Resources

About Us

Cardiac Pacemaker Devices Market by Product (Implantable Pacemakers [Dual Chamber, CRT Pacemaker], External Pacemaker, Pacing Leads), Indication (Arrhythmia, CHF), End User (Hospitals & Clinics, Ambulatory Care Centers) – Forecast to 2036

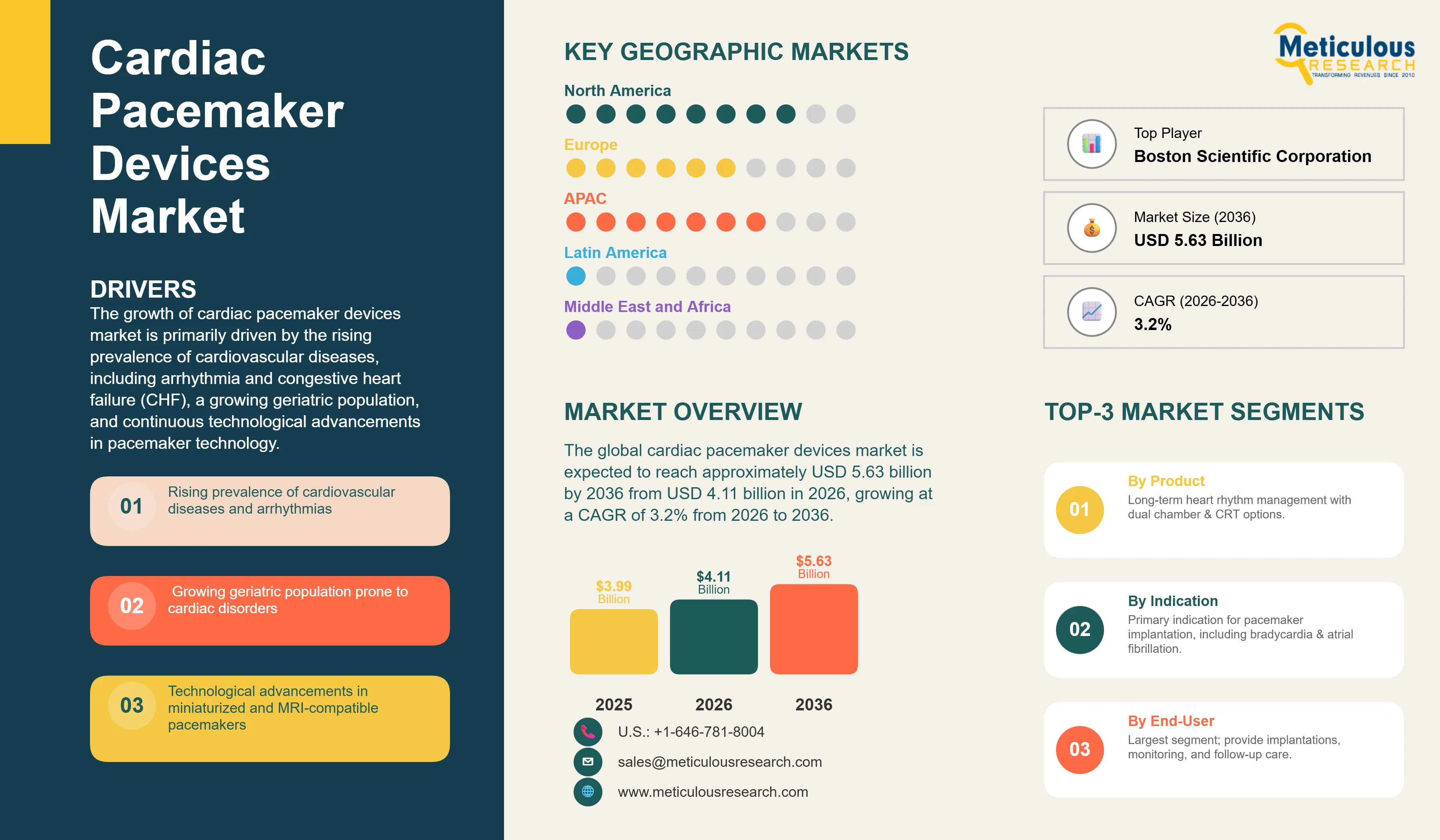

Report ID: MRHC - 10464 Pages: 200 Feb-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 48 Hours Download Free Sample ReportThe global cardiac pacemaker devices market was valued at approximately USD 3.99 billion in 2025. This market is expected to reach approximately USD 5.63 billion by 2036 from USD 4.11 billion in 2026, growing at a CAGR of 3.2% from 2026 to 2036. The growth of this market is primarily driven by the rising prevalence of cardiovascular diseases, including arrhythmia and congestive heart failure (CHF), a growing geriatric population, and continuous technological advancements in pacemaker technology. For instance, the development of leadless pacemakers and devices with remote monitoring capabilities has significantly improved patient outcomes and expanded the market potential.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global cardiac pacemaker devices market encompasses a range of medical devices designed to regulate the heart's rhythm by delivering electrical impulses to the heart muscle. These devices are critical for patients suffering from bradycardia, arrhythmia, and other heart rhythm disorders. The market includes implantable pacemakers, such as dual-chamber and cardiac resynchronization therapy (CRT) pacemakers, as well as external pacemakers and pacing leads.

The market is characterized by a high degree of technological innovation, with leading manufacturers continuously developing smaller, more efficient, and longer-lasting devices. The introduction of leadless pacemakers, such as Medtronic's Micra Transcatheter Pacing System, has revolutionized the market by offering a minimally invasive alternative to traditional pacemakers. These devices are implanted directly into the heart, eliminating the need for pacing leads and reducing the risk of complications.

Remote monitoring capabilities have also become a standard feature in modern pacemakers, allowing healthcare providers to monitor patients' heart rhythms and device performance remotely. This has improved patient care and reduced the need for frequent in-person follow-up appointments. The American Heart Association (AHA) and the European Society of Cardiology (ESC) have both issued guidelines that support the use of remote monitoring for patients with cardiac implantable electronic devices (CIEDs).

What are the Key Trends in the Cardiac Pacemaker Devices Market?

Development of Leadless Pacemakers

The shift toward leadless pacemakers represents one of the most transformative technological trends in the cardiac pacemaker market. Unlike traditional transvenous systems, leadless devices are self-contained units implanted directly into the right ventricle, eliminating leads and surgical pockets, the two major sources of long-term complications in conventional pacemakers. This design significantly reduces risks associated with lead fracture, venous obstruction, pocket infections, and device erosion.

