Resources

About Us

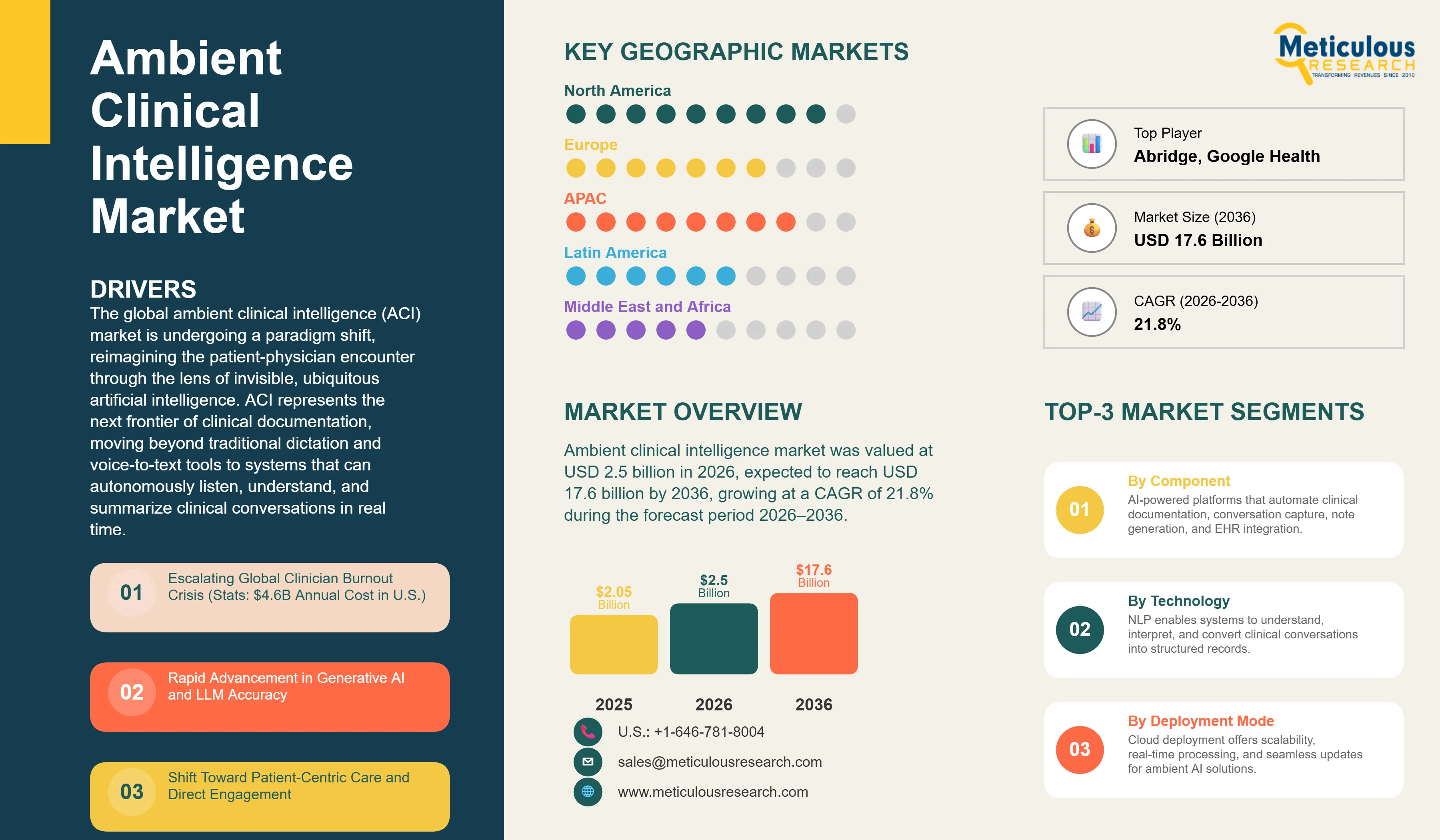

The global ambient clinical intelligence market was valued at USD 2.5 billion in 2026. This market is expected to reach USD 17.6 billion by 2036, growing at a CAGR of 21.8% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global ambient clinical intelligence (ACI) market is undergoing a paradigm shift, reimagining the patient-physician encounter through the lens of invisible, ubiquitous artificial intelligence. ACI represents the next frontier of clinical documentation, moving beyond traditional dictation and voice-to-text tools to systems that can autonomously listen, understand, and summarize clinical conversations in real time. This market's emergence is a direct response to the growing clinician burnout crisis, where the administrative burden associated with electronic health records (EHRs) has become a major contributor to workforce attrition and reduced clinical productivity. According to the American Medical Association, approximately 45% of physicians report at least one symptom of burnout, while physicians spend nearly two hours on administrative and documentation activities for every hour of direct patient care. By leveraging ambient sensing technologies and advanced Large Language Models (LLMs), ACI platforms reduce manual documentation requirements and enable clinicians to devote more attention to patient care.

The growth of the ACI market is closely linked to rapid advances in Generative AI and healthcare-specific natural language processing capabilities. Healthcare organizations increasingly recognize documentation burden as a key operational challenge, with studies showing that clinicians can spend up to 16 minutes per patient encounter on EHR-related activities. Early deployments of ambient AI solutions have demonstrated documentation time reductions of approximately 30–60%, enabling physicians to recover significant portions of their workday. These efficiency gains support broader healthcare objectives, including improved clinician experience, enhanced patient engagement, better care quality, and lower operational costs. As health systems pursue the Quadruple Aim framework, ACI is emerging as an important enabler of sustainable healthcare delivery.

The ACI ecosystem is characterized by deep integration between AI software providers and major EHR platforms. Leading healthcare organizations are increasingly adopting enterprise-wide ACI deployments rather than limiting usage to individual specialties. Cloud-based delivery models dominate the market due to their scalability and ability to support real-time speech recognition and natural language processing workloads. Furthermore, advancements in ambient audio capture technologies, speaker differentiation, and noise suppression are improving system performance in complex clinical environments, further supporting adoption across hospitals and ambulatory care settings.

Geographically, North America remains the largest market due to its advanced digital health infrastructure, widespread EHR adoption, and supportive innovation ecosystem. The financial impact of physician burnout is substantial; research published by the Mayo Clinic and healthcare policy organizations estimates that physician burnout contributes approximately USD 4.6 billion annually in costs to the U.S. healthcare system through turnover and reduced clinical productivity. Meanwhile, the Asia-Pacific region is expected to experience the fastest growth, supported by government-led digital health initiatives, expanding healthcare IT investments, and persistent healthcare workforce shortages. According to the World Health Organization, the world faces a projected shortage of approximately 10 million healthcare workers by 2030, reinforcing the need for AI-enabled workflow automation solutions across healthcare systems.

The primary driver for the ambient clinical intelligence market is the escalating global crisis of clinician burnout. According to the American Medical Association, approximately 45% of physicians report at least one symptom of burnout, while physicians spend nearly two hours on administrative and documentation tasks for every hour of direct patient care. Additionally, studies have shown that clinicians can spend up to 16 minutes per patient encounter interacting with EHR systems, significantly reducing time available for patient engagement. As healthcare organizations seek to alleviate administrative burdens and improve workforce retention, demand for ambient documentation solutions is increasing rapidly.

Furthermore, the rapid advancement and democratization of Large Language Models (LLMs) have made ACI significantly more reliable and easier to deploy than previous voice-to-text tools. The shift toward patient-centric care, which prioritizes the quality of the patient-physician interaction, is also a major catalyst for ACI adoption, as it removes the computer screen as a barrier during clinical encounters.

Data privacy and ethical concerns regarding the recording of sensitive patient-physician conversations remain significant restraints. Managing these recordings in compliance with regulations like HIPAA and GDPR requires robust security infrastructure and transparent consent processes. Furthermore, the high initial implementation costs and ongoing subscription fees can be a barrier for smaller medical practices and under-resourced community hospitals. There are also concerns regarding the potential for AI 'hallucinations' in clinical notes, necessitating a high level of physician oversight and verification.

Significant opportunities exist in the integration of ACI with predictive analytics and social determinants of health (SDOH) identification. By analyzing the natural language of clinical conversations, ACI can identify subtle cues regarding a patient's home environment or mental health that might not be captured in a standard EHR form. Additionally, the expansion of ACI into non-English speaking markets through the localization of LLMs presents a massive growth opportunity. The use of ACI in surgical and emergency medicine settings, where hands-free documentation is critical, also offers high potential for market expansion.

A critical challenge for ACI providers is maintaining high accuracy in busy, high-noise clinical environments with multiple speakers. Differentiating between the clinician, the patient, and family members while filtering out background noise requires advanced multi-directional microphone arrays and sophisticated audio processing. Ensuring seamless, real-time integration with a wide variety of EHR platforms is also a persistent challenge. Furthermore, as regulatory bodies increase their scrutiny of AI transparency, ACI vendors must ensure their models are explainable and that the generated notes are easily verifiable by the clinician.

The most prominent trend in the ACI market is the move away from simple transcription toward Generative AI-powered structured note generation. Modern ACI platforms can understand the clinical context of a conversation and automatically populate the correct sections of a SOAP note or clinical summary. This trend is significantly reducing the 'cognitive load' on clinicians, as they no longer need to manually organize their thoughts after a visit, leading to higher physician satisfaction and better documentation quality.

There is a growing trend toward using ACI as a platform for real-time Clinical Decision Support (CDS) and automated medical coding. By analyzing the conversation as it happens, ACI can provide clinicians with relevant evidence-based guidelines or suggest appropriate ICD-10 codes for billing. This integration not only improves clinical accuracy but also streamlines the revenue cycle, providing a comprehensive solution that addresses both clinical and administrative needs.

Based on component, the market is segmented into Software Platforms, Hardware & Sensors, and Services. In 2026, the Software Platforms segment is expected to hold the largest share of the market. The core AI engines, cloud-based processing portals, and subscription-based licensing models generate the majority of recurring revenue in the ACI market. As AI models become more advanced and require more computational power, the value of the software component continues to rise.

The Services segment is projected to register the fastest CAGR during the forecast period. This growth is driven by the increasing need for enterprise-wide implementation, EHR integration, and comprehensive clinician training. As large health systems move toward full-scale deployment, the demand for managed services and technical support is expected to surge.

Based on specialty, the market is segmented into Primary Care & Internal Medicine, Radiology & Pathology, Emergency Medicine, and Surgery & Specialty Clinics. In 2026, the Primary Care segment is expected to hold the largest share of the market. Primary care clinicians manage the highest volume of conversational patient visits and face the most significant documentation burden, making them the primary target for ACI solutions.

The Emergency Medicine segment is projected to witness the fastest growth during the forecast period. The high-pressure, high-noise environment of the emergency department is particularly well-suited for hands-free ambient AI documentation. As ACI technology improves its ability to handle multi-speaker environments, its adoption in emergency medicine is expected to accelerate.

North America is expected to hold the largest share of the global ambient clinical intelligence market in 2026, driven by a high concentration of leading ACI vendors and the significant financial impact of physician burnout in the United States. The region accounts for approximately 45% of the global share, supported by a robust digital health infrastructure and early adoption by large health systems. Key companies operating in the North American market include Microsoft (Nuance), Abridge, and Suki AI.

Asia-Pacific is projected to witness the fastest growth during the forecast period. Countries like China and India are rapidly digitalizing their healthcare systems and investing in AI to overcome clinician shortages. The rising number of specialized AI startups in the region and the growing focus on improving healthcare access present significant opportunities for market expansion. Key companies operating in the Asia-Pacific market include Oracle Health, Philips Healthcare, and emerging domestic AI providers.

The global ambient clinical intelligence market is highly competitive and is characterized by the dominance of Microsoft (Nuance) and a group of highly innovative AI startups like Abridge and Suki AI. Microsoft's DAX Copilot is a market leader due to its deep integration with major EHRs and its established presence in health systems. However, startups are gaining significant traction by offering highly flexible, mobile-first solutions and leveraging the latest advancements in LLMs to provide superior note accuracy and clinician experience.

Strategic partnerships and 'Best in KLAS' rankings are critical for market positioning. Companies are increasingly focusing on multi-specialty support and hands-free workflows to differentiate their offerings. Clinical validation and evidence of burnout reduction are also key competitive factors. Key players in the global ambient clinical intelligence market include Microsoft Corporation (Nuance), Abridge, Suki AI, Amazon Web Services (AWS), Google Health, Oracle Health, Ambience Healthcare, DeepScribe, Nabla, and Heidi Health.

The market is projected to reach USD 17,643.6 million by 2036, growing at a CAGR of 21.8% from 2026 to 2036.

The Software Platforms segment is expected to hold the largest share in 2026 due to its core role in note generation.

The escalating global crisis of clinician burnout and the maturity of Generative AI are the primary drivers.

Emergency Medicine is expected to grow the fastest due to the high-pressure need for hands-free documentation.

ACI autonomously summarizes conversations into structured medical notes, whereas voice-to-text requires manual dictation.

Physician burnout is estimated to cost the U.S. healthcare system approximately $4.6 billion annually.

North America holds the largest share, accounting for approximately 45% of the global market in 2026.

Data privacy concerns, high implementation costs for small practices, and concerns over AI accuracy are the main restraints.

Generative AI (LLMs) allows for the automated creation of accurate, human-like structured clinical summaries.

The market is led by Microsoft (Nuance), Abridge, Suki AI, and major cloud providers like AWS and Google Health.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Component

3.2.2. Market Analysis, by Technology

3.2.3. Market Analysis, by Deployment Mode

3.2.4. Market Analysis, by Application

3.2.5. Market Analysis, by Specialty

3.2.6. Market Analysis, by End User

3.2.7. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Escalating Global Clinician Burnout Crisis (Stats: $4.6B Annual Cost in U.S.)

4.2.1.2. Rapid Advancement in Generative AI and LLM Accuracy

4.2.1.3. Shift Toward Patient-Centric Care and Direct Engagement

4.2.2. Restraints

4.2.2.1. Data Privacy, Security, and Ethical Concerns in Patient Recording

4.2.2.2. High Implementation and Subscription Costs for Smaller Practices

4.2.3. Opportunities

4.2.3.1. Integration with Predictive Analytics for SDOH Identification

4.2.3.2. Expansion into Non-English Speaking Markets via Localized LLMs

4.2.4. Challenges

4.2.4.1. Maintaining Accuracy in High-Noise, Multi-Speaker Environments

4.2.4.2. Regulatory Scrutiny on AI Transparency and Clinical Accountability

4.2.5. Trends

4.2.5.1. Shift Toward Generative AI-Powered Structured Note Generation

4.2.5.2. Integration of ACI with Real-Time CDS and Coding Automation

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Ambient Clinical Intelligence Market, by Component

5.1. Overview

5.2. Software Platforms

5.3. Hardware & Sensors

5.3.1. Ambient Microphones & Smart Speakers

5.3.2. Mobile & Wearable Devices

5.4. Services

5.4.1. Implementation & Integration Services

5.4.2. Training & Support Services

6. Global Ambient Clinical Intelligence Market, by Technology

6.1. Overview

6.2. Natural Language Processing (NLP)

6.3. Generative AI (LLMs)

6.4. Voice Biometrics & Speaker Identification

7. Global Ambient Clinical Intelligence Market, by Deployment Mode

7.1. Overview

7.2. Cloud-based (SaaS)

7.3. On-premise

8. Global Ambient Clinical Intelligence Market, by Application

8.1. Overview

8.2. Clinical Documentation & EMR Integration

8.3. Clinical Decision Support (CDS)

8.4. Patient Engagement & Communication

8.5. Medical Coding & Billing Automation

9. Global Ambient Clinical Intelligence Market, by Specialty

9.1. Overview

9.2. Primary Care & Internal Medicine

9.3. Radiology & Pathology

9.4. Emergency Medicine

9.5. Surgery & Specialty Clinics

10. Global Ambient Clinical Intelligence Market, by End User

10.1. Overview

10.2. Hospitals & Health Systems

10.3. Ambulatory Surgical Centers (ASCs)

10.4. Specialty Clinics & Physician Practices

11. Global Ambient Clinical Intelligence Market, by Geography

11.1. Overview

11.2. North America

11.2.1. U.S.

11.2.2. Canada

11.3. Europe

11.3.1. U.K.

11.3.2. Germany

11.3.3. France

11.3.4. Italy

11.3.5. Spain

11.3.6. Rest of Europe

11.4. Asia-Pacific

11.4.1. China

11.4.2. Japan

11.4.3. India

11.4.4. Australia

11.4.5. Rest of Asia-Pacific

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Rest of Latin America

11.6. Middle East & Africa

12. Competitive Landscape

12.1. Overview

12.2. Key Growth Strategies

12.3. Competitive Dashboard

12.4. Vendor Market Positioning

12.5. Market Share Analysis, 2025

13. Company Profiles

13.1. Microsoft Corporation (Nuance Communications)

13.2. Abridge

13.3. Suki AI

13.4. Amazon Web Services (AWS)

13.5. Google Health (Alphabet Inc.)

13.6. Oracle Health

13.7. Ambience Healthcare

13.8. DeepScribe

13.9. Nabla

13.10. Heidi Health

13.11. NextGen Healthcare

13.12. Augmedix

13.13. Robin Healthcare

13.14. Tali AI

13.15. Freed AI

13.16. Corti

14. Appendix

Published Date: Jun-2024

Published Date: Jun-2024

Published Date: Jan-2024

Subscribe to get the latest industry updates