Resources

About Us

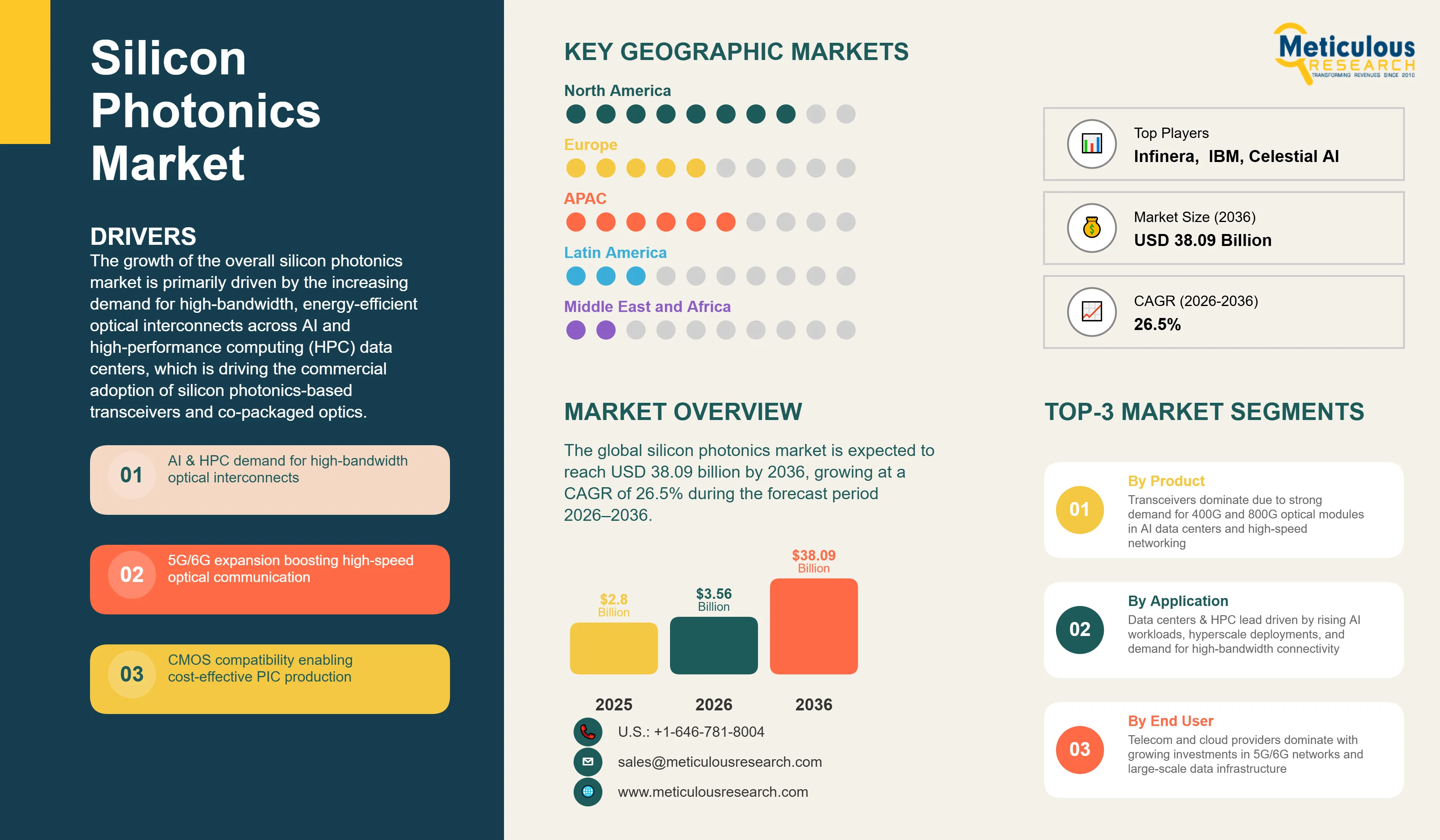

The global silicon photonics market was valued at USD 2.80 billion in 2025. This market is expected to reach USD 38.09 billion by 2036 from an estimated USD 3.56 billion in 2026, growing at a CAGR of 26.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global silicon photonics market covers the integrated photonic products and components manufactured using CMOS-compatible silicon or silicon-on-insulator (SOI) wafer platforms. These include optical transceivers, active optical cables, optical switches, variable optical attenuators, photonic sensors, lasers, optical modulators, photodetectors, optical waveguides, wavelength-division multiplexing (WDM) filters, and optical interconnect modules, which are deployed across data centers, telecommunications, defense, healthcare, automotive, and consumer electronics applications.

Silicon photonics enables the integration of optical and electronic functionalities on a single silicon chip by leveraging standard semiconductor fabrication processes. This integration facilitates the high-volume, cost-effective production of miniaturized photonic integrated circuits (PICs), offering superior bandwidth density, lower power consumption, and enhanced energy efficiency compared with conventional electrical interconnects and discrete optical module assemblies.

The growth of the overall silicon photonics market is primarily driven by the increasing demand for high-bandwidth, energy-efficient optical interconnects across AI and high-performance computing (HPC) data centers, which is driving the commercial adoption of silicon photonics-based transceivers and co-packaged optics. In addition, the rapid expansion of 5G networks and the early-stage development of 6G telecommunications infrastructure are generating significant demand for high-speed, low-power optical communication solutions. Furthermore, the compatibility of silicon photonics with CMOS manufacturing processes enables cost-effective, high-volume production of photonic integrated circuits (PICs) on conventional semiconductor fabrication lines, further driving growth of the overall silicon photonics market.

However, the growth of this market is restrained by the technical complexity associated with integrating efficient on-chip light sources on silicon substrates, primarily due to silicon’s indirect bandgap properties. Moreover, the high initial costs associated with the development, validation, and qualification of photonic integrated circuit platforms pose an additional challenge to widespread adoption.

On the other hand, the increasing commercial deployment of co-packaged optics in hyperscale AI data center switching architectures offers significant growth opportunities for market players. The increasing adoption of silicon photonics-based frequency-modulated continuous-wave (FMCW) LiDAR solutions in automotive and autonomous vehicle applications is also expected to create substantial growth opportunities. Additionally, the emergence of quantum photonics and optical computing as long-term technology growth vectors is anticipated to further drive the growth of this market.

A major trend shaping this market is the ongoing transition from 800G to 1.6T and 3.2T optical data rates, which continues to broaden the addressable market for silicon photonics solutions.

Co-Packaged Optics Transitioning from Laboratory to Commercial Hyperscale Deployment

Co-packaged optics (CPO), which involves the integration of optical input/output (I/O) directly onto or adjacent to switch and processor silicon, thereby eliminating the electrical signaling bottleneck between the ASIC and pluggable transceiver, represents one of the most transformative near-term developments in the commercialization of silicon photonics. This technology is increasingly moving beyond laboratory validation toward early-stage commercial deployment in hyperscale data center environments.

The standardization ecosystem is also progressing rapidly. The Optical Internetworking Forum (OIF) has advanced key standards, including the 3.2T Co-Packaged Module Implementation Agreement, while also demonstrating large-scale multi-vendor interoperability at recent industry events, reinforcing the technology’s readiness for hyperscale deployment. By eliminating copper serializer/deserializer (SerDes) lanes between switch ASICs and transceiver cages, co-packaged optics significantly reduces power consumption, potentially by nearly threefold compared with conventional pluggable architectures, thereby improving overall energy efficiency in high-bandwidth switching environments.

Furthermore, CPO enables bandwidth scaling beyond 51.2 Tbps per switch by overcoming the physical and power limitations associated with pluggable electrical I/O architectures. This is becoming increasingly critical as hyperscale AI and high-performance computing data centers continue to demand ultra-high-speed optical interconnect solutions.

Leading semiconductor and photonics companies, including Broadcom, Marvell Technology, Intel, and Ayar Labs, are actively advancing their co-packaged optics roadmaps, targeting commercial-scale hyperscale deployments over the next few years. In addition, Marvell Technology’s acquisition of Celestial AI, a specialist in photonic fabric technology for scale-up optical interconnects, further highlights the growing strategic importance of co-packaged optics within the broader silicon photonics ecosystem.

This trend is expected to remain a key factor as the industry transitions toward next-generation 1.6T, 3.2T, and higher-speed optical networking architectures.

Automotive FMCW LiDAR Driving Silicon Photonics Beyond Data Center Applications

The increasing adoption of frequency-modulated continuous-wave (FMCW) LiDAR systems is expanding the silicon photonics market beyond its traditional data center and telecommunications applications, positioning the automotive and autonomous vehicle sector as a high-growth application segment. These systems utilize silicon photonics chips to generate and process coherent light signals for highly accurate three-dimensional range and velocity measurement, thereby enhancing sensing capabilities in advanced driver assistance and autonomous driving platforms.

Compared with conventional time-of-flight (ToF) LiDAR technologies, silicon photonics-based FMCW LiDAR offers several fundamental advantages in automotive applications, including greater immunity to interference from nearby LiDAR systems, simultaneous velocity measurement without the need for additional signal processing, and compatibility with CMOS fabrication processes that enable scalable manufacturing and cost optimization to meet automotive pricing requirements.

Leading companies such as Intel, Mobileye, Aurora Innovation, and Blackmore Sensors and Analytics are actively advancing silicon photonics-based FMCW LiDAR platforms. In parallel, the increasing deployment of automotive driver assistance systems featuring SAE Level 2+ capabilities is creating a strong design-win pipeline for silicon photonics LiDAR components, which is expected to support long-term market growth.

Accelerating Transition to 1.6T and 3.2T Data Rates Continuously Expanding Addressable Market

The rapid evolution of optical transceiver industry from 400G to 800G, 1.6T, and emerging 3.2T data-rate standards is continuously expanding the market for silicon photonics. This transition is primarily driven by the rapid growth in bandwidth requirements across AI and hyperscale data centers, where network traffic demands continue to increase at an accelerated pace. As data rates advance, the per-port optical content value rises significantly, while successive technology upgrade cycles across the installed transceiver base further strengthen market demand.

The 1.6T transceiver segment is entering the commercial ramp-up phase during 2025–2026, marking a significant milestone in next-generation optical networking. Commercial deployments and product demonstrations based on Intel silicon photonics technology, including solutions commercialized through Jabil, reflect the transition toward large-scale adoption of ultra-high-speed optical modules.

In parallel, 3.2T transceiver architectures are moving into active commercial development, further extending the performance of silicon photonics and highlighting its role as a core enabling technology for future AI infrastructure. Industry roadmaps indicate that this progression toward higher-speed optical interconnect standards will continue to expand the total addressable market, ensuring that the data center segment remains the dominant growth driver for the silicon photonics market throughout the forecast period.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 38.09 Billion |

|

Market Size in 2026 |

USD 3.56 Billion |

|

Market Size in 2025 |

USD 2.80 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 26.5% |

|

Dominating Product |

Transceivers |

|

Fastest Growing Product |

Sensors |

|

Dominating Component |

Optical Waveguides |

|

Fastest Growing Component |

Lasers |

|

Dominating Wafer Size |

300 mm |

|

Dominating Application |

Data Centers & High-Performance Computing |

|

Fastest Growing Application |

Automotive & Industrial LiDAR |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

By Product: In 2026, the Transceivers Segment to Dominate the Global Silicon Photonics Market

Based on product, the global silicon photonics market is segmented into transceivers, active optical cables, optical switches, variable optical attenuators, sensors, and other products. In 2026, the transceivers segment is expected to account for the largest share of the global silicon photonics market. The large share of this segment is attributed to the dominant commercial volume of silicon photonics-based 400G and 800G optical transceivers deployed in hyperscale data centers for server-to-switch, switch-to-switch, and inter-data center interconnect applications. Each AI GPU server requires multiple high-speed transceivers for GPU-to-switch fabric connectivity, and the rapidly expanding installed base of AI training clusters is generating a substantial volume of transceiver procurement. The 1.6T transceiver ramp beginning in 2025 to 2026 is further expanding the segment's revenue contribution as higher-value per-unit transceivers enter volume production.

However, the sensors segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the growing adoption of silicon photonics-based LiDAR sensors in automotive and industrial applications, the growing integration of photonic biosensors in healthcare diagnostics and wearable health monitoring, and the proliferation of environmental sensing applications leveraging silicon photonics' miniaturization and CMOS manufacturing scalability.

By Component: In 2026, the Optical Waveguides Segment to Hold the Largest Share

Based on component, the global silicon photonics market is segmented into optical waveguides, lasers, optical modulators, photodetectors, WDM filters, optical interconnects, and other components. In 2026, the optical waveguides segment is expected to account for the largest share of the global silicon photonics market. The large share of this segment is attributed to the fundamental role of optical waveguides as the light-routing backbone of every silicon photonics photonic integrated circuit, present in transceivers, switches, sensors, and virtually every other silicon photonics product, making waveguide components the highest-volume and most broadly applicable component category in the silicon photonics value chain.

However, the lasers segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the growing requirement for on-chip and heterogeneously integrated laser light sources across co-packaged optics, advanced transceiver, and LiDAR applications, and the commercial launch of high-power continuous-wave laser products, such as Coherent Corp.'s 400 mW 1311 nm lasers introduced in September 2025, that address the key performance gaps previously limiting silicon photonics integration in high-power optical applications.

By Application: In 2026, the Data Centers & HPC Segment to Hold the Largest Share

Based on application, the overall silicon photonics market is segmented into data centers and high-performance computing, telecommunications and networking, military and defense, medical and life sciences, automotive and industrial LiDAR, consumer electronics and IoT, and other applications. In 2026, the data centers and high-performance computing segment is expected to account for the largest share of around 35–40% of the global silicon photonics market. This dominance indicates the rapidly growing volume of silicon photonics transceivers procured by hyperscale cloud providers and colocation operators for AI GPU cluster connectivity.

Each NVIDIA HGX H200 server requires multiple 800G transceivers (typically 2-4 OSFP/XDPD modules for AI fabric connectivity), and the increasing deployment of AI training clusters across North America, Europe, and Asia Pacific, with 800G shipments projected at 33.5 million units in 2026, is generating the largest transceiver procurement volumes in the history of the optical interconnect industry.

However, the automotive and industrial LiDAR segment is projected to grow at the highest CAGR during the forecast period. The strong growth of this segment is primarily attributed to the rapid commercialization of silicon photonics-based frequency-modulated continuous-wave (FMCW) LiDAR solutions for automotive driver assistance and autonomous driving applications. The combination of CMOS-compatible manufacturing scalability, high levels of miniaturization, and the performance advantages of FMCW modulation is enabling cost reductions to automotive bill-of-materials (BOM) price points that conventional time-of-flight (ToF) discrete optical architectures cannot competitively match.

Based on geography, the global silicon photonics market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of the global silicon photonics market. This dominant position is supported by the presence of leading silicon photonics technology companies including Intel, which pioneered the commercial silicon photonics transceiver market, Broadcom, Cisco, Lumentum, Coherent Corp., Marvell, Ayar Labs, and Celestial AI; the highest global concentration of AI data center deployments generating transceiver demand; and the most advanced photonic integrated circuit foundry and design ecosystem including GlobalFoundries' GF Fotonix platform and the AIM Photonics national institute providing open-access silicon photonics manufacturing.

However, the Asia Pacific silicon photonics market is expected to grow at the fastest CAGR during the forecast period. The rapid growth of this region is driven by the rapid expansion of data center infrastructure across China, Japan, South Korea, and Taiwan; the strong presence of semiconductor foundries including TSMC, Samsung, and SMIC that are advancing silicon photonics process platforms; the large concentration of optical module manufacturers in China and Taiwan procuring silicon photonics chips for transceiver assembly; and aggressive government-led photonics R&D investment in Japan's moonshot program and South Korea's photonic semiconductor strategy. Taiwan's position at the center of the global semiconductor supply chain makes it a critical manufacturing hub for silicon photonics wafer production, with TSMC's silicon photonics process platform enabling leading-edge photonic integrated circuit fabrication at volume production scale.

The competition within the global silicon photonics market is primarily driven by technological innovation, manufacturing scalability, product performance, and strategic collaborations across the semiconductor and optical networking value chain.

Intel remains one of the leading players in the market, driven by its strong commercial presence in high-volume 100G, 400G, and 800G transceiver product lines, along with the advancement of next-generation 1.6T optical transceiver solutions through its strategic partnership with Jabil.

Broadcom maintains a strong position through its high-performance switching platforms, including the Tomahawk and Trident product families, which are increasingly aligned with co-packaged optics architectures, as well as its integrated DSP and optical interconnect capabilities strengthened through previous strategic acquisitions.

In addition, Cisco Systems and Marvell Technology hold significant market positions through their broad portfolios of silicon photonics-based optical modules, switching solutions, and subsystems catering to data center and telecommunications applications. Foundry and manufacturing players such as GlobalFoundries, Taiwan Semiconductor Manufacturing Company, and Samsung Electronics also play a critical role in enabling large-scale commercial production of photonic integrated circuits.

The report provides a comprehensive competitive analysis based on an extensive assessment of the leading players’ product portfolios, geographic presence, financial strength, and key growth strategies adopted over the last few years.

Some of the key players operating in the global silicon photonics market include Intel (U.S.), Cisco Systems (U.S.), Broadcom (U.S.), Lumentum Holdings (U.S.), Coherent Corp. (U.S.), GlobalFoundries (U.S.), Marvell Technology (U.S.), MACOM Technology Solutions (U.S.), Infinera (U.S.), STMicroelectronics (Switzerland/France), Taiwan Semiconductor Manufacturing Company (Taiwan), Samsung Electronics (South Korea), Ayar Labs (U.S.), Celestial AI (U.S.), and IBM (U.S.), among others.

The global silicon photonics market is expected to reach USD 38.09 billion by 2036 from an estimated USD 3.56 billion in 2026, at a CAGR of 26.5% during the forecast period 2026–2036.

In 2026, the transceivers segment is expected to hold the largest share of the global silicon photonics market, driven by the dominant commercial volume of 400G and 800G optical transceivers deployed in AI data centers.

The sensors segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by expanding adoption of silicon photonics-based LiDAR sensors in automotive and industrial applications and photonic biosensors in healthcare.

In 2026, the optical waveguides segment is expected to hold the largest share of the global silicon photonics market.

In 2026, the data centers and high-performance computing segment is expected to hold the largest share of the global silicon photonics market.

The growth of this market is primarily driven by explosive AI data center demand for high-bandwidth, energy-efficient optical interconnects accelerating adoption of silicon photonics-based transceivers and co-packaged optics, the rapid expansion of 5G telecommunications infrastructure, and CMOS manufacturing compatibility enabling cost-effective high-volume production.

Key players operating in the silicon photonics market include Intel Corporation (U.S.), Cisco Systems, Inc. (U.S.), Broadcom Inc. (U.S.), Lumentum Holdings Inc. (U.S.), Coherent Corp. (U.S.), GlobalFoundries Inc. (U.S.), Marvell Technology, Inc. (U.S.), MACOM Technology Solutions Holdings, Inc. (U.S.), Infinera Corporation (U.S.), STMicroelectronics N.V. (Switzerland/France), Taiwan Semiconductor Manufacturing Company Limited (Taiwan), Samsung Electronics Co., Ltd. (South Korea), Ayar Labs, Inc. (U.S.), Celestial AI (U.S.), and IBM Corporation (U.S.).

Asia Pacific is expected to register the highest growth rate in the global silicon photonics market during the forecast period 2026–2036.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.2.2.1. Primary Interviews with Experts

2.2.2.2. Approaches for Country-/Region-Level Analysis

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

3.1. Market Overview

3.2. Market Analysis by Product

3.3. Market Analysis by Component

3.4. Market Analysis by Wafer Size

3.5. Market Analysis by Application

3.6. Market Analysis by Geography

4. Market Dynamics

4.1. Overview

4.2. Drivers

4.2.1. Explosive AI and HPC Demand for High-Bandwidth, Energy-Efficient Optical Interconnects

4.2.2. Rapid Expansion of 5G and Early 6G Telecommunications Infrastructure

4.2.3. CMOS Manufacturing Compatibility Enabling Cost-Effective High-Volume Production of PICs

4.2.4. Accelerating Transition from 800G to 1.6T and 3.2T Optical Data Rates Expanding Addressable Market

4.3. Restraints

4.3.1. Complexity of Integrating Efficient On-Chip Light Sources on Silicon Due to Indirect Bandgap

4.3.2. High Initial Development and Qualification Costs of Photonic Integrated Circuit Platforms

4.4. Opportunities

4.4.1. Commercial Deployment of Co-Packaged Optics in Hyperscale AI Data Center Switching Architectures

4.4.2. Automotive FMCW LiDAR Adoption Expanding Silicon Photonics Beyond Data Center and Telecom

4.4.3. Quantum Photonics and Optical Computing Emerging as Long-Term Growth Vectors

4.5. Challenges

4.5.1. Thermal Management Requirements for High-Density Photonic Integration Above 70°C

4.5.2. Lack of Standardized Packaging Frameworks Slowing Silicon Photonics Ecosystem Development

5. Silicon Photonics Market, by Product

5.1. Overview

5.2. Transceivers

5.3. Active Optical Cables

5.4. Optical Switches

5.5. Variable Optical Attenuators

5.6. Sensors

5.7. Other Products

6. Silicon Photonics Market, by Component

6.1. Overview

6.2. Optical Waveguides

6.3. Lasers

6.4. Optical Modulators

6.5. Photodetectors

6.6. WDM Filters

6.7. Optical Interconnects

6.8. Other Components

7. Silicon Photonics Market, by Wafer Size

7.1. Overview

7.2. 300 mm

7.3. 200 mm

7.4. Other Wafer Sizes

8. Silicon Photonics Market, by Application

8.1. Overview

8.2. Data Centers & High-Performance Computing

8.3. Telecommunications & Networking

8.4. Military & Defense

8.5. Medical & Life Sciences

8.6. Automotive & Industrial LiDAR

8.7. Consumer Electronics & IoT

8.8. Other Applications

9. Silicon Photonics Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Netherlands

9.3.5. Italy

9.3.6. Switzerland

9.3.7. Sweden

9.3.8. Rest of Europe

9.4. Asia Pacific

9.4.1. China

9.4.2. Japan

9.4.3. South Korea

9.4.4. India

9.4.5. Taiwan

9.4.6. Singapore

9.4.7. Australia

9.4.8. Rest of Asia Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Argentina

9.5.4. Chile

9.5.5. Rest of Latin America

9.6. Middle East and Africa

9.6.1. UAE

9.6.2. Saudi Arabia

9.6.3. South Africa

9.6.4. Israel

9.6.5. Rest of Middle East and Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Benchmarking

10.4. Competitive Dashboard

10.4.1. Industry Leaders

10.4.2. Market Differentiators

10.4.3. Vanguards

10.4.4. Emerging Companies

10.5. Market Share/Ranking Analysis of Key Players, 2025

11. Company Profiles

11.1. Intel Corporation

11.2. Broadcom Inc.

11.3. Cisco Systems, Inc.

11.4. Marvell Technology, Inc.

11.5. Coherent Corp.

11.6. GlobalFoundries Inc.

11.7. Lumentum Holdings Inc.

11.8. Taiwan Semiconductor Manufacturing Company Limited

11.9. Samsung Electronics Co., Ltd.

11.10. MACOM Technology Solutions Holdings, Inc.

11.11. STMicroelectronics N.V.

11.12. Infinera Corporation

11.13. Ayar Labs, Inc.

11.14. Celestial AI

11.15. IBM Corporation

11.16. Others

12. Appendix

12.1. Questionnaire

12.2. Available Customization Options

12.3. Related Reports

Published Date: Feb-2026

Published Date: Jun-2022

Published Date: Jan-2025

Published Date: Apr-2026

Published Date: Jun-2026

Subscribe to get the latest industry updates