and accountability. By recording cargo condition data on an immutable, distributed ledger, all parties in the supply chain can have absolute confidence in the integrity of the data. This is particularly valuable for insurance claims, regulatory audits, and verifying the provenance of sensitive goods. The integration of condition monitoring with Blockchain platforms can streamline administrative processes, reduce disputes, and create a new standard for transparency in global trade.

Rapid Proliferation of 'Smart Containers' and Integrated Sensor Networks

A major trend in 2026 is the transition from external, add-on sensors to 'smart containers' with built-in, integrated monitoring systems. Leading shipping lines and container lessors are increasingly ordering new equipment with factory-installed telematics and sensor arrays. This integrated approach ensures higher reliability, better power management, and seamless data transmission from the moment the container is loaded. This shift is expected to significantly accelerate the digitalization of the global container fleet and lower the barrier for shippers to access monitoring services.

Advancements in Low-Power Connectivity and Energy-Harvesting Technologies

To address the challenge of powering sensors over long journeys, the industry is witnessing rapid advancements in energy-harvesting technologies and low-power connectivity. Solar-powered gateways and sensors that utilize kinetic energy or thermal gradients are becoming more common. Coupled with the rollout of global LPWAN (LTE-M/NB-IoT) networks, these innovations enable 'install and forget' monitoring solutions that can operate autonomously for years. This focus on sustainability and operational simplicity is a key driver for the mass adoption of condition monitoring across diverse cargo types.

Analysis by Component

Based on component, the hardware segment is expected to hold the largest share of the global cargo condition monitoring market in 2026. This dominance is fundamentally rooted in the physical requirement for sensors and communication gateways to capture and transmit environmental data. Every pallet, container, or warehouse zone requires the physical installation of devices capable of monitoring temperature, humidity, shock, and light. Hardware remains the primary revenue generator during the current phase of massive infrastructure build-out and fleet-wide tagging. However, the software/platform segment is projected to register the highest CAGR during the forecast period. As the hardware foundation matures, the market's value is rapidly shifting toward the data analytics platforms that transform raw sensor readings into actionable insights. Shippers and carriers are increasingly prioritizing platforms that offer predictive spoilage alerts, automated compliance reporting, and AI-driven risk mitigation, leading to higher margins and recurring revenue for software providers.

Analysis by Technology

By technology, the cellular (LTE-M/NB-IoT) segment is expected to hold the largest share in 2026. Cellular networks provide the most cost-effective and widespread coverage for regional and national logistics networks, offering a perfect balance of data throughput and power efficiency. The widespread availability of global roaming agreements for LPWAN technologies makes cellular the default choice for over 90% of land-based and near-shore cargo monitoring. However, the satellite & hybrid connectivity segment is projected to grow at the fastest CAGR during the forecast period. The expansion of LEO satellite constellations and the increasing demand for seamless, uninterrupted visibility during deep-sea maritime transit and in remote cross-border corridors are driving this growth. Shippers of high-value and ultra-sensitive cargo are increasingly adopting hybrid devices that intelligently switch between cellular and satellite networks to ensure 'zero-gap' visibility, regardless of the asset's location.

Analysis by End User

By end user, the pharmaceutical & healthcare segment is expected to hold the largest share in 2026. This leadership is driven by the extreme sensitivity and high financial value of medical cargo, coupled with rigorous global regulatory requirements (e.g., EU GDP, FDA Title 21 CFR Part 11). For these industries, any environmental excursion can lead to total product loss and significant legal liability, making advanced condition monitoring an absolute necessity rather than an optional service. However, the food & beverage segment is projected to register the highest CAGR during the forecast period. The rapid expansion of the global cold chain to meet consumer demand for fresh, organic, and exotic produce is a major driver. Furthermore, the increasing industry focus on reducing food waste, which accounts for billions of dollars in annual losses, is pushing food producers and retailers to adopt real-time monitoring to ensure food safety and optimize inventory management.

Largest Share: North America

North America is expected to dominate the global cargo condition monitoring market in 2026, holding a market share of approximately 38%. This leading position is primarily attributed to the region's advanced logistics infrastructure, early adoption of IoT technologies, and the presence of a massive pharmaceutical and healthcare sector. Stringent regulatory frameworks enforced by the FDA and Health Canada necessitate the use of advanced monitoring solutions for temperature-sensitive cargo. Furthermore, the high concentration of technology vendors and the rapid integration of smart warehouse systems drive significant demand. The key companies operating in the North America market are Sensitech (Carrier Global), Emerson Electric Co., ORBCOMM Inc., Tive, and Roambee Corporation.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global cargo condition monitoring market, with a CAGR of 11.5% during the forecast period. This rapid expansion is fueled by massive investments in cold chain infrastructure and the digital transformation of logistics sectors in China, India, and Southeast Asia. The region's booming e-commerce market and the increasing demand for high-quality, fresh produce are driving the adoption of real-time monitoring solutions. Additionally, the modernization of pharmaceutical manufacturing hubs in India and China is creating substantial demand for compliant and reliable condition tracking. The key companies operating in the Asia Pacific market are Advantech Co., Ltd., Dot Telematics, and various regional technology integrators.

Competitive Landscape: Innovating for a Resilient Supply Chain

The global cargo condition monitoring market is characterized by a high degree of innovation and strategic collaboration. Key players are focusing on developing end-to-end solutions that combine ruggedized hardware with sophisticated, AI-driven analytics platforms. Strategic partnerships with shipping lines, airlines, and container lessors are common as companies seek to integrate their monitoring services directly into the transport infrastructure. Furthermore, a strong emphasis is placed on developing user-friendly platforms that provide actionable insights, moving beyond mere data collection to value-added services like predictive maintenance and automated compliance reporting. The market is also seeing a surge in specialized startups focusing on niche areas like ultra-low temperature monitoring for vaccines or shock-sensitive tracking for high-tech electronics.

Sensitech (Carrier Global) (US), Emerson Electric Co. (US), ORBCOMM Inc. (US), Controlant (Iceland), Tive (US), Roambee Corporation (US), Arviem AG (Switzerland), Envirotainer (Sweden), SkyCell AG (Switzerland), Berlinger & Co. AG (Switzerland), ELPRO-BUCHS AG (Switzerland), LogTag Recorders (New Zealand), DeltaTrak Inc. (US), OnAsset Intelligence Inc. (US), Monnit Corporation (US), Hanwell Solutions (Ellab) (UK), Savvy Telematic Systems (Switzerland), Globe Tracker (Denmark), Nexxiot AG (Switzerland), Advantech Co., Ltd. (Taiwan).

The global Cargo Condition Monitoring market is estimated to be approximately USD 2.88 billion in 2026, with a projected growth to USD 10.69 billion by 2036, at a CAGR of 14.0%.

Key drivers include the escalating regulatory compliance requirements for sensitive cargo and the urgent need to reduce global spoilage and financial loss in the cold chain.

Restraints include the significant upfront investment required for large-scale sensor deployment and challenges in data interoperability across fragmented logistics networks.

Opportunities lie in the integration of AI for proactive spoilage prevention and the use of Blockchain for immutable chain-of-custody records.

The hardware segment is expected to hold the largest share due to the foundational need for physical sensors, while the software segment is projected for the fastest growth.

Satellite and hybrid connectivity solutions are expected to grow at the fastest CAGR, providing uninterrupted visibility for deep-sea and remote maritime transit.

The pharmaceutical & healthcare segment is expected to hold the largest share, necessitated by the high value and extreme sensitivity of medical cargo.

North America is expected to dominate the market due to its advanced logistics infrastructure and early adoption of IoT technologies.

Asia Pacific is projected to witness the fastest growth, fueled by massive investments in cold chain infrastructure in China and India.

Key trends include the rapid proliferation of 'smart containers' with integrated sensor networks and advancements in energy-harvesting technologies.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency & Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Size Estimation

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Assumptions

3. Executive Summary

3.1. Market Snapshot

3.2. Segmental Summary

3.3. Regional Summary

3.4. Competitive Snapshot

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Escalating Regulatory Compliance Requirements for Sensitive Cargo

4.2.1.2. Urgent Need to Reduce Global Spoilage and Financial Loss in the Cold Chain

4.2.1.3. Rising Demand for End-to-End Visibility in High-Value Intermodal Logistics

4.2.2. Restraints

4.2.2.1. Significant Upfront Investment for Large-Scale Sensor Deployment

4.2.2.2. Challenges in Data Interoperability and Cross-Platform Integration

4.2.3. Opportunities

4.2.3.1. AI-Driven Predictive Analytics for Proactive Spoilage Prevention

4.2.3.2. Integration with Blockchain for Immutable Chain-of-Custody Records

4.2.4. Trends

4.2.4.1. Rapid Proliferation of 'Smart Containers' and Integrated Sensor Networks

4.2.4.2. Advancements in Low-Power Connectivity and Energy-Harvesting Technologies

4.3. Porter's Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Cargo Condition Monitoring Market, by Component

5.1. Hardware

5.1.1. Sensors (Temp, Humidity, Shock, Light, Pressure)

5.1.2. Telematics Gateways/Communication Units

5.1.3. Power Management Units

5.2. Software/Platform

5.2.1. Cloud-based Visibility Platforms

5.2.2. Predictive Analytics & Spoilage Models

5.2.3. Compliance & Reporting Modules

6. Global Cargo Condition Monitoring Market, by Technology

6.1. Cellular (LTE-M/NB-IoT)

6.2. Satellite Tracking

6.3. Short-Range Wireless (BLE/RFID/NFC)

6.4. Hybrid Connectivity

7. Global Cargo Condition Monitoring Market, by End User

7.1. Pharmaceutical & Healthcare

7.2. Food & Beverage

7.3. Chemical & Petrochemical

7.4. Electronics & High-Tech

7.5. Others

8. Global Cargo Condition Monitoring Market, by Geography

8.1. North America

8.1.1. U.S.

8.1.2. Canada

8.2. Europe

8.2.1. Germany

8.2.2. U.K.

8.2.3. France

8.2.4. Italy

8.2.5. Spain

8.2.6. Rest of Europe

8.3. Asia Pacific

8.3.1. China

8.3.2. Japan

8.3.3. India

8.3.4. South Korea

8.3.5. Rest of Asia Pacific

8.4. Latin America

8.4.1. Brazil

8.4.2. Argentina

8.4.3. Mexico

8.4.4. Rest of Latin America

8.5. Middle East & Africa

8.5.1. UAE

8.5.2. Saudi Arabia

8.5.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1 Overview

9.2 Key Growth Strategies

9.3 Competitive Benchmarking

9.4 Competitive Dashboard

9.4.1 Industry Leaders

9.4.2 Market Differentiators

9.4.3 Vanguards

9.4.4 Emerging Companies

9.5 Market Share/Ranking Analysis

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. Sensitech (Carrier Global)

10.2. Emerson Electric Co.

10.3. ORBCOMM Inc.

10.4. Controlant

10.5. Tive

10.6. Roambee Corporation

10.7. Arviem AG

10.8. Envirotainer

10.9. SkyCell AG

10.10. Berlinger & Co. AG

10.11. ELPRO-BUCHS AG

10.12. LogTag Recorders

10.13. DeltaTrak Inc.

10.14. OnAsset Intelligence Inc.

10.15. Monnit Corporation

10.16. Hanwell Solutions (Ellab)

10.17. Savvy Telematic Systems

10.18. Globe Tracker

10.19. Nexxiot AG

10.20. Advantech Co., Ltd.

11. Appendix

11.1. References

11.2. Disclaimer

12. Key Questions Answered

Published Date: May-2024

Published Date: Jun-2026

Subscribe to get the latest industry updates