Resources

About Us

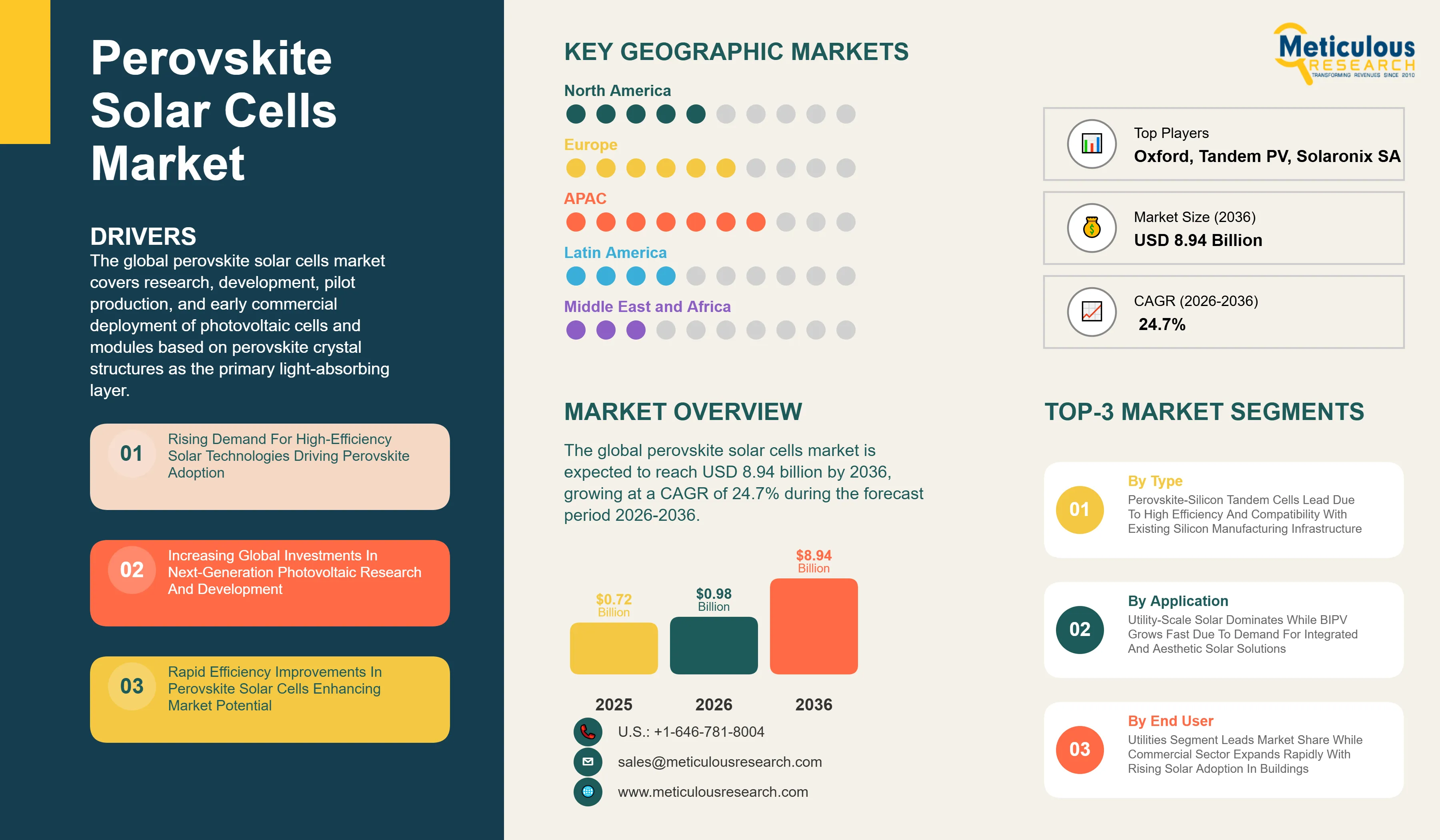

The global perovskite solar cells market was valued at USD 0.72 billion in 2025. This market is expected to reach USD 8.94 billion by 2036 from an estimated USD 0.98 billion in 2026, growing at a CAGR of 24.7% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

The global perovskite solar cells market covers research, development, pilot production, and early commercial deployment of photovoltaic cells and modules based on perovskite crystal structures as the primary light-absorbing layer. This includes single-junction perovskite cells, perovskite-silicon tandem cells, all-perovskite tandem cells, and flexible thin-film perovskite configurations, spanning solution-processed, vapor-deposited, and printed manufacturing methods across utility-scale, building-integrated, portable, and specialty application segments.

The growth of the global perovskite solar cells market is primarily driven by the rapid improvement in certified power conversion efficiencies, which have advanced from below 4% in 2009 to certified records exceeding 26% for single-junction and 33% for tandem configurations, approaching and in some configurations surpassing the practical efficiency limits of conventional silicon PV. The potential for significantly lower manufacturing costs through solution-processed and printed deposition methods, combined with the demonstrated tunability of the perovskite bandgap across the visible and near-infrared spectrum enabling tailored absorption profiles, is attracting substantial investment from both established PV manufacturers and venture-backed startups pursuing commercialization of this technology.

However, the market faces key constraints. Long-term operational stability under real-world conditions of moisture, heat, and UV exposure remains the primary technical barrier to commercial deployment, with most perovskite formulations demonstrating operational lifetimes substantially shorter than the 25-year warranty standards of commercial silicon modules. The environmental and regulatory challenges associated with the lead content in high-performance perovskite formulations are adding complexity to regulatory approval and end-of-life disposal frameworks in key markets.

Despite these challenges, several opportunities are accelerating market development. The rapid commercial momentum of perovskite-silicon tandem cells, which are approaching pilot production at Oxford PV, Tandem PV, and several Chinese manufacturers, represents the nearest-term commercialization pathway. Advancements in encapsulation technologies are progressively extending perovskite module operational lifetimes, while the expansion of BIPV demand is creating near-term application pull for the aesthetic and form-factor flexibility that perovskite cells uniquely enable.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 8.94 Billion |

|

Market Size in 2026 |

USD 0.98 Billion |

|

Market Size in 2025 |

USD 0.72 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 24.7% |

|

Dominating Cell Architecture |

Perovskite-Silicon Tandem Solar Cells |

|

Fastest Growing Cell Architecture |

All-Perovskite Tandem Solar Cells |

|

Dominating Material Composition |

Lead-Based Perovskites |

|

Fastest Growing Material Composition |

Lead-Free Perovskites |

|

Dominating Manufacturing Method |

Solution-Processed Cells |

|

Fastest Growing Manufacturing Method |

Printed and Roll-to-Roll Cells |

|

Dominating Application |

Utility-Scale Solar Power |

|

Fastest Growing Application |

Building-Integrated Photovoltaics (BIPV) |

|

Dominating End User |

Utilities |

|

Fastest Growing End User |

Commercial |

|

Dominating Geography |

Asia-Pacific |

|

Fastest Growing Geography |

Europe |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Rapid Development of Perovskite-Silicon Tandem Cells

The accelerating development and near-term commercialization of perovskite-silicon tandem solar cells is the defining technology trend in the global perovskite solar cells market. By stacking a perovskite top cell tuned to absorb high-energy photons with a silicon bottom cell optimized for lower-energy photon absorption, tandem architectures have achieved certified power conversion efficiencies exceeding 33%, compared with the practical single-junction silicon efficiency ceiling of approximately 29%.

Oxford PV announced the commencement of its first commercial-scale perovskite-silicon tandem module production facility in Brandenburg, Germany, representing a landmark transition from laboratory demonstration to early commercial manufacturing. Tandem PV and several Chinese manufacturers have announced parallel pilot production programs. This technology trend is expected to be the primary near-term commercial driver of the global perovskite solar cells market through the forecast period.

Shift Toward Lead-Free Perovskite Formulations

The progressive development of commercially viable lead-free perovskite formulations is an important long-term trend driven by the anticipated tightening of lead restrictions under EU RoHS regulations and equivalent frameworks in other major markets. Tin-based perovskite compositions including methylammonium tin iodide and formamidinium tin iodide have demonstrated power conversion efficiencies approaching 15%, while bismuth-based and antimony-based compositions are advancing along their respective development trajectories.

The efficiency gap between lead-free and lead-based perovskite formulations remains substantial, but the pace of improvement in tin-based compositions has accelerated significantly, with several research groups reporting certified efficiencies above 13-14% for tin-based single junctions. Companies including Saule Technologies and EneCoat Technologies are actively developing low-toxicity perovskite formulations aimed at regulatory preemptive positioning in European and Japanese markets where lead restrictions are most likely to affect commercial deployment timelines.

Advancements in Stability and Efficiency Exceeding 25%

Overcoming the operational stability limitations of perovskite photovoltaic materials is the central research priority of the global perovskite solar cells industry, and sustained progress across multiple stability enhancement approaches is progressively extending demonstrated operational lifetimes toward commercially relevant thresholds. The development of 2D-3D perovskite compositional engineering, defect passivation strategies using organic molecular additives, and advanced inorganic encapsulation architectures have collectively extended laboratory-scale operational stability under accelerated aging conditions from hundreds of hours to thousands of hours.

Certified efficiencies for research-scale perovskite cells have exceeded 26% for single-junction configurations and 33% for tandem devices, establishing performance benchmarks that exceed commercially deployed monocrystalline silicon modules. The convergence of efficiency improvement and stability enhancement is creating the technical foundation required for the commercialization programs that multiple companies are advancing toward initial production-scale deployments during the forecast period.

Rising Demand for High-Efficiency Solar Technologies

The primary driver of the global perovskite solar cells market is the sustained global push for photovoltaic technologies that can surpass the efficiency limits of conventional crystalline silicon solar cells, which are approaching their practical conversion ceiling of 26-29% for single-junction configurations. Perovskite solar cells have demonstrated the fastest efficiency improvement trajectory of any photovoltaic technology in research history, advancing from 3.8% in 2009 to certified efficiencies exceeding 26% for single-junction and 33% for tandem configurations within 15 years. This performance trajectory is attracting substantial capital from both established PV manufacturers seeking technology differentiation and policy-driven investment programs targeting next-generation clean energy technologies.

Increasing Investments in Next-Generation Photovoltaics

Global investment in next-generation photovoltaic technologies has accelerated substantially, with perovskite solar cells attracting the largest share of research and early-stage commercial funding among emerging PV technologies. The U.S. Department of Energy's Solar Energy Technologies Office, the European Commission's Horizon programs, and equivalent national funding bodies in China, Japan, South Korea, and Australia have collectively committed hundreds of millions of dollars to perovskite photovoltaic research and early commercialization programs. Venture capital investment in perovskite solar cell startups has grown significantly, with companies including Oxford PV, Swift Solar, Tandem PV, and Saule Technologies collectively raising substantial funding to advance their respective technology and manufacturing programs toward commercial scale.

Stability and Degradation Issues

Long-term operational stability under real-world environmental conditions remains the primary technical barrier to commercial deployment of perovskite solar cells. Standard perovskite formulations based on methylammonium lead iodide exhibit significant sensitivity to moisture, oxygen, elevated temperature, and UV irradiation that causes progressive degradation of the perovskite crystal structure and associated loss of photovoltaic performance. While laboratory-scale stability demonstrations have extended considerably through compositional engineering and encapsulation advances, demonstrating module-level stability meeting the IEC 61215 and IEC 61730 certification standards required for commercial solar module qualification at the module sizes relevant for commercial deployment remains a significant and not yet fully resolved challenge for the industry.

Presence of Lead and Environmental Concerns

The high-performance perovskite formulations that have driven the technology's rapid efficiency advancement are predominantly lead halide compositions whose lead content raises environmental concerns regarding manufacturing exposure, in-field degradation leachate potential, and end-of-life disposal. Lead is a regulated substance under EU RoHS and REACH regulations, the U.S. EPA's hazardous substance frameworks, and equivalent regulations in other major markets. While current photovoltaic applications benefit from specific RoHS exemptions, the regulatory trajectory in Europe and other markets suggests progressive tightening of restrictions on lead-containing electronics that could constrain market entry for lead-halide perovskite modules. This regulatory exposure is motivating both the development of lead-free alternative compositions and investment in robust encapsulation and recycling frameworks for lead-containing perovskite modules.

Tandem Solar Cell Integration with Silicon

The integration of perovskite top cells with existing silicon bottom cells in tandem architectures represents the most commercially validated and nearest-term opportunity in the perovskite solar cells market. Perovskite-silicon tandems leverage the substantial installed base of silicon solar cell manufacturing infrastructure and can be commercially positioned as high-efficiency premium modules targeting applications where higher efficiency per unit area commands price premiums sufficient to justify higher production costs. Oxford PV has reported perovskite-silicon tandem module efficiencies exceeding 28% at commercial module sizes, establishing a credible performance advantage over the best commercial silicon modules available. The compatibility of tandem architecture with established silicon manufacturing processes is enabling established silicon PV manufacturers to explore perovskite top cell incorporation as a technology upgrade pathway.

Expansion in Portable and IoT Power Applications

The expanding ecosystem of IoT sensors, wearable electronics, portable consumer devices, and low-power wireless equipment is creating demand for lightweight, flexible, and low-cost photovoltaic power sources that can harvest indoor and outdoor ambient light to support battery-free or battery-extension operation. Perovskite solar cells demonstrate favorable indoor light harvesting efficiency characteristics under the low-intensity, spectrally varied conditions of artificial indoor illumination, enabling energy harvesting from office lighting and consumer electronics displays. This application segment enables early commercial deployment of perovskite cells at small areas and relatively modest stability requirements compared with utility-scale applications, providing revenue-generating deployment pathways that can support manufacturing learning curve progress while longer-duration stability requirements for outdoor utility applications continue to be addressed.

By Cell Architecture: In 2026, the Perovskite-Silicon Tandem Segment to Dominate

Based on cell architecture, the global perovskite solar cells market is segmented into single-junction perovskite solar cells, perovskite-silicon tandem solar cells, all-perovskite tandem solar cells, and flexible perovskite solar cells. In 2026, the perovskite-silicon tandem solar cells segment is expected to account for the largest share of the global perovskite solar cells market. The large share of this segment is attributed to the demonstrated performance advantage of tandem architectures over single-junction silicon, the strongest commercial development activity among all perovskite cell architectures, and the direct compatibility of perovskite top cells with the silicon manufacturing infrastructure that major PV manufacturers have already established.

However, the all-perovskite tandem solar cells segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the theoretical efficiency ceiling exceeding 43% for optimally designed all-perovskite multijunction configurations, the growing research investment directed at this architecture by leading academic groups and startups including Swift Solar, and the potential for fully solution-processed all-perovskite tandem manufacturing at costs below silicon-based alternatives once stability and efficiency targets are achieved.

By Material Composition: In 2026, Lead-Based Perovskites to Hold the Largest Share

Based on material composition, the global perovskite solar cells market is segmented into hybrid organic-inorganic perovskites, inorganic perovskites, lead-based perovskites, and lead-free perovskites. In 2026, the lead-based perovskites segment is expected to account for the largest share of the global perovskite solar cells market. This dominance reflects the current efficiency leadership of lead halide perovskite formulations, which hold all major certified efficiency records for single-junction and tandem perovskite cells, and the concentration of commercial development activity at companies including Oxford PV, Saule Technologies, and GCL Technology around lead-based formulations that have demonstrated the strongest performance and manufacturing compatibility to date.

However, the lead-free perovskites segment is projected to register the highest CAGR during the forecast period. This growth is driven by the anticipated tightening of EU RoHS regulations affecting lead content in photovoltaic applications, the accelerating research progress in tin-based and bismuth-based perovskite compositions narrowing the efficiency gap with lead-based alternatives, and the strategic positioning investments being made by companies seeking regulatory preemptive advantage in markets where lead restrictions are expected to affect commercial approval timelines.

By Manufacturing Method: In 2026, Solution-Processed Cells to Hold the Largest Share

Based on manufacturing method, the global perovskite solar cells market is segmented into solution-processed cells, vapor-deposited cells, and printed and roll-to-roll cells. In 2026, the solution-processed cells segment is expected to account for the largest share of the global perovskite solar cells market. This is driven by the broad research and pilot production base built on solution-processed perovskite deposition techniques, the lower capital equipment requirements compared with vapor deposition, and the demonstrated ability of solution-processed approaches to achieve high efficiencies at research and pilot production scales across a wide range of perovskite formulations.

However, the printed and roll-to-roll cells segment is projected to register the highest CAGR during the forecast period. This growth is driven by the potential of continuous roll-to-roll and inkjet printing manufacturing to achieve very low production costs through high-throughput processing of flexible substrates, the progress of companies including Saule Technologies and Heliatek in advancing inkjet-printed perovskite manufacturing toward commercial viability, and the alignment of printed flexible perovskite cells with the rapidly growing BIPV and portable power application segments.

By Application: In 2026, Utility-Scale Solar Power to Hold the Largest Share

Based on application, the global perovskite solar cells market is segmented into utility-scale solar power, building-integrated photovoltaics (BIPV), portable and consumer electronics, IoT and wearable devices, automotive and mobility, aerospace and defense, and other applications. In 2026, the utility-scale solar power segment is expected to account for the largest share of the global perovskite solar cells market. This is driven by the initial commercial deployment focus of leading perovskite-silicon tandem manufacturers including Oxford PV and GCL Technology on high-efficiency utility-scale module formats, where the efficiency premium of tandem cells justifies the price premium over standard silicon modules for developers seeking maximum energy yield per unit area.

However, the BIPV segment is projected to register the highest CAGR during the forecast period. This growth is driven by the rapidly expanding global BIPV market propelled by net-zero building standards, the unique form-factor and transparency advantages of perovskite cells for architectural integration, and the early commercial BIPV deployments by companies including Saule Technologies demonstrating commercially viable perovskite BIPV installations on commercial building facades.

By End User: In 2026, Utilities to Hold the Largest Share

Based on end user, the global perovskite solar cells market is segmented into residential, commercial, industrial, and utilities. In 2026, the utilities segment is expected to account for the largest share of the global perovskite solar cells market. This dominance is attributed to the focus of initial commercial perovskite module deployments on large-scale solar power projects where high-efficiency tandem modules are being evaluated as premium alternatives to standard silicon modules for maximizing energy density in land-constrained project sites.

However, the commercial end user segment is projected to register the highest CAGR during the forecast period. This growth is driven by the growing adoption of perovskite-based BIPV products in commercial building construction and retrofit programs, the expansion of commercial rooftop and facade solar installations targeting net-zero building certification, and the suitability of perovskite module form factors for commercial building integration applications that are driving strong demand growth in this end user category.

Perovskite Solar Cells Market by Region: Asia-Pacific Leading by Share, Europe by Growth

Based on geography, the global perovskite solar cells market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, Asia-Pacific is expected to account for the largest share of the global perovskite solar cells market. The largest share of this region is mainly due to the leading position of Chinese research institutions and manufacturers including GCL Technology in advancing perovskite cell technology toward pilot and commercial production, the strong research programs in Japan at Panasonic, Toshiba, and Sharp, the active perovskite research ecosystem in South Korea, and Taiwan's established solar cell manufacturing infrastructure that provides a manufacturing platform for perovskite cell integration. China's national solar technology development programs have specifically identified perovskite photovoltaics as a strategic next-generation technology with significant public research funding commitments, creating a concentrated development ecosystem that is accelerating the region's commercial readiness.

However, the European perovskite solar cells market is expected to grow at the fastest CAGR during the forecast period. Europe's rapid growth is driven by Oxford PV's commercial manufacturing facility in Germany representing the world's most advanced perovskite-silicon tandem production program, the strong academic and startup ecosystem at institutions including the University of Oxford, Helmholtz-Zentrum Berlin, and IMEC in Belgium that is translating research advances into commercial ventures, the European Commission's substantial Horizon program funding for perovskite photovoltaic commercialization, and the EU's ambitious solar energy deployment targets that are creating strong demand pull for high-efficiency photovoltaic technologies.

North America is establishing a growing position in the perovskite solar cells market, with companies including Swift Solar, Tandem PV, and Hunt Perovskite Technologies advancing perovskite cell commercialization programs supported by U.S. Department of Energy funding and the Inflation Reduction Act incentives for domestic solar manufacturing. The U.S. market's large solar installation base and strong research university ecosystem provide a favorable environment for perovskite solar cell market development through the forecast period.

The global perovskite solar cells market is in an early stage of commercialization, with competition currently focused on technology differentiation, efficiency records, stability milestones, and advancement toward IEC-certified module qualification rather than on commercial revenue scale. The competitive landscape spans specialist perovskite startups, established solar PV manufacturers integrating perovskite capabilities, and electronics conglomerates with photovoltaic research programs.

Oxford PV leads the perovskite-silicon tandem segment with its production facility in Brandenburg, Germany, and holds multiple certified efficiency records for large-area tandem modules. Saule Technologies is advancing inkjet-printed perovskite manufacturing and has deployed commercial BIPV installations in Europe. GCL Technology is applying its large-scale solar manufacturing infrastructure to perovskite cell development in China. Tandem PV and Swift Solar are advancing U.S.-based perovskite tandem commercialization programs. Panasonic, Toshiba, and Sharp are pursuing perovskite research programs in Japan, while EneCoat Technologies and Solaronix are focusing on stability enhancement and dye-sensitized perovskite hybrid formulations.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' product pipelines, technology differentiation, geographic presence, and key strategic developments. Some of the key players operating in the global perovskite solar cells market include Oxford PV Ltd. (U.K.), Saule Technologies (Poland), Microquanta Semiconductor (China), Swift Solar (U.S.), Tandem PV (U.S.), Heliatek GmbH (Germany), Hunt Perovskite Technologies (U.S.), Greatcell Energy (Australia), GCL Technology Holdings (China), Panasonic Corporation (Japan), Toshiba Corporation (Japan), Sharp Corporation (Japan), EneCoat Technologies (Japan), Solaronix SA (Switzerland), and Dyesol Limited (Australia), among others.

The global perovskite solar cells market is expected to reach USD 8.94 billion by 2036 from an estimated USD 0.98 billion in 2026, at a CAGR of 24.7% during the forecast period 2026-2036.

In 2026, the perovskite-silicon tandem solar cells segment is expected to hold the largest share of the global perovskite solar cells market.

The all-perovskite tandem solar cells segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the segment's theoretical efficiency ceiling exceeding 43% and the growing research and startup investment directed at this architecture.

In 2026, the lead-based perovskites segment is expected to hold the largest share of the global perovskite solar cells market, reflecting the current efficiency leadership and broadest commercial development base of lead halide perovskite formulations.

In 2026, the utility-scale solar power segment is expected to hold the largest share of the global perovskite solar cells market.

The growth of this market is primarily driven by the rapid efficiency improvement trajectory of perovskite photovoltaic technologies approaching and surpassing practical silicon PV efficiency limits, increasing global investment in next-generation photovoltaic commercialization, and the demonstrated cost reduction potential of solution-processed and printed perovskite manufacturing relative to conventional silicon PV production.

Key players are Oxford PV Ltd. (U.K.), Saule Technologies (Poland), Microquanta Semiconductor (China), Swift Solar (U.S.), Tandem PV (U.S.), Heliatek GmbH (Germany), Hunt Perovskite Technologies (U.S.), Greatcell Energy (Australia), GCL Technology Holdings (China), Panasonic Corporation (Japan), Toshiba Corporation (Japan), Sharp Corporation (Japan), EneCoat Technologies (Japan), Solaronix SA (Switzerland), and Dyesol Limited (Australia), among others.

Europe is expected to register the highest growth rate in the global perovskite solar cells market during the forecast period 2026-2036.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.2.2.1. Primary Interviews with Experts

2.2.2.2. Approaches for Country-/Region-Level Analysis

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rising Demand for High-Efficiency Solar Technologies

4.2.1.2. Increasing Investments in Next-Generation Photovoltaics

4.2.1.3. Low Manufacturing Cost Potential Compared to Silicon PV

4.2.1.4. Growing Focus on Lightweight and Flexible Solar Solutions

4.2.2. Restraints

4.2.2.1. Stability and Degradation Issues

4.2.2.2. Presence of Lead and Environmental Concerns

4.2.2.3. Limited Commercial-Scale Manufacturing

4.2.3. Opportunities

4.2.3.1. Tandem Solar Cell Integration with Silicon

4.2.3.2. Building-Integrated Photovoltaics (BIPV) Applications

4.2.3.3. Expansion in Portable and IoT Power Applications

4.2.3.4. Advancements in Encapsulation Technologies

4.2.4. Challenges

4.2.4.1. Scaling from Lab to Mass Production

4.2.4.2. Long-Term Durability Certification

4.3. Key Market Trends

4.3.1. Rapid Development of Perovskite-Silicon Tandem Cells

4.3.2. Shift Toward Flexible and Printable Solar Cells

4.3.3. Increasing Strategic Partnerships Between Startups and PV Giants

4.3.4. Growth in Pilot Manufacturing Facilities

4.3.5. Advancements in Stability and Efficiency (>25%)

4.4. Technology Landscape

4.4.1. Single-Junction Perovskite Solar Cells

4.4.2. Tandem (Perovskite-Silicon) Solar Cells

4.4.3. Flexible and Thin-Film Perovskite Cells

4.4.4. Printable and Roll-to-Roll Manufacturing Technologies

4.4.5. Encapsulation and Stability Enhancement Technologies

4.5. Manufacturing Process Landscape

4.5.1. Solution Processing Techniques

4.5.2. Vapor Deposition Methods

4.5.3. Roll-to-Roll Manufacturing

4.5.4. Inkjet Printing and Coating Technologies

4.6. Regulatory and Environmental Landscape

4.6.1. Environmental Regulations (Lead Usage)

4.6.2. Renewable Energy Policies and Incentives

4.6.3. Certification Standards (IEC, UL)

4.7. Porter's Five Forces Analysis

4.8. Value Chain & Ecosystem Analysis

4.8.1. Raw Material Suppliers

4.8.2. Perovskite Material Developers

4.8.3. Cell & Module Manufacturers

4.8.4. System Integrators

4.8.5. End Users

4.9. Investment and Funding Landscape

4.9.1. Venture Capital and Startup Funding

4.9.2. Strategic Collaborations and Partnerships

4.9.3. Pilot Production Investments

4.10. Patent Landscape and Innovation Analysis

4.11. Pricing and Cost Analysis

4.11.1. Cost Comparison vs Silicon Solar Cells

4.11.2. Manufacturing Cost Breakdown

4.11.3. Future Cost Reduction Trends

5. Perovskite Solar Cells Market, by Cell Architecture (Primary Segmentation)

5.1. Introduction

5.2. Single-Junction Perovskite Solar Cells

5.3. Perovskite-Silicon Tandem Solar Cells

5.4. All-Perovskite Tandem Solar Cells

5.5. Flexible Perovskite Solar Cells

6. Perovskite Solar Cells Market, by Material Composition

6.1. Introduction

6.2. Hybrid Organic-Inorganic Perovskites

6.3. Inorganic Perovskites

6.4. Lead-Based Perovskites

6.5. Lead-Free Perovskites

7. Perovskite Solar Cells Market, by Manufacturing Method

7.1. Introduction

7.2. Solution-Processed Cells

7.3. Vapor-Deposited Cells

7.4. Printed and Roll-to-Roll Cells

8. Perovskite Solar Cells Market, by Application

8.1. Introduction

8.2. Utility-Scale Solar Power

8.3. Building-Integrated Photovoltaics (BIPV)

8.4. Portable & Consumer Electronics

8.5. IoT & Wearable Devices

8.6. Automotive & Mobility

8.7. Aerospace & Defense

8.8. Other Applications

9. Perovskite Solar Cells Market, by End User

9.1. Introduction

9.2. Residential

9.3. Commercial

9.4. Industrial

9.5. Utilities

10. Perovskite Solar Cells Market, by Geography

10.1. Introduction

10.2. North America

10.2.1. U.S.

10.2.2. Canada

10.3. Europe

10.3.1. Germany

10.3.2. U.K.

10.3.3. France

10.3.4. Italy

10.3.5. Spain

10.3.6. Netherlands

10.3.7. Sweden

10.3.8. Rest of Europe

10.4. Asia-Pacific

10.4.1. China

10.4.2. Japan

10.4.3. South Korea

10.4.4. India

10.4.5. Australia

10.4.6. Taiwan

10.4.7. Rest of Asia-Pacific

10.5. Latin America

10.5.1. Brazil

10.5.2. Mexico

10.5.3. Chile

10.5.4. Argentina

10.5.5. Rest of Latin America

10.6. Middle East & Africa

10.6.1. UAE

10.6.2. Saudi Arabia

10.6.3. South Africa

10.6.4. Israel

10.6.5. Rest of Middle East & Africa

11. Competitive Landscape

11.1. Overview

11.2. Key Growth Strategies

11.3. Competitive Benchmarking

11.4. Competitive Dashboard

11.4.1. Industry Leaders

11.4.2. Market Differentiators

11.4.3. Vanguards

11.4.4. Emerging Companies

11.5. Market Ranking/Positioning Analysis of Key Players, 2025

12. Company Profiles

(Business Overview, Financial Overview, Product Pipeline, Strategic Developments, SWOT Analysis)

12.1. Oxford PV Ltd.

12.2. Saule Technologies

12.3. Microquanta Semiconductor

12.4. Swift Solar

12.5. Tandem PV

12.6. Heliatek GmbH

12.7. Hunt Perovskite Technologies

12.8. Greatcell Energy

12.9. GCL Technology Holdings

12.10. Panasonic Corporation

12.11. Toshiba Corporation

12.12. Sharp Corporation

12.13. EneCoat Technologies

12.14. Solaronix SA

12.15. Dyesol Limited

13. Appendix

13.1. Additional Customization

13.2. Related Reports

Published Date: May-2025

Subscribe to get the latest industry updates