Resources

About Us

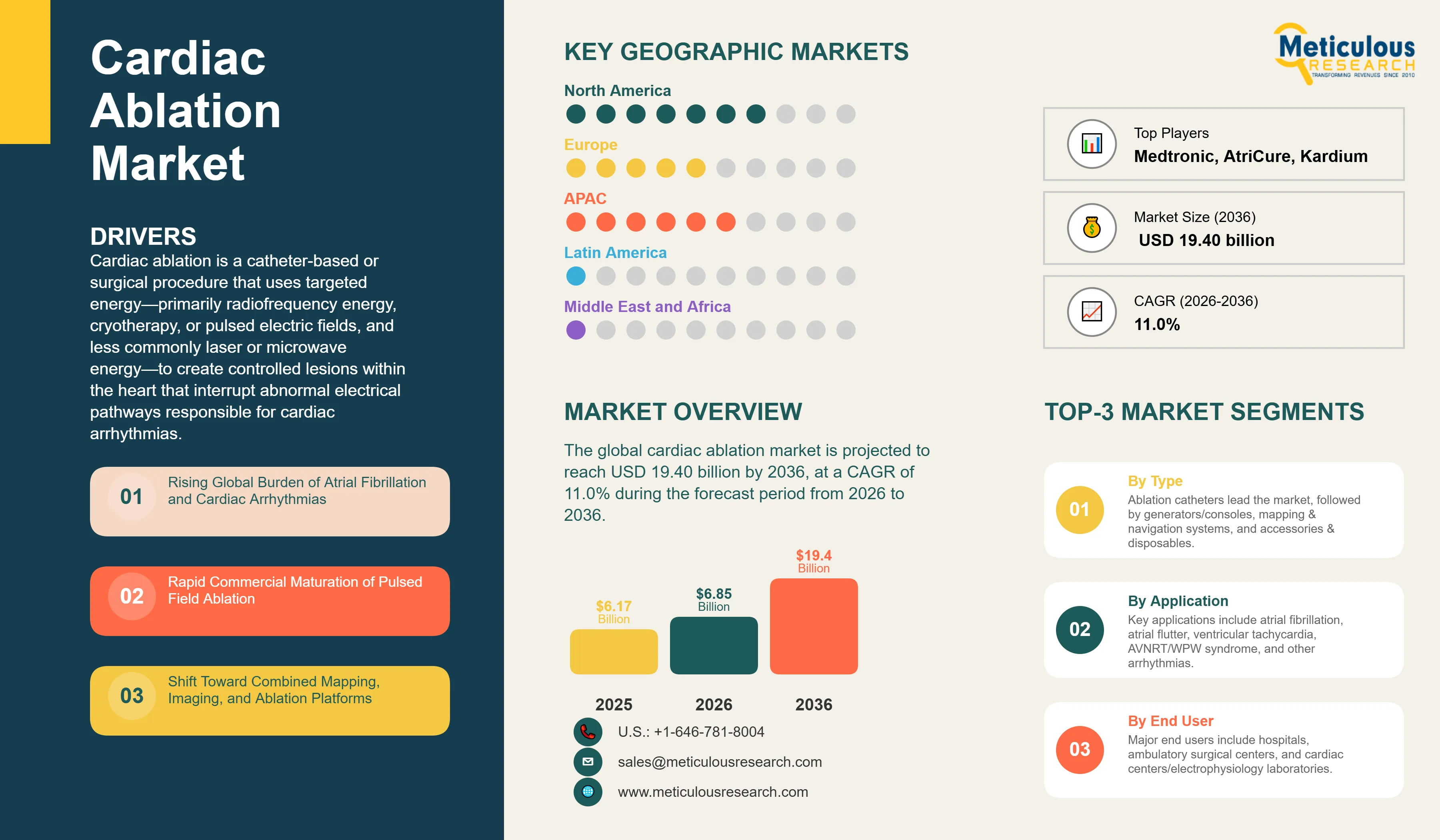

The global cardiac ablation market is projected to reach USD 19.40 billion by 2036 from an estimated USD 6.85 billion in 2026, at a CAGR of 11.0% during the forecast period from 2026 to 2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Cardiac ablation is a catheter-based or surgical procedure that uses targeted energy—primarily radiofrequency energy, cryotherapy, or pulsed electric fields, and less commonly laser or microwave energy—to create controlled lesions within the heart that interrupt abnormal electrical pathways responsible for cardiac arrhythmias. The market comprises ablation catheters, generators and consoles, three-dimensional mapping and navigation systems, and procedure-related accessories and disposables that together enable complete cardiac ablation procedures and form the technological foundation of modern electrophysiology practice.

