Resources

About Us

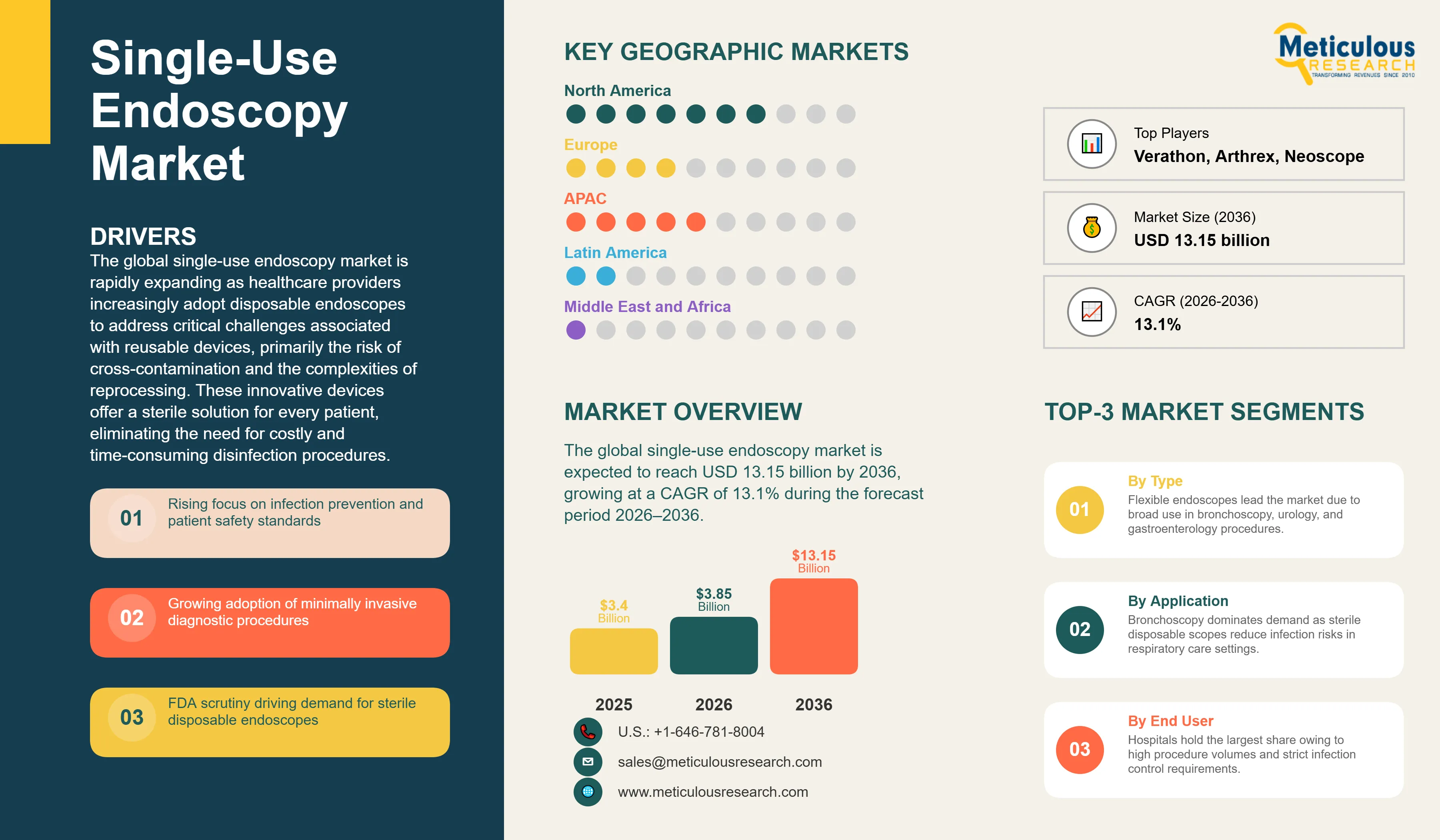

The global single-use endoscopy market is estimated to be USD 3.85 billion in 2026. This market is expected to reach USD 13.15 billion by 2036, growing at a CAGR of 13.1% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global single-use endoscopy market is rapidly expanding as healthcare providers increasingly adopt disposable endoscopes to address critical challenges associated with reusable devices, primarily the risk of cross-contamination and the complexities of reprocessing. These innovative devices offer a sterile solution for every patient, eliminating the need for costly and time-consuming disinfection procedures. The market encompasses a wide range of single-use endoscopes, including bronchoscopes, ureteroscopes, cystoscopes, and duodenoscopes, designed for various diagnostic and therapeutic applications. The shift towards single-use solutions is driven by a heightened focus on patient safety, regulatory pressures, and the desire to enhance operational efficiency in endoscopy suites and operating rooms.

Drivers: Mitigating Cross-Contamination Risks and Enhancing Operational Efficiency through Sterile, Single-Use Solutions

A key driver for the single-use endoscopy market is the persistent risk of cross-contamination associated with reusable endoscopes, even after rigorous reprocessing protocols. Published studies report that contamination in reusable duodenoscopes can still occur in a notable proportion of cases, depending on sampling methods and detection criteria, highlighting ongoing infection-control challenges in clinical practice. This has resulted in heightened regulatory scrutiny, including FDA safety communications and updated guidance focused on improving duodenoscope reprocessing and surveillance practices. Single-use endoscopes significantly reduce the risk of reprocessing-related cross-contamination by providing a sterile device for each procedure. In addition, the economic burden of reprocessing reusable endoscopes—including labor, sterilization time, and equipment downtime—adds substantial operational cost, with studies indicating meaningful increases in both procedure time and per-case expenses. These combined clinical and operational factors are accelerating the adoption of disposable endoscopy solutions across hospitals and ambulatory surgical centers.

Restraints: High Initial Costs and Environmental Concerns

Despite the compelling advantages, the single-use endoscopy market faces restraints, primarily concerning the higher per-procedure cost compared to reusable devices and growing environmental concerns. While single-use devices eliminate reprocessing costs, their individual unit cost can be higher, posing a challenge for budget-constrained healthcare systems. Additionally, the increased volume of medical waste generated by disposable endoscopes raises environmental sustainability concerns. Healthcare providers are increasingly seeking 'green' solutions, and the disposal of single-use devices contributes to the overall carbon footprint of healthcare. Manufacturers are actively exploring biodegradable materials and recycling programs to mitigate these environmental impacts, but it remains a significant consideration for widespread adoption.

Opportunities: Expansion into New Clinical Applications and Emerging Markets

Significant opportunities for growth lie in the expansion of single-use endoscopes into new clinical applications and emerging markets. The development of smaller, more versatile disposable endoscopes is opening doors for procedures in areas like neurosurgery, ENT, and peripheral vascular interventions, where traditional reusable scopes may be too large or pose higher infection risks. Emerging markets in Asia Pacific, Latin America, and the Middle East & Africa present substantial untapped potential. With increasing healthcare expenditure, expanding hospital networks, and a growing focus on infection control, these regions are poised for rapid adoption of single-use endoscopy solutions. The demand for immediate availability and sterility in critical care settings, such as ICUs, also drives the adoption of single-use bronchoscopes.

Increasing Focus on Infection Prevention and Patient Safety

The primary driver of the single-use endoscopy market is the intensified global focus on infection prevention and patient safety. The U.S. FDA has repeatedly issued safety communications on duodenoscopes, noting that design complexity can make complete reprocessing difficult even when IFU protocols are followed, contributing to documented infection transmission events. Complementing this, the CDC estimates that approximately 1 in 31 hospital patients in the U.S. acquires a healthcare-associated infection (HAI) on any given day, reinforcing the broader institutional push to reduce device-related infection risks. In addition, published clinical surveillance studies have reported residual contamination rates in reusable duodenoscopes ranging from ~5% to over 20% depending on sampling and detection methods, underscoring persistent reprocessing limitations. These concerns have driven hospitals and ambulatory surgical centers to increasingly adopt single-use endoscopes to eliminate reprocessing-associated cross-contamination risks and strengthen infection-control compliance.

Technological Advancements and Miniaturization

Technological innovation in miniaturization, optics, and sensor integration is significantly accelerating adoption of single-use endoscopy. Modern disposable platforms now incorporate high-definition CMOS imaging, chip-on-tip architectures, and advanced LED illumination, enabling visualization performance approaching reusable systems. Industry leaders have introduced devices supporting HD to near-4K visualization standards, improving diagnostic confidence in bronchoscopy, urology, and GI procedures. Additionally, enhanced distal tip articulation and reduced device diameter have expanded access to complex anatomical regions, particularly in pulmonary and urological applications. According to medtech industry analyses, improved imaging quality combined with reduced infection risk is a key factor driving double-digit (~10–15%+) adoption growth rates in single-use endoscopy across developed healthcare systems, particularly in high-volume hospital and ASC settings.

Analysis by Product

Based on product, the flexible endoscopes segment is expected to hold the largest share in 2026. This dominance is attributed to their versatility across a broad range of diagnostic and therapeutic procedures, including bronchoscopy, urology, and gastroenterology. The increasing demand for minimally invasive procedures and the ability of flexible scopes to navigate complex anatomies contribute to their market leadership. The rigid endoscopes segment is also growing, particularly for applications requiring greater precision and stability. The market is witnessing continuous innovation in both flexible and rigid single-use designs, focusing on improved optics, maneuverability, and integration with other surgical tools.

Analysis by Application

By application, the bronchoscopy segment is expected to account for the largest share in 2026. This is primarily driven by the critical need for sterile solutions in respiratory care, especially in intensive care units (ICUs) and during infectious disease outbreaks, where cross-contamination risks are high. The urology segment (ureteroscopy, cystoscopy) is projected to exhibit significant growth, fueled by the rising prevalence of urological conditions and the benefits of single-use ureteroscopes in reducing post-operative infections. The gastroenterology segment, particularly for duodenoscopy, is also a key area of growth due to past contamination concerns with reusable devices.

Analysis by End User

By end user, hospitals are expected to hold the largest share in 2026. Hospitals are the primary adopters due to the high volume of endoscopic procedures performed, the critical need for infection control, and the increasing emphasis on patient safety. Ambulatory surgical centers (ASCs) are projected to witness the fastest growth, driven by the shift of procedures from inpatient to outpatient settings, where single-use endoscopes offer significant advantages in terms of turnaround time, cost-effectiveness, and reduced reprocessing burden. Specialty clinics also represent a growing end-user segment, particularly for niche endoscopic procedures.

North America

North America is expected to dominate the global single-use endoscopy market in 2026, with an estimated market share of around 40%. The region's leadership is attributed to high awareness of healthcare-associated infections (HAIs), stringent regulatory oversight from the FDA, and favorable reimbursement policies for single-use devices. The presence of key market players, advanced healthcare infrastructure, and a strong focus on patient safety further solidify its market position. The U.S., in particular, is a major contributor to this dominance, driven by a high volume of endoscopic procedures and a proactive approach to adopting innovative infection control solutions.

Europe

Europe is projected to hold the second-largest market share, estimated at around 25% in 2026. The region's growth is driven by increasing regulatory emphasis on infection control, guidelines from organizations like the European Society of Gastrointestinal Endoscopy (ESGE), and national health initiatives aimed at reducing waiting times and improving procedural efficiency. Countries like Germany, the UK, and France are leading in the adoption of single-use endoscopy solutions to enhance patient safety and streamline their healthcare systems.

Asia Pacific

The Asia Pacific region is projected to be the fastest-growing market for single-use endoscopy, registering a mid-to-high teens CAGR over the forecast period. This growth is driven by rising healthcare expenditure, rapid expansion of hospital infrastructure, and accelerating adoption of advanced medical technologies across key markets such as China, India, Japan, and Australia. Increasing investments in digital health transformation and healthcare modernization are further supporting procedural volumes and endoscopy adoption rates. In addition, the region’s high burden of chronic diseases, combined with growing emphasis on infection prevention and patient safety, is significantly boosting demand for single-use endoscopes. The expansion of ambulatory surgical centers, increasing medical tourism, and improving access to minimally invasive procedures in tier-2 and tier-3 cities are further strengthening market growth, as healthcare providers prioritize operational efficiency and reduced cross-contamination risk.

Latin America

Latin America is an emerging market for single-use endoscopy, driven by increasing healthcare digitalization initiatives and growing awareness of the benefits of integrated care. Countries like Brazil and Mexico are investing in modernizing their healthcare infrastructure, leading to a gradual adoption of single-use solutions. The market growth is supported by efforts to improve patient safety and streamline clinical workflows in a cost-effective manner, particularly in response to the challenges of reprocessing reusable devices.

Middle East & Africa

The Middle East & Africa region is expected to witness steady growth in the single-use endoscopy market. This growth is primarily driven by government initiatives to develop smart hospitals and healthcare cities, particularly in the UAE and Saudi Arabia. Increasing healthcare expenditure, coupled with a focus on adopting advanced medical technologies to enhance patient care and operational efficiency, contributes to the market expansion in this region. The emphasis on reducing healthcare-associated infections is also a key factor driving the adoption of single-use solutions.

The competitive landscape of the global single-use endoscopy market is characterized by intense innovation, strategic partnerships, and a focus on expanding product portfolios to address diverse clinical needs. Leading players are investing heavily in research and development to enhance imaging capabilities, improve maneuverability, and reduce the cost of disposable endoscopes. Acquisitions and collaborations are common strategies to expand market reach and integrate complementary technologies. The market is also seeing an influx of specialized startups offering niche solutions for specific procedural areas, contributing to a dynamic and evolving competitive environment in June 2026.

Ambu A/S (Denmark), Boston Scientific Corporation (U.S.), Olympus Corporation (Japan), Coloplast A/S (Denmark), Cook Medical (U.S.), Karl Storz SE & Co. KG (Germany), Fujifilm Holdings Corporation (Japan), HOYA Corporation (PENTAX Medical) (Japan), Richard Wolf GmbH (Germany), Teleflex Incorporated (U.S.), Medtronic plc (Ireland), Stryker Corporation (U.S.), Smith & Nephew plc (U.K.), B. Braun Melsungen AG (Germany), Verathon Inc. (U.S.), Arthrex, Inc. (U.S.), CONMED Corporation (U.S.), OTU Medical Inc. (U.S.), Flexicare Medical Limited (U.K.), Neoscope, Inc. (U.S.)

The market is projected to reach USD 13.15 billion by 2036, growing at a CAGR of 13.1% from 2026 to 2036.

The primary drivers are the mitigation of cross-contamination risks, enhancement of patient safety, and improvement of operational efficiency by eliminating reprocessing complexities.

The flexible endoscopes segment is expected to hold the largest share in 2026, driven by their versatility across various diagnostic and therapeutic procedures.

Contamination in reusable duodenoscopes has been documented even after high-level disinfection and standard reprocessing protocols. Published studies report variable residual contamination rates, generally ranging from low single digits to over 10%, depending on methodology and detection criteria. This persistent risk has been highlighted by regulatory agencies such as the FDA and CDC, supporting the shift toward single-use endoscopes.

North America holds the largest share, estimated at around 40% in 2026, driven by high awareness of HAIs and stringent regulatory oversight.

Single-use endoscopes eliminate reprocessing requirements. Studies indicate that updated reprocessing protocols for reusable scopes can add roughly 24 minutes and US$52–68 in cost per procedure, making disposable systems an attractive option for improving workflow efficiency.

The bronchoscopy segment is expected to account for the largest share in 2026, primarily due to the critical need for sterile solutions in respiratory care and ICUs.

Regulatory bodies like the FDA issue safety communications and guidelines that drive the adoption of single-use solutions to enhance patient safety and mitigate infection risks.

Ambulatory surgical centers (ASCs) are projected to witness the fastest growth, driven by the shift of procedures to outpatient settings and the operational advantages of single-use endoscopes.

The top 5 players are Ambu A/S, Boston Scientific Corporation, Olympus Corporation, Coloplast A/S, and Cook Medical.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/KOL Interviews

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Product

3.2.2. Market Analysis, by Application

3.2.3. Market Analysis, by End User

3.2.4. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Mitigating Cross-Contamination Risks and Enhancing Operational Efficiency through Sterile, Single-Use Solutions

4.2.1.2. Increasing Regulatory Scrutiny and FDA Safety Communications on Reusable Endoscopes

4.2.1.3. Growing Demand for Minimally Invasive Procedures and Point-of-Care Diagnostics

4.2.2. Restraints

4.2.2.1. High Initial Costs of Single-Use Endoscopes Compared to Reusable Devices

4.2.2.2. Environmental Concerns Related to Increased Medical Waste Generation

4.2.3. Opportunities

4.2.3.1. Expansion into New Clinical Applications (e.g., ENT, Peripheral Vascular) and Emerging Markets

4.2.3.2. Technological Advancements in Miniaturization and Imaging Capabilities

4.2.3.3. Development of Cost-Effective and Eco-Friendly Single-Use Solutions

4.2.4. Challenges

4.2.4.1. Ensuring Adequate Reimbursement Policies for Single-Use Endoscopes

4.2.4.2. Overcoming Physician Resistance to Adopting New Technologies

4.2.4.3. Supply Chain Management for High-Volume Disposable Devices

4.2.5. Trends

4.2.5.1. Increasing Focus on Infection Prevention and Patient Safety

4.2.5.2. Technological Advancements and Miniaturization

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Single-Use Endoscopy Market, by Product

5.1. Overview

5.2. Flexible Endoscopes

5.2.1. Bronchoscopes

5.2.2. Ureteroscopes

5.2.3. Cystoscopes

5.2.4. Duodenoscopes

5.2.5. Gastroscopes

5.2.6. Colonoscopes

5.2.7. Other Flexible Endoscopes

5.3. Rigid Endoscopes

5.3.1. Laparoscopes

5.3.2. Arthroscopes

5.3.3. Hysteroscopes

5.3.4. Other Rigid Endoscopes

6. Global Single-Use Endoscopy Market, by Application

6.1. Overview

6.2. Bronchoscopy

6.3. Urology

6.4. Gastroenterology

6.5. ENT (Ear, Nose, and Throat)

6.6. Arthroscopy

6.7. Other Applications

7. Global Single-Use Endoscopy Market, by End User

7.1. Overview

7.2. Hospitals

7.3. Ambulatory Surgical Centers (ASCs)

7.4. Specialty Clinics

7.5. Other End Users

8. Global Single-Use Endoscopy Market, by Geography

8.1. Overview

8.2. North America

8.2.1. U.S.

8.2.2. Canada

8.3. Europe

8.3.1. Germany

8.3.2. U.K.

8.3.3. France

8.3.4. Italy

8.3.5. Spain

8.3.6. Rest of Europe

8.4. Asia Pacific

8.4.1. China

8.4.2. Japan

8.4.3. India

8.4.4. Rest of Asia Pacific

8.5. Latin America

8.5.1. Brazil

8.5.2. Mexico

8.5.3. Rest of Latin America

8.6. Middle East & Africa

8.6.1. UAE

8.6.2. Saudi Arabia

8.6.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Introduction

9.2. Key Strategic Developments

9.3. Market Share Analysis

10. Company Profiles

10.1. Ambu A/S (Denmark)

10.2. Boston Scientific Corporation (U.S.)

10.3. Olympus Corporation (Japan)

10.4. Coloplast A/S (Denmark)

10.5. Cook Medical (U.S.)

10.6. Karl Storz SE & Co. KG (Germany)

10.7. Fujifilm Holdings Corporation (Japan)

10.8. HOYA Corporation (PENTAX Medical) (Japan)

10.9. Richard Wolf GmbH (Germany)

10.10. Teleflex Incorporated (U.S.)

10.11. Medtronic plc (Ireland)

10.12. Stryker Corporation (U.S.)

10.13. Smith & Nephew plc (U.K.)

10.14. B. Braun Melsungen AG (Germany)

10.15. Verathon Inc. (U.S.)

10.16. Arthrex, Inc. (U.S.)

10.17. CONMED Corporation (U.S.)

10.18. OTU Medical Inc. (U.S.)

10.19. Flexicare Medical Limited (U.K.)

10.20. Neoscope, Inc. (U.S.)

10.21. Parburch Medical Developments Ltd (U.K.)

11. Appendix

11.1. References

11.2. Disclaimer

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Jan-2025

Published Date: May-2023

Subscribe to get the latest industry updates