Resources

About Us

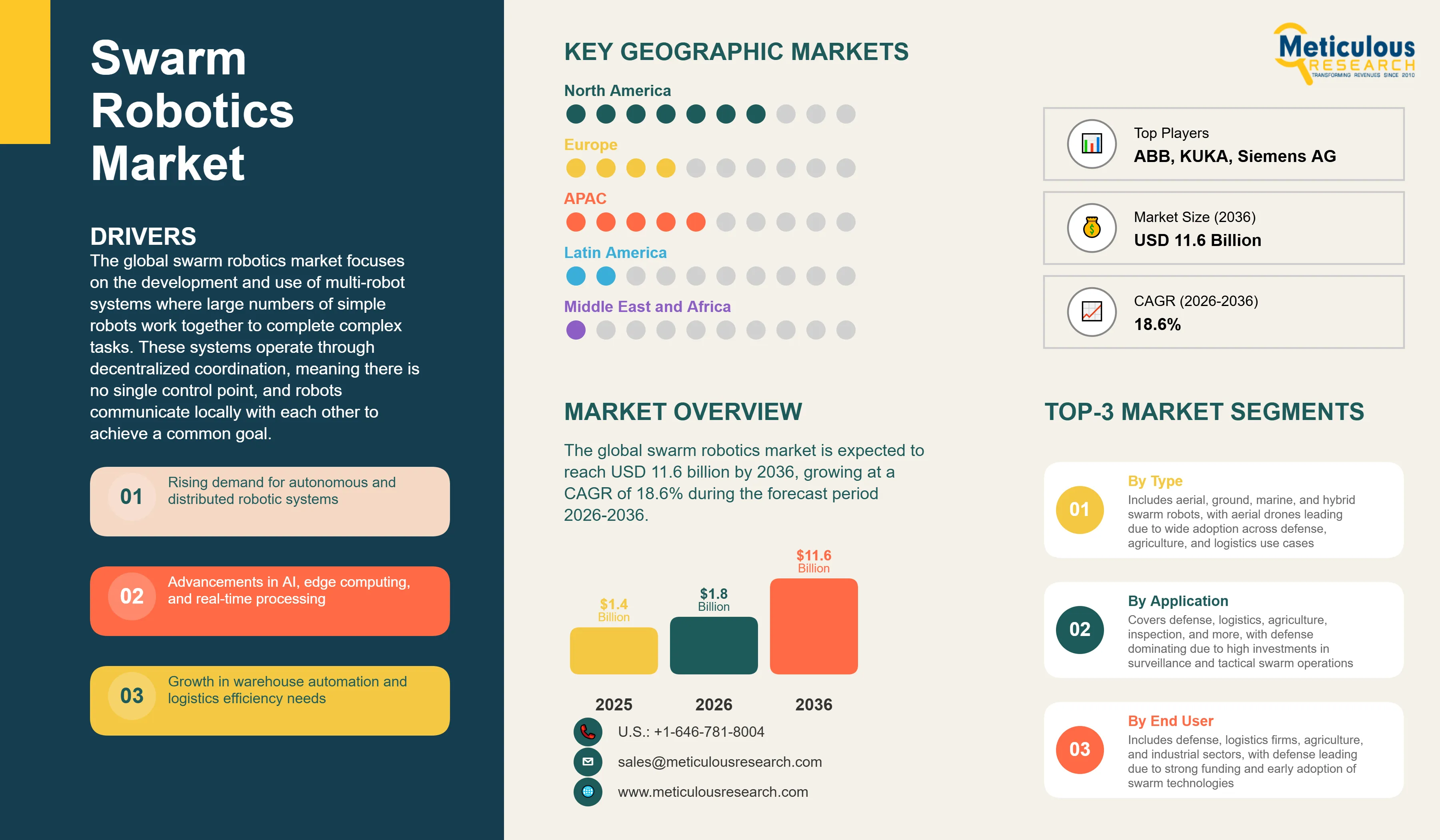

The global swarm robotics market was valued at USD 1.4 billion in 2025. This market is expected to reach USD 11.6 billion by 2036 from an estimated USD 1.8 billion in 2026, growing at a CAGR of 18.6% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

The global swarm robotics market focuses on the development and use of multi-robot systems where large numbers of simple robots work together to complete complex tasks. These systems operate through decentralized coordination, meaning there is no single control point, and robots communicate locally with each other to achieve a common goal.

The market includes different types of swarm systems such as aerial drones and UAV swarms, ground-based robots (wheeled, tracked, or legged), marine robots (surface and underwater), and hybrid systems that combine multiple environments. These solutions are used across a wide range of applications, including defense and surveillance, warehouse automation, agriculture, infrastructure inspection, environmental monitoring, and disaster response. Deployment can vary from fully autonomous systems to those that are partially or fully controlled by humans.

Market growth is being driven by advancements in key technologies. These include embedded AI chips that allow robots to process data and make decisions individually, low-latency communication networks that enable real-time coordination between robots, and ongoing miniaturization of sensors, batteries, and computing hardware. Together, these developments are making swarm robots more capable and cost-effective.

Defense remains the primary driver of demand in the near term. Government programs, especially in the U.S., China, Israel, and the U.K., are investing heavily in drone swarm technologies for tactical and surveillance applications. These investments are also helping accelerate the development of technologies that can later be used in commercial sectors.

However, the market still faces some challenges. Coordinating large numbers of robots without centralized control is complex, particularly in dynamic and unpredictable environments. Ensuring smooth communication, avoiding collisions, and maintaining system reliability at scale are still evolving areas. In addition, regulations for autonomous multi-robot systems—especially drone swarms operating in shared airspace—are still developing and vary across regions, which creates uncertainty for commercial deployment.

Despite these challenges, the market is steadily progressing. Advances in swarm algorithms, along with the use of simulation platforms like Gazebo, ROS2, and NVIDIA Isaac Sim, are helping improve system performance and speed up development. At the same time, regulatory bodies in regions such as the U.S., Europe, and the U.K. are working toward clearer frameworks for autonomous operations.

Early commercial use cases in warehouse automation, agriculture, and drone-based events are also demonstrating real-world viability. These developments are building confidence in the technology and supporting increased investment, positioning swarm robotics as a high-growth market with strong long-term potential.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 11.6 Billion |

|

Market Size in 2026 |

USD 1.8 Billion |

|

Market Size in 2025 |

USD 1.4 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 18.6% |

|

Dominating Robot Type |

Aerial Swarm Robots (Drones/UAVs) |

|

Fastest Growing Robot Type |

Hybrid and Multi-Domain Swarms |

|

Dominating Control Architecture |

Hybrid Control Systems |

|

Fastest Growing Control Architecture |

Fully Decentralized Swarm Systems |

|

Dominating Communication Technology |

RF Communication |

|

Fastest Growing Communication |

5G/6G Communication |

|

Dominating Application |

Defense and Security |

|

Fastest Growing Application |

Emerging Applications (Smart Cities, Space) |

|

Dominating End User |

Defense and Military |

|

Fastest Growing End User |

Logistics and E-commerce Companies |

|

Dominating Deployment Mode |

Semi-Autonomous Swarms |

|

Fastest Growing Deployment Mode |

Fully Autonomous Swarms |

|

Dominating Swarm Size |

Medium Swarms (10 to 100 Robots) |

|

Fastest Growing Swarm Size |

Large Swarms (100 or More Robots) |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Increasing Adoption of Autonomous and Distributed Systems

A major driver of the swarm robotics market is the growing shift toward autonomous and distributed systems across defense, logistics, and industrial sectors. Organizations are increasingly looking to reduce human involvement in repetitive, risky, or large-scale operations, and swarm robotics offers a scalable solution.

In the defense sector, swarm systems are gaining traction as they can operate in high-risk environments where human involvement is limited. Instead of relying on a single unmanned system, multiple low-cost drones can work together, making operations more flexible and difficult for adversaries to counter.

In logistics, companies are adopting swarm-based automation to improve efficiency and handle large volumes. For example, warehouse systems using fleets of robots are already proving successful, encouraging wider adoption across e-commerce, retail, and third-party logistics providers. This is creating strong demand for swarm-inspired automation globally.

Advancements in AI, Edge Computing, and Communication Technologies

Technological advancements are another key driver supporting market growth. Improvements in AI processing, edge computing, and communication networks are making swarm robotics more practical and scalable. Modern robots are now equipped with onboard AI capabilities, allowing them to process data, avoid obstacles, and coordinate with other robots in real time without relying heavily on cloud connectivity. At the same time, advancements in communication technologies—especially 5G and mesh networks—enable fast and reliable communication between large numbers of robots.

Additionally, the miniaturization of sensors, processors, and batteries is reducing costs and improving performance. These developments are making it economically feasible to deploy large swarms consisting of hundreds or even thousands of robots, which was previously difficult due to hardware and cost limitations.

Integration with 5G/6G and Edge AI

The rollout of private 5G networks across locations such as military bases, warehouses, ports, and farms is creating strong opportunities for swarm robotics. These networks provide fast, reliable, and low-latency communication, which is essential for coordinating large numbers of robots in real time—something that traditional Wi-Fi or RF systems cannot handle effectively.

Private 5G also offers features like guaranteed network performance, accurate positioning, and the ability to separate swarm communication from other network traffic. Looking ahead, the introduction of 6G in the early 2030s is expected to further enhance capabilities with even faster speeds and near-instant communication, enabling more advanced and synchronized swarm operations.

As a result, companies are developing 5G-enabled swarm systems that can operate at larger scales with better coordination and responsiveness, opening up new commercial and industrial use cases.

Expansion in Warehouse Automation and Smart Logistics

The rapid growth of e-commerce is creating strong demand for advanced warehouse automation solutions that can handle high volumes, faster delivery timelines, and operational flexibility. Swarm robotics is well-suited for this environment due to its scalability, reliability, and adaptability.

Unlike fixed automation systems, swarm robotics allows companies to easily scale operations by adding more robots without redesigning the entire system. It also offers higher reliability, as the system can continue functioning even if individual robots fail. Additionally, tasks can be dynamically reassigned based on real-time demand, improving overall efficiency.

Large-scale deployments by leading companies have already proven the effectiveness of this model, and it is now being adopted by a broader range of e-commerce players and logistics providers. This trend is creating significant growth opportunities for swarm robotics in the global logistics and supply chain sector.

Defense Programs Driving Tactical Drone Swarm Commercialization

Large-scale defense programs are playing a key role in accelerating the commercialization of drone swarm technologies. Governments are heavily investing in swarm systems for military use, and these investments are helping advance the technology, reduce costs, and build real-world operational experience.

For example, defense programs in the U.S. and China have successfully demonstrated large-scale coordinated drone operations involving hundreds to thousands of drones. These developments are not only strengthening military capabilities but also creating a strong foundation for commercial applications.

As the technology matures and production scales up, costs are decreasing, making swarm solutions more accessible for industries such as agriculture, infrastructure inspection, and entertainment (e.g., drone light shows). In this way, defense investments are indirectly driving growth in the commercial swarm robotics market.

Hybrid and Multi-Domain Swarms Emerging as a High-Value Segment

Another important opportunity is the development of hybrid swarm systems that operate across multiple environments—air, ground, and water. These multi-domain swarms combine the strengths of different types of robots to perform more complex and high-value tasks.

For instance, aerial drones can provide surveillance and mapping, while ground robots handle inspection or physical tasks in confined spaces, and marine robots support underwater or coastal operations. Together, these systems can complete missions that a single type of robot cannot handle alone.

This approach is gaining traction in both defense and commercial sectors, with increasing focus on coordinated operations across domains. Early developments are already emerging, and this segment is expected to become a high-value area within the swarm robotics market due to its advanced capabilities and broader application potential.

By Robot Type: In 2026, Aerial Swarm Robots to Dominate

Based on robot type, the swarm robotics market is segmented into aerial swarm robots (drones/UAVs), ground swarm robots, marine swarm robots, and hybrid or multi-domain swarms.

In 2026, aerial swarm robots are expected to dominate the market. This is because drones are currently the most mature and widely used swarm technology. They benefit from large-scale manufacturing, relatively clearer regulations for commercial use, and strong adoption across multiple applications such as surveillance, infrastructure inspection, agriculture, and entertainment. In addition, both defense programs and commercial applications, such as drone light shows and advertising, are already deploying large numbers of coordinated drones. This has created the largest installed base of swarm systems, making aerial robots the leading segment in terms of market share.

However, hybrid and multi-domain swarms are expected to grow at the fastest rate during the forecast period. These systems combine aerial, ground, and marine robots to deliver more advanced capabilities. By leveraging the strengths of each type of robot, they can handle complex tasks that single-domain systems cannot perform. This segment is attracting strong investment from both defense and commercial sectors, particularly for applications requiring coordination across multiple environments. As a result, hybrid swarm systems are expected to emerge as a high-growth, high-value segment in the coming years.

By Control Architecture: In 2026, Hybrid Control Systems to Hold the Largest Share

Based on control architecture, the swarm robotics market is segmented into fully decentralized systems, centralized systems, and hybrid control systems. This is an important classification, as the control approach directly impacts scalability, reliability, and operational complexity.

In 2026, hybrid control systems are expected to hold the largest market share. This reflects the current commercial reality, where most deployments combine the strengths of both centralized and decentralized approaches. In these systems, a central platform handles overall planning and monitoring, while individual robots make real-time decisions such as navigation and collision avoidance. This balance ensures better control, efficiency, and safety. For example, in warehouse automation, companies are using centralized systems for task allocation while allowing robots to operate independently on the ground. This hybrid approach has become the standard for large-scale commercial deployments.

However, fully decentralized systems are expected to grow at the fastest rate during the forecast period. These systems allow robots to operate entirely without central control, making them more scalable and resilient, especially in environments where communication is limited or unreliable. Advancements in swarm intelligence and AI are enabling more effective decentralized coordination, making these systems increasingly suitable for applications such as defense, disaster response, and exploration.

By Communication Technology: In 2026, RF Communication to Hold the Largest Share

Based on communication technology, the swarm robotics market is segmented into RF communication, mesh networks, 5G/6G communication, and satellite communication. In 2026, RF communication is expected to hold the largest market share. This is because most current swarm systems, especially drones and ground robots, rely on RF technologies operating in sub-GHz and 2.4 GHz bands. These solutions are widely used due to their long range, good signal penetration, low cost, and proven reliability. Standard RF protocols and proprietary mesh-based RF systems are already well established and support effective communication for most existing swarm deployments within controlled environments.

However, 5G/6G communication is expected to grow at the fastest rate during the forecast period. The increasing deployment of private 5G networks in warehouses, defense sites, and agricultural operations is enabling faster, more reliable, and low-latency communication—critical for coordinating large-scale swarms with hundreds of robots in real time.Looking ahead, the expected rollout of 6G in the early 2030s will further enhance connectivity with ultra-low latency and higher data speeds, enabling more advanced and large-scale swarm operations.

By Application: In 2026, Defense and Security to Hold the Largest Share

Based on application, the swarm robotics market is segmented into defense and security, logistics and warehousing, agriculture, industrial and infrastructure inspection, environmental monitoring, disaster management and search & rescue, and emerging applications.

In 2026, defense and security is expected to hold the largest market share. This is mainly because defense projects involve very high contract values and significant government funding. Programs in countries like the U.S., China, and Israel are heavily investing in drone swarm technologies for surveillance, tactical operations, and autonomous missions.The defense sector also plays a key role in advancing swarm technology, as it is willing to invest in early-stage innovations and accept higher initial costs. This results in faster development and deployment compared to most commercial applications.

However, emerging applications are expected to grow at the fastest rate during the forecast period. This segment includes new and innovative use cases such as smart city traffic management, drone-based entertainment shows, urban delivery systems, and space exploration. For example, synchronized drone shows are already being used for large-scale events, while companies are testing drone swarms for last-mile delivery in urban areas. In addition, space agencies are exploring the use of robot swarms for future missions to the Moon and Mars.

By End User: In 2026, Defense and Military to Hold the Largest Share

Based on end user, the global swarm robotics market is segmented into defense and military, logistics and e-commerce companies, agriculture sector, industrial enterprises, and government and research institutions. In 2026, the defense and military segment is expected to account for the largest share. This aligns with the overall dominance of defense spending in swarm robotics. Military organizations across countries such as the U.S., U.K., China, and Israel are major adopters, investing heavily in swarm technologies for surveillance, tactical operations, and autonomous missions. Defense contracts are typically large, long-term, and high-value, providing stable revenue streams for vendors. These investments also support ongoing research and development, making defense the most influential end-user segment in the market

However, logistics and e-commerce companies are expected to grow at the fastest rate during the forecast period. The rapid expansion of e-commerce is putting pressure on fulfillment operations to become faster, more efficient, and cost-effective. Swarm-based warehouse automation has already demonstrated strong returns for leading companies, encouraging wider adoption across the industry. As more companies expand their fulfillment networks, the deployment of robot swarms for sorting, picking, and material movement is expected to increase significantly.

By Swarm Size: In 2026, Medium Swarms (10 to 100 Robots) to Hold the Largest Share

Based on swarm size, the global swarm robotics market is segmented into small swarms (2 to 10 robots), medium swarms (10 to 100 robots), and large swarms (100 or more robots). In 2026, the medium swarms segment is expected to account for the largest share of the market. These deployments offer the right balance between performance and cost. They are large enough to deliver meaningful operational benefits, while still being manageable in terms of coordination and infrastructure requirements. Most current commercial applications—such as warehouse automation, agriculture, and inspection—operate within this range, as existing technologies can efficiently support this level of scale.

However, large swarms (100+ robots) are expected to grow at the fastest rate during the forecast period. This growth is being driven by increasing demand for high-scale operations, particularly in defense, logistics, and agriculture. In defense, there is a strong focus on deploying large numbers of low-cost drones for tactical missions. In logistics, large fulfillment centers are expanding automation with bigger robot fleets. Similarly, in agriculture, covering large land areas efficiently requires higher numbers of coordinated robots.

Swarm Robotics Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global swarm robotics market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global swarm robotics market. This is mainly due to the strong presence of the United States as both the largest investor and innovator in swarm robotics. The U.S. government is heavily funding research and development through defense programs, while leading companies are actively developing and deploying advanced swarm solutions. In addition, large-scale commercial adoption, especially in warehouse automation and logistics, has strengthened the region’s leadership. The presence of a strong technology ecosystem and early adoption of advanced robotics continues to drive market growth in North America.

However, Asia-Pacific is expected to register the highest growth rate during the forecast period. This growth is driven by a combination of large-scale manufacturing capabilities, rising demand for automation, and increasing investments in robotics and drone technologies. China plays a key role as a major producer of drones and a growing technology innovator. At the same time, countries like Japan, South Korea, Australia, and India are expanding their investments in robotics, agriculture automation, and defense technologies. The rapid growth of e-commerce, smart agriculture, and industrial automation across the region is further accelerating the adoption of swarm robotics.

Key players operating in the global swarm robotics market include SwarmFarm Robotics (Australia), DJI/SZ DJI Technology Co. Ltd. (China), Lockheed Martin Corporation (U.S.), Elbit Systems Ltd. (Israel), Northrop Grumman Corporation (U.S.), Parrot Drones SAS (France), Boston Dynamics Inc. (U.S.), ABB Ltd. (Switzerland), KUKA AG (Germany), Siemens AG (Germany), NVIDIA Corporation (U.S.), Clearpath Robotics Inc. (Canada), Locus Robotics Corp. (U.S.), GreyOrange Pte Ltd. (Singapore), and AgEagle Aerial Systems Inc. (U.S.), among others.

The global swarm robotics market is expected to reach USD 11.6 billion by 2036 from an estimated USD 1.8 billion in 2026, at a CAGR of 18.6% during the forecast period 2026-2036.

In 2026, aerial swarm robots (drones/UAVs) is expected to hold the largest share, driven by the mature commercial drone platform ecosystem, broad applicability across defense, agriculture, inspection, and entertainment use cases, and the largest existing installed base of coordinated swarm deployments of any robot type.

Hybrid and multi-domain swarms is expected to register the highest CAGR during the forecast period. This emerging high-value segment combines aerial, ground, and marine agents for complex missions that no single-domain swarm can perform, attracting significant defense and commercial R&D investment through the forecast period.

Control architecture determines the fundamental scalability, resilience, and operational characteristics of a swarm system. Fully decentralized architectures scale to large swarm sizes without communication bottlenecks but are harder to predict and oversee. Centralized architectures offer predictability but create single points of failure that limit scalability and resilience. Hybrid architectures balance these trade-offs and currently dominate commercial deployments, making this the most consequential design choice in swarm system development that directly influences performance, cost, and regulatory approvability.

Swarm size determines the coordination algorithm complexity, communication infrastructure requirements, software orchestration sophistication, and economic viability of each deployment. Small swarms (2 to 10 robots) are addressable with simple coordination approaches and minimal infrastructure. Medium swarms (10 to 100 robots) require dedicated coordination middleware and represent the current commercial sweet spot. Large swarms of 100 or more robots demand advanced decentralized algorithms, high-capacity communication networks, and sophisticated simulation and testing environments. Understanding swarm size distribution within each application is essential for accurate market sizing and technology roadmap alignment.

