Resources

About Us

Dangerous Goods Monitoring Market Size, Share & Trends Analysis by Component, Technology, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

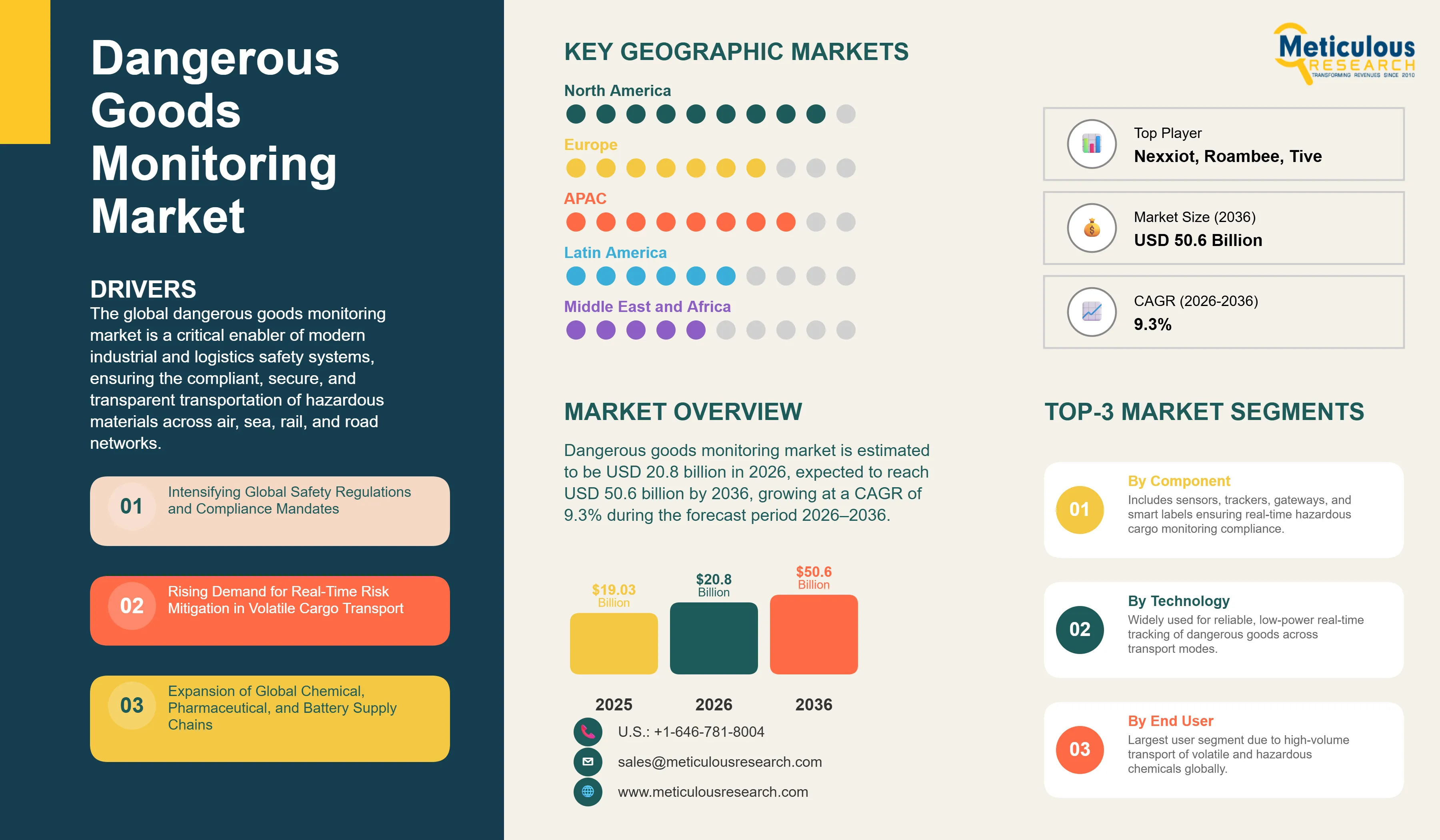

Report ID: MRAUTO - 1042061 Pages: 315 Jun-2026 Formats*: PDF Category: Automotive and Transportation Delivery: 24 to 72 Hours Download Free Sample ReportThe global dangerous goods monitoring market is estimated to be USD 20.8 billion in 2026. This market is expected to reach USD 50.6 billion by 2036, growing at a CAGR of 9.3% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global dangerous goods monitoring market is a critical enabler of modern industrial and logistics safety systems, ensuring the compliant, secure, and transparent transportation of hazardous materials across air, sea, rail, and road networks. The International Air Transport Association (IATA) reports that over 1.25 million dangerous goods consignments are transported annually by air, underscoring the scale of regulated hazardous cargo movement in global aviation. Similarly, the International Maritime Organization (IMO) regulates the transport of over 90% of global trade by sea, with the International Maritime Dangerous Goods (IMDG) Code mandating strict handling and documentation requirements for hazardous shipments.

As global supply chains increasingly handle volatile chemicals, lithium-ion batteries, flammable liquids, and radioactive substances, continuous condition monitoring has become a regulatory necessity rather than an optional safety enhancement. Dangerous goods monitoring systems leverage IoT-enabled sensors and telematics devices to track critical parameters such as temperature, shock, vibration, pressure, humidity, and gas leakage, enabling early detection of deviations that could lead to safety incidents or regulatory non-compliance.

The market is further strengthened by regulatory frameworks such as the U.S. Department of Transportation (DOT) Hazardous Materials Regulations (HMR) and the European Agreement concerning the International Carriage of Dangerous Goods by Road (ADR), both of which require strict packaging, labeling, and documentation controls. According to the United Nations Economic Commission for Europe (UNECE), ADR compliance has been adopted across 50+ countries, reflecting the global harmonization of hazardous goods transport standards.

Driven by these regulatory pressures, the proliferation of NB-IoT, LTE-M, and satellite-connected tracking systems, and the increasing complexity of multimodal logistics networks, dangerous goods monitoring platforms are evolving into integrated compliance ecosystems. These platforms not only provide real-time visibility but also automate documentation, risk alerts, and audit trails, significantly reducing incident response time and improving regulatory adherence across global supply chains.

Drivers: Strengthening Public Safety and Regulatory Compliance through Advanced Monitoring

The growth of the global dangerous goods monitoring market is primarily driven by the intensification of safety regulations and the increasing demand for real-time risk mitigation in hazardous material logistics. Global bodies such as the UNECE and IATA are continuously updating their frameworks to incorporate digital monitoring as a standard for high-risk cargo.

Intensifying Global Safety Regulations and Compliance Mandates

Regulatory frameworks like the ADR (European Agreement concerning the International Carriage of Dangerous Goods by Road) and the US DOT's PHMSA mandates are increasingly pushing for digitalized monitoring. These regulations require shippers to maintain detailed, real-time logs of hazardous cargo conditions. Advanced monitoring platforms automate the generation of dangerous goods declarations and manifests, ensuring that all transport participants have immediate access to critical safety data, thereby reducing the risk of compliance-related delays and fines.

Rising Demand for Real-Time Risk Mitigation in Volatile Cargo Transport

For volatile materials such as pressurized gases and reactive chemicals, even minor environmental excursions can lead to catastrophic failures. Real-time monitoring provides the 'situational awareness' necessary to intervene before an incident occurs. Shippers are increasingly investing in ATEX-certified sensors that provide immediate alerts for pressure build-ups or temperature spikes. This proactive approach to risk management is a powerful driver for the adoption of monitoring technology across the global chemical and energy sectors.

Restraints: High Costs of ATEX Certification and Data Security Concerns

Despite the clear benefits, the market faces challenges related to the high cost of specialized hardware and concerns over the security of sensitive transport data. Navigating the diverse certification requirements across different global jurisdictions also remains a significant hurdle.

Prohibitive Costs of Ruggedized and ATEX-Certified Hardware

Monitoring dangerous goods requires hardware that can operate safely in potentially explosive atmospheres. The engineering and certification processes for ATEX and IECEx-compliant devices are extremely costly, leading to high unit prices for sensors and trackers. For logistics providers with large fleets, the capital expenditure required for a full-scale rollout can be significant, often leading to a slower adoption rate among smaller operators or for lower-risk hazardous cargo.

Data Security and Privacy Risks in Sensitive Material Logistics

The real-time tracking of hazardous materials involves the transmission of sensitive data regarding the location and nature of dangerous cargo. This information is highly sensitive from a security and competitive standpoint. Concerns over data breaches or the unauthorized interception of tracking signals can deter some shippers from adopting cloud-based monitoring platforms. Ensuring robust, end-to-end encryption and compliance with global data privacy standards is essential for building the trust necessary for mass market adoption.

Opportunities: Integrating AI and Blockchain for Transparent and Autonomous Safety Management

The future of the dangerous goods monitoring market lies in the integration of AI for predictive safety and Blockchain for immutable compliance records. These technologies offer the potential to create self-auditing and highly resilient hazardous material supply chains.

AI-Powered Predictive Risk Analytics and Emergency Response

The integration of AI into monitoring platforms allows for the analysis of vast datasets to predict potential hazards. Machine learning models can identify patterns that precede a pressure excursion or a leak, providing early warning signals to emergency responders and transport operators. This transition from reactive monitoring to predictive safety management represents a significant growth opportunity for technology providers specializing in high-risk cargo logistics.

Blockchain for Immutable Dangerous Goods Compliance and Auditing

Blockchain technology offers a powerful solution for the challenges of dangerous goods documentation. By creating a decentralized and immutable ledger of every condition update and regulatory declaration, Blockchain ensures absolute transparency and trust among shippers, carriers, and regulators. This 'single source of truth' can significantly streamline the auditing process and reduce the administrative burden of hazardous material transport, offering a major opportunity for platform developers

Adoption of Disposable Smart Labels for Hazardous Package Monitoring

A key trend in 2026 is the rapid adoption of low-cost disposable smart labels and thin-film sensors for package-level monitoring of dangerous goods. These labels integrate temperature, shock, and sometimes humidity sensing into ultra-thin formats, enabling per-parcel visibility at scale, which was previously economically unviable for bulk deployments. This shift is strongly aligned with regulatory and operational pressures in high-risk verticals. The International Air Transport Association (IATA) reports that over 1.25 million dangerous goods consignments are transported by air annually, with pharmaceuticals and lithium-ion batteries representing a fast-growing share of regulated cargo requiring strict condition control. In parallel, the European Federation of Pharmaceutical Industries and Associations (EFPIA) highlights that temperature excursions remain one of the leading causes of pharmaceutical shipment losses, reinforcing demand for single-use monitoring solutions. In pharmaceuticals and specialty chemicals, these disposable sensors are increasingly used to support compliance with Good Distribution Practice (GDP) guidelines (EU GDP framework), which require continuous temperature integrity assurance across the supply chain. The declining cost of printed electronics and NB-IoT-enabled trackers is accelerating adoption from pallet-level to individual shipment-level monitoring, significantly improving traceability and reducing compliance risk.

Convergence of Multi-Modal Monitoring into Unified Visibility Platforms

Another major structural shift is the convergence of road, rail, air, and maritime dangerous goods monitoring into unified end-to-end visibility platforms. Traditionally, monitoring systems operated in silos due to fragmented carrier systems and differing regulatory regimes. However, global shippers now increasingly demand a single digital control layer for hazardous cargo visibility across all transport modes. This transition is strongly influenced by global regulatory harmonization efforts such as the International Maritime Dangerous Goods (IMDG) Code by the International Maritime Organization (IMO) and the UNECE ADR framework, which governs road transport of dangerous goods across more than 50 countries. Similarly, IATA’s Cargo-XML and e-Freight initiatives have accelerated digital standardization in air cargo documentation and tracking. From an operational standpoint, intermodal complexity is increasing as global trade becomes more containerized and time-sensitive. According to the World Trade Organization (WTO), over 80% of global merchandise trade by volume is transported by sea, making maritime visibility integration essential for end-to-end hazardous material tracking. This has driven adoption of cloud-based control towers and IoT-enabled logistics platforms that unify sensor data, compliance documentation, and incident alerts into a single dashboard. As a result, dangerous goods monitoring is evolving from fragmented tracking tools into integrated compliance intelligence ecosystems, enabling real-time risk mitigation and automated regulatory reporting across the entire logistics chain.

Analysis by Component

Based on component, the **hardware segment** is expected to hold the largest share of the global dangerous goods monitoring market in 2026. This dominance is primarily due to the mandatory requirement for specialized, ruggedized, and ATEX-certified monitoring devices (sensors, trackers, gateways) to operate safely in hazardous environments. Hardware remains the primary revenue generator as global logistics providers invest heavily in equipping their fleets with compliant IoT infrastructure. However, the **software & platforms segment** is projected to register the highest CAGR during the forecast period. The market is rapidly shifting toward 'Compliance-as-a-Service' models, where the value lies in the platform's ability to automate regulatory documentation, provide predictive risk analytics, and ensure end-to-end visibility. The increasing demand for integrated safety management systems that can handle complex global dangerous goods regulations is a key driver for this segment's rapid growth.

Analysis by Technology

By technology, the **cellular (LTE-M/NB-IoT)** segment is expected to hold the largest share in 2026. Cellular connectivity provides the most reliable and cost-effective real-time tracking for the majority of land-based and near-shore hazardous material transport. Its established global roaming infrastructure makes it the default choice for large-scale dangerous goods monitoring. However, the **satellite & hybrid connectivity segment** is projected to grow at the fastest CAGR during the forecast period. The demand for 'zero-gap' visibility during transcontinental and deep-sea maritime transit is driving the adoption of hybrid devices. These systems intelligently switch between cellular and satellite networks to ensure continuous monitoring of hazardous cargo, regardless of its location, which is increasingly required by international maritime safety standards.

Analysis by End User

By end user, the **chemical & petrochemical segment** is expected to hold the largest share in 2026. This leadership is driven by the high volume and inherent risks associated with transporting volatile chemicals and petroleum products. Stringent safety mandates (e.g., Cefic's SQAS, US DOT PHMSA) necessitate extensive monitoring infrastructure for this sector. However, the **pharmaceutical & healthcare segment** is projected to register the highest CAGR during the forecast period. The rapid growth in the transport of hazardous medical supplies, including radioactive isotopes and temperature-sensitive biological samples, is a major driver. Strict GxP compliance and the need for continuous environmental monitoring to ensure product efficacy and public safety are pushing healthcare providers to adopt advanced dangerous goods monitoring solutions.

Geographic Analysis: North American Dominance and Asia-Pacific's Rapid Expansion in Hazardous Material Monitoring

Largest Share: North America

North America is expected to dominate the global dangerous goods monitoring market in 2026, holding a market share of around 38%. This leading position is attributed to the region's mature regulatory framework (e.g., PHMSA, US DOT), the presence of major global chemical producers, and the early adoption of advanced IoT technologies for supply chain security. The region's extensive intermodal networks for hazardous materials drive significant demand for integrated monitoring solutions. The key companies operating in the North America market are Sensitech (Carrier Global), ORBCOMM Inc., Roambee Corporation, and Honeywell International Inc.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global dangerous goods monitoring market, with a CAGR of 11.5% during the forecast period. This rapid expansion is fueled by the massive expansion of the chemical and electronics manufacturing sectors in China, India, and Southeast Asia. Increasing regional trade and the modernization of transport infrastructure to meet international safety standards (e.g., IATA, IMO) are driving rapid adoption of digital monitoring tools. The key companies operating in the Asia Pacific market are Yokogawa Electric Corporation, and various regional technology integrators for global players.

The global dangerous goods monitoring market is characterized by a strong focus on technical innovation and regulatory compliance. Key players are investing heavily in developing ATEX-certified hardware and integrated software platforms that can handle the complexities of global hazardous material regulations. Strategic partnerships between technology providers and global logistics firms are common as they seek to create end-to-end, multi-modal monitoring solutions. Furthermore, there is an increasing emphasis on data security and the integration of AI to provide predictive risk analytics, moving the industry from reactive monitoring to proactive safety management.

Sensitech (Carrier), ORBCOMM, Nexxiot, Roambee, Tive, Savvy Telematic Systems, Globe, Tracker, Arviem, Honeywell, Emerson, ABB, Siemens, Yokogawa, Endress+Hauser, SGS, Intertek, Bureau Veritas, Labelmaster (DGeo), Samsara, Identec Solutions

The global market is estimated at USD 20.8 billion in 2026, with a projected growth to USD 50.6 billion by 2036, at a CAGR of 9.3%.

Primary drivers include intensifying global safety regulations (e.g., ADR, PHMSA) and the rising demand for real-time risk mitigation in volatile cargo transport.

Major restraints include the high costs of ATEX-certified hardware and concerns over data security and privacy in sensitive material logistics.

Opportunities lie in AI-powered predictive risk analytics and the integration of Blockchain for immutable compliance records.

The hardware segment is expected to hold the largest share due to the mandatory requirement for specialized, ruggedized monitoring devices.

The satellite and hybrid connectivity segment is projected to grow at the fastest CAGR, ensuring 'zero-gap' visibility for transcontinental transit.

The chemical & petrochemical segment is expected to hold the largest share, necessitated by the high volume and risks of hazardous material transport.

North America is expected to dominate the market due to its mature regulatory framework and early adoption of advanced IoT technologies.

Asia Pacific is projected to witness the fastest growth, fueled by the expansion of chemical and electronics manufacturing in China and India.

Key trends include the adoption of disposable smart labels for package-level monitoring and the convergence of multi-modal monitoring into unified platforms.

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Jun-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates