Resources

About Us

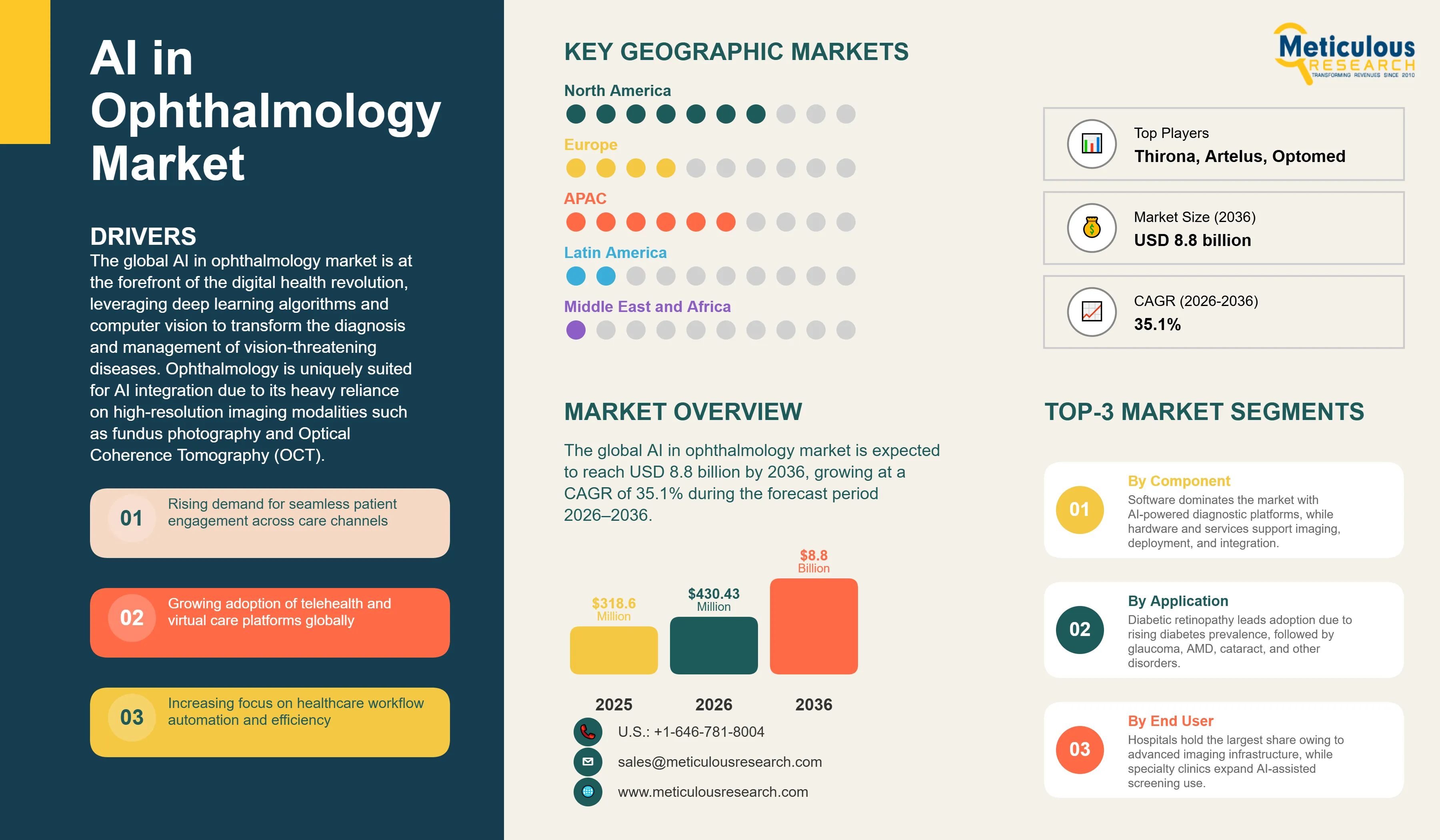

The global AI in ophthalmology market was valued at USD 430.43 million in 2026. This market is expected to reach USD 8.8 billion by 2036, growing at a CAGR of 35.1% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global AI in ophthalmology market is at the forefront of the digital health revolution, leveraging deep learning algorithms and computer vision to transform the diagnosis and management of vision-threatening diseases. Ophthalmology is uniquely suited for AI integration due to its heavy reliance on high-resolution imaging modalities such as fundus photography and Optical Coherence Tomography (OCT). The primary focus of AI applications in this field is the automated screening and early detection of chronic conditions like diabetic retinopathy, glaucoma, and age-related macular degeneration (AMD). The growth of this market is fundamentally driven by the rising global burden of eye diseases, the critical shortage of ophthalmologists in many regions, and the continuous advancement in neural network architectures that allow for human-level diagnostic accuracy.

Diabetic retinopathy (DR) represents the most significant application for AI in ophthalmology, driven by the growing global burden of diabetes. According to the International Diabetes Federation, approximately 589 million adults were living with diabetes worldwide in 2024, and this number is projected to reach approximately 853 million by 2050. Among individuals with diabetes, studies estimate that more than one-third develop some form of diabetic retinopathy, making DR one of the leading causes of preventable blindness among working-age adults. AI systems for autonomous DR screening have already received landmark regulatory clearances from agencies such as the U.S. Food and Drug Administration, enabling point-of-care diagnosis in primary care and community settings. These systems can analyze retinal images within seconds and have demonstrated sensitivity exceeding 85% and specificity exceeding 80% for detecting referable diabetic retinopathy in pivotal clinical studies. Furthermore, the integration of AI into OCT analysis is enabling precise quantification of retinal fluid and biomarkers, supporting treatment monitoring for patients receiving anti-VEGF therapy for age-related macular degeneration (AMD) and other retinal disorders.

Despite the immense potential, the market faces challenges related to data privacy, algorithm bias, and interoperability with existing electronic health records (EHR). The handling of sensitive patient imaging data requires robust cybersecurity measures and compliance with stringent regulations like GDPR and HIPAA. Additionally, ensuring that AI models perform consistently across diverse patient populations and imaging devices is critical for maintaining clinical trust. However, the emergence of AI in surgical guidance and home-based monitoring presents substantial growth opportunities. AI-powered intraoperative tools are being developed to assist surgeons during cataract and vitreoretinal procedures, while mobile apps for patient self-monitoring are extending the reach of eye care beyond the clinic. These innovations are expected to further drive market expansion and improve patient outcomes globally.

Geographically, North America is expected to dominate the market in 2026, supported by early regulatory clearances, high healthcare expenditure, and a robust ecosystem of AI healthcare startups. Meanwhile, the Asia-Pacific region is projected to witness the fastest growth during the forecast period. This growth is fueled by the massive diabetic population in China and India, increasing government investments in digital health infrastructure, and the rising adoption of cloud-based diagnostic platforms. The competitive landscape is characterized by collaboration between traditional imaging device manufacturers and AI software specialists, alongside tech giants like Google and Microsoft who are investing heavily in medical AI. As the industry moves toward 2036, the focus is expected to shift toward multi-modal AI models that can integrate clinical data with imaging for comprehensive patient assessment.

The primary driver for the AI in ophthalmology market is the growing gap between the availability of eye care specialists and the rapidly expanding patient population requiring vision care. According to the World Health Organization, at least 2.2 billion people globally live with a vision impairment or blindness, of whom at least 1 billion cases are preventable or remain unaddressed. Additionally, the International Diabetes Federation estimates that approximately 589 million adults were living with diabetes worldwide in 2024, increasing the demand for diabetic retinopathy screening and retinal disease management. As healthcare systems struggle to meet rising screening requirements, AI is emerging as a scalable solution capable of automating the analysis of millions of retinal images and enabling earlier detection and intervention. The American Academy of Ophthalmology has highlighted the growing importance of AI-enabled screening tools in addressing workforce shortages and expanding access to eye care services.

Another key driver is the continuous advancement in deep learning and computer vision technologies. Modern AI algorithms have demonstrated diagnostic performance comparable to expert graders in detecting retinal diseases such as diabetic retinopathy and age-related macular degeneration. The expansion of cloud-based AI platforms is enabling real-time diagnostic support in remote and underserved regions, where specialist availability remains limited. According to the World Health Organization, approximately 90% of people living with vision impairment reside in low- and middle-income countries, highlighting the need for scalable diagnostic solutions. Furthermore, increasing adoption of retinal imaging technologies, including portable fundus cameras and OCT systems, is generating large volumes of high-quality clinical data that continue to improve AI model performance and accelerate market adoption.

A major restraint is the concern over data privacy and the security of sensitive medical imaging data. AI systems require access to large datasets for training and validation, and the transmission of patient images to cloud-based servers can pose cybersecurity risks. Compliance with varying data protection regulations across different countries can also be a significant hurdle for international AI providers. Additionally, the high initial cost of integrating AI software with existing clinical workflows and imaging hardware can be a barrier for smaller ophthalmology practices and diagnostic centers.

The expansion of AI into intraoperative guidance and surgical robotics presents a massive growth opportunity. AI-powered tools can assist surgeons during complex procedures like cataract surgery or retinal detachment repair by providing real-time feedback on tissue anatomy and surgical maneuvers. Another key opportunity lies in home-based monitoring and patient self-care. AI-powered mobile apps that can analyze photos of the eye or monitor visual acuity are being developed to help patients with chronic conditions like AMD track their disease progression between clinical visits, allowing for timely intervention when changes occur.

The primary challenge for the AI in ophthalmology market is ensuring the interoperability of AI algorithms with diverse imaging devices and electronic health records (EHR). Retinal images can vary significantly depending on the camera model, lighting conditions, and patient characteristics, and AI models must be robust enough to handle this variability. Another challenge is navigating the complex regulatory landscape for AI medical devices. Manufacturers must provide extensive clinical evidence to demonstrate the safety and efficacy of their algorithms, which can be a costly and time-consuming process, particularly in emerging markets.

There is a dominant trend toward the development of autonomous AI systems that can provide a diagnosis without the need for human over-read. These systems are particularly valuable in primary care and community screening settings, where eye specialists are not readily available. By providing an immediate 'refer' or 'no-refer' decision, autonomous AI is streamlining the screening process and ensuring that high-risk patients are prioritized for specialist care. This trend is expected to accelerate as more AI systems receive regulatory clearance for autonomous use.

An emerging trend is the integration of imaging data with clinical information, such as patient history, lab results, and genetic data, to provide a more comprehensive assessment of eye health. Multi-modal AI models are being developed to predict disease progression and treatment response more accurately by considering the broader clinical context. This holistic approach is expected to lead to more personalized treatment plans and improved long-term outcomes for patients with chronic eye conditions.

Based on component, the market is segmented into Software, Hardware, and Services. In 2026, the software segment is expected to hold the largest share of the market. This dominance is due to the high demand for cloud-based AI diagnostic platforms and the recurring revenue models associated with software subscriptions. AI software is the core engine of diagnostic innovation in ophthalmology, with continuous updates and new algorithm releases driving market growth.

The Hardware segment is projected to register a significant CAGR, as diagnostic centers and hospitals invest in high-quality retinal cameras and OCT devices that are compatible with AI software. The need for specialized hardware to capture high-resolution images for AI analysis is a key driver for this segment, particularly in emerging markets where infrastructure is being upgraded.

North America is expected to dominate the global AI in ophthalmology market in 2026, primarily due to its advanced healthcare infrastructure, early regulatory clearances for AI medical devices, and high adoption of digital health solutions. The U.S. is the leading market for AI innovation, with a robust ecosystem of startups and research institutions. The presence of major industry players like Digital Diagnostics and Eyenuk is a key driver. The key companies operating in the North American market are Digital Diagnostics, Eyenuk, AEYE Health, and Google Health.

Asia-Pacific is projected to witness the fastest growth during the forecast period. This is driven by the massive diabetic population in China and India, increasing government investments in digital health infrastructure, and the rising burden of vision-threatening diseases. The region's large population and the increasing adoption of advanced medical technologies are driving the demand for scalable AI screening solutions. The key companies operating in the Asia-Pacific market are Topcon, Optomed, and various emerging medical technology specialists in the region.

The global AI in ophthalmology market is characterized by intense competition and a high degree of innovation. The competitive landscape is dominated by specialized AI software companies that have secured early regulatory approvals and are partnering with imaging device manufacturers to drive adoption. Digital Diagnostics and Eyenuk currently lead the market in autonomous DR screening, having pioneered the regulatory pathway for AI medical devices. These companies are actively investing in clinical trials to expand the indications for their algorithms to include glaucoma and AMD.

In addition to specialized startups, major technology companies like Google and Microsoft are investing heavily in ophthalmology AI through their health divisions. Traditional imaging giants such as Carl Zeiss Meditec and Topcon are also integrating AI into their devices to provide a complete diagnostic solution. The competitive landscape is also shaped by strategic collaborations between AI providers and public health organizations to implement large-scale screening programs. Key players in the global AI in ophthalmology market include Digital Diagnostics Inc., Eyenuk, Inc., AEYE Health, Google Health, Carl Zeiss Meditec AG, and Topcon Corporation.

The market is projected to reach USD 8.8 billion by 2036, growing at a CAGR of 35.1% from 2026 to 2036.

Diabetic retinopathy is expected to hold the largest share in 2026 due to the global diabetes epidemic and autonomous screening.

The shortage of eye specialists and the need for scalable screening solutions for chronic eye diseases are the primary drivers.

Asia-Pacific is projected to witness the highest CAGR due to its large diabetic population and digital health investments.

AI algorithms can identify subtle pathological changes with sensitivity and specificity exceeding 90%, rivaling expert graders.

Challenges include data privacy concerns, high implementation costs, and the need for interoperability with clinical workflows.

Yes, AI-powered tools are being developed to provide real-time intraoperative guidance during cataract and retinal surgeries.

Cloud platforms allow for real-time diagnostic support in remote areas by analyzing images captured by portable fundus cameras.

Key trends include the shift toward autonomous diagnostic systems and the integration of multi-modal clinical data.

Leading companies include Digital Diagnostics, Eyenuk, AEYE Health, Google Health, Zeiss, and Topcon.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency and Pricing

2. Research Methodology

2.1. Research Process

2.2. Data Collection & Sources

2.2.1. Primary Research

2.2.2. Secondary Research

2.3. Market Sizing & Forecasting

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Data Triangulation & Validation

2.5. Assumptions & Limitations

3. Executive Summary

3.1. Market Overview

3.2. Segmental Analysis

3.3. Geographic Outlook

3.4. Competitive Insights

4. Market Insights

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Growing Shortage of Eye Specialists and Rising Patient Population

4.2.1.2. Continuous Advancements in Deep Learning and Computer Vision Technologies

4.2.2. Restraints

4.2.2.1. Data Privacy Concerns and Security of Sensitive Medical Imaging Data

4.2.2.2. High Implementation Costs for AI Software and Infrastructure Upgrades

4.2.3. Opportunities

4.2.3.1. Expansion of AI into Intraoperative Guidance and Surgical Robotics

4.2.3.2. Development of AI-Powered Home-Based Monitoring and Self-Care Tools

4.2.4. Challenges

4.2.4.1. Ensuring Interoperability with Diverse Imaging Devices and EHR Systems

4.2.4.2. Navigating Complex Regulatory Pathways for AI Medical Devices

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global AI in Ophthalmology Market Assessment, by Component

5.1. Introduction

5.2. Software

5.3. Hardware

5.4. Services

6. Global AI in Ophthalmology Market Assessment, by Application

6.1. Introduction

6.2. Diabetic Retinopathy

6.3. Glaucoma

6.4. Age-Related Macular Degeneration (AMD)

6.5. Cataract

6.6. Others

7. Global AI in Ophthalmology Market Assessment, by End User

7.1. Introduction

7.2. Hospitals

7.3. Specialty Clinics

7.4. Diagnostic Centers

8. Global AI in Ophthalmology Market Assessment, by Geography

8.1. Introduction

8.2. North America

8.2.1. U.S.

8.2.2. Canada

8.3. Europe

8.3.1. Germany

8.3.2. UK

8.3.3. France

8.3.4. Italy

8.3.5. Spain

8.3.6. Rest of Europe

8.4. Asia-Pacific

8.4.1. China

8.4.2. India

8.4.3. Japan

8.4.4. Singapore

8.4.5. Australia

8.4.6. South Korea

8.4.7. Rest of Asia-Pacific

8.5. Latin America

8.5.1. Brazil

8.5.2. Mexico

8.5.3. Rest of Latin America

8.6. Middle East & Africa

8.6.1. UAE

8.6.2. Saudi Arabia

8.6.3. South Africa

8.6.4. Rest of MEA

9. Global AI in Ophthalmology Market Assessment, by Country/Sub-Region Analysis

9.1. Introduction

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. UK

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. India

9.4.3. Japan

9.4.4. Singapore

9.4.5. Australia

9.4.6. South Korea

9.4.7. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

9.6.1. UAE

9.6.2. Saudi Arabia

9.6.3. South Africa

9.6.4. Rest of MEA

10. Competitive Landscape

10.1. Introduction

10.2. Market Share Analysis

10.3. Competitive Benchmarking

10.4. Strategic Developments

10.4.1. Product Launches & Enhancements

10.4.2. Partnerships & Collaborations

10.4.3. Mergers & Acquisitions

11. Company Profiles (Active Manufacturers Only)

11.1. Digital Diagnostics Inc.

11.2. Eyenuk, Inc.

11.3. AEYE Health

11.4. Google Health

11.5. Microsoft Corporation

11.6. NVIDIA Corporation

11.7. Topcon Corporation

11.8. Carl Zeiss Meditec AG

11.9. RetinAI Medical AG

11.10. Optomed Plc

11.11. VisionQuest Biomedical Inc.

11.12. DeepMind Technologies Limited

11.13. Thirona

11.14. Lunit Inc.

11.15. Vuno Inc.

11.16. Remidio Innovative Solutions

11.17. Artelus

11.18. Selvas AI Inc.

11.19. IBM Corporation

11.20. Orbis International

12. Appendix

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Feb-2026

Subscribe to get the latest industry updates