Emerging applications including smart city traffic management, entertainment drone shows, and space exploration swarms is projected to register the highest CAGR during the forecast period. This segment encompasses frontier commercial applications at the intersection of swarm robotics and adjacent technology trends including urban air mobility, AI-driven smart infrastructure, and space robotics that will define the next wave of commercial swarm deployment beyond the established defense, logistics, and agriculture verticals.

Growth is primarily driven by the structural adoption of autonomous distributed systems in defense, logistics, and agriculture that demands scalable multi-robot coordination, the convergence of embedded AI, 5G connectivity, and miniaturized sensor hardware enabling capable swarm agents at commercially viable costs, large-scale defense investment in tactical drone swarm programs that advance the underlying technology base for commercial applications, and the demonstrated commercial ROI of swarm-inspired warehouse automation driving rapid expansion across global e-commerce logistics networks.

Asia-Pacific is expected to register the highest growth rate during the forecast period 2026-2036, driven by China's leading drone manufacturing scale and military swarm programs, Australia's commercial agricultural swarm adoption, Japan's advanced industrial robotics ecosystem, South Korea's defense and electronics manufacturing swarm investment, and India's rapidly growing drone sector supported by the Production Linked Incentive scheme for domestic drone manufacturing.

Key players are SwarmFarm Robotics (Australia), DJI/SZ DJI Technology Co. Ltd. (China), Lockheed Martin Corporation (U.S.), Elbit Systems Ltd. (Israel), Northrop Grumman Corporation (U.S.), Parrot Drones SAS (France), Boston Dynamics Inc. (U.S.), ABB Ltd. (Switzerland), KUKA AG (Germany), Siemens AG (Germany), NVIDIA Corporation (U.S.), Clearpath Robotics Inc. (Canada), Locus Robotics Corp. (U.S.), GreyOrange Pte Ltd. (Singapore), and AgEagle Aerial Systems Inc. (U.S.), among others.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection and Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research and Validation

2.2.2.1. Primary Interviews with Experts

2.2.2.2. Approaches for Country/Region-Level Analysis

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.2. Restraints

4.2.3. Opportunities

4.2.4. Challenges

4.3. Technology Landscape

4.3.1. Swarm Intelligence Algorithms

4.3.2. Multi-Agent Systems and Distributed AI

4.3.3. Communication Technologies (RF, Mesh Networks, 5G)

4.3.4. Edge Computing and Onboard Processing

4.3.5. Sensor Fusion and Perception Systems

4.4. Swarm Robotics Architecture

4.4.1. Decentralized Coordination Frameworks

4.4.2. Inter-Robot Communication Protocols

4.4.3. Collective Behavior and Task Allocation

4.4.4. Human-Swarm Interaction Interfaces

4.4.5. Simulation and Digital Twin Environments

4.5. Value Chain Analysis

4.5.1. Component Suppliers (Sensors, Chips, Batteries)

4.5.2. Robot Manufacturers

4.5.3. Software and AI Developers

4.5.4. System Integrators

4.5.5. End Users

4.6. Regulatory and Standards Landscape

4.6.1. Robotics and AI Regulations

4.6.2. UAV/Drone Regulations (for Aerial Swarms)

4.6.3. Safety and Operational Standards

4.7. Porter's Five Forces Analysis

4.8. Investment and Industry Trends

4.8.1. Funding in Autonomous Robotics Startups

4.8.2. Defense Investments in Swarm Systems

4.8.3. Commercial Adoption in Logistics and Agriculture

5. Swarm Robotics Market, by Robot Type

5.1. Introduction

5.2. Aerial Swarm Robots (Drones/UAVs)

5.2.1. Fixed-Wing Drones

5.2.2. Rotary-Wing Drones

5.2.3. Hybrid UAV Systems

5.3. Ground Swarm Robots

5.3.1. Wheeled Robots

5.3.2. Tracked Robots

5.3.3. Legged Robots

5.4. Marine Swarm Robots

5.4.1. Surface Vehicles (USVs)

5.4.2. Underwater Vehicles (AUVs)

5.5. Hybrid and Multi-Domain Swarms

6. Swarm Robotics Market, by Control Architecture

6.1. Introduction

6.2. Fully Decentralized Swarm Systems

6.3. Centralized Control Systems

6.4. Hybrid Control Systems

7. Swarm Robotics Market, by Communication Technology

7.1. Introduction

7.2. RF Communication

7.3. Mesh Networks

7.4. 5G/6G Communication

7.5. Satellite Communication

8. Swarm Robotics Market, by Application

8.1. Introduction

8.2. Defense and Security Applications

8.2.1. Surveillance and Reconnaissance

8.2.2. Border Security and Patrol

8.2.3. Combat and Tactical Operations

8.2.4. Mine Detection and Clearance

8.3. Logistics and Warehousing

8.3.1. Warehouse Automation

8.3.2. Inventory Management

8.3.3. Order Picking and Fulfillment

8.4. Agriculture Applications

8.4.1. Crop Monitoring

8.4.2. Precision Spraying

8.4.3. Harvesting Support

8.5. Industrial and Infrastructure Inspection

8.5.1. Oil and Gas Inspection

8.5.2. Power Line and Utility Inspection

8.5.3. Construction Site Monitoring

8.6. Environmental Monitoring

8.6.1. Climate and Weather Monitoring

8.6.2. Wildlife Tracking

8.6.3. Pollution Monitoring

8.7. Disaster Management and Search and Rescue

8.7.1. Post-Disaster Assessment

8.7.2. Search and Rescue Operations

8.8. Emerging Applications (Fastest-Growing Segment)

8.8.1. Smart Cities and Traffic Management

8.8.2. Entertainment and Drone Shows

8.8.3. Space Exploration Swarms

9. Swarm Robotics Market, by End User

9.1. Introduction

9.2. Defense and Military

9.3. Logistics and E-commerce Companies

9.4. Agriculture Sector

9.5. Industrial Enterprises

9.6. Government and Research Institutions

10. Swarm Robotics Market, by Deployment Mode

10.1. Introduction

10.2. Fully Autonomous Swarms

10.3. Semi-Autonomous Swarms

10.4. Human-in-the-Loop Systems

11. Swarm Robotics Market, by Swarm Size

11.1. Introduction

11.2. Small Swarms (2 to 10 Robots)

11.3. Medium Swarms (10 to 100 Robots)

11.4. Large Swarms (100 or More Robots)

12. Swarm Robotics Market, by Geography

12.1. Introduction

12.2. North America

12.2.1. U.S.

12.2.2. Canada

12.3. Europe

12.3.1. Germany

12.3.2. U.K.

12.3.3. France

12.3.4. Italy

12.3.5. Spain

12.3.6. Netherlands

12.3.7. Sweden

12.3.8. Switzerland

12.3.9. Rest of Europe

12.4. Asia-Pacific

12.4.1. China

12.4.2. India

12.4.3. Japan

12.4.4. South Korea

12.4.5. Australia

12.4.6. Singapore

12.4.7. Indonesia

12.4.8. Thailand

12.4.9. Vietnam

12.4.10. Rest of Asia-Pacific

12.5. Latin America

12.5.1. Brazil

12.5.2. Mexico

12.5.3. Argentina

12.5.4. Chile

12.5.5. Colombia

12.5.6. Rest of Latin America

12.6. Middle East and Africa

12.6.1. UAE

12.6.2. Saudi Arabia

12.6.3. Israel

12.6.4. Turkey

12.6.5. South Africa

12.6.6. Rest of Middle East and Africa

13. Competitive Landscape

13.1. Overview

13.2. Key Growth Strategies

13.3. Competitive Benchmarking

13.4. Competitive Dashboard

13.4.1. Industry Leaders

13.4.2. Market Differentiators

13.4.3. Vanguards

13.4.4. Emerging Companies

13.5. Market Ranking/Positioning Analysis of Key Players, 2025

14. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

14.1. SwarmFarm Robotics

14.2. DJI (SZ DJI Technology Co., Ltd.)

14.3. Lockheed Martin Corporation

14.4. Elbit Systems Ltd.

14.5. Northrop Grumman Corporation

14.6. Parrot Drones SAS

14.7. Boston Dynamics, Inc.

14.8. ABB Ltd.

14.9. KUKA AG

14.10. Siemens AG

14.11. NVIDIA Corporation

14.12. Clearpath Robotics Inc.

14.13. Locus Robotics Corp.

14.14. GreyOrange Pte Ltd.

14.15. AgEagle Aerial Systems Inc.

15. Appendix

15.1. Additional Customization

15.2. Related Reports

Published Date: May-2025

Published Date: Nov-2024

Published Date: Nov-2022

Published Date: Jun-2024

Subscribe to get the latest industry updates