Clinical adoption is increasing as long-term data demonstrate favorable safety and performance outcomes. For instance, the Abbott Laboratories Aveir VR leadless pacemaker features retrievability and extended battery longevity, addressing earlier limitations of leadless systems. Similarly, the Medtronic plc Micra™ AV enables atrioventricular (AV) synchrony using accelerometer-based sensing, expanding the eligible patient population beyond single-chamber pacing candidates. These innovations are particularly valuable for elderly patients, those with limited venous access, and individuals at high risk of infection, thereby supporting broader procedural adoption in both developed and emerging healthcare markets.

Integration of Remote Monitoring and Connectivity

The incorporation of remote patient monitoring (RPM) and wireless connectivity into pacemaker systems is reshaping post-implantation care models. Modern pacemakers now enable continuous transmission of device diagnostics, arrhythmia burden data, and battery status to clinicians, allowing proactive intervention and reducing the need for routine in-person follow-ups.

This trend is reinforced by growing clinical evidence linking remote monitoring with improved patient outcomes and reduced hospitalization rates. Platforms such as Boston Scientific Corporation LATITUDE NXT Remote Patient Management System and BIOTRONIK SE & Co. KG Home Monitoring Service exemplify this evolution, offering automated alerts for arrhythmic events, lead performance issues, and device integrity concerns. These systems align with guideline-based recommendations advocating continuous device surveillance to optimize therapy effectiveness.

Additionally, integration with smartphone applications and cloud-based ecosystems is enhancing patient engagement and supporting value-based healthcare models, where continuous monitoring helps reduce readmissions and long-term care costs.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 5.63 Billion |

|

Market Size in 2026 |

USD 4.11 Billion |

|

Market Size in 2025 |

USD 3.99 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 3.2% |

|

Dominating Product |

Implantable Pacemakers |

|

Fastest Growing Product |

Leadless Pacemakers |

|

Largest Indication Segment |

Arrhythmia |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Drivers: Rising Prevalence of Cardiovascular Diseases

The increasing prevalence of cardiovascular diseases, particularly arrhythmias and congestive heart failure, is a primary driver of the cardiac pacemaker market. According to the World Health Organization (WHO), cardiovascular diseases are the leading cause of death globally, taking an estimated 17.9 million lives each year. The growing geriatric population, which is more susceptible to heart rhythm disorders, further contributes to the demand for pacemakers.

Opportunity: Growing Demand for Minimally Invasive Procedures

The growing demand for minimally invasive surgical procedures is creating significant opportunities for manufacturers of leadless pacemakers and other advanced cardiac devices. Patients and healthcare providers are increasingly opting for less invasive treatment options that offer faster recovery times, reduced risk of complications, and improved cosmetic outcomes. This trend is expected to drive the adoption of leadless pacemakers and other innovative cardiac devices in the coming years.

Why Do Implantable Pacemakers Dominate the Market?

Based on product, the implantable pacemakers segment is expected to account for the largest share of the market, in 2026. This dominance is attributed to the long-term efficacy and reliability of these devices in managing chronic heart rhythm disorders. The development of dual-chamber and CRT pacemakers has further expanded the therapeutic applications of implantable pacemakers, allowing for more physiological pacing and improved outcomes for patients with heart failure.

How Does the Arrhythmia Segment Lead the Market?

The arrhythmia segment is expected to account for the largest share of the market by indication, in 2026. Arrhythmias, including bradycardia and atrial fibrillation, are the most common indications for pacemaker implantation. The rising prevalence of these conditions, coupled with the growing awareness among patients and healthcare providers about the benefits of pacemaker therapy, is driving the growth of this segment.

How is North America Maintaining Its Leadership?

North America is projected to account for the largest share of the global cardiac pacemaker devices market throughout the forecast period. The large share of this region is primarily driven by the high prevalence of cardiovascular diseases, including arrhythmias and heart failure, which continue to increase with the aging population. In addition, North America benefits from a well-established healthcare infrastructure, advanced electrophysiology centers, and strong clinical expertise in cardiac device implantation procedures.

Favorable reimbursement frameworks and widespread insurance coverage further support patient access to implantable cardiac devices, encouraging the adoption of technologically advanced pacemaker systems. Early uptake of innovations such as MRI-compatible pacemakers, leadless pacing technologies, and remote monitoring platforms also strengthens regional demand. Moreover, the strong presence of leading manufacturers, including Medtronic plc, Abbott Laboratories, and Boston Scientific Corporation, supports continuous product innovation, clinical research, and physician training, further strengthening its dominant market position.

Which Regions Are Experiencing Rapid Growth?

Asia-Pacific is expected to register the fastest growth in the global cardiac pacemaker devices market during the forecast period. This is mainly attributed to the rising burden of cardiovascular diseases, a large and rapidly aging population, and improving diagnosis and treatment rates. Increasing healthcare expenditure, expansion of hospital infrastructure, and government initiatives to enhance access to advanced cardiac care are also contributing to market growth.

Greater awareness of minimally invasive cardiac procedures and increasing adoption of implantable cardiac devices are accelerating demand across the region. Major economies such as China and India are anticipated to serve as key growth engines due to their large patient pools, expanding private healthcare sectors, and rising investments in medical technology. Additionally, the growing presence of regional manufacturers and improving affordability of cardiac devices are further supporting market penetration.

The global cardiac pacemaker devices market is moderately consolidated, with competition focused on technological innovation, device reliability, and expanded service capabilities. Key companies profiled in this report include Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, BIOTRONIK SE & Co. KG, LivaNova PLC, MicroPort Scientific Corporation, and Lepu Medical Technology. These companies focus on product innovation, expansion of leadless and MRI-compatible device portfolios, and integration of remote monitoring solutions to strengthen their competitive positions.

The global lateral flow assays market is valued at USD 13.7 billion in 2026 and is expected to reach approximately USD 27.4 billion by 2036.

The market is expected to grow at a CAGR of 7.9% from 2026 to 2036.

The key players include Abbott Laboratories, F. Hoffmann-La Roche AG, Becton Dickinson and Company, Siemens Healthineers AG, Thermo Fisher Scientific, Inc., and others.

The main factors include the benefits of LFA-based rapid tests, increasing usage of home-based lateral flow assays, growing demand for point-of-care testing, and the growing prevalence of chronic and infectious diseases.

North America is expected to maintain leadership, while Asia-Pacific is projected to experience the fastest growth during the forecast period.

Published Date: Jul-2026

Published Date: Jun-2026

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates