Resources

About Us

Endometrial Ablation Devices Market Size, Share & Trends Analysis by Device Type, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

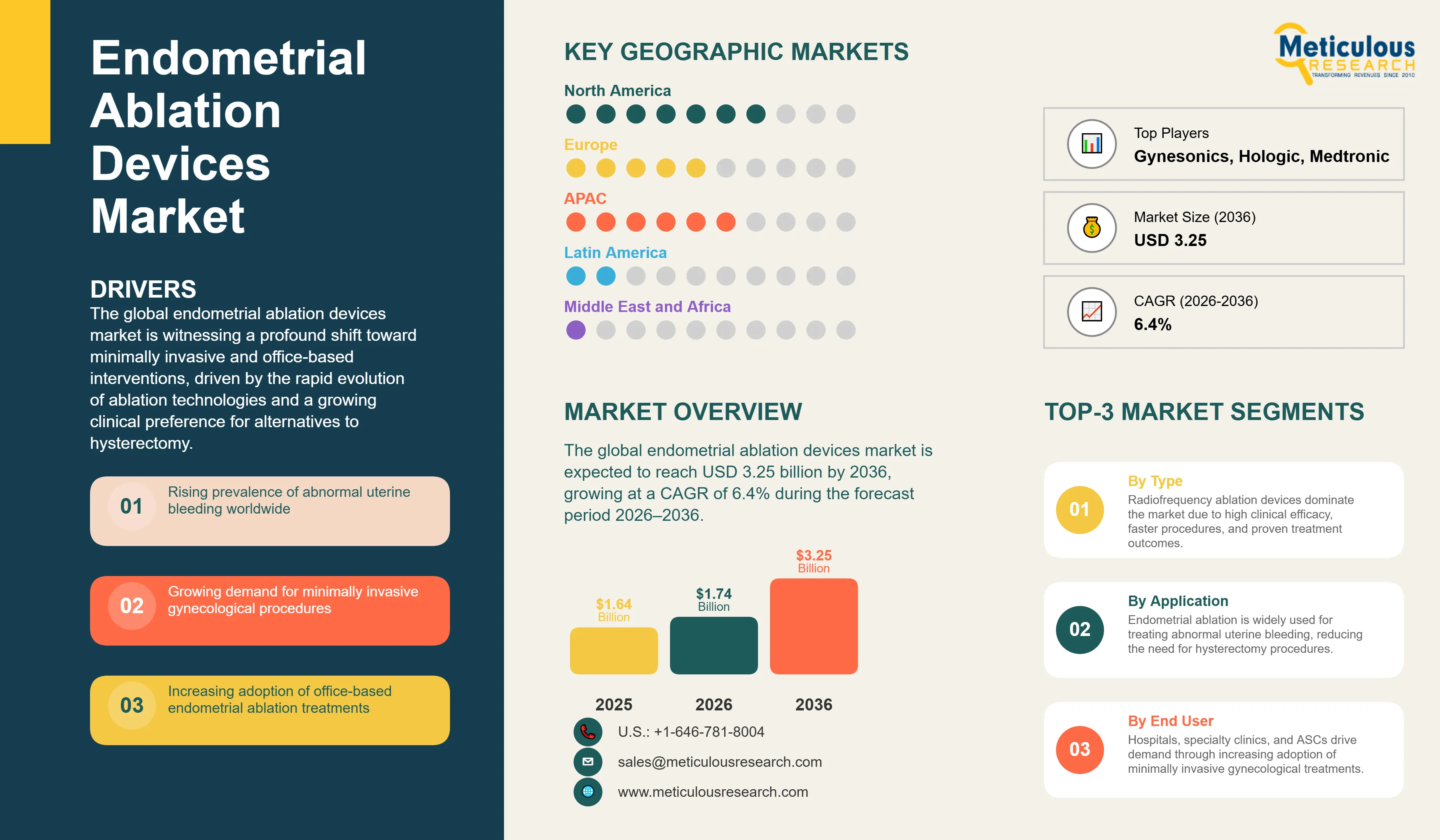

Report ID: MRHC - 1042072 Pages: 287 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global endometrial ablation devices market is estimated to be USD 1.74 billion in 2026. This market is expected to reach USD 3.25 billion by 2036, growing at a CAGR of 6.4% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global endometrial ablation devices market is witnessing a profound shift toward minimally invasive and office-based interventions, driven by the rapid evolution of ablation technologies and a growing clinical preference for alternatives to hysterectomy. Abnormal uterine bleeding (AUB), characterized by heavy or prolonged menstrual bleeding, remains a significant global health burden, affecting millions of women and significantly impacting their quality of life. The market is primarily fueled by the increasing prevalence of gynecological disorders, rising awareness of minimally invasive treatment options, and the growing clinical focus on organ-preserving surgeries. Technological innovations such as second-generation radiofrequency ablation and precision cryoablation are redefining the clinical standard of care. These advanced devices allow gynecologists to achieve higher amenorrhea rates with fewer complications and shorter recovery times. Clinical guidelines from the American College of Obstetricians and Gynecologists (ACOG) and the European Society for Gynaecological Endoscopy (ESGE) increasingly favor endometrial ablation for patients who have completed childbearing. As the healthcare landscape shifts toward value-based care, the adoption of office-based procedures is gaining traction, particularly in specialized clinics and ambulatory settings, by offering high-quality care with lower overhead costs and improved patient convenience. The integration of advanced imaging and personalized treatment planning is further expected to enhance the precision and consistency of endometrial ablation, driving sustained market growth.

The growth of the global endometrial ablation devices market is primarily driven by the rising incidence of heavy menstrual bleeding and the transformative shift toward organ-preserving gynecological surgeries.

Increasing Global Prevalence of Abnormal Uterine Bleeding Linked to Lifestyle and Hormonal Factors

A major driver for the market is the increasing global prevalence of abnormal uterine bleeding (AUB), which is closely linked to rising obesity rates, hormonal disorders, and changing reproductive health patterns. According to the World Health Organization, more than 1 billion people worldwide were living with obesity in 2022, a key risk factor for hormonal imbalances and menstrual disorders. Furthermore, clinical studies estimate that up to 30% of women of reproductive age experience