Resources

About Us

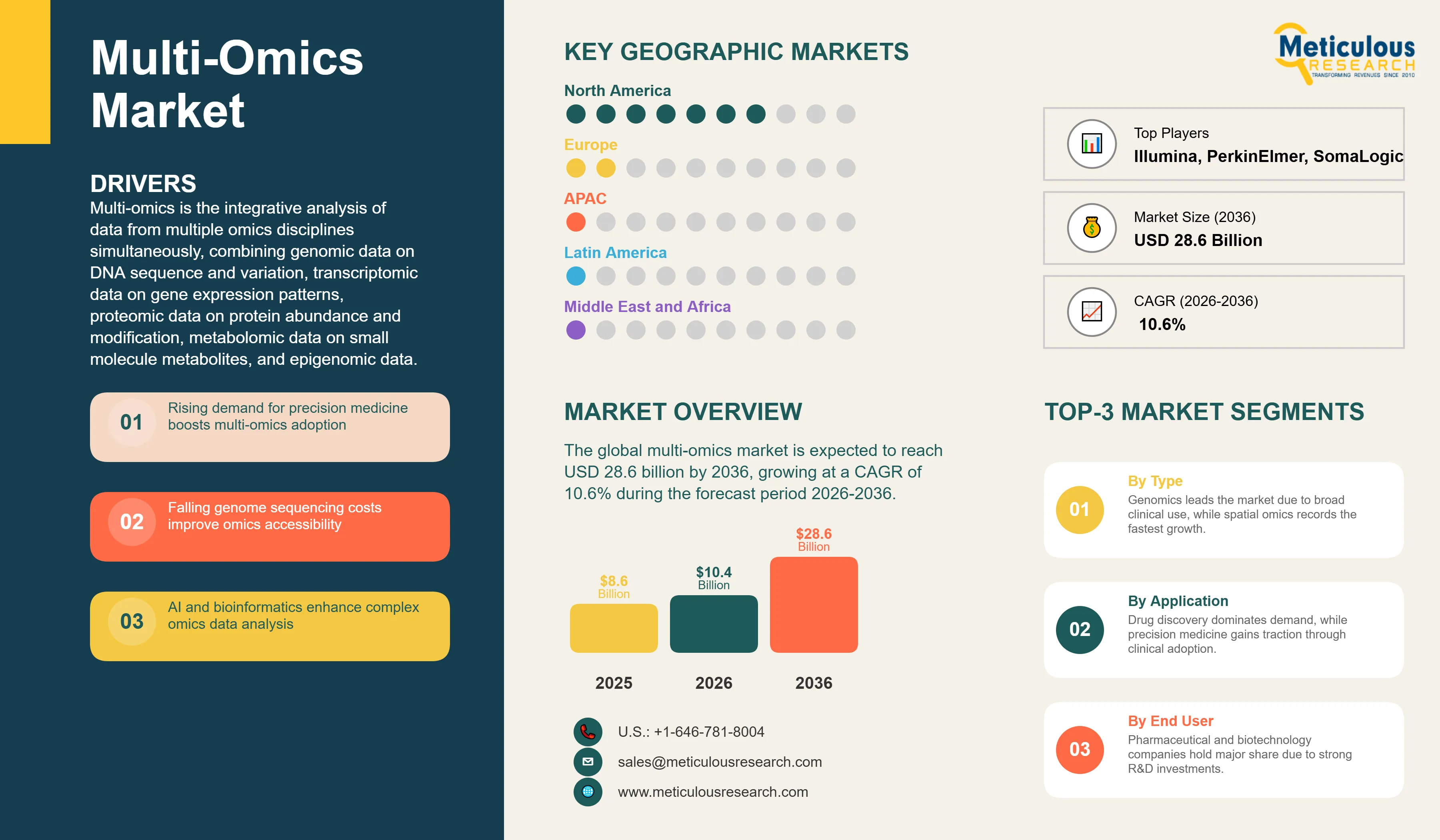

The global multi-omics market was valued at USD 8.6 billion in 2025. This market is expected to reach USD 28.6 billion by 2036 from an estimated USD 10.4 billion in 2026, growing at a CAGR of 10.6% during the forecast period 2026-2036. According to the National Human Genome Research Institute's 2025 sequencing cost database, the cost of sequencing a human genome has fallen below USD 200, a more than 500,000-fold reduction from the USD 100 million cost in 2001, and this extraordinary cost reduction is the fundamental enabling condition for the multi-omics market by making the simultaneous measurement of molecular features across multiple biological layers economically feasible for both research and increasingly clinical applications.

Click here to: Get Free Sample Pages of this Report

Multi-omics is the integrative analysis of data from multiple omics disciplines simultaneously, combining genomic data on DNA sequence and variation, transcriptomic data on gene expression patterns, proteomic data on protein abundance and modification, metabolomic data on small molecule metabolites, and epigenomic data on DNA methylation and chromatin structure, to build a more complete and mechanistically grounded picture of biological systems than any single omics layer can provide alone. Where genomics can identify a disease-associated genetic variant, multi-omics can additionally reveal how that variant alters gene expression, which proteins are affected and how their function changes, what metabolic perturbations result, and how epigenetic modifications modulate the entire cascade. This layered molecular understanding is the foundation for precision medicine, which requires matching treatments to the specific molecular profile of individual patients and tumors.

The market is growing because the scientific and clinical value of multi-omics is being validated at scale. The UK Biobank, which collected multi-omics data from approximately 500,000 UK participants, has generated thousands of peer-reviewed publications demonstrating associations between molecular features across omics layers and disease outcomes that single-omics analysis could not detect. According to the Broad Institute's 2025 research publication summary, multi-omics integration studies published in high-impact journals grew by approximately 45% in 2024 compared with 2023, reflecting the rapidly expanding scientific community applying these methods. The pharmaceutical industry's recognition of multi-omics as a drug discovery tool is reflected in the very large investment Pharma companies have made in multi-omics capabilities: AstraZeneca's partnership with the UK Biobank and Wellcome Sanger Institute for multi-omics drug target discovery, Pfizer's investment in proteomics-driven drug discovery through its partnership with SomaLogic, and Roche's acquisition of Flatiron Health and Foundation Medicine as part of a broader data-driven precision oncology strategy all represent major corporate commitments to multi-omics-informed drug development.

Two technology advances are currently transforming the multi-omics landscape. Single-cell omics, which allows molecular profiling of individual cells rather than bulk tissue averages, has revealed that the biological heterogeneity within apparently homogeneous cell populations is far greater than previously understood, fundamentally changing how researchers think about tumor biology, immune responses, and developmental processes. According to 10x Genomics' 2025 annual report, the company shipped systems to over 8,000 customer sites globally, reflecting the rapid spread of single-cell omics capability across the research community. Spatial omics, which combines single-cell resolution molecular profiling with spatial information about where each cell sits within a tissue, is the most recently emerged and fastest-growing omics category, enabling researchers to understand how cellular diversity maps onto tissue architecture and how cellular neighborhoods influence cell behavior.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 28.6 Billion |

|

Market Size in 2026 |

USD 10.4 Billion |

|

Market Size in 2025 |

USD 8.6 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 10.6% |

|

Dominating Omics Type |

Genomics |

|

Fastest Growing Omics Type |

Spatial Omics |

|

Dominating Product & Service |

Instruments |

|

Fastest Growing Product & Service |

Software & Bioinformatics Platforms |

|

Dominating Technology |

NGS-based Technologies |

|

Fastest Growing Technology |

Single-cell Technologies |

|

Dominating Application |

Drug Discovery & Development |

|

Fastest Growing Application |

Clinical Diagnostics & Precision Medicine |

|

Dominating End User |

Pharmaceutical & Biotechnology Companies |

|

Fastest Growing End User |

Clinical Laboratories |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Single-Cell and Spatial Omics Revolutionizing Biological Understanding

The emergence of single-cell omics technologies, led commercially by 10x Genomics' Chromium single-cell RNA sequencing platform and its newer Visium spatial transcriptomics platform, has created an entirely new category of multi-omics research capability that is transforming how biologists and clinicians understand disease. Where conventional bulk RNA sequencing measures the average gene expression of thousands of cells together, masking the diversity of cell states within a sample, single-cell RNA sequencing profiles each individual cell separately, enabling researchers to identify rare cell populations, trace developmental trajectories, and characterize the cellular heterogeneity of tumors that drives treatment resistance. According to 10x Genomics' 2025 annual report, the company generated revenues of approximately USD 611 million in 2024, growing above its overall average in its Chromium single-cell and Visium spatial platforms, confirming strong commercial momentum in both single-cell and spatial omics.

The 2022 Human Cell Atlas initiative, which aims to create a comprehensive reference map of every cell type in the human body using single-cell omics, has published cell atlases for multiple organs and tissues that have become foundational reference datasets for the entire biomedical research community. Nature published a special series on the Human Cell Atlas in 2024 highlighting its completion of atlases for the human lung, gut, and fetal development, establishing these datasets as essential resources for pharmaceutical drug target discovery and disease mechanism research. Spatial omics is extending the capabilities of single-cell analysis by adding the tissue context that cell dissociation for single-cell sequencing destroys, enabling researchers to understand not just which cell types are present but where they are in the tissue and how they interact with their neighbors. 10x Genomics' Xenium in situ platform and Vizgen's MERFISH platform are leading the commercialization of subcellular spatial transcriptomics, which can map thousands of RNA transcripts within intact tissue sections at subcellular resolution.

AI-driven Multi-Omics Integration Enabling New Drug Target Discovery

The integration of artificial intelligence with multi-omics datasets is enabling drug target discovery at a scale and speed that was impossible with conventional bioinformatics approaches, creating a new category of AI-driven drug discovery that is attracting very large pharmaceutical industry investment. The fundamental challenge of multi-omics data integration is that different omics layers use different measurement technologies, different scales of data, and different biological reference frameworks, requiring sophisticated computational methods to identify the true biological signal across layers rather than spurious correlations driven by technical noise. Deep learning models that have been trained on large multi-omics datasets from cohorts like the UK Biobank and The Cancer Genome Atlas are increasingly capable of identifying multi-omics signatures that predict disease progression, treatment response, and drug target vulnerability with accuracy that exceeds single-omics approaches.

According to Recursion Pharmaceuticals' 2025 investor communications, its AI platform has integrated multi-omics data across phenomics, transcriptomics, and chemical biology to identify drug targets and design clinical candidates at a scale that traditional drug discovery cannot match, with multiple programs advancing into clinical trials based on AI-multi-omics driven target identification. Exscientia and several other AI drug discovery companies have also published results demonstrating that multi-omics-informed AI target identification leads to higher clinical trial success rates than conventional approaches, a critical validation for the pharmaceutical industry. The pharmaceutical industry's investment in multi-omics AI capabilities is reflected in a series of large partnership deals: AstraZeneca disclosed a multi-year multi-omics AI drug discovery collaboration with BenevolentAI, and Pfizer's ongoing partnership with SomaLogic for proteomics-informed drug discovery continues to generate novel target identification data.

Long-Read Sequencing Expanding Multi-Omics Capability Across Genome Complexity

The commercial maturation of long-read sequencing technologies from Pacific Biosciences and Oxford Nanopore Technologies is extending multi-omics capability into genomic regions and molecular events that short-read NGS cannot characterize, including structural variants, repeat expansions, full-length RNA isoforms, and direct detection of DNA base modifications without bisulfite conversion. Short-read sequencing, which generates reads of 150 to 300 base pairs, struggles to resolve complex structural variants, repetitive genome regions, and the phasing of genetic variants across chromosome-length haplotypes, all of which are biologically important for understanding disease mechanisms. Long-read sequencing, which generates reads of tens of thousands to millions of base pairs, can resolve these genomic complexities and simultaneously detect DNA methylation during sequencing without separate library preparation steps.

According to Oxford Nanopore Technologies' 2025 annual report, the company generated revenues of approximately GBP 183 million in 2024 with growing adoption in research, clinical genomics, and pathogen surveillance applications where its nanopore sequencing technology's real-time output and portability offer advantages over conventional NGS. Pacific Biosciences reported growing demand for its Revio long-read sequencing system, which dramatically increased throughput and reduced cost compared with its previous generation, making long-read sequencing economically feasible for whole-genome population studies that were previously cost-prohibitive. The combination of long-read sequencing for structural and epigenomic characterization with short-read NGS for high-coverage variant calling and bulk or single-cell transcriptomics is emerging as a powerful multi-omics design for comprehensive molecular profiling of complex diseases.

Growing Demand for Precision Medicine

Precision medicine, which tailors treatment decisions to the specific molecular characteristics of individual patients and their diseases, is the primary commercial driver of multi-omics market growth because it creates clinical demand for the comprehensive molecular profiling that only multi-omics integration can provide. According to the Pharmaceutical Research and Manufacturers of America's 2025 annual report, over 2,000 medicines are in clinical development in the United States, and precision oncology represents the largest and most molecularly stratified subset of this pipeline. The growing commercial adoption of FDA-approved companion diagnostics for targeted therapies creates direct clinical demand for genomic and transcriptomic profiling, and the progressive expansion of precision medicine beyond oncology into rare genetic diseases, cardiovascular disease, and psychiatric conditions is driving multi-omics adoption across new therapeutic areas. The All of Us Research Program, which aims to collect genomic and other omics data from at least one million U.S. participants according to NIH's 2025 progress report, represents the largest government investment in population-scale multi-omics for precision medicine in the world.

Rising Adoption of AI & Bioinformatics

The rapid advancement of AI and machine learning capabilities for biological data analysis is directly enabling multi-omics integration at the scale and sophistication required to extract clinically and commercially actionable insights from complex multi-dimensional datasets. Transformer-based language models adapted for biological sequences, graph neural networks for molecular interaction networks, and multimodal deep learning architectures that can jointly analyze data across multiple omics layers are all creating new analytical capabilities that are accelerating the pace of multi-omics discovery. According to a 2025 analysis published in Nature Methods, AI-based multi-omics integration methods identified biologically validated associations between omics layers at a rate approximately three times higher than conventional statistical correlation methods in a benchmark comparison across cancer datasets, providing quantitative evidence of AI's analytical advantage for multi-omics research.

Integration with Clinical Diagnostics

The progressive integration of multi-omics profiling into clinical diagnostic workflows represents the largest near-term commercial expansion opportunity for the multi-omics market, as clinical diagnostics volumes at scale are orders of magnitude larger than research volumes. The FDA's approval of comprehensive genomic profiling assays including Foundation Medicine's FoundationOne CDx, which profiles hundreds of cancer genes from tissue or liquid biopsy, has established multi-gene oncology profiling as a clinical standard of care. The extension of profiling to transcriptomics for gene fusion detection, methylomics for cancer type identification in liquid biopsy, and proteomics for protein biomarker quantification is progressively moving clinical diagnostics toward a multi-omics model for the most complex and therapeutically important diagnostic questions. According to IQVIA's 2025 Oncology Trends report, comprehensive molecular profiling in oncology grew at above-average rates in 2024, with multi-analyte profiling panels capturing a growing share of total oncology molecular testing volume.

Growth in Drug Discovery and Biomarker Identification

The pharmaceutical industry's shift toward data-driven drug target identification using population-scale multi-omics data is creating growing demand for the instruments, reagents, software, and services that enable large-scale omics profiling. The UK Biobank's multi-omics data from approximately 500,000 participants, including genomics, proteomics, metabolomics, and imaging data, has enabled the identification of hundreds of novel drug targets through multi-omics association studies published in landmark papers in Nature and other high-impact journals. According to AstraZeneca's 2025 annual report, the company has used the UK Biobank multi-omics data to inform the target selection and patient stratification strategies for multiple clinical programs, providing a concrete commercial example of how population-scale multi-omics data is being translated into drug discovery value.

By Omics Type: In 2026, Genomics to Hold the Largest Share

Based on omics type, the global multi-omics market is segmented into genomics, transcriptomics, proteomics, metabolomics, epigenomics, and other omics types. In 2026, the genomics segment is expected to account for the largest share of the global multi-omics market. Genomics is the foundational omics layer from which all other molecular characterizations follow, providing the reference genome against which transcriptomic and epigenomic variation is interpreted and the germline and somatic mutation profiles that define disease risk and tumor characteristics. The genomics market benefits from the most mature and cost-efficient sequencing technology ecosystem, the broadest range of established clinical applications—including germline disease risk profiling, companion diagnostic tumor profiling, and pharmacogenomics—and the largest installed base of next-generation sequencing (NGS) instruments globally. Illumina reported approximately USD 4.37 billion in revenue in 2024, with its sequencing instruments and consumables continuing to represent the dominant commercial platform for genomics research and clinical testing worldwide.

However, the spatial omics segment is projected to register the highest CAGR during the forecast period. Spatial omics is the newest commercial omics category, having only emerged as a commercial product category around 2019 with the launch of 10x Genomics' Visium platform, and it is growing from a smaller base than established omics types. The extraordinary scientific value of understanding gene expression and protein distribution in their tissue spatial context, combined with the rapidly improving resolution and multiplexing capabilities of spatial omics platforms from 10x Genomics, Vizgen, and Nanostring Technologies, is driving rapid research adoption and growing pharmaceutical and clinical interest in spatial multi-omics for tumor heterogeneity analysis, drug mechanism of action studies, and biomarker discovery.

By Product & Service: In 2026, Instruments to Hold the Largest Share

Based on product and service, the global multi-omics market is segmented into instruments (sequencers, mass spectrometers, and microarray systems), consumables and reagents (kits and assays, and reagents), software and bioinformatics platforms, and services (sequencing services, data analysis services, and multi-omics integration services). In 2026, the instruments segment is expected to account for the largest share of the global multi-omics market. Next-generation sequencers, mass spectrometers, and microarray systems are the foundational capital equipment purchases in multi-omics workflows, representing the largest single cost items in laboratory infrastructure investment. Illumina's sequencing systems, Thermo Fisher Scientific's Orbitrap mass spectrometers, and Bruker's TIMSTOF Pro mass spectrometry platforms collectively account for a large share of the global multi-omics instruments market, and the ongoing instrument upgrade cycle driven by the transition to newer higher-throughput platforms sustains strong instrument procurement volumes.

However, the software and bioinformatics platforms segment is projected to register the highest CAGR during the forecast period. As multi-omics data generation becomes increasingly routine and as data analysis capability becomes the bottleneck limiting scientific and clinical insights, the value of sophisticated bioinformatics platforms that can integrate, analyze, and interpret complex multi-omics datasets is growing rapidly. Cloud-based multi-omics analysis platforms, AI-powered data integration tools, and clinical interpretation software represent a growing and increasingly high-value product category with strong recurring subscription revenue characteristics. DNAnexus, Benchling, and several specialist bioinformatics companies are capturing growing revenues from cloud-based multi-omics data management and analysis.

By Technology: In 2026, NGS-based Technologies to Hold the Largest Share

Based on technology, the global multi-omics market is segmented into NGS-based technologies, mass spectrometry-based technologies, microarray-based technologies, single-cell technologies, and spatial omics technologies. In 2026, the NGS-based technologies segment is expected to account for the largest share of the global multi-omics market. Next-generation sequencing is the enabling technology for genomics, transcriptomics, epigenomics, and a growing fraction of single-cell multi-omics profiling, making it the most broadly deployed and highest-revenue technology in the multi-omics ecosystem. The very large installed base of NGS systems in research institutions, clinical laboratories, and pharmaceutical companies globally, combined with Illumina's dominant commercial position in short-read sequencing with revenues of approximately USD 4.37 billion in 2024, reflects the NGS segment's commanding market position.

However, the single-cell technologies segment is projected to register the highest CAGR during the forecast period. Single-cell omics has transformed from a specialized research technique to a standard approach in a very short time, driven by the commercial availability of user-friendly platforms from 10x Genomics that have democratized access to high-quality single-cell data across the research community. According to 10x Genomics' 2025 annual report, the company had shipped systems to over 2,800 customer sites globally, and single-cell transcriptomics is now a standard experimental approach in cancer biology, immunology, and developmental biology research. The rapid adoption of single-cell multi-omics methods that simultaneously profile genome, transcriptome, and epigenome from individual cells is expanding the already fast-growing single-cell segment into true simultaneous multi-omics territory.

By Application: In 2026, Drug Discovery & Development to Hold the Largest Share

Based on application, the global multi-omics market is segmented into drug discovery and development (target identification and biomarker discovery), clinical diagnostics and precision medicine, oncology research, agricultural and environmental research, and other applications. In 2026, the drug discovery and development segment is expected to account for the largest share of the global multi-omics market. Pharmaceutical companies are among the largest and most sophisticated consumers of multi-omics data and analysis services, applying genomics, transcriptomics, and proteomics data throughout the drug discovery pipeline from initial target identification and validation through clinical biomarker development and companion diagnostic qualification. According to the Pharmaceutical Research and Manufacturers of America, U.S. biopharmaceutical companies continue to invest nearly USD 100 billion annually in research and development, with multi-omics profiling increasingly embedded across drug discovery and clinical development programs as the industry shifts toward data-driven precision medicine approaches.

However, the clinical diagnostics and precision medicine segment is projected to register the highest CAGR during the forecast period. The progressive transition of comprehensive molecular profiling from research to clinical standard of care, exemplified by the growing clinical adoption of comprehensive genomic profiling assays and the emerging clinical use of proteomics and metabolomics biomarkers for disease stratification and monitoring, is driving the fastest-growing revenue opportunity in the multi-omics market. According to IQVIA's 2025 Oncology Trends report, comprehensive molecular profiling in oncology grew at above-average rates in 2024, with multi-analyte panels capturing a growing share of total molecular testing.

By End User: In 2026, Pharmaceutical & Biotechnology Companies to Hold the Largest Share

Based on end user, the global multi-omics market is segmented into pharmaceutical and biotechnology companies, academic and research institutes, CROs, and clinical laboratories. In 2026, the pharmaceutical and biotechnology companies segment is expected to account for the largest share of the global multi-omics market. The pharmaceutical industry's very large and growing multi-omics investment for drug target discovery, clinical biomarker development, and patient stratification makes it the highest-spending single end user category. Large pharma companies including AstraZeneca, Pfizer, Roche, and GSK have each invested in internal multi-omics capabilities and external partnerships that collectively represent very large annual expenditures on instruments, consumables, software, and services. According to PhRMA's 2025 data, U.S. biopharma R&D investment reached a record USD 100 billion in 2024, with a growing proportion directed toward precision medicine and multi-omics-driven drug discovery.

However, the clinical laboratories segment is projected to register the highest CAGR during the forecast period. The transition of multi-omics profiling into clinical diagnostic practice is creating new and fast-growing procurement activity in clinical reference laboratories, hospital-based molecular pathology departments, and commercial clinical genomics laboratories. As comprehensive genomic profiling becomes standard of care for more cancer types, as liquid biopsy multi-omics tests enter clinical practice, and as multi-omics biomarker panels are validated for non-oncology precision medicine applications, the clinical laboratory multi-omics market is expanding at above-average rates from its currently smaller commercial base compared with pharmaceutical industry spending.

Multi-Omics Market by Region: North America Leading by Share, Asia-Pacific by Growth

Based on geography, the global multi-omics market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, North America is expected to account for the largest share of the global multi-omics market. The United States is the world's most advanced multi-omics research and commercial market, home to the leading multi-omics instrument companies including Illumina, Thermo Fisher Scientific, 10x Genomics, Pacific Biosciences, and Waters Corporation, and to the largest concentration of pharmaceutical R&D investment and academic multi-omics research globally. According to National Institutes of Health budget data, the NIH allocated approximately USD 48–49 billion in medical research funding for fiscal year 2025. A substantial portion of this funding supports genomics, transcriptomics, proteomics, and other omics-related research programs, driving continued demand for sequencing instruments, reagents, bioinformatics software, and advanced analytical platforms across academic and clinical research institutions. The All of Us Research Program, targeting one million U.S. participant multi-omics profiles per its NIH 2025 progress report, represents a multi-year government-funded driver of multi-omics instrument and service demand. The Broad Institute of MIT and Harvard, the Jackson Laboratory, and the Chan Zuckerberg Biohub are among the U.S. research institutions with the largest multi-omics research programs, collectively representing very large annual multi-omics infrastructure procurement. Illumina's revenues of approximately USD 4.37 billion in 2024, 10x Genomics' approximately USD 611 million in revenues in 2024, and SomaLogic's commercial proteomics services growth all reflect the commercial scale of North America's multi-omics ecosystem.

However, the Asia-Pacific multi-omics market is expected to grow at the fastest CAGR during the forecast period. China is making the most significant national investment in multi-omics research infrastructure of any country outside the United States. BGI Genomics, headquartered in Shenzhen, is one of the world's largest genomics sequencing service providers and has built the China National GeneBank, a national genomics data infrastructure that is among the world's largest. According to BGI's 2025 annual communications, the company processes millions of samples annually across genomic, transcriptomic, and other omics services, making it the world's largest omics service provider by volume. China's national precision medicine initiatives, funded through the National Key Research and Development Program, are directing very large research investments into multi-omics profiling of large Chinese patient cohorts for disease mechanism research and drug target identification. Japan's strong pharmaceutical industry and advanced medical device manufacturing ecosystem make it a significant multi-omics instruments and reagents market, and South Korea's growing biotechnology industry and government investment in precision medicine research programs are driving above-average multi-omics procurement growth. Singapore's Genome Institute of Singapore and its national precision medicine program are establishing Singapore as a regional multi-omics research hub.

The multi-omics market is served by large diversified life science tool companies with broad multi-omics instrument and reagent portfolios, specialist companies focused on specific omics layers or enabling technologies, bioinformatics and software companies providing data analysis platforms, and genomics service providers offering contract sequencing and multi-omics profiling. Competition is based on instrument performance and throughput, reagent quality and workflow integration, software analytical capability and clinical interpretation quality, service turnaround time and data quality, and the breadth and integration of the multi-omics product portfolio.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' product portfolios, omics coverage, customer base, geographic presence, and recent strategic developments. Some of the key players operating in the global multi-omics market include Illumina Inc. (U.S.), Thermo Fisher Scientific Inc. (U.S.), Agilent Technologies Inc. (U.S.), Bruker Corporation (U.S.), QIAGEN N.V. (Netherlands), Danaher Corporation (U.S.), PerkinElmer Inc. (U.S.), Bio-Rad Laboratories Inc. (U.S.), Waters Corporation (U.S.), Pacific Biosciences of California Inc. (U.S.), Oxford Nanopore Technologies plc (UK), BGI Genomics Co. Ltd. (China), 10x Genomics Inc. (U.S.), Standard BioTools Inc. (U.S.), and SomaLogic Inc. (U.S.), among others.

The global multi-omics market is expected to reach USD 28.6 billion by 2036 from an estimated USD 10.4 billion in 2026, at a CAGR of 10.6% during the forecast period 2026-2036.

In 2026, the genomics segment is expected to hold the largest share of the global multi-omics market.

The spatial omics segment is projected to register the highest CAGR during the forecast period,

The single-cell technologies segment is projected to register the highest CAGR during the forecast period.

The market is primarily driven by the NHGRI's 2025 data showing genome sequencing costs below USD 200, enabling economically feasible multi-omics profiling, combined with PhRMA's 2025 report documenting USD 100 billion in U.S. biopharma R&D investment in 2024 driving pharmaceutical multi-omics adoption, and the All of Us Research Program targeting one million participant multi-omics profiles per its NIH 2025 progress report.

Key players are Illumina Inc. (U.S.), Thermo Fisher Scientific Inc. (U.S.), Agilent Technologies Inc. (U.S.), Bruker Corporation (U.S.), QIAGEN N.V. (Netherlands), Danaher Corporation (U.S.), PerkinElmer Inc. (U.S.), Bio-Rad Laboratories Inc. (U.S.), Waters Corporation (U.S.), Pacific Biosciences of California Inc. (U.S.), Oxford Nanopore Technologies plc (UK), BGI Genomics Co. Ltd. (China), 10x Genomics Inc. (U.S.), Standard BioTools Inc. (U.S.), and SomaLogic Inc. (U.S.), among others.

Asia-Pacific is expected to register the highest growth rate in the global multi-omics market during the forecast period 2026-2036, driven by BGI Genomics processing millions of samples annually as the world's largest omics service provider by volume, China's National Key Research and Development Program investments in multi-omics patient cohort profiling, and Singapore and South Korea's growing precision medicine research programs.

1. Introduction

1.1. Market Definition

1.2. Scope

1.3. Market Ecosystem

1.4. Currency and Limitations

1.4.1. Currency

1.4.2. Limitations

1.5. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research (Researchers, Pharma, CROs, Diagnostics Firms)

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Forecast Modeling

2.4. Data Triangulation

2.5. Assumptions

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Growing Demand for Precision Medicine

4.2.1.2. Advancements in High-throughput Sequencing Technologies

4.2.1.3. Increasing Investment in Omics Research

4.2.1.4. Rising Adoption of AI & Bioinformatics

4.2.2. Restraints

4.2.2.1. High Cost of Multi-Omics Integration

4.2.2.2. Data Complexity and Interpretation Challenges

4.2.2.3. Lack of Skilled Professionals

4.2.3. Opportunities

4.2.3.1. Integration with Clinical Diagnostics

4.2.3.2. Growth in Drug Discovery and Biomarker Identification

4.2.3.3. Expansion in Emerging Markets

4.2.3.4. Development of Multi-Omics Platforms

4.2.4. Challenges

4.2.4.1. Standardization of Multi-Omics Data

4.2.4.2. Data Storage and Management

4.3. Technology Landscape

4.3.1. Next-Generation Sequencing (NGS)

4.3.2. Mass Spectrometry (MS)

4.3.3. Microarray Technologies

4.3.4. Single-cell Omics Technologies

4.3.5. Spatial Omics

4.3.6. Bioinformatics & AI Platforms

4.4. Multi-Omics Ecosystem

4.4.1. Sequencing & Instrument Providers

4.4.2. Bioinformatics & Software Providers

4.4.3. Pharmaceutical & Biotechnology Companies

4.4.4. CROs & Research Organizations

4.4.5. Academic & Research Institutions

4.5. Value Chain Analysis

4.5.1. Sample Collection & Preparation

4.5.2. Data Generation (Sequencing/Profiling)

4.5.3. Data Integration

4.5.4. Data Analysis & Interpretation

4.5.5. Clinical & Research Applications

4.6. Regulatory Landscape

4.6.1. Genomics & Diagnostics Regulations

4.6.2. Data Privacy & Compliance (HIPAA, GDPR)

4.6.3. Clinical Validation Guidelines

4.7. Industry Trends

4.7.1. Rise of Single-cell and Spatial Omics

4.7.2. Integration of AI in Omics Data Analysis

4.7.3. Growth of Multi-Omics Platforms

4.7.4. Increasing Collaborations in Research

4.8. Cost and Pricing Analysis

4.8.1. Cost Breakdown by Omics Type

4.8.2. Pricing Trends for Multi-Omics Services

4.8.3. Infrastructure and Data Costs

5. Multi-Omics Market, by Omics Type

5.1. Introduction

5.2. Genomics

5.3. Transcriptomics

5.4. Proteomics

5.5. Metabolomics

5.6. Epigenomics

5.7. Other Omics Types

6. Multi-Omics Market, by Product & Service

6.1. Introduction

6.2. Instruments

6.2.1. Sequencers

6.2.2. Mass Spectrometers

6.2.3. Microarray Systems

6.3. Consumables & Reagents

6.3.1. Kits & Assays

6.3.2. Reagents

6.4. Software & Bioinformatics Platforms

6.5. Services

6.5.1. Sequencing Services

6.5.2. Data Analysis Services

6.5.3. Multi-Omics Integration Services

7. Multi-Omics Market, by Technology

7.1. NGS-based Technologies

7.2. Mass Spectrometry-based Technologies

7.3. Microarray-based Technologies

7.4. Single-cell Technologies

7.5. Spatial Omics Technologies

8. Multi-Omics Market, by Application

8.1. Introduction

8.2. Drug Discovery & Development

8.2.1. Target Identification

8.2.2. Biomarker Discovery

8.3. Clinical Diagnostics & Precision Medicine

8.4. Oncology Research

8.5. Agricultural & Environmental Research

8.6. Other Applications

9. Multi-Omics Market, by End User

9.1. Pharmaceutical & Biotechnology Companies

9.2. Academic & Research Institutes

9.3. CROs

9.4. Clinical Laboratories

10. Multi-Omics Market, by Geography

10.1. Introduction

10.2. North America

10.2.1. U.S.

10.2.2. Canada

10.3. Europe

10.3.1. Germany

10.3.2. U.K.

10.3.3. France

10.3.4. Italy

10.3.5. Spain

10.3.6. Netherlands

10.3.7. Sweden

10.3.8. Switzerland

10.3.9. Rest of Europe

10.4. Asia-Pacific

10.4.1. China

10.4.2. Japan

10.4.3. India

10.4.4. South Korea

10.4.5. Australia

10.4.6. Singapore

10.4.7. Rest of Asia-Pacific

10.5. Latin America

10.5.1. Brazil

10.5.2. Mexico

10.5.3. Rest of Latin America

10.6. Middle East & Africa

10.6.1. UAE

10.6.2. Saudi Arabia

10.6.3. South Africa

10.6.4. Rest of MEA

11. Competitive Landscape

11.1. Overview

11.2. Key Growth Strategies

11.3. Competitive Benchmarking

11.4. Competitive Dashboard

11.4.1. Industry Leaders

11.4.2. Market Differentiators

11.4.3. Emerging Players

11.5. Market Ranking/Positioning Analysis

12. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

12.1. Illumina, Inc.

12.2. Thermo Fisher Scientific Inc.

12.3. Agilent Technologies, Inc.

12.4. Bruker Corporation

12.5. QIAGEN N.V.

12.6. Danaher Corporation

12.7. PerkinElmer, Inc.

12.8. Bio-Rad Laboratories, Inc.

12.9. Waters Corporation

12.10. Pacific Biosciences of California, Inc.

12.11. Oxford Nanopore Technologies plc

12.12. BGI Genomics Co., Ltd.

12.13. 10x Genomics, Inc.

12.14. Standard BioTools Inc.

12.15. SomaLogic, Inc.

13. Appendix

13.1. Customization Options

13.2. Related Reports

Published Date: Sep-2024

Published Date: Jan-2025

Published Date: Jun-2026

Subscribe to get the latest industry updates