Resources

About Us

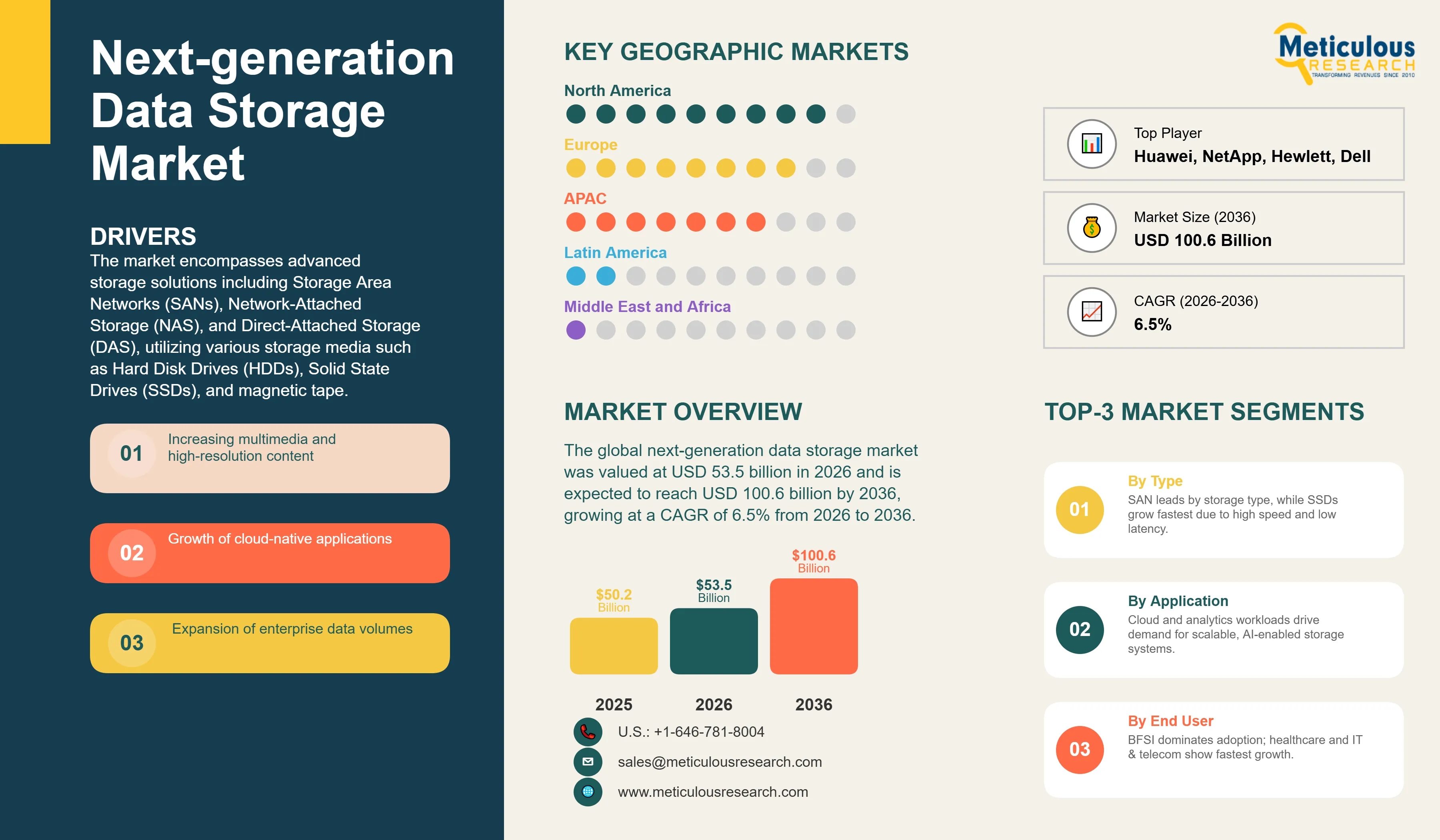

The global next-generation data storage market was valued at USD 53.5 billion in 2026 and is expected to reach USD 100.6 billion by 2036, growing at a CAGR of 6.5% from 2026 to 2036. The market encompasses advanced storage solutions including Storage Area Networks (SANs), Network-Attached Storage (NAS), and Direct-Attached Storage (DAS), utilizing various storage media such as Hard Disk Drives (HDDs), Solid State Drives (SSDs), and magnetic tape. The growth of the next-generation data storage market is driven by the exponential increase in digital data generation, the proliferation of Internet of Things (IoT) devices, the rapid adoption of cloud computing, and the increasing need for efficient data management and analytics. Organizations across various sectors, including BFSI, healthcare, retail, manufacturing, government, and IT & telecommunications, are investing heavily in advanced storage infrastructure to manage and extract value from massive volumes of data. The market is characterized by continuous technological innovation, with vendors developing increasingly sophisticated solutions that incorporate artificial intelligence, machine learning, and advanced analytics capabilities to optimize storage performance and efficiency.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Next-generation data storage encompasses advanced technologies designed to address the challenges of managing exponentially growing data volumes while maintaining performance, reliability, and cost-effectiveness. The market includes diverse storage architectures and technologies that enable organizations to store, access, and manage data efficiently across on-premises, cloud, and hybrid environments.

The rapid expansion of digital data creation from multiple sources, including enterprise applications, IoT sensors, mobile devices, social media, and artificial intelligence systems, has created unprecedented demand for scalable and efficient storage solutions. Traditional storage technologies have become inadequate for handling the massive data volumes and complex workloads generated by modern enterprises. Next-generation storage solutions address these challenges through advanced features such as improved reliability, enhanced efficiency, superior scalability, and cost-effectiveness compared to legacy systems.

The market is characterized by intense competition among established technology vendors and emerging innovators. Major players including Dell Technologies Inc., Hewlett Packard Enterprise Company, NetApp Inc., International Business Machines Corporation, and Huawei Technologies Co., Ltd. are continuously investing in research and development to enhance their storage offerings. These vendors are integrating advanced technologies such as artificial intelligence, machine learning, and advanced analytics into their storage platforms to provide customers with intelligent data management capabilities.

The deployment of next-generation storage solutions is particularly pronounced in data-intensive industries such as BFSI, healthcare, and government sectors. Financial institutions are leveraging advanced storage infrastructure to support real-time analytics, fraud detection, and customer relationship management. Healthcare organizations are utilizing sophisticated storage systems to manage electronic health records, medical imaging data, and research datasets. Government agencies are implementing next-generation storage to support citizen services, national security initiatives, and data-driven policy making.

What Are the Key Trends in the Next-Generation Data Storage Market?

Integration of Artificial Intelligence and Advanced Analytics

A prominent trend in the next-generation data storage market is the integration of artificial intelligence (AI) and advanced analytics into storage platforms. Vendors are embedding AI- and machine learning–driven capabilities to enable intelligent data management, workload-aware optimization, and predictive performance monitoring. These systems can automatically analyze usage patterns, forecast capacity requirements, and optimize data placement across storage tiers to improve efficiency and reduce latency.

AI-enabled storage solutions also support proactive fault detection and self-healing mechanisms, minimizing downtime and improving system reliability. As organizations increasingly rely on data-intensive workloads such as real-time analytics, AI model training, and high-performance computing, intelligent storage architectures play a critical role in ensuring optimal performance and resource utilization.

Shift Toward Hybrid and Multi-Cloud Storage Architectures

Another major trend is the transition toward hybrid and multi-cloud storage environments. Enterprises are moving away from purely on-premises infrastructures toward architectures that combine private data centers with public cloud platforms. This hybrid approach provides greater flexibility, scalability, and cost efficiency while enabling organizations to distribute workloads based on performance, compliance, and security requirements.

Multi-cloud strategies further enhance resilience by avoiding vendor lock-in and enabling workload portability across different cloud providers. Storage solutions that offer unified data management, seamless interoperability, and centralized control across diverse environments are gaining prominence. This shift is particularly significant as organizations seek to balance data sovereignty concerns with the need for agile, scalable infrastructure.

|

Metric |

Value |

|

Market Size (2026) |

USD 53.5 Billion |

|

Market Size (2036) |

USD 100.6 Billion |

|

Revenue CAGR (2026-2036) |

6.5% |

|

Dominating Storage Type |

Storage Area Networks (SANs) |

|

Fastest Growing Storage Type |

Solid State Drives (SSDs) |

|

Leading End-User Segment |

BFSI |

|

Fastest Growing End-User |

Healthcare & IT & Telecom |

|

Leading Region |

North America |

What Are the Key Drivers of the Next-Generation Data Storage Market?

The next-generation data storage market is primarily driven by the exponential growth in digital data generation across enterprise IT systems, connected IoT ecosystems, and cloud-native applications. Organizations are managing unprecedented volumes of structured and unstructured data, necessitating scalable, high-capacity storage architectures capable of supporting real-time access and long-term retention. The widespread adoption of advanced analytics, big data platforms, and artificial intelligence (AI) workloads further accelerates demand for high-performance, low-latency storage technologies such as NVMe-based systems and all-flash arrays.

In addition, increasing regulatory requirements surrounding data security, privacy, and compliance are prompting enterprises to invest in resilient storage infrastructures with built-in redundancy, encryption, and disaster recovery capabilities. Business continuity planning, backup modernization, and cyber-resilience initiatives are strengthening the role of next-generation storage solutions that offer enhanced reliability, automation, and data protection features.

What Opportunities Are Emerging in the Market?

The rapid expansion of cloud computing and edge computing environments presents substantial growth opportunities for next-generation storage vendors. As enterprises adopt hybrid and multi-cloud strategies, demand is rising for storage solutions that provide seamless interoperability, centralized management, and workload mobility across distributed environments. Edge deployments—supporting applications such as real-time analytics, industrial IoT, and remote operations—are further increasing the need for compact, high-speed storage systems.

Emerging data-intensive applications, including autonomous vehicles, smart city infrastructure, and AI-driven analytics, are generating new requirements for ultra-low latency and high-throughput storage architectures. Furthermore, growing emphasis on sustainability and energy efficiency is driving innovation in storage hardware and software designed to reduce power consumption, optimize data center footprints, and support green IT initiatives. These factors collectively expand the addressable market for advanced storage technologies.

By Storage Type: NAS Segment Expected to Dominate

The Network-Attached Storage (NAS) segment is projected to account for the largest share of the next-generation data storage market. NAS systems are widely adopted due to their scalability, centralized management, and ability to support unstructured data workloads such as media files, backups, and enterprise collaboration platforms. The growth of file-based workloads, remote work environments, and cloud-connected storage has further accelerated NAS adoption across enterprises. In contrast, Storage Area Networks (SAN) remain critical for high-performance block storage applications such as databases and virtualized environments, while Direct-Attached Storage (DAS) continues to serve small-scale and edge deployments where cost and simplicity are key considerations.

By Storage Medium: SSDs Witnessing the Fastest Growth

Solid-State Drives (SSDs) represent the fastest-growing segment due to their superior speed, lower latency, and energy efficiency compared to traditional hard disk drives (HDDs). The increasing adoption of NVMe and all-flash storage arrays in AI, analytics, and real-time processing environments is accelerating SSD demand. However, HDDs continue to hold a significant share in capacity-centric applications such as archiving and cold storage due to their cost-per-terabyte advantage. Magnetic tape remains relevant in long-term archival storage and regulatory compliance scenarios, particularly in sectors such as BFSI and government.

By Architecture: Object Storage Gaining Strong Momentum

File and object-based storage architectures are gaining strong traction, particularly object storage, due to their scalability and suitability for cloud-native applications and large-scale unstructured data. Object storage supports metadata-rich environments and is widely used in analytics, content repositories, and backup systems. Meanwhile, block storage remains essential for mission-critical applications, transactional databases, and virtualization workloads that require high IOPS and low latency.

By End User: IT & Telecom Leading Adoption

The IT & telecommunications sector is expected to hold the largest market share, driven by the exponential growth of data traffic, cloud services, and digital platforms. Telecom operators and hyperscale data center providers require high-performance and scalable storage infrastructures to manage streaming, 5G networks, and cloud workloads. Other significant adopters include BFSI (data security and compliance), healthcare (medical imaging and patient data), and manufacturing (industrial IoT and automation data).

By Geography: Asia-Pacific Emerging as High-Growth Region

Asia-Pacific is projected to witness the fastest growth through 2036 due to rapid digital transformation, expansion of data centers, and increasing cloud adoption in countries such as China, India, and South Korea. However, North America continues to hold the largest market share owing to early adoption of advanced storage technologies, the presence of hyperscale cloud providers, and strong enterprise IT spending.

Who Are the Key Players in the Global Next-Generation Data Storage Market?

The global next-generation data storage market features a mix of established infrastructure providers and specialized storage technology companies. Key players profiled in this report include Dell Technologies Inc., Hewlett Packard Enterprise Company, NetApp, Inc., International Business Machines Corporation, Huawei Technologies Co., Ltd., Hitachi Vantara Corporation, Pure Storage Inc., Kaminario Ltd., Tintri Inc., and Tegile Systems Inc.. These companies compete through portfolio expansion, innovation in flash and software-defined storage, strategic partnerships, and cloud-integrated offerings.

The global next-generation data storage market is valued at USD 53.5 billion in 2026 and is expected to reach approximately USD 100.6 billion by 2036.

The market is expected to grow at a CAGR of 6.5% from 2026 to 2036.

The key players include Dell Technologies Inc., Hewlett Packard Enterprise Company, NetApp Inc., International Business Machines Corporation, and Huawei Technologies Co., Ltd.

The main factors include exponential growth in digital data, increasing adoption of cloud computing, proliferation of IoT devices, and growing emphasis on data security and compliance.

North America is expected to maintain leadership, while Asia-Pacific is projected to experience the fastest growth during the forecast period.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Process

2.2. Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.1.1. Bottom-up Approach

2.3.1.2. Top-down Approach

2.3.1.3. Growth Forecast

2.4. Assumptions for the Study

2.5. Limitations for the Study

3. Executive Summary

4. Market Insights

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Growth in the Generation of Digital Data

4.2.1.1.1. Expansion of enterprise data volumes

4.2.1.1.2. Growth of cloud-native applications

4.2.1.1.3. Increasing multimedia and high-resolution content

4.2.1.2. Increasing Usage of the Internet of Things (IoT)

4.2.1.2.1. Rise in edge-generated data

4.2.1.2.2. Growth of industrial IoT deployments

4.2.1.2.3. Smart city and connected infrastructure initiatives

4.2.1.3. Proliferation of Mobile Computing Devices

4.2.1.3.1. Growth in mobile workforce data requirements

4.2.1.3.2. Rising demand for low-latency storage

4.2.1.3.3. Increased use of content streaming platforms

4.2.2. Restraints

4.2.2.1. High Infrastructure and Upgrade Costs

4.2.2.1.1. Capital-intensive storage modernization

4.2.2.1.2. Cost of transitioning from legacy systems

4.2.2.2. Data Security and Privacy Concerns

4.2.2.2.1. Risk of cyberattacks and data breaches

4.2.2.2.2. Compliance with regional data regulations

4.2.3. Opportunities

4.2.3.1. Expansion of Hybrid and Multi-Cloud Environments

4.2.3.1.1. Demand for scalable and flexible storage

4.2.3.1.2. Growth of cloud backup and disaster recovery

4.2.3.2. Advancements in NVMe and Flash Storage Technologies

4.2.3.2.1. Adoption of high-performance SSDs

4.2.3.2.2. Integration of NVMe-over-Fabrics

4.2.3.3. Growth in AI and Big Data Analytics

4.2.3.3.1. High-speed storage for AI workloads

4.2.3.3.2. Data lake and analytics infrastructure expansion

4.2.4. Challenges

4.2.4.1. Complexity in Data Management

4.2.4.1.1. Managing unstructured data growth

4.2.4.1.2. Integration across storage platforms

4.2.4.2. Energy Consumption of Data Centers

4.2.4.2.1. Power efficiency concerns

4.2.4.2.2. Sustainability compliance requirements

4.3. Trends

4.3.1. Adoption of Software-Defined Storage

4.3.2. Growth of Edge Storage Architectures

4.3.3. Increasing Use of Object Storage Systems

4.3.4. Integration of AI in Storage Optimization

4.4. Porter’s Five Forces Analysis

4.4.1. Threat of New Entrants

4.4.2. Bargaining Power of Suppliers

4.4.3. Bargaining Power of Buyers

4.4.4. Threat of Substitutes

4.4.5. Competitive Rivalry

5. Global Next-Generation Data Storage Market, by Storage Type

5.1. Introduction

5.2. Storage Area Network (SAN)

5.3. Network-Attached Storage (NAS)

5.4. Direct-Attached Storage (DAS)

6. Global Next-Generation Data Storage Market, by Storage Medium

6.1. Introduction

6.2. Hard Disk Drives (HDDs)

6.3. Solid-State Drives (SSDs)

6.4. Magnetic Tape

7. Global Next-Generation Data Storage Market, by Architecture

7.1. Introduction

7.2. File and Object-Based Storage

7.3. Block Storage

8. Next-Generation Data Storage Market, by End User

8.1. Introduction

8.2. BFSI

8.3. Healthcare

8.4. Retail

8.5. Manufacturing

8.6. Government

8.7. IT & Telecom

8.8. Other End Users

9. Next-Generation Data Storage Market, by Geography

9.1. Introduction

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. South Korea

9.4.4. India

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.6. Middle East & Africa

10. Competitive Landscape

10.1. Introduction

10.2. Key Growth Strategies

10.3. Market Share Analysis (2025)

10.3.1. Dell Technologies Inc.

10.3.2. Hewlett Packard Enterprise Company

10.3.3. NetApp, Inc.

10.3.4. International Business Machines Corporation

10.3.5. Huawei Technologies Co., Ltd.

11. Company Profiles

11.1. Dell Technologies Inc.

11.2. Hewlett Packard Enterprise Company

11.3. NetApp, Inc.

11.4. International Business Machines Corporation

11.5. Huawei Technologies Co., Ltd.

11.6. Hitachi Vantara Corporation

11.7. Pure Storage Inc.

11.8. Kaminario Ltd.

11.9. Tintri Inc.

11.10. Tegile Systems Inc.

11.11. Others

12. Appendix

12.1. Questionnaire

12.2. Available Customization

Subscribe to get the latest industry updates