abnormal uterine bleeding at some point in their lives, making AUB one of the most common reasons for gynecological consultations. As women become increasingly aware of the impact of heavy menstrual bleeding on their quality of life, productivity, and overall well-being, demand for effective and minimally invasive treatment options continues to grow. This expanding patient population is creating sustained demand for endometrial ablation procedures. In addition, growing awareness among patients and healthcare providers regarding the benefits of endometrial ablation as a safe and uterus-preserving alternative to hysterectomy is contributing to higher diagnosis rates and increased procedural volumes.

Rapid Clinical Shift toward Office-Based Gynecological Procedures to Enhance Patient Convenience

The market is significantly driven by the rapid adoption of office-based gynecological procedures. These interventions eliminate the need for general anesthesia and hospital stays, thereby reducing procedural costs and improving patient convenience. For healthcare facilities, office-based ablation offers a predictable procedural workflow and eliminates the high overhead costs associated with hospital operating rooms. The improved ergonomics and consistent performance of modern ablation systems are encouraging their widespread use in specialized clinics and community settings, which is a fundamental driver for market expansion.

Despite their clinical benefits, the adoption of advanced endometrial ablation devices is hindered by significant capital investment requirements and the inherent limitations of the technology in certain patient populations.

High Capital Investment and Operational Costs for Advanced Ablation Systems

A major restraint for the market is the high capital investment required for advanced ablation systems, particularly radiofrequency and cryoablation platforms. These technologies involve significant upfront costs for equipment, as well as ongoing expenses for specialized disposables, maintenance, and clinical training. According to the World Health Organization, approximately 90% of high-income countries have comprehensive access to essential health services, compared with only around 25% of low-income countries, highlighting the disparities in healthcare infrastructure and access to advanced medical technologies. Furthermore, the World Bank reports that out-of-pocket healthcare spending accounts for more than 40% of total health expenditure in many low- and middle-income countries, creating additional barriers to the adoption of elective gynecological procedures. As a result, smaller gynecology practices and healthcare facilities in resource-constrained settings often face challenges in acquiring and maintaining advanced endometrial ablation systems. This can limit the availability of minimally invasive treatment options and concentrate access within larger, well-funded healthcare institutions.

Inherent Clinical Limitations and Potential Procedural Complications in Certain Patient Populations

The global endometrial ablation devices market is also impacted by the inherent clinical limitations and potential complications associated with the procedure. While minimally invasive, ablation may not be suitable for patients with certain uterine anomalies, large fibroids, or suspected malignancy. Furthermore, the possibility of procedure failure and the potential need for subsequent hysterectomy can deter some patients and clinicians from seeking ablation. These clinical concerns, combined with the stringent regulatory requirements for new gynecological devices, remain significant hurdles for manufacturers and can restrain the rapid adoption of new ablation technologies.

Future growth opportunities in the endometrial ablation devices market are centered on the adoption of next-generation cryoablation technologies and the migration of procedures to ambulatory settings.

Increasing Clinical Adoption of Precision Cryoablation for Enhanced Patient Comfort

There is a significant opportunity for market growth driven by the increasing clinical adoption of precision cryoablation technology. Cryoablation offers high patient comfort and reduced post-procedural pain compared to thermal-based methods, allowing for procedures to be performed with minimal anesthesia. The ability to use smaller probes and operate with higher safety profiles makes cryoablation highly attractive for modern gynecological practices. Manufacturers that focus on developing and promoting cryoablation-based systems are well-positioned to capitalize on the ongoing technology replacement cycle in the gynecology market.

Significant Migration of Gynecological Procedures to Ambulatory Surgical Centers (ASCs)

The ongoing migration of gynecological procedures from hospital operating rooms to ambulatory surgical centers (ASCs) represents a major opportunity. ASCs offer a more efficient and cost-effective setting for minimally invasive procedures like endometrial ablation. The availability of high-performance, compact ablation systems has enabled ASCs to provide high-quality care with faster patient turnaround times. Manufacturers that can offer comprehensive solutions optimized for the ASC environment, including flexible procurement models for disposables, are likely to lead the next phase of market expansion.

Accelerating Transition toward Office-Based Endometrial Ablation in Gynecological Practice

A prominent trend in 2026 is the accelerating transition toward office-based endometrial ablation in daily gynecological practice. This shift is driven by the desire to eliminate hospital bottlenecks, reduce the total cost of ownership, and ensure consistent device performance. Manufacturers are continuously improving the ergonomics and safety profiles of ablation systems, making them increasingly competitive with hospital-based procedures. This trend is particularly strong in high-volume clinics and specialized centers, where procedural efficiency and patient convenience are paramount.

Integration of Advanced Visualization for Enhanced Procedural Precision and Consistency

The market is witnessing an increasing trend toward the integration of advanced visualization in endometrial ablation procedures. Enhanced imaging technologies allow gynecologists to precisely identify the uterine anatomy and monitor the ablation process in real-time. This information allows for more accurate energy delivery and ensures thorough treatment of the uterine lining. This trend aims to improve clinical precision, reduce procedure times, and enhance the predictability of amenorrhea outcomes, representing the next frontier in personalized gynecological care.

Analysis by Device Type

Based on device type, the radiofrequency ablation devices segment is expected to hold the largest share of the global endometrial ablation devices market in 2026. This leadership is substantiated by the proven clinical efficacy and high success rates of RF-based systems in achieving amenorrhea. The rapid procedural times and consistent outcomes across diverse patient populations have made RF ablation the clinical standard of care. However, the cryoablation devices segment is projected to register the highest CAGR during the forecast period. The high patient comfort and reduced post-procedural pain associated with cryoablation are driving significant clinical adoption and driving the growth of this segment.

Analysis by End User

By end user, the hospitals & specialty clinics segment is expected to hold the largest share in 2026. Hospitals lead the market as they provide the comprehensive infrastructure and specialized equipment required for a full range of endometrial ablation treatments. However, the ambulatory surgical centers (ASCs) segment is projected to register the highest CAGR during the forecast period. The ongoing shift toward minimally invasive, outpatient gynecological procedures, enabled by the availability of high-performance, compact ablation systems, is accelerating the migration of treatments to these outpatient facilities.

Largest Share: North America

North America is expected to dominate the global endometrial ablation devices market in 2026. This leading position is attributed to the high prevalence of abnormal uterine bleeding (AUB), a highly advanced healthcare system, and early adoption of innovative technologies like RF and cryoablation. The region benefits from favorable reimbursement policies for office-based gynecological procedures and the presence of major industry players. Key companies operating in the North America market are Hologic, Inc., Medtronic plc, and Boston Scientific Corporation.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global endometrial ablation devices market, with a CAGR of 8-10% during the forecast period. This rapid expansion is driven by the increasing incidence of gynecological disorders associated with urbanization, expanding healthcare infrastructure, and rising medical tourism. Governments in countries like China and India are also increasing investments in medical technology, facilitating the adoption of advanced endometrial ablation devices. Key companies operating in the Asia Pacific market are Olympus Corporation, Karl Storz SE & Co. KG, and Richard Wolf GmbH.

The global endometrial ablation devices market is characterized by intense competition among established medical technology giants and specialized gynecological firms. Competition is primarily focused on enhancing the procedural speed and safety of ablation systems and improving the patient experience through reduced pain and faster recovery. Key players are investing heavily in R&D to develop next-generation cryoablation probes and high-performance radiofrequency systems to capture the growing outpatient market. Strategic developments often involve acquisitions of specialized ablation technology firms and partnerships with leading gynecological clinics to validate new treatment protocols. Furthermore, there is a growing focus on providing integrated digital solutions that combine visualization, energy control, and personalized treatment planning. Manufacturers are also increasingly focusing on cost-effective procurement models for disposables and comprehensive clinical training programs to support the successful implementation of their technologies in diverse healthcare settings, which is critical for maintaining market leadership in this rapidly evolving field.

Hologic, Inc. (US), Medtronic plc (Ireland/US), Boston Scientific Corporation (US), The Cooper Companies, Inc. (CooperSurgical) (US), Minerva Surgical, Inc. (US), Olympus Corporation (Japan), Johnson & Johnson (Ethicon) (US), Idoman Teoranta (Ireland), Laborie Medical Technologies Corp. (Canada/US), Gynesonics, Inc. (US), Karl Storz SE & Co. KG (Germany), Richard Wolf GmbH (Germany), Symmetry Surgical Inc. (US), AngioDynamics, Inc. (US), Merit Medical Systems, Inc. (US), Teleflex Incorporated (US), B. Braun Melsungen AG (Germany), Smith & Nephew plc (UK), Cook Medical LLC (US), and AEGEA Medical, Inc. (Acquired by CooperSurgical) (US).

The global market is estimated at USD 1.74 billion in 2026, with a projected growth to USD 3.25 billion by 2036, at a CAGR of 6.4%.

Primary drivers include the rising global prevalence of abnormal uterine bleeding and the growing clinical preference for hysterectomy alternatives.

Major restraints include the high capital costs of specialized ablation systems and the potential clinical limitations in complex cases.

Opportunities lie in the increasing adoption of precision cryoablation technology and the significant migration of procedures to ambulatory surgical centers (ASCs).

Radiofrequency ablation devices are expected to hold the largest share due to their proven clinical efficacy and high success rates.

Cryoablation devices are projected to grow at the fastest CAGR, driven by high patient comfort and reduced post-procedural pain.

Hospitals & specialty clinics are expected to hold the largest share as the primary setting for comprehensive endometrial ablation treatments.

North America is expected to dominate the market due to high prevalence, advanced healthcare infrastructure, and early technology adoption.

Asia-Pacific is projected to witness the fastest growth, fueled by increasing incidence of gynecological disorders and expanding healthcare infrastructure.

Key trends include the accelerating transition toward office-based gynecology and the rise of organ-preserving surgical strategies.

Published Date: Jul-2026

Published Date: Jun-2026

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Mar-2016

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates