Resources

About Us

Industrial Agitators Market Size, Share & Trends Analysis, by Product Type, Impeller Design, Sealing Arrangement, End-use Industry, and Geography — Global Opportunity Analysis & Forecast (2026–2036)

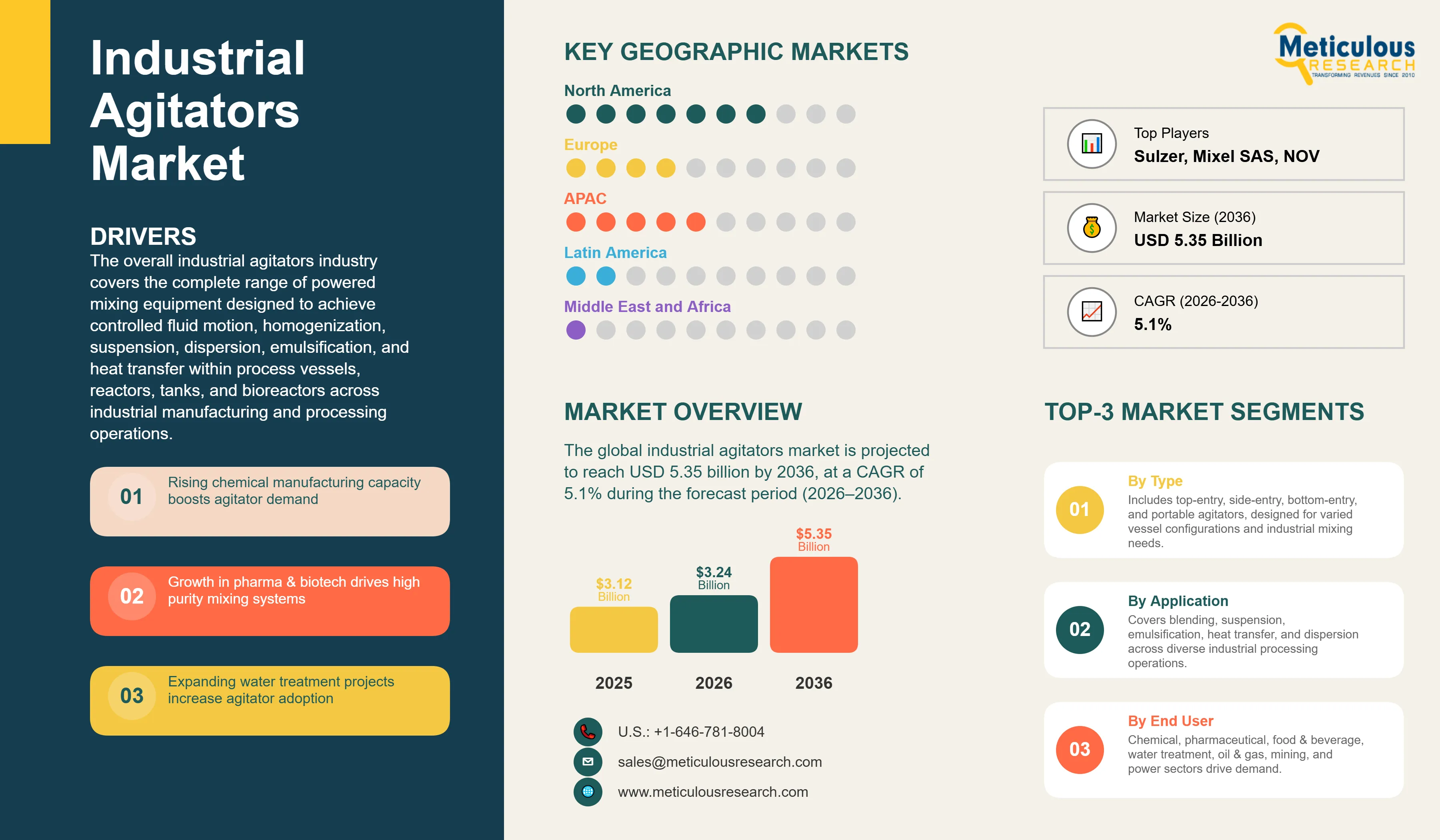

Report ID: MRSE - 1041959 Pages: 285 May-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global industrial agitators market was valued at USD 3.12 billion in 2025. The market is projected to reach USD 5.35 billion by 2036, growing from USD 3.24 billion in 2026 at a CAGR of 5.1% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The overall industrial agitators industry covers the complete range of powered mixing equipment designed to achieve controlled fluid motion, homogenization, suspension, dispersion, emulsification, and heat transfer within process vessels, reactors, tanks, and bioreactors across industrial manufacturing and processing operations. The market includes top-entry agitators, side-entry agitators, bottom-entry agitators, and portable drum agitators differentiated by mechanical configuration, impeller design, sealing arrangement, drive type, and materials of construction. These systems are deployed across a wide range of end-use industries including chemical processing, pharmaceutical and biotechnology, food and beverage processing, water and wastewater treatment, oil and gas, pulp and paper, mining and mineral processing, and power generation.

Industrial agitators are integral to process operations where inadequate mixing compromises product quality, reaction yield, heat transfer efficiency, phase separation, and process safety. The selection of agitator configuration, impeller geometry, and sealing technology is determined by the rheological properties of the process fluid, the required mixing intensity and flow pattern, vessel geometry, operating pressure and temperature conditions, and the level of sanitary or containment performance mandated by applicable regulatory standards. Agitators are engineered and supplied as both custom-configured capital equipment for new plant installations and as replacement units for aging process infrastructure, with aftermarket impeller, seal, and drive component supply representing a significant and growing share of overall market revenues.

The growth of the industrial agitators market is primarily driven by the continued expansion of global chemical manufacturing capacity and the accelerating buildout of pharmaceutical and biotechnology production infrastructure across Asia Pacific, North America, and the Middle East. In the United States, ongoing investment in chemical plant modernization and specialty chemical capacity expansion is sustaining steady demand for advanced agitation technology. The American Chemistry Council consistently identifies the United States as the world's second-largest chemical producer after China, with the domestic industry representing one of the largest single-market drivers of industrial process equipment demand globally.

The expansion of biopharmaceutical manufacturing capacity, driven by the growth of biologics, cell therapy, and mRNA vaccine production, is creating strong incremental demand for high-purity agitation systems capable of meeting the stringent cleanability, sterilizability, and containment requirements specified under U.S. FDA Current Good Manufacturing Practice regulations and European Medicines Agency GMP guidelines. Single-use bioreactor platforms, which increasingly incorporate integrated agitation assemblies designed for gamma-irradiated disposable vessel configurations, are opening a structurally new category of agitator demand within the pharmaceutical and biotechnology sector that is growing independently of conventional stainless steel vessel installations.

Growing investment in water and wastewater treatment infrastructure is also supporting sustained demand for agitation equipment used in coagulation, flocculation, sludge conditioning, and anaerobic digestion processes. The USD 55 billion allocated for water and wastewater infrastructure under the U.S. Infrastructure Investment and Jobs Act of 2021, being disbursed through annual program cycles, has reinforced capital spending on process equipment upgrades at municipal and industrial water treatment facilities across the United States through 2026 and beyond. Similar infrastructure investment programs underway in the European Union and across Asia Pacific are providing additional demand support for water treatment process equipment in major international markets.

Despite strong growth fundamentals, the market faces challenges related to the high degree of application-specific engineering required for agitator specification, particularly in complex rheological environments involving non-Newtonian fluids, high-viscosity process media, or multiphase systems with simultaneous gas, liquid, and solid phases. Corrosion-resistant and exotic alloy material requirements for aggressive chemical service applications add to capital procurement costs and extend delivery lead times. The growing complexity of hazardous area certification requirements under ATEX and NEC standards for agitators deployed in flammable process environments, combined with the validation and qualification burden associated with pharmaceutical process equipment procurement, continues to influence total cost of ownership calculations for industrial buyers.

The accelerating adoption of single-use bioreactor technology and the growing preference for modular and skid-mounted agitation solutions are creating significant opportunities for manufacturers that can offer validated, standardized designs compatible with diverse vessel configurations and process scales. The rapid growth of pharmaceutical contract manufacturing organizations globally, driven by the increasing preference of innovative drug developers to outsource manufacturing to specialized contract partners, is expanding the addressable market for GMP-compliant agitation equipment. In water and wastewater treatment, growing adoption of advanced anaerobic digestion and nutrient recovery processes is creating new application areas for specialized low-speed, high-torque agitation systems optimized for sludge and slurry handling.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 5.35 Billion |

|

Market Size in 2026 |

USD 3.24 Billion |

|

Market Size in 2025 |

USD 3.12 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 5.1% |

|

Dominating Product Type |

Top-entry Agitators |

|

Fastest Growing Product Type |

Bottom-entry Agitators |

|

Dominating Impeller Design |

Axial Flow Impellers |

|

Fastest Growing Impeller Design |

Mixed Flow Impellers |

|

Dominating Sealing Arrangement |

Mechanical Seal Agitators |

|

Fastest Growing Sealing Arrangement |

Magnetic Drive Agitators |

|

Dominating End-use Industry |

Chemical Processing |

|

Fastest Growing End-use Industry |

Pharmaceutical & Biotechnology |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Biopharmaceutical Manufacturing Expansion and Evolving GMP Regulatory Requirements Accelerating Demand for High-Purity Agitation Systems

The rapid global expansion of biopharmaceutical manufacturing capacity is emerging as one of the most structurally significant growth drivers for the industrial agitators market over the forecast period. The proliferation of biologics, monoclonal antibody therapies, cell and gene therapies, and mRNA vaccine manufacturing has created a fundamentally new category of agitation demand characterized by requirements for sanitary design, full vessel drainability, Clean-in-Place and Steam-in-Place compatibility, and validated surface finish standards that differ substantially from conventional chemical processing agitator specifications. According to the U.S. FDA, the number of biological license applications received by the agency reached record levels in recent years, reflecting the sustained pipeline activity driving new biopharmaceutical manufacturing investment across the United States, Europe, and Asia Pacific.

The U.S. FDA's Current Good Manufacturing Practice regulations and the EMA's GMP guidelines for medicinal products impose stringent documentation, material traceability, and design qualification requirements on process equipment used in pharmaceutical manufacturing, including agitation systems. These requirements are compelling pharmaceutical manufacturers to invest in purpose-engineered agitators designed and certified in compliance with ASME BPE (Bioprocessing Equipment) standards, which specify surface finish, weld quality, material traceability, and hygienic design parameters for all product-contact components. The growing adoption of single-use bioreactor systems, which require agitation assemblies specifically designed for gamma-irradiated disposable vessel liners, is further expanding the technology scope of pharmaceutical agitation, creating a new and rapidly growing commercial segment for disposable impeller and agitator shaft assemblies that is adding incremental revenue to the market independent of conventional capital equipment cycles.

Manufacturers including EKATO Group, Alfa Laval AB, and SPX Flow, Inc. have responded to this demand shift by expanding their high-purity and pharmaceutical-grade agitator product lines with configurations certified to ASME BPE, FDA 21 CFR, and EHEDG standards. The growing participation of contract development and manufacturing organizations in biopharmaceutical production, which requires flexible multi-product manufacturing platforms capable of rapid changeover between different therapeutic modalities, is reinforcing demand for standardized, fully drainable, and easily qualifiable agitator configurations across a broader base of pharmaceutical manufacturing sites globally. India's Government-backed Production-Linked Incentive scheme for pharmaceutical manufacturing, approved with a total outlay of approximately USD 1.8 billion, is additionally accelerating the construction of new GMP-compliant pharmaceutical facilities in India that are driving incremental agitator procurement across the Asia Pacific region.

Industrial IoT Integration and Smart Agitator Platforms Redefining Process Optimization and Predictive Maintenance

The integration of smart sensor technology, industrial IoT connectivity, and advanced data analytics into industrial agitator platforms is progressively transforming the operational model of agitation system ownership from periodic reactive maintenance toward continuous, condition-based process monitoring and optimization. Traditional agitator management relied on fixed maintenance schedules, manual torque and vibration checks, and empirical process adjustment, resulting in undetected seal degradation, unplanned mechanical failures, and suboptimal mixing performance that directly impacted product quality and process throughput in critical manufacturing environments.

Connected agitator platforms incorporate embedded sensors for real-time monitoring of shaft torque, vibration, bearing temperature, mechanical seal condition, and motor power consumption, providing operators with continuous visibility into agitator health and process performance. Companies such as EKATO Group and SPX Flow, Inc. have integrated smart monitoring and process optimization capabilities into their agitator control platforms, enabling operators to track mixing performance metrics in real time and correlate mechanical parameters with process outcomes. Sulzer Ltd offers digital performance monitoring solutions for its agitation equipment that enable remote diagnostics and alert-driven maintenance scheduling, reducing unplanned downtime in continuous manufacturing operations.

The business case for connected agitator monitoring is particularly compelling in pharmaceutical batch manufacturing, specialty chemical synthesis, and fermentation applications where process deviations attributable to agitator underperformance can result in product quality failures, batch rejections, and costly manufacturing investigations. In large-scale chemical plants operating hundreds of process vessels simultaneously, centralized digital monitoring of distributed agitator assets reduces the operational burden associated with manual inspection rounds and enables maintenance resources to be deployed more efficiently based on actual equipment condition rather than fixed time-based schedules. This trend is accelerating the shift from transactional agitator procurement toward integrated equipment, monitoring, and service offerings that improve customer retention and generate predictable aftermarket revenue streams for leading system manufacturers.

Magnetic Drive Agitator Technology Gaining Strong Commercial Traction in Pharmaceutical, Fine Chemical, and Hazardous Fluid Processing Applications

The accelerating displacement of conventional mechanically sealed agitator designs by magnetic drive configurations in pharmaceutical, fine chemical, and hazardous material processing applications represents one of the most significant product-level technology transitions currently shaping the competitive landscape of the global industrial agitators market. Magnetic drive agitators eliminate the rotating shaft seal entirely, using a hermetically sealed, leak-proof magnetic coupling to transmit rotational torque from the drive motor through the vessel wall to the internal impeller assembly. This design eliminates the risk of process fluid leakage at the shaft seal, which represents a critical compliance concern in pharmaceutical GMP manufacturing environments and a significant process safety and environmental liability in applications involving toxic, carcinogenic, or highly flammable chemical compounds.

In pharmaceutical manufacturing, the zero-emission operating profile of magnetic drive agitators aligns with the increasing emphasis on containment engineering and operator exposure limits for highly potent active pharmaceutical ingredients, where trace-level leakage from a conventional mechanical seal can generate unacceptable occupational exposure risks. In fine chemicals and specialty chemical processing, the elimination of seal-related maintenance requirements reduces operational intervention frequency in corrosive and aggressive service environments, improving both operational safety and total equipment lifecycle cost. The tightening of fugitive emission standards under the U.S. EPA's National Emission Standards for Hazardous Air Pollutants and the EU's Industrial Emissions Directive is further reinforcing adoption of leak-free agitator designs across chemical manufacturing facilities handling volatile organic compounds and hazardous chemical intermediates.

Manufacturers including EKATO Group, Jongia Mixing Technology B.V., and GMM Pfaudler Ltd. have expanded their magnetic drive agitator portfolios to address a growing range of vessel sizes, operating pressures, and process fluid viscosities, extending the applicability of this technology beyond its original niche in small-volume, high-purity pharmaceutical reactors into broader industrial chemical processing applications. The commercial momentum behind this technology transition is further supported by total ownership cost analyses that demonstrate the elimination of recurring mechanical seal replacement costs and associated downtime expenses can offset the higher initial capital premium of magnetic drive configurations within three to five years of operation in high-utilization chemical and pharmaceutical process environments.

By Product Type: In 2026, the Top-entry Agitators Segment to Dominate the Global Industrial Agitators Market

Based on product type, the industrial agitators industry is segmented into top-entry agitators, side-entry agitators, bottom-entry agitators, and portable drum agitators. In 2026, the top-entry agitators segment is expected to account for the largest share of this market. The leading position of this segment is attributed to the versatility of top-entry configurations across the widest range of vessel sizes, process fluid types, and mixing duty classifications, from gentle blending of pharmaceutical intermediates in glass-lined reactors to high-intensity dispersing and emulsification in large-scale chemical synthesis vessels. Top-entry agitators are compatible with the full range of standard and specialty impeller designs, support multiple sealing arrangements including mechanical seals, magnetic drives, and stuffing box seals, and can be engineered for operating pressures ranging from atmospheric to high-pressure reactor service, making them the standard configuration selection for the large majority of new industrial process vessel installations globally. Gear drive top-entry configurations, which dominate within this segment, provide the high-torque, low-speed performance required for viscous process applications in polymer, adhesive, and personal care product manufacturing. Leading product lines from SPX Flow, Inc., including the Lightnin XJ and XT series, and from EKATO Group's reactor agitator range, exemplify the continued product development investment sustaining this segment's dominant commercial position.

However, the bottom-entry agitators segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by accelerating adoption in sterile biopharmaceutical manufacturing, where bottom-mounted configurations enable superior vessel drainability, reduce the risk of top-entry shaft seal contamination in aseptic processing environments, and are increasingly specified as the preferred design in single-use bioreactor systems. The growing adoption of bottom-entry agitators in specialty chemical applications requiring fully enclosed, zero-headspace vessel operation, combined with expanding global bioreactor manufacturing capacity, is expected to drive above-average growth for this segment over the forecast period.

By Impeller Design: In 2026, the Axial Flow Impellers Segment to Hold the Largest Share

Based on impeller design, the industrial agitators industry is segmented into axial flow impellers, radial flow impellers, and mixed flow impellers. In 2026, the axial flow impellers segment is expected to account for the largest share of this market. The growth of this segment is driven by the broad suitability of axial flow geometries for the most common industrial mixing duties including bulk blending of miscible liquids, solid particle suspension, heat transfer enhancement, and gas dispersion in fermentation and biological process applications. High-efficiency hydrofoil impeller designs such as SPX Flow's A310 series and Alfa Laval's Scaba range deliver low power consumption per unit of mixing intensity, making them the default selection for energy-conscious process operators across chemical, food and beverage, and water treatment applications. The large installed base of axial flow impeller configurations across the global installed agitator fleet, combined with the recurring replacement and upgrade market for impeller components, ensures that this segment retains its dominant revenue position throughout the forecast period.

However, the mixed flow impellers segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by growing demand for impeller geometries that provide both axial and radial flow components within a single configuration, enabling process engineers to achieve efficient bulk blending and moderate shear simultaneously in multipurpose reactors and bioreactors handling a broader range of process fluids and mixing objectives than single-purpose axial or radial designs can address efficiently. The increasing adoption of multipurpose reaction vessels in pharmaceutical API manufacturing and in specialty chemical contract manufacturing, driven by the need for capital-efficient flexible production platforms, is reinforcing procurement of mixed flow impeller configurations that can deliver adequate performance across diverse process duties without vessel redesign.

By Sealing Arrangement: In 2026, the Mechanical Seal Agitators Segment to Account for the Largest Share

Based on sealing arrangement, the industrial agitators industry is segmented into mechanical seal agitators, magnetic drive agitators, and stuffing box/packing seal agitators. In 2026, the mechanical seal agitators segment is expected to account for the largest share of this market. This growth is mainly driven by the widespread deployment of mechanical seal configurations across the established installed base of agitators serving chemical, food and beverage, water treatment, and general industrial process applications, where mechanical seals provide reliable shaft sealing performance across a broad range of operating conditions at a lower capital cost than magnetic drive alternatives. Single and double mechanical seal configurations remain the dominant sealing selection for new agitator installations across the large majority of industrial process applications that do not have hermetic containment requirements, and the significant installed base of mechanically sealed agitators globally generates a large and recurring aftermarket for seal component replacements that contributes materially to overall segment revenues.

However, the magnetic drive agitators segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by growing regulatory pressure for zero-emission operation in pharmaceutical and chemical manufacturing, the increasing stringency of hazardous chemical containment requirements under EPA and EU industrial emissions directives, and the total lifecycle cost advantages of seal-less operation in corrosive and abrasive service environments where conventional mechanical seal replacement represents a recurring maintenance cost and process downtime burden. The expanding commercial portfolio of magnetic drive agitator designs now covers vessel sizes from small-scale laboratory reactors to large-scale industrial chemical vessels, with operating pressure capabilities exceeding 100 bar in high-performance configurations, significantly broadening the addressable market for this technology segment.

By End-use Industry: In 2026, the Chemical Processing Segment to Hold the Largest Share

Based on end-use industry, the industrial agitators industry is segmented into chemical processing, pharmaceutical and biotechnology, food and beverage processing, water and wastewater treatment, oil and gas, pulp and paper, mining and mineral processing, power generation, and other end-use industries. In 2026, the chemical processing segment is expected to account for the largest share of this market, reflecting the position of the global chemical industry as the largest and most process-intensive consumer of industrial agitation equipment globally. Chemical processing encompasses reaction, blending, dissolution, neutralization, polymerization, crystallization, and formulation operations that collectively represent the broadest agitator application base across all industrial sectors, spanning commodity petrochemicals, specialty chemicals, agrochemicals, adhesives, coatings, and performance materials manufacturing. The ongoing expansion of specialty chemical and agrochemical manufacturing capacity across North America, Europe, and Asia Pacific is continuously adding new process vessel installations that require engineered agitation solutions. OSHA's Process Safety Management standard and EPA's Risk Management Program continue to drive compliance-led investment in process equipment upgrades across chemical manufacturing facilities in the United States, reinforcing procurement of compliant and reliably performing agitation systems.

However, the pharmaceutical and biotechnology segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the global expansion of biological medicine manufacturing capacity, the rapid commercialization of cell therapy and gene therapy products requiring specialized bioreactor agitation systems, and the stringent GMP-compliant agitator design and qualification requirements imposed by the U.S. FDA, EMA, and national regulatory authorities that compel pharmaceutical manufacturers to invest in purpose-engineered, validated, and fully documented agitation equipment. The parallel growth of pharmaceutical contract manufacturing organizations globally, driven by the increasing preference of innovative drug developers to outsource production to specialized contract partners, is generating incremental demand for flexible, multi-product agitator configurations across a broadening global network of GMP-certified manufacturing facilities. The pharmaceutical and biotechnology segment is also unique in its requirement for full design qualification documentation, Factory Acceptance Testing protocols, and post-installation qualification packages that generate additional professional service revenues alongside capital equipment sales for leading agitator manufacturers.

Based on geography, the overall industrial agitators market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of this market. This growth is driven by the presence of one of the world's largest and most technologically advanced chemical manufacturing bases, the sustained expansion of biopharmaceutical and specialty chemical manufacturing capacity, and the enforcement of stringent process safety, occupational health, and environmental regulations by OSHA and the EPA that drive investment in compliant, high-quality agitation equipment across the region's broad industrial manufacturing base. The United States in particular benefits from ongoing capital investment in water and wastewater treatment infrastructure, supported by the USD 55 billion water infrastructure commitment under the Infrastructure Investment and Jobs Act of 2021, which is sustaining procurement of process equipment including agitation systems at municipal and industrial water treatment facilities across the country. The presence of leading agitator manufacturers including SPX Flow, Inc., Philadelphia Mixing Solutions, Ltd., ProQuip Inc., and Brawn Mixer, Inc. ensures a deep local supply base and extensive aftermarket support infrastructure that reinforces procurement confidence among North American industrial operators. The large installed base of aging agitators across chemical, food processing, and water treatment sectors is additionally generating a growing replacement and upgrade market that provides demand support independent of new plant construction activity.

However, the Asia Pacific industrial agitators market is expected to grow at the fastest rate from 2026 to 2036. The rapid growth of this market is driven by the massive expansion of chemical, pharmaceutical, food and beverage, and water treatment manufacturing capacity across China, India, Japan, South Korea, and Southeast Asia. India's chemical industry, supported by Government of India Production-Linked Incentive schemes for specialty chemicals and pharmaceutical active ingredient manufacturing, is expanding rapidly across multiple product categories, driving sustained demand for process equipment including industrial agitators across a growing number of greenfield and brownfield plant installations. China's extensive network of chemical industrial parks, combined with ongoing capacity expansion in pharmaceutical API manufacturing, food processing, and municipal water infrastructure, is generating broad-based demand for agitation equipment across multiple end-use sectors. The rapid development of municipal water and wastewater treatment infrastructure across Southeast Asia, driven by urbanization, population growth, and increasing regulatory enforcement of water quality standards, is additionally creating a growing demand base for agitation equipment used in water treatment process applications across markets including Vietnam, Indonesia, Thailand, and the Philippines.

Europe is a large and well-established market for industrial agitators, supported by a highly developed chemical, pharmaceutical, and food and beverage manufacturing base and a strong regulatory environment that enforces rigorous process safety, occupational exposure, and industrial emissions standards across manufacturing operations. The enforcement of the EU's Industrial Emissions Directive and the implementation of the Seveso III Directive governing major accident hazards at chemical facilities continue to drive compliance-led investment in process equipment upgrades across European industrial facilities. European manufacturers including EKATO Group (Germany), Sulzer Ltd (Switzerland), Alfa Laval AB (Sweden), Jongia Mixing Technology B.V. (Netherlands), Mixel SAS (France), and STELZER Rührtechnik International GmbH (Germany) maintain strong market positions in their home region supported by deep application engineering expertise, established customer relationships across European process industries, and close integration with the region's highly developed engineering, procurement, and construction contractor ecosystem.

The global industrial agitators market is moderately fragmented at the system level, with competition primarily driven by the depth and breadth of product portfolios across entry configurations, impeller designs, and sealing arrangements, the strength of application engineering capabilities across end-use industries, compliance with industry-specific regulatory and hygienic design standards, and the scale and geographic reach of aftermarket impeller, seal, and drive component supply networks.

Large diversified process equipment manufacturers such as SPX Flow, Inc. and Sulzer Ltd compete through comprehensive product portfolios covering multiple agitator configurations and a wide range of end-use industry applications, supported by global manufacturing footprints and extensive aftermarket service organizations that generate recurring revenue alongside capital equipment sales. Specialized agitator manufacturers including EKATO Group and Philadelphia Mixing Solutions, Ltd. compete through superior application engineering depth and proprietary impeller technology, with EKATO maintaining particular strength in high-viscosity and high-pressure chemical reactor agitation and in large-scale industrial fermentation and biotechnology applications. Alfa Laval AB and Jongia Mixing Technology B.V. have built strong competitive positions in sanitary and hygienic agitation for pharmaceutical and food and beverage industries through purpose-engineered product lines compliant with ASME BPE, EHEDG, and 3-A Sanitary Standards. Regionally focused manufacturers including GMM Pfaudler Ltd. and Satake Chemical Equipment Mfg., Ltd. compete effectively across Asia Pacific by combining locally competitive pricing with application engineering expertise well suited to the chemical and pharmaceutical industries dominant in their home markets. NOV Inc. serves process industries including oil and gas and chemical processing through its Chemineer product line, competing on the strength of established specification positions and a large global distribution network across energy-producing markets.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global industrial agitators market include SPX Flow, Inc. (U.S.), EKATO Group (Germany), Sulzer Ltd (Switzerland), Alfa Laval AB (Sweden), Philadelphia Mixing Solutions, Ltd. (U.S.), Jongia Mixing Technology B.V. (Netherlands), Dynamix Agitators Inc. (Canada), GMM Pfaudler Ltd. (India), Satake Chemical Equipment Mfg., Ltd. (Japan), Mixel SAS (France), ProQuip Inc. (U.S.), Brawn Mixer, Inc. (U.S.), STELZER Rührtechnik International GmbH (Germany), Xylem Inc. (U.S.), and NOV Inc. (U.S.), among others.

The global industrial agitators market is expected to reach USD 5.35 billion by 2036 from an estimated USD 3.24 billion in 2026, at a CAGR of 5.1% during the forecast period 2026–2036.

In 2026, the top-entry agitators segment is expected to hold the largest share of this market, driven by its broad process applicability across blending, homogenization, suspension, and heat transfer operations in chemical, pharmaceutical, food and beverage, and water treatment applications.

The bottom-entry agitators segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by growing adoption in sterile biopharmaceutical manufacturing, high-containment bioreactor applications, and specialty chemical synthesis processes that require minimal contamination risk and full vessel drainability.

In 2026, the axial flow impellers segment is expected to hold the largest share of this market, reflecting the broad suitability of axial flow geometries for bulk blending, solid suspension, heat transfer, and gas dispersion duties across the most common industrial agitator applications.

The mixed flow impellers segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by growing demand for versatile impeller configurations that deliver efficient bulk blending and moderate dispersing performance in multipurpose reactors and bioreactors handling diverse process fluids.

In 2026, the mechanical seal agitators segment is expected to hold the largest share of this market, driven by its established position as the standard sealing solution across the broad range of industrial agitator applications where hermetic containment requirements do not apply.

In 2026, the chemical processing segment is expected to hold the largest share of this market, reflecting the broad and continuous agitation requirements of this sector across reaction, blending, dissolution, polymerization, crystallization, and formulation operations.

The growth of this market is primarily driven by the global expansion of biopharmaceutical and specialty chemical manufacturing capacity, growing investment in water and wastewater treatment infrastructure across North America, Asia Pacific, and the Middle East, tightening GMP and process safety regulatory requirements compelling investment in validated and compliant agitation equipment, the integration of smart monitoring and IoT capabilities into agitator platforms, and the accelerating adoption of magnetic drive and sanitary agitator technologies in pharmaceutical and high-purity chemical applications.

Key players in the global industrial agitators market include SPX Flow, Inc. (U.S.), EKATO Group (Germany), Sulzer Ltd (Switzerland), Alfa Laval AB (Sweden), Philadelphia Mixing Solutions, Ltd. (U.S.), Jongia Mixing Technology B.V. (Netherlands), Dynamix Agitators Inc. (Canada), GMM Pfaudler Ltd. (India), Satake Chemical Equipment Mfg., Ltd. (Japan), Mixel SAS (France), ProQuip Inc. (U.S.), Brawn Mixer, Inc. (U.S.), STELZER Rührtechnik International GmbH (Germany), Xylem Inc. (U.S.), and NOV Inc. (U.S.).

Asia Pacific is expected to register the highest growth rate in the global industrial agitators market during the forecast period 2026–2036, driven by rapid expansion of chemical, pharmaceutical, and food and beverage manufacturing capacity, increasing enforcement of industrial process safety and water quality regulations, and growing investment in municipal water and wastewater treatment infrastructure across the region.

Published Date: Nov-2024

Published Date: Jan-2023

Published Date: Apr-2022

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates