Resources

About Us

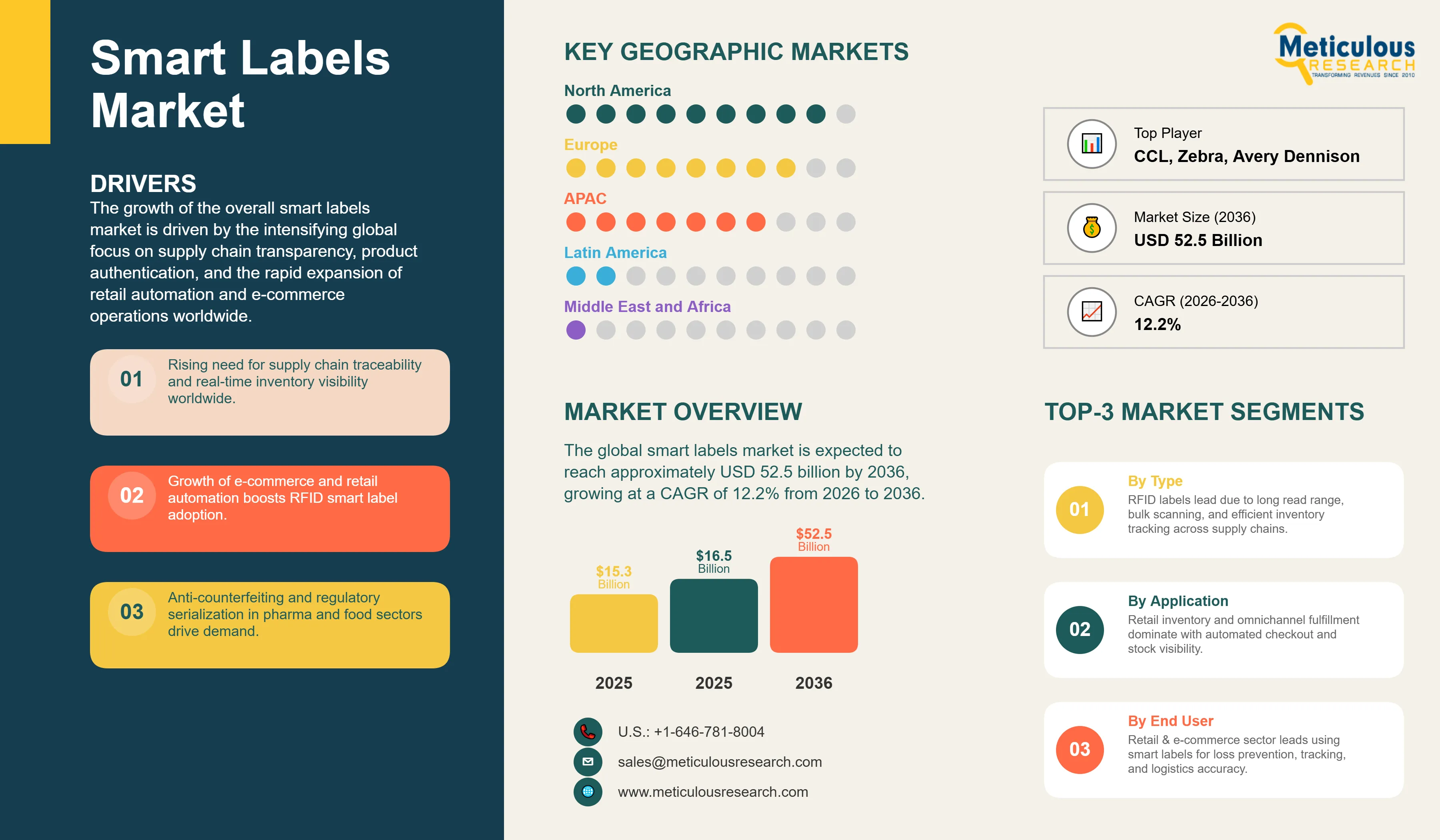

The global smart labels market was valued at USD 15.3 billion in 2025. The market is expected to reach approximately USD 52.5 billion by 2036 from USD 16.5 billion in 2026, growing at a CAGR of 12.2% from 2026 to 2036. The growth of the overall smart labels market is driven by the intensifying global focus on supply chain transparency, product authentication, and the rapid expansion of retail automation and e-commerce operations worldwide. As brand owners, retailers, and logistics providers seek to integrate advanced tracking and real-time data capabilities into physical goods, smart label technology has become indispensable for achieving end-to-end visibility, inventory accuracy, and enhanced consumer engagement. The rapid rollout of item-level RFID mandates by major global retailers, the growing regulatory requirements for pharmaceutical serialization and food traceability, and the accelerating adoption of electronic shelf labels in omnichannel retail continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Smart labels are electronically enhanced identification and data-communication solutions embedded with technologies such as radio frequency identification (RFID), near field communication (NFC), electronic article surveillance (EAS), electronic shelf label (ESL) systems, and condition-sensing elements. Unlike traditional barcodes, smart labels are capable of storing, receiving, and transmitting digital data without requiring direct line-of-sight scanning, allowing for real-time, automated identification and monitoring of individual items throughout their entire lifecycle — from manufacturing and warehousing to the retail floor and final delivery. The market encompasses a broad range of solutions, from high-volume passive UHF RFID inlays used in apparel and consumer goods to sophisticated active sensor labels monitoring the temperature and humidity of high-value pharmaceutical shipments.

These labels are increasingly integrated with cloud-based data platforms, IoT connectivity, and AI-driven analytics to provide services such as real-time inventory reconciliation, product authentication, cold-chain condition monitoring, and interactive consumer engagement. Manufacturers like Avery Dennison and Impinj have built comprehensive digital ecosystems around their label hardware, enabling end-users to connect physical goods to cloud-based digital twins and draw actionable supply chain intelligence at scale. The ability to deliver precise, item-level traceability while reducing manual labor and human error has made smart labels the technology of choice for enterprises where operational efficiency, brand integrity, and regulatory compliance are critical priorities.

The global retail and consumer goods sector continues to push hard to modernize its operational infrastructure, aiming to meet consumer expectations for product transparency, faster fulfillment, and authentic goods. This shift has accelerated the adoption of item-level smart labeling, with advanced RFID and NFC solutions helping to eliminate stock discrepancies, improve on-shelf availability, and enable seamless self-checkout and omnichannel experiences. Simultaneously, the healthcare and pharmaceutical industries are subject to increasingly stringent serialization and track-and-trace mandates globally, driving sustained demand for smart labels capable of supporting unique device identification (UDI) and drug supply chain security requirements. The convergence of these regulatory, commercial, and technological forces is creating a compelling long-term growth environment across the smart labels market.

Accelerating Item-Level RFID Adoption Driven by Retail Giants and E-commerce Expansion

Global retailers are rapidly scaling their item-level RFID programs well beyond apparel into hard goods, grocery, and general merchandise categories. Major retailers including Walmart and Target have progressively expanded their RFID tagging requirements across supplier networks, triggering high-volume demand for passive UHF RFID inlays from manufacturers such as Avery Dennison and Alien Technology. At the same time, the explosive growth of e-commerce fulfillment operations has created a compelling need for high-speed, automated label reading systems capable of processing thousands of individual items per hour without manual intervention. These developments are driving manufacturers to invest in next-generation inlay designs with improved read sensitivity, smaller form factors, and on-metal performance to support the expanding range of product categories being tagged at the item level.

Electronic shelf labels represent another significant growth vector within the retail segment, with VusionGroup and SES-imagotag deploying cloud-connected ESL systems across tens of thousands of stores globally. These systems allow retailers to automate price updates, reduce labor costs, and synchronize online and in-store pricing in real time — capabilities that have become operationally essential in the competitive omnichannel environment. The integration of ESL platforms with broader inventory management and retail analytics systems is further strengthening the strategic value proposition of smart labels for large-format and convenience retailers alike.

Innovation in Sustainable Smart Labels and Sensor-Embedded Condition Monitoring

The smart labels industry is undergoing a significant material science transformation as manufacturers respond to growing regulatory and corporate sustainability mandates. Leading inlay producers, including Avery Dennison and Tageos, are actively developing RFID and NFC inlays using paper-based substrates, recycled PET liners, and biodegradable antenna materials designed to align with extended producer responsibility regulations in Europe and voluntary circular economy commitments by major brands. These innovations address one of the most persistent criticisms of smart label adoption — the difficulty of recycling labels that combine paper or film substrates with embedded electronic components — and are opening new market opportunities with sustainability-focused brand owners in the fast-moving consumer goods and premium goods segments.At the same time, the market is experiencing rapid growth in sensor-integrated smart labels capable of monitoring real-time environmental conditions such as temperature, humidity, shock, and light exposure throughout the supply chain. Companies including Identiv, Giesecke+Devrient, and Schreiner MediPharm are commercializing thin, flexible sensor labels for cold-chain pharmaceuticals, fresh food, and high-value logistics applications. The combination of shrinking sensor electronics, falling component costs, and the broader build-out of IoT connectivity infrastructure is making sensor-embedded smart labels increasingly viable for mid-market and high-volume applications — well beyond the specialized, premium use cases they were initially limited to.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 52.5 Billion |

|

Market Size in 2026 |

USD 16.5 Billion |

|

Market Size in 2025 |

USD 15.3 Billion |

|

Market Growth Rate (2026–2036) |

CAGR of 12.2% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Technology, Component, Form Factor, End-use, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Rising Demand for Supply Chain Traceability and Anti-counterfeiting Measures

A key driver of the smart labels market is the mounting pressure on businesses across industries to deliver complete, verifiable traceability of their products throughout the supply chain. Regulatory frameworks such as the U.S. Drug Supply Chain Security Act (DSCSA), the EU Falsified Medicines Directive (FMD), and food safety modernization regulations across North America, Europe, and Asia-Pacific are mandating item-level serialization and electronic track-and-trace capabilities across pharmaceutical, food and beverage, and consumer goods supply chains. Compliance with these regulations requires unique, machine-readable identifiers on individual product units — a requirement that smart labels, particularly RFID and NFC variants, are uniquely well-positioned to fulfill at scale. Beyond regulatory compliance, the staggering global cost of counterfeit goods — estimated to run into hundreds of billions of dollars annually across sectors including luxury goods, electronics, and pharmaceuticals — is driving brand owners to deploy smart labels with embedded authentication features as a frontline defense against product fraud and brand dilution.

Opportunity: Healthcare Digitalization and Cold-Chain Expansion in Emerging Markets

The rapid expansion of advanced healthcare delivery systems and the growing complexity of pharmaceutical distribution networks globally represent a major growth opportunity for the smart labels market. The increasing adoption of biologic therapies, mRNA-based vaccines, and precision medicines — all of which require tightly controlled cold-chain conditions — is driving demand for sensor-integrated labels capable of providing continuous, validated temperature and condition monitoring. Regulatory bodies including the U.S. FDA and the European Medicines Agency (EMA) are tightening requirements around cold-chain data integrity, further strengthening the business case for smart sensing labels in pharmaceutical logistics. At the same time, the rapid growth of organized retail, modern trade, and e-commerce infrastructure in emerging markets across Asia-Pacific, Latin America, and the Middle East is creating large, underpenetrated addressable markets for RFID-based inventory management and EAS-based loss prevention solutions, as retailers in these regions invest in upgrading their operational capabilities to compete with global players.

Why Does the RFID Labels Segment Lead the Market?

The RFID labels segment accounts for the largest share of the overall smart labels market in 2026. This dominant position is primarily attributed to the technology's unmatched combination of read range, simultaneous multi-tag scanning capability, data storage capacity, and no-line-of-sight reading advantages — characteristics that make RFID the preferred solution for high-throughput inventory management, automated logistics processing, and item-level tracking across large retail and distribution environments. Passive UHF RFID labels, in particular, have achieved highly competitive unit economics through decades of volume scaling, making item-level deployment financially viable across a broad range of product categories. Large retailers, third-party logistics providers, and contract manufacturers worldwide have made substantial investments in RFID reader infrastructure, creating a self-reinforcing adoption cycle that continues to expand the addressable market for RFID label manufacturers.

The electronic shelf label (ESL) segment is expected to witness the fastest growth during the forecast period. The widespread shift to omnichannel retail and the intensifying labor cost pressures facing brick-and-mortar retailers are creating a powerful economic justification for ESL deployment, as these systems eliminate the need for manual price-tag changes while enabling dynamic, real-time pricing synchronized with online channels. The rapid advancement of ESL display technologies — including color e-paper displays and NFC-based communication — combined with falling system costs are expanding the addressable market for ESL solutions beyond large-format grocery and hypermarket operators into convenience stores, pharmacies, and specialized retail formats.

How Does the Inlays & Antennas Segment Dominate?

Based on component, the inlays & antennas segment holds the largest share of the overall smart labels market in 2026. This is primarily due to the massive volume of RFID and NFC inlays manufactured annually to serve the retail, logistics, and healthcare end-use sectors, where inlays represent the essential functional element — the antenna and chip assembly — that is laminated into every finished smart label. Avery Dennison's Intelligent Labels division and Smartrac (now part of Avery Dennison) are the world's largest producers of RFID inlays, collectively manufacturing billions of units annually for a global customer base. Current large-scale deployments of item-level RFID in apparel, footwear, and general merchandise retail are creating sustained, high-volume demand for inlays that continues to grow as retailer mandates expand into new product categories.

The integrated circuits (ICs) segment is expected to witness the fastest growth during the forecast period. Semiconductor manufacturers including Impinj, NXP Semiconductors, and Murata Manufacturing are investing heavily in next-generation RFID and NFC chip architectures that offer enhanced memory capacity, improved read sensitivity, smaller physical dimensions, and integrated sensor capabilities. The growing demand for sensor-embedded smart labels capable of monitoring real-time environmental conditions is driving a new class of IC designs that integrate analog sensing elements directly on the chip, enabling a new generation of multi-function smart labels that can simultaneously track identity, location, and condition data.

Why Does the Retail & E-commerce Segment Lead the Market?

The retail & e-commerce segment commands the largest share of the global smart labels market in 2026. This dominance stems from the sector's high-volume, sustained demand for RFID-based inventory management, EAS loss-prevention systems, and electronic shelf labeling across its vast global store and fulfillment network footprint. The combination of large global retailers enforcing item-level RFID supplier mandates, the explosive growth of e-commerce fulfillment operations requiring automated order processing, and the growing deployment of ESL systems in brick-and-mortar stores collectively drive the retail and e-commerce sector's leading position. Advanced systems from providers like Avery Dennison, Zebra Technologies, and VusionGroup enable reliable performance at the scale and throughput required by the world's largest retail networks.

However, the healthcare & pharmaceuticals segment is poised for the strongest growth through 2036, fueled by expanding global regulatory requirements for pharmaceutical serialization, the rapid growth of biologics and cold-chain sensitive therapies, and the accelerating adoption of RFID-enabled medication management systems in hospital and clinical settings. Healthcare facilities face mounting pressure to optimize medication dispensing accuracy and improve asset utilization, where smart labels provide a cost-effective and scalable solution for tracking individual drug doses, medical devices, and surgical supplies in real time.

How is North America Maintaining Dominance in the Global Smart Labels Market?

North America holds the largest share of the global smart labels market in 2026. The region's leading position is primarily attributed to the early and deep adoption of RFID technology across its large-scale retail and logistics sectors, driven by influential retailer mandates and a well-developed technology supplier ecosystem. The United States alone accounts for a significant portion of global smart label consumption, with leading retailers across grocery, apparel, and general merchandise categories deploying RFID at scale. The U.S. pharmaceutical sector's compliance with the Drug Supply Chain Security Act (DSCSA) requirements has also generated substantial demand for serialized smart labels across the drug manufacturing and distribution supply chain. The presence of leading technology developers including Avery Dennison, Zebra Technologies, Impinj, Alien Technology, and Checkpoint Systems further underpins the region's market leadership through a continuous cycle of product innovation and commercial deployment.

Which Factors Support Asia-Pacific and European Market Growth?

Asia-Pacific is the fastest-growing regional market for smart labels and is expected to record the highest CAGR during the forecast period, driven by the rapid expansion of e-commerce infrastructure, strong government-backed smart manufacturing initiatives, and a growing retail modernization wave across China, India, South Korea, and Southeast Asia. China's position as the world's largest e-commerce market and its broad adoption of QR code-based consumer engagement systems have created a large and growing installed base for smart label technologies. India's manufacturing sector is also adopting RFID-based inventory and asset tracking at an accelerating pace, supported by government programs promoting industrial digitalization.

In Europe, stringent regulatory requirements for pharmaceutical serialization and food traceability, combined with strong corporate sustainability commitments driving demand for eco-friendly smart label solutions, are the primary growth catalysts. Countries including Germany, France, and the United Kingdom are at the forefront of smart label adoption, with significant investments in RFID-enabled supply chain transparency and ESL deployment in modern retail. Europe's leadership in sustainability regulations is also directly shaping product innovation among smart label manufacturers, who are developing recyclable, compostable, and reduced-electronic-waste label formats to meet the region's circular economy requirements.

Companies such as Avery Dennison Corporation, CCL Industries Inc., Zebra Technologies Corporation, and SATO Holdings Corporation lead the global smart labels market with comprehensive portfolios of RFID inlays, NFC labels, EAS solutions, and integrated labeling software platforms. Meanwhile, players including Impinj, Inc., NXP Semiconductors N.V., Alien Technology, LLC., and Murata Manufacturing Co., Ltd. focus on specialized semiconductor and inlay components that form the core of next-generation smart label architectures. Emerging manufacturers and integrated platform providers such as Smartrac Technology GmbH, Mühlbauer Group, Invengo Information Technology Co., Ltd., VusionGroup, Brady Corporation, Schreiner Group GmbH & Co. KG, Checkpoint Systems, Inc., and TOPPAN Holdings Inc. are strengthening the market through innovations in sustainable inlay materials, sensor-integrated labels, and cloud-connected smart label management platforms.

The global smart labels market is expected to grow from USD 16.5 billion in 2026 to USD 52.5 billion by 2036.

The global smart labels market is projected to grow at a CAGR of 12.2% from 2026 to 2036.

RFID labels are expected to dominate the market in 2026 due to their superior inventory tracking capabilities, no-line-of-sight scanning, and widespread retailer mandates. However, the electronic shelf label (ESL) segment is projected to be the fastest-growing technology segment, driven by the rapid adoption of automated pricing systems and omnichannel retail strategies in global retail environments.

IoT connectivity and AI analytics are transforming the smart labels landscape by enabling physical labels to serve as dynamic data nodes within broader digital supply chain ecosystems. Connected RFID and sensor labels, integrated with cloud platforms such as Avery Dennison's atma.io and Zebra's Savanna platform, allow companies to capture real-time location, condition, and authentication data at the item level. AI-driven analytics then process this data to generate actionable intelligence — such as predictive inventory replenishment, cold-chain exception alerts, and counterfeit detection — that directly improves operational efficiency, product quality, and consumer safety.

North America holds the largest share of the global smart labels market in 2026. The region's leadership is primarily attributed to the high penetration of RFID technology in retail and logistics, regulatory-driven pharmaceutical serialization demand, and the concentration of leading smart label technology developers and manufacturers.

The leading companies include Avery Dennison Corporation, CCL Industries Inc., Zebra Technologies Corporation, SATO Holdings Corporation, Impinj, Inc., NXP Semiconductors N.V., and Alien Technology, LLC.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Research Methodology

1.4. Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1. Introduction

3.2. Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.2.4. Challenges

3.3. Impact of IoT, AI, and Cloud Platforms on Smart Labels

3.4. Regulatory Landscape and Serialization Requirements

3.5. Porter's Five Forces Analysis

4. Global Smart Labels Market, by Technology

4.1. Introduction

4.2. RFID Labels

4.2.1. Passive RFID Labels

4.2.1.1. UHF (Ultra-High Frequency) RFID Labels

4.2.1.2. HF (High Frequency) RFID Labels

4.2.1.3. LF (Low Frequency) RFID Labels

4.2.2. Active RFID Labels

4.3. NFC Labels

4.3.1. NFC Authentication Labels

4.3.2. NFC Consumer Engagement Labels

4.4. Electronic Article Surveillance (EAS) Labels

4.4.1. Acousto-Magnetic (AM) EAS Labels

4.4.2. Radio Frequency (RF) EAS Labels

4.4.3. Electromagnetic (EM) EAS Labels

4.5. Electronic Shelf Labels (ESL)

4.5.1. E-Paper (E-Ink) Shelf Labels

4.5.2. LCD Shelf Labels

4.6. Sensing Labels

4.6.1. Temperature-Sensing Labels

4.6.2. Freshness & Gas-Sensing Labels

4.6.3. Humidity-Sensing Labels

4.7. Others (QR Code-Integrated Smart Labels, Printed Electronics Labels)

5. Global Smart Labels Market, by Component

5.1. Introduction

5.2. Inlays & Antennas

5.2.1. Wet Inlays

5.2.2. Dry Inlays

5.3. Integrated Circuits (ICs/Chips)

5.3.1. RFID Chips

5.3.2. NFC Chips

5.3.3. Sensor ICs

5.4. Batteries

5.4.1. Thin-Film Batteries

5.4.2. Printed Batteries

5.5. Substrates & Adhesives

5.5.1. Paper Substrates

5.5.2. Film & Synthetic Substrates

5.5.3. Specialty Adhesives

6. Global Smart Labels Market, by Form Factor

6.1. Introduction

6.2. Wet Inlay Labels

6.3. Dry Inlay Labels

6.4. Tag-Based Smart Labels

6.4.1. Hard Tags

6.4.2. Hang Tags

6.5. Printable Smart Labels

6.5.1. Pressure-Sensitive Printable Labels

6.5.2. In-Mold Labels

7. Global Smart Labels Market, by End-use

7.1. Introduction

7.2. Retail & E-commerce

7.2.1. Apparel & Footwear

7.2.2. General Merchandise & Hardlines

7.2.3. E-commerce Fulfillment

7.3. Food & Beverage

7.3.1. Fresh & Perishable Goods

7.3.2. Packaged Food & Beverages

7.3.3. Alcoholic Beverages & Premium Goods

7.4. Healthcare & Pharmaceuticals

7.4.1. Drug & Pharmaceutical Packaging

7.4.2. Medical Devices & Surgical Supplies

7.4.3. Hospital Asset & Medication Management

7.5. Logistics & Supply Chain

7.5.1. Parcel & Courier Services

7.5.2. Warehouse & Distribution Management

7.5.3. Cold Chain Logistics

7.6. Manufacturing & Automotive

7.6.1. Work-in-Process Tracking

7.6.2. Automotive Parts & Component Identification

7.6.3. Industrial Asset Tracking

7.7. Others (Consumer Electronics, Luxury Goods, Apparel Authentication)

8. Global Smart Labels Market, by Region

8.1. Introduction

8.2. North America

8.2.1. U.S.

8.2.2. Canada

8.3. Europe

8.3.1. Germany

8.3.2. France

8.3.3. U.K.

8.3.4. Italy

8.3.5. Spain

8.3.6. Netherlands

8.3.7. Rest of Europe

8.4. Asia-Pacific

8.4.1. China

8.4.2. India

8.4.3. Japan

8.4.4. South Korea

8.4.5. Southeast Asia

8.4.6. Australia

8.4.7. Rest of Asia-Pacific

8.5. Latin America

8.5.1. Brazil

8.5.2. Mexico

8.5.3. Rest of Latin America

8.6. Middle East & Africa

8.6.1. Saudi Arabia

8.6.2. UAE

8.6.3. South Africa

8.6.4. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Overview

9.2. Key Growth Strategies

9.3. Competitive Benchmarking

9.4. Competitive Dashboard

9.4.1. Industry Leaders

9.4.2. Market Differentiators

9.4.3. Vanguards

9.4.4. Emerging Companies

9.5. Market Ranking / Positioning Analysis of Key Players, 2025

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. Avery Dennison Corporation

10.2. CCL Industries Inc.

10.3. Zebra Technologies Corporation

10.4. SATO Holdings Corporation

10.5. Impinj, Inc.

10.6. NXP Semiconductors N.V.

10.7. Alien Technology, LLC.

10.8. Smartrac Technology GmbH

10.9. Mühlbauer Group

10.10. Invengo Information Technology Co., Ltd.

10.11. VusionGroup

10.12. Brady Corporation

10.13. Checkpoint Systems, Inc.

10.14. Schreiner Group GmbH & Co. KG

10.15. TOPPAN Holdings Inc.

10.16. Murata Manufacturing Co., Ltd.

11. Appendix

11.1. Questionnaire

11.2. Related Reports

Published Date: Oct-2024

Subscribe to get the latest industry updates