Demand for these systems closely follows the global burden of cardiac arrhythmias, particularly atrial fibrillation (AF), which continues to rise worldwide. An estimated 52.55 million individuals were living with atrial fibrillation and atrial flutter globally in 2021, representing a 137% increase compared with 1990, while adults aged over 40 years face an approximately 25% lifetime risk of developing AF. The expanding prevalence of arrhythmias, supported by population aging, improved diagnosis, and increasing cardiovascular risk factors, is expected to sustain procedural volumes throughout the forecast period.

Technological innovation continues to reshape the market. Pulsed field ablation (PFA), which uses high-voltage electrical pulses to selectively ablate myocardial tissue while minimizing injury to adjacent structures such as the esophagus and phrenic nerve, has rapidly progressed from early commercialization into one of the fastest-growing segments of cardiac electrophysiology. At the same time, advanced three-dimensional electroanatomical mapping, intracardiac echocardiography integration, contact-force sensing, and artificial intelligence-assisted workflow optimization are enhancing procedural precision, efficiency, and safety, increasing the strategic importance of software and imaging platforms alongside ablation catheters.

The delivery of cardiac ablation procedures is also evolving. Hospitals remain the primary care setting because of their ability to support complex electrophysiology laboratories and manage high-risk patients; however, an increasing proportion of procedures is being performed in ambulatory surgical centers and specialized cardiac centers as technologies become faster, safer, and more efficient. Collectively, the growing global burden of arrhythmias, continued adoption of pulsed field ablation, ongoing advances in mapping and imaging technologies, and the gradual shift toward lower-cost outpatient care settings are expected to drive sustained double-digit growth in the global cardiac ablation market over the coming decade.

"Pulsed field ablation has moved from a promising concept to a standard-of-care option in a remarkably short window. Electrophysiologists are drawn to the combination of shorter procedure times and a differentiated safety profile compared with thermal energy sources."

– Director of Electrophysiology, Multi-Hospital Cardiovascular Program

"Health systems are no longer buying a catheter in isolation. They are evaluating an entire ecosystem, mapping, imaging, and navigation, that needs to work together to shorten procedures and improve first-pass success."

– Vice President, Cardiac Rhythm Management Solutions Provider

"The competitive intensity in pulsed field ablation has been unlike anything we've seen in electrophysiology. Every major player now has a commercial platform, and the differentiation battle has shifted to catheter design, mapping integration, and procedural workflow."

– Chief Medical Officer, Regional Cardiovascular Care Network

Rising Global Burden of Atrial Fibrillation and Cardiac Arrhythmias

The primary driver of the cardiac ablation market is the steady increase in the number of patients with cardiac arrhythmias who become candidates for interventional treatment. As populations age, the prevalence of atrial fibrillation (AF), the most common sustained cardiac arrhythmia, continues to rise, while associated risk factors such as hypertension, obesity, diabetes, heart failure, and chronic kidney disease further contribute to disease burden. In Europe, the number of individuals living with AF and atrial flutter is projected to reach 8.8–18 million by 2060, while the prevalence of AF in the United States is expected to continue increasing substantially over the coming decades. As a growing proportion of diagnosed AF patients become eligible for rhythm-control strategies when pharmacological therapy proves inadequate or is poorly tolerated, the expanding patient population is expected to provide a sustained and long-term source of demand for cardiac ablation procedures and associated technologies.

Rapid Commercial Maturation of Pulsed Field Ablation

A second major growth driver is the rapid commercialization of pulsed field ablation (PFA), which has evolved from an emerging technology into one of the most competitive segments of the cardiac electrophysiology market. Boston Scientific Corporation received U.S. FDA approval for its FARAPULSE™ Pulsed Field Ablation System in January 2024, and within a short period the technology achieved rapid adoption across the United States and Europe while also expanding into China and Japan. By 2026, more than 200,000 patients had been treated using the FARAPULSE platform, demonstrating strong physician acceptance and accelerating the transition toward non-thermal ablation technologies. Subsequently, Abbott Laboratories received FDA approval for its Volt™ Pulsed Field Ablation System in December 2025, joining Medtronic plc, Boston Scientific Corporation, and Johnson & Johnson MedTech in the rapidly expanding U.S. PFA market. The near-simultaneous commercialization of PFA platforms by the industry's leading electrophysiology companies is accelerating technology replacement cycles, increasing hospital investment in next-generation electrophysiology systems, and intensifying competition across the global cardiac ablation market.

Shift Toward Combined Mapping, Imaging, and Ablation Platforms

A third driver is the move toward fully integrated electrophysiology platforms rather than standalone catheters. Johnson & Johnson has introduced its CARTOSOUND SONATA Module, which uses artificial intelligence with the CARTO System to automatically transform intracardiac echocardiography images into detailed maps, allowing physicians to build accurate models of multiple heart chambers, illustrating how vendors are bundling ablation energy, navigation, and imaging into a single procedural workflow. Hospitals evaluating new electrophysiology investments increasingly weigh the full platform, not the catheter in isolation, which favors vendors with mapping, imaging, and ablation capabilities under one roof.

Expansion of Ambulatory and Dedicated Cardiac Center Capacity

A significant opportunity lies in the shift of ablation procedures toward ambulatory surgical centers and dedicated cardiac/electrophysiology centers. As pulsed field ablation and improved catheter designs shorten procedure times and reduce complication rates, more cases that once required an overnight hospital stay can be performed in outpatient settings. This shift is particularly relevant in the United States, where payers are increasingly supportive of site-of-care migration for lower-risk arrhythmia procedures, and it opens the ablation market to a broader set of buyers beyond large tertiary hospitals.

Untapped Demand in Asia-Pacific and Latin America

Emerging markets represent a substantial growth opportunity. Electrophysiology lab infrastructure remains comparatively underdeveloped across much of Asia-Pacific and Latin America relative to procedure-eligible patient populations, and rising healthcare investment in these regions is expanding access to ablation therapy. As leading manufacturers extend regulatory approvals and distribution into these markets, following the same sequence seen in pulsed field ablation's rollout across China and Japan, this white space is expected to become an increasingly important contributor to global volume growth.

By Product Type: Ablation Catheters Lead the Market in 2026

By product type, the market is segmented into ablation catheters, generators/consoles, and mapping and navigation systems. Ablation catheters are expected to account for the largest share of the market in 2026, reflecting their nature as a per-procedure consumable that is replaced with every case, unlike capital equipment which is purchased once and used across many procedures. Mapping and navigation systems are projected to register strong growth as integrated, AI-assisted platforms become a standard part of new electrophysiology lab builds.

By Technology: Radiofrequency Ablation Leads, Pulsed Field Ablation Grows Fastest

By technology, the market spans radiofrequency ablation, cryoablation, pulsed field ablation, and microwave/laser ablation. Radiofrequency ablation holds the largest share in 2026, supported by decades of clinical precedent and its status as a default choice across many arrhythmia types beyond atrial fibrillation. Pulsed field ablation is projected to grow the fastest by a wide margin, having expanded from a single commercial vendor to four major competitors within roughly two years of its first U.S. approval.

By Approach: Catheter-based Ablation Leads the Market in 2026

By approach, the market is divided into catheter-based and surgical ablation. Catheter-based procedures hold the dominant share given their minimally invasive nature, shorter recovery time, and lower procedural trauma relative to surgical Maze-type procedures, which are typically reserved for patients undergoing concurrent open-heart surgery.

By Application: Atrial Fibrillation Leads the Market in 2026

By application, the market includes atrial fibrillation, atrial flutter, ventricular tachycardia, and AVNRT/WPW syndrome. Atrial fibrillation accounts for the largest share in 2026, consistent with its position as the most common sustained cardiac arrhythmia and the leading indication for ablation referral globally.

By End User: Hospitals Lead the Market in 2026

By end user, the market covers hospitals, ambulatory surgical centers, and cardiac centers/electrophysiology labs. Hospitals hold the largest share in 2026, supported by their capacity to run advanced mapping suites and manage procedural complications. Ambulatory surgical centers and dedicated cardiac centers are expected to grow the fastest as procedure times shorten and site-of-care shifts continue.

North America Leads the Market in 2026

By region, the global cardiac ablation market spans North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America holds the largest share in 2026, supported by high procedure volumes, favorable reimbursement for electrophysiology interventions, and the fastest pace of pulsed field ablation adoption among the major device makers. The United States is the dominant national market, reflecting its role as the first launch market for nearly every major ablation platform.

Asia-Pacific is expected to record the fastest growth over the forecast period, driven by expanding electrophysiology lab infrastructure, rising diagnosis rates for atrial fibrillation, and the phased extension of pulsed field ablation approvals into China and Japan. Europe remains an important market, supported by strong adoption of next-generation ablation platforms and an active clinical research base presenting data at meetings such as the European Heart Rhythm Association congress.

Leading companies in the market have grown through new product launches, regulatory approvals, clinical data generation, and strategic acquisitions of smaller pulsed field ablation and mapping specialists. Securing regulatory clearance for pulsed field platforms, expanding integrated mapping and imaging capabilities, and presenting late-breaking clinical data at major electrophysiology congresses have been the most common ways players have strengthened their position through 2026.

Prominent companies active in the global cardiac ablation market include Medtronic plc (Ireland), Johnson & Johnson MedTech (U.S.), Abbott Laboratories (U.S.), Boston Scientific Corporation (U.S.), MicroPort Scientific Corporation (China), BIOTRONIK SE & Co. KG (Germany), AtriCure, Inc. (U.S.), Japan Lifeline Co., Ltd. (Japan), Stereotaxis, Inc. (U.S.), CardioFocus, Inc. (U.S.), Kardium Inc. (Canada), Adagio Medical Holdings, Inc. (U.S.), Acutus Medical, Inc. (U.S.), CathRx Ltd. (Australia), Imricor Medical Systems, Inc. (U.S.).

|

Particulars |

Details |

|

Forecast Period |

2026 to 2036 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

CAGR (Value) |

11.0% |

|

Market Size (Value) in 2026 |

USD 6.85 Billion* |

|

Market Size (Value) in 2036 |

USD 19.40 Billion* |

|

Segments Covered |

By Product Type: Ablation Catheters, Generators/Consoles, Mapping & Navigation Systems, Accessories |

|

Countries Covered |

North America (U.S., Canada), Europe (Germany, U.K., France, Italy, Spain, and Rest of Europe), Asia-Pacific (Japan, China, India, South Korea, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and the Middle East & Africa (Saudi Arabia, UAE, South Africa, and Rest of Middle East & Africa) |

|

Key Companies |

Medtronic plc (Ireland), Johnson & Johnson MedTech (U.S.), Abbott Laboratories (U.S.), Boston Scientific Corporation (U.S.), MicroPort Scientific Corporation (China), BIOTRONIK SE & Co. KG (Germany), AtriCure, Inc. (U.S.), Japan Lifeline Co., Ltd. (Japan), Stereotaxis, Inc. (U.S.), CardioFocus, Inc. (U.S.), Kardium Inc. (Canada), Adagio Medical Holdings, Inc. (U.S.), Acutus Medical, Inc. (U.S.), CathRx Ltd. (Australia), Imricor Medical Systems, Inc. (U.S.) |

The global cardiac ablation market size is estimated at USD 6.85 billion in 2026 (directional, pending internal model validation).

The market is projected to grow from USD 6.85 billion in 2026 to USD 19.40 billion by 2036, at a CAGR of 11.0%.

Key players include Medtronic plc, Johnson & Johnson MedTech (Biosense Webster), Abbott Laboratories, Boston Scientific Corporation, MicroPort Scientific Corporation, BIOTRONIK SE & Co. KG, AtriCure, Inc., and others.

The rapid commercial expansion of pulsed field ablation from a single vendor to four major competitors within roughly two years, and the integration of AI-assisted mapping and imaging into ablation platforms, are the most prominent trends.

In 2026, ablation catheters lead by product type, radiofrequency ablation leads by technology, catheter-based procedures lead by approach, atrial fibrillation leads by application, and hospitals lead by end user. Pulsed field ablation systems and ambulatory/cardiac centers are among the fastest-growing segments.

North America holds the largest share of the market in 2026, supported by high procedure volumes and rapid pulsed field ablation adoption. Asia-Pacific is expected to record the highest growth rate over the forecast period, driven by expanding electrophysiology infrastructure.

Key drivers include the rising global burden of atrial fibrillation, the rapid commercial maturation of pulsed field ablation, and the shift toward integrated mapping, imaging, and ablation platforms.

1. Introduction

1.1. Market Definition

1.2. Currency & Limitations

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.2. Bottom-Up Approach

2.3.3. Top-Down Approach

2.3.4. Growth Forecast

2.4. Assumptions for the Study

3. Executive Summary

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Rising Global Burden of Atrial Fibrillation and Cardiac Arrhythmias

4.2.1.2. Rapid Commercial Maturation of Pulsed Field Ablation

4.2.1.3. Shift Toward Combined Mapping, Imaging, and Ablation Platforms

4.2.2. Restraints

4.2.2.1. High Cost of Advanced Ablation Systems and Procedures

4.2.3. Opportunities

4.2.3.1. Expansion of Ambulatory and Dedicated Cardiac Center Capacity

4.2.3.2. Untapped Demand in Asia-Pacific and Latin America

4.2.4. Challenges

4.2.4.1. Reimbursement Variability Across Geographies

4.2.4.2. Shortage of Trained Electrophysiologists

4.3. Key Trends

4.3.1. Intensifying Competition in Pulsed Field Ablation

4.3.2. Convergence of Ablation, Mapping, and Intracardiac Imaging

4.4. Vendor Selection Criteria/Factors Influencing Purchase Decisions

4.5. Use Cases

4.6. Porter's Five Forces Analysis

4.6.1. Bargaining Power of Buyers: Moderate

4.6.2. Bargaining Power of Suppliers: Moderate to High

4.6.3. Threat of Substitutes: Low to Moderate

4.6.4. Threat of New Entrants: Moderate

4.6.5. Degree of Competition: High

4.7. Value Chain Analysis

4.8. Pricing Analysis

4.9. Technology Analysis

4.10. Regulatory Landscape (U.S. FDA, EU MDR, China NMPA)

4.11. Pestel Analysis

5. Cardiac Ablation Market Assessment—By Product Type

5.1. Overview

5.2. Ablation Catheters

5.3. Generators/Consoles

5.4. Mapping & Navigation Systems

5.5. Accessories & Disposables

6. Cardiac Ablation Market Assessment—By Technology and Approach

6.1. Overview

6.2. Radiofrequency Ablation

6.3. Cryoablation

6.4. Pulsed Field Ablation

6.5. Microwave/Laser Ablation

6.6. Catheter-based Ablation

6.7. Surgical Ablation

7. Cardiac Ablation Market Assessment—By Application

7.1. Overview

7.2. Atrial Fibrillation

7.3. Atrial Flutter

7.4. Ventricular Tachycardia

7.5. AVNRT and WPW Syndrome

7.6. Other Arrhythmias

8. Cardiac Ablation Market Assessment—By End User

8.1. Overview

8.2. Hospitals

8.3. Ambulatory Surgical Centers

8.4. Cardiac Centers/Electrophysiology Labs

9. Cardiac Ablation Market Assessment—By Geography

9.1. Overview

9.2. North America

9.2.1. United States

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. United Kingdom

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia Pacific

9.4.1. Japan

9.4.2. China

9.4.3. India

9.4.4. South Korea

9.4.5. Australia & New Zealand

9.4.6. Rest of Asia Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

9.6.1. Saudi Arabia

9.6.2. United Arab Emirates

9.6.3. South Africa

9.6.4. Rest of Middle East & Africa

10. Competitive Landscape

10.1. Introduction

10.2. Key Growth Strategies

10.3. Competitive Benchmarking

10.4. Competitive Dashboard

10.4.1. Industry Leaders

10.4.2. Market Differentiators

10.4.3. Vanguards

10.4.4. Emerging Companies

10.5. Market Share/Position Analysis

11. Company Profiles (Company Overview, Financial Overview, Product Portfolio, Strategic Developments)

11.1. Medtronic plc (Ireland)

11.2. Johnson & Johnson MedTech (U.S.)

11.3. Abbott Laboratories (U.S.)

11.4. Boston Scientific Corporation (U.S.)

11.5. MicroPort Scientific Corporation (China)

11.6. BIOTRONIK SE & Co. KG (Germany)

11.7. AtriCure, Inc. (U.S.)

11.8. Japan Lifeline Co., Ltd. (Japan)

11.9. Stereotaxis, Inc. (U.S.)

11.10. CardioFocus, Inc. (U.S.)

11.11. Kardium Inc. (Canada)

11.12. Adagio Medical Holdings, Inc. (U.S.)

11.13. Acutus Medical, Inc. (U.S.)

11.14. CathRx Ltd. (Australia)

11.15. Imricor Medical Systems, Inc. (U.S.)

12. Appendix

12.1. Available Customization

12.2. Related Reports

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Feb-2026

Published Date: Jan-2025

Subscribe to get the latest industry updates