Resources

About Us

Pulsed Field Ablation Market Size, Share & Trends Analysis by Product (Catheters, Generators, Accessories), Application (Atrial Fibrillation, Ventricular Tachycardia, Oncology), End User (Hospitals, Cardiac Centers, Ambulatory Surgical Centers), and Geography — Global Opportunity Analysis and Industry Forecast (2026–2036)

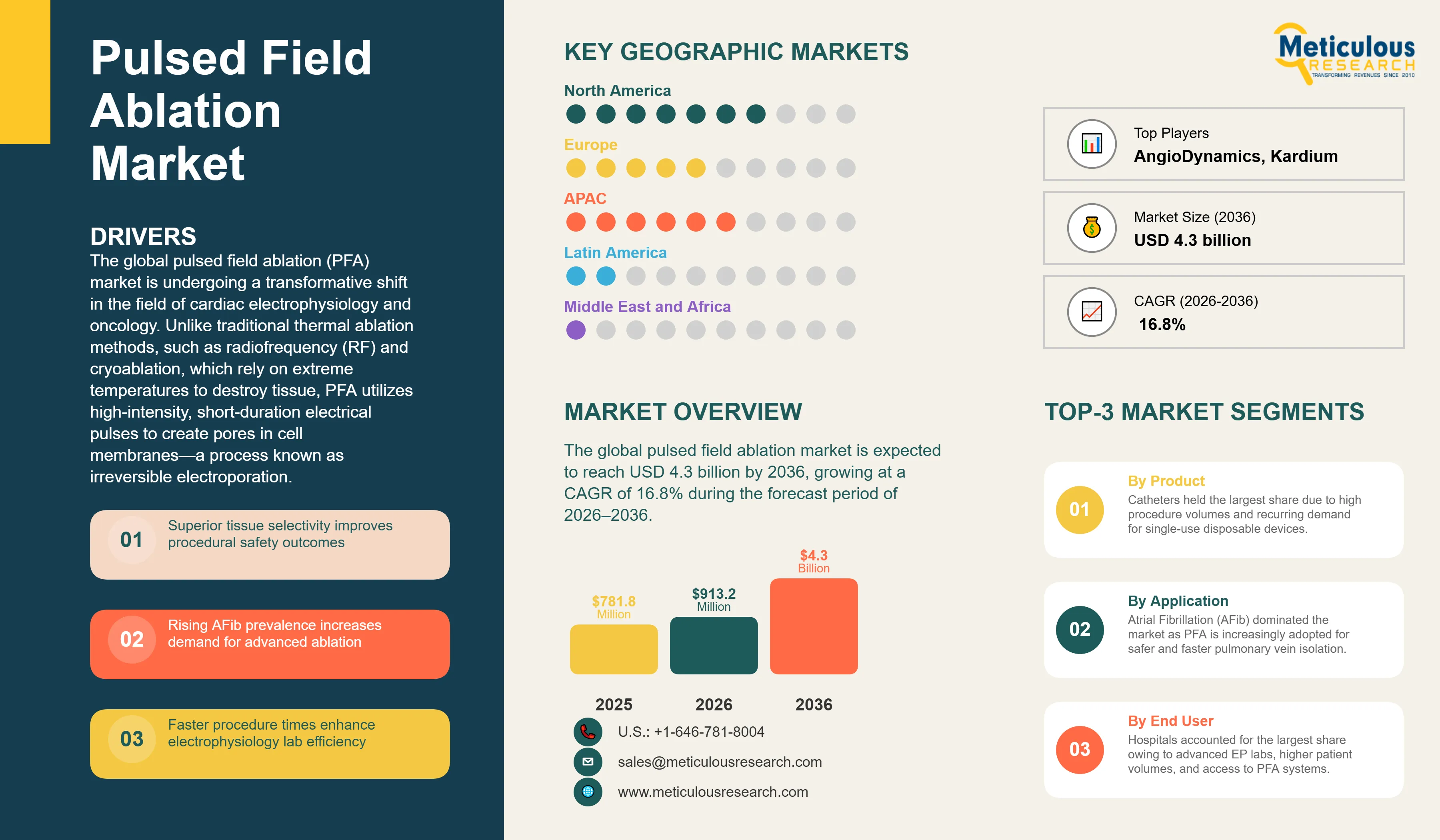

Report ID: MRHC - 1042006 Pages: 260 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global pulsed field ablation market is valued at USD 913.2 million in 2026. This market is expected to reach USD 4.3 billion by 2036, growing at a CAGR of 16.8% during the forecast period of 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global pulsed field ablation (PFA) market is undergoing a transformative shift in the field of cardiac electrophysiology and oncology. Unlike traditional thermal ablation methods, such as radiofrequency (RF) and cryoablation, which rely on extreme temperatures to destroy tissue, PFA utilizes high-intensity, short-duration electrical pulses to create pores in cell membranes—a process known as irreversible electroporation. This non-thermal mechanism is highly tissue-selective, allowing for the precise destruction of cardiomyocytes while sparing adjacent critical structures like the esophagus, phrenic nerve, and pulmonary vein adventitia. The adoption of PFA is driven by its superior safety profile, significantly reduced procedure times, and the growing global prevalence of atrial fibrillation (AFib) among aging populations.

The regulatory landscape for PFA has accelerated rapidly, with major medical device manufacturers receiving key authorizations. In late 2023 and early 2024, the FDA granted approval for the first PFA systems in the United States, marking the beginning of a new era in arrhythmia management. Medtronic's PulseSelect PFA system received FDA approval on December 13, 2023, followed by Boston Scientific's FARAPULSE™ PFA System on January 30, 2024. Clinical data from the pivotal ADVENT trial demonstrated that PFA is non-inferior to thermal ablation in terms of efficacy while offering a substantially better safety profile, with reduced pulmonary vein narrowing (0.9% vs 12.0% for thermal ablation).

Electrophysiology (EP) labs are increasingly adopting PFA due to its ability to streamline workflows and provide ultrarapid pulmonary vein isolation (PVI), which is critical for managing the increasing volume of AFib patients and improving hospital throughput.

Despite the strong momentum, the market faces restraints, including the high cost of PFA generators and specialized disposable catheters. The initial capital investment required for hospitals to transition to PFA technology can be significant, mainly for smaller cardiac centers. Additionally, while the short-term results are promising, the industry is still awaiting multi-year, long-term durability data to confirm that the lesions created by PFA are as permanent as those produced by thermal energy. However, the potential expansion of PFA into ventricular tachycardia and oncology, specifically for treating solid tumors in the liver, lung, and prostate, offers significant growth opportunities. PFA's ability to destroy malignant cells without damaging nearby blood vessels or bile ducts makes it a highly attractive alternative to thermal tumor ablation.

Geographically, North America is expected to dominate the global pulse field ablation market in 2026, driven by recent FDA approvals and a mature infrastructure for cardiac care. Meanwhile, Europe has benefited from earlier CE Mark clearances, leading to established clinical experience in several countries. The Asia-Pacific region is projected to witness the fastest growth, driven by increasing healthcare investments in China and India and a rising burden of cardiovascular diseases.

The competitive landscape within the global pulse field ablation market is characterized by intense innovation among giants like Medtronic, Boston Scientific, and Johnson & Johnson, alongside specialized startups focused on next-generation PFA catheter designs. As the industry moves toward 2036, the focus is expected to shift toward 'single-shot' multi-electrode catheters and integrated mapping-ablation systems.

The key driver for the pulsed field ablation market is the superior safety and tissue selectivity of the technology. Traditional thermal ablation methods carry a risk of damaging adjacent structures such as the esophagus (leading to atrioesophageal fistula) or the phrenic nerve. PFA's non-thermal mechanism targets cardiomyocytes while sparing these critical structures, significantly improving the safety profile of ablation procedures. The American Heart Association (AHA) and other clinical bodies have noted that this safety advantage is a major catalyst for clinical adoption.

Another key driver is the significant reduction in procedure time and improved lab efficiency. PFA allows for rapid pulmonary vein isolation, often requiring only a few seconds of energy delivery per site. This efficiency allows electrophysiology labs to treat more patients per day, addressing the growing backlog of AFib cases. As healthcare systems focus on value-based care and cost-efficiency, the ability to increase throughput without compromising safety is a compelling driver for hospital administrators and clinicians alike.

A major restraint is the high cost of PFA systems and disposable components. The capital expenditure for a PFA generator can be substantial, and the cost per catheter is typically higher than that of standard radiofrequency catheters. In many regions, reimbursement rates have not yet caught up with the higher costs of PFA technology, which may slow adoption in price-sensitive markets. Furthermore, the need for specialized training and the initial learning curve for electrophysiologists can be a barrier to widespread implementation in smaller cardiac centers.

The expansion of PFA into oncology and other non-cardiac applications presents a massive growth opportunity. Irreversible electroporation (IRE), the underlying principle of PFA, is being investigated for the treatment of solid tumors in the liver, pancreas, and prostate. Because PFA does not rely on heat, it can be used to treat tumors located near major blood vessels or bile ducts without the risk of thermal injury. Additionally, the development of 'single-shot' catheters that can ablate an entire pulmonary vein in one application is expected to further drive market growth.

The key challenge for the PFA market is the lack of long-term clinical durability data. While short-term success rates are comparable to thermal ablation, the industry needs multi-year follow-up to confirm that PFA-induced lesions remain permanent and do not lead to late-stage arrhythmia recurrence. Another challenge is the intense regulatory scrutiny as the technology evolves. Manufacturers must continuously provide robust clinical evidence to support new catheter designs and expanded indications, which can lead to significant delays in market entry.

There is a growing trend toward the integration of PFA catheters with advanced 3D cardiac mapping systems. This allows electrophysiologists to visualize the electrical activity of the heart in real-time while delivering PFA energy, ensuring more precise lesion placement and confirming pulmonary vein isolation immediately. Leading manufacturers are developing integrated platforms that combine high-density mapping with pulsed field energy to provide a seamless clinical workflow.

To address the diverse anatomy of the pulmonary veins, manufacturers are developing PFA catheters with adjustable shapes, such as variable-loop or 'flower' designs. These catheters can be adapted to fit different vein sizes and orientations, improving the consistency of tissue contact and lesion formation. This trend is expected to further reduce procedure times and improve the success rates of PFA-based AFib treatments.

Based on product, the overall pulse field ablation market is segmented into Catheters, Generators, and Accessories. In 2026, the catheters segment is expected to hold the largest share of the market. This dominance is due to the high volume of single-use disposable catheters required for each ablation procedure. The recurring revenue model associated with disposables makes this the most lucrative segment for manufacturers, driving continuous innovation in catheter design and materials.

The Generators segment is projected to register a significant CAGR, as hospitals and cardiac centers invest in the necessary hardware to support PFA technology. The transition from thermal to non-thermal ablation requires the installation of dedicated pulsed field generators, creating a robust market for capital equipment in the early years of the forecast period.

North America is expected to dominate the global pulsed field ablation market in 2026, primarily due to the recent FDA approvals and the high volume of cardiac ablation procedures performed in the United States. The region's advanced healthcare infrastructure, high awareness of AFib treatments, and strong presence of major medical device manufacturers like Medtronic and Boston Scientific are key drivers. The key companies operating in the North American market are Medtronic, Boston Scientific, and Johnson & Johnson.

Asia-Pacific is projected to witness the fastest growth during the forecast period. This is driven by rapid digitalization in healthcare, increasing investments in cardiac care in China and India, and a rising burden of cardiovascular diseases. The region's large population and the increasing adoption of advanced medical technologies are driving the demand for scalable PFA solutions. The key companies operating in the Asia-Pacific market are Abbott, Medtronic, and various emerging medical technology specialists.

The global pulsed field ablation market is characterized by intense competition and a high degree of innovation. The competitive landscape is dominated by a few major medical device giants who have secured early regulatory approvals and are leveraging their extensive distribution networks to drive adoption. Medtronic and Boston Scientific currently lead the market, having received the first FDA approvals for their PFA systems. These companies are actively investing in clinical trials to expand the indications for PFA and are acquiring specialized startups to bolster their technology portfolios.

In addition to the large incumbents, the market features several specialized companies focused on next-generation PFA technologies. Companies like Johnson & Johnson (Biosense Webster) and Abbott are in the advanced stages of clinical validation for their own PFA platforms. The competitive landscape is also shaped by strategic partnerships between catheter manufacturers and mapping system providers. Key players in the global pulsed field ablation market include Medtronic plc, Boston Scientific Corporation, Johnson & Johnson (Biosense Webster), Abbott Laboratories, AngioDynamics, Inc., and Kardium Inc.

The market is projected to reach USD 4.3 billion by 2036, growing at a CAGR of 16.8% from 2026 to 2036.

The catheters segment is expected to hold the largest share in 2026 due to the high recurring revenue from single-use disposables.

PFA is tissue-selective, targeting cardiomyocytes while sparing critical adjacent structures like the esophagus and nerves.

Asia-Pacific is projected to witness the highest CAGR due to rapid healthcare expansion and a rising burden of AFib.

PFA can reduce pulmonary vein isolation procedure times by up to 40% compared to traditional thermal methods.

Challenges include the high capital cost of generators and the current lack of multi-year, long-term durability data.

Pivotal trials such as ADVENT and PULSED AF have confirmed the safety and non-inferior efficacy of PFA systems.

Yes, PFA (as irreversible electroporation) is being investigated for treating solid tumors in the liver, lung, and prostate.

Integrated 3D mapping allows for precise lesion placement and immediate confirmation of pulmonary vein isolation.

Leading companies include Medtronic, Boston Scientific, Johnson & Johnson, Abbott, and AngioDynamics.

Published Date: Jul-2026

Published Date: Jun-2026

Published Date: May-2024

Published Date: Feb-2023

Published Date: Mar-2016

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates