Resources

About Us

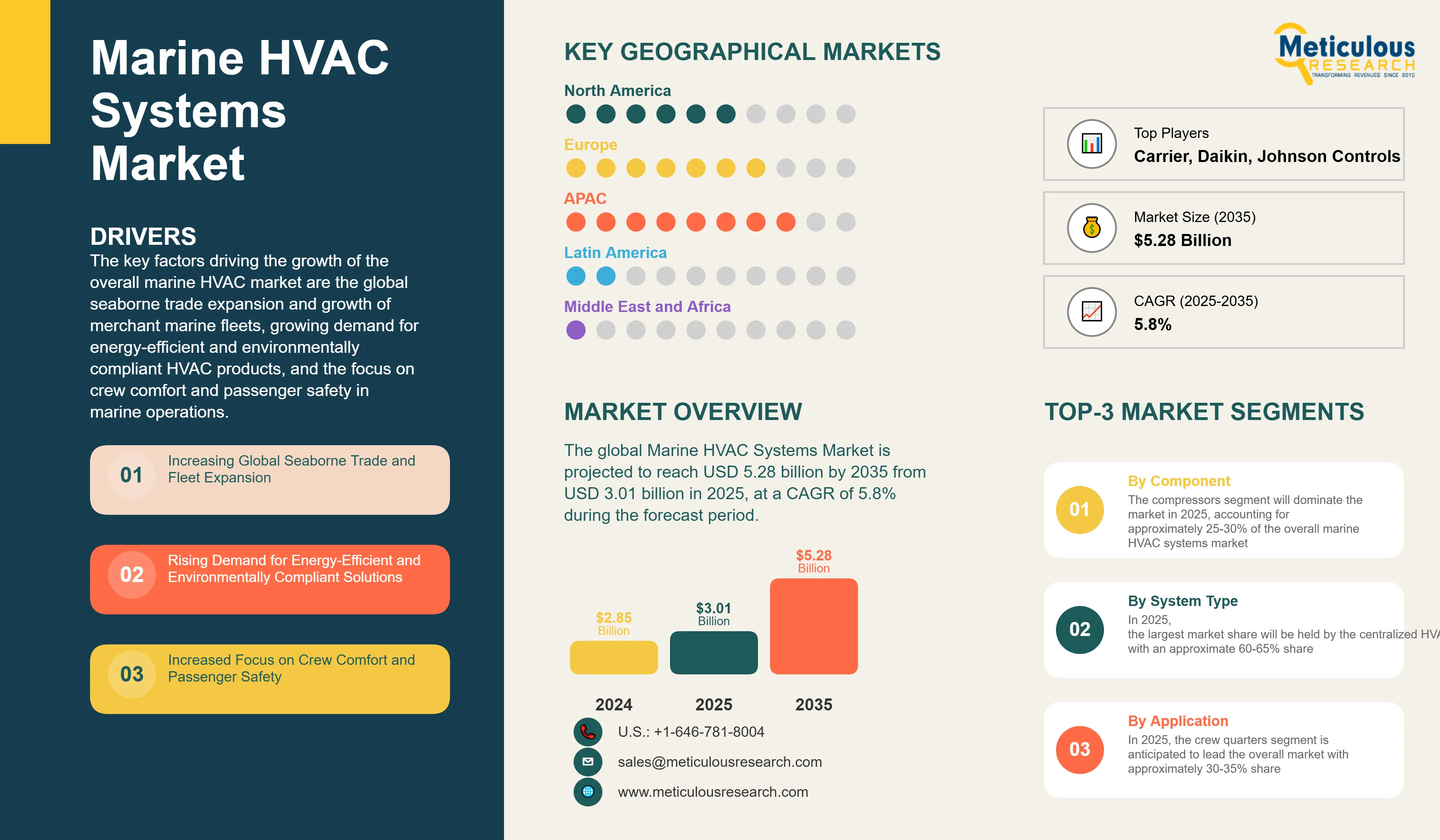

Marine HVAC Systems Market Size, Share & Forecast (2025–2035): Global Trends, Energy Efficiency, Vessel Modernization & Regional Outlook

Report ID: MREP - 1041536 Pages: 285 Jul-2025 Formats*: PDF Category: Energy and Power Delivery: 24 to 72 Hours Download Free Sample ReportThe key factors driving the growth of the overall marine HVAC market are the global seaborne trade expansion and growth of merchant marine fleets, growing demand for energy-efficient and environmentally compliant HVAC products, and the focus on crew comfort and passenger safety in marine operations. Additionally, enforcement of tight international maritime policies for emissions control and energy efficiency have spurred the market's growth. Further, the modernization of aging fleets of vessels and growth in offshore renewable energy projects are fueling demand for advanced marine HVAC technologies.

However, high upfront installation costs and demanding integration requirements could discourage some shipowners, especially for retrofit purposes. Also, the cyclic nature of the shipping business and volatility of freight rates introduce uncertainty into capital expenditure projects. Technical difficulty in designing HVAC systems to withstand extreme marine environments, such as salt corrosion and space limitations, presents engineering challenges, while keeping up with changing international maritime regulations entails ongoing technology refreshes.

In spite of these challenges, the market holds significant untapped potential. The surge in cruise travel and luxury yacht markets offers high-end opportunities for sophisticated climate control technologies. Offshore wind farms and floating production platforms expansion bring with them demand for custom HVAC systems adapted to the harsh marine environments. There is also increased demand for incorporating renewable energy resources and heat recovery systems to enhance overall vessel energy efficiency.

The new trends in smart ship technology and predictive maintenance through IoT are transforming the market scenario. There is increasing demand for light and compact HVAC designs to maximize vessel space efficiency, as well as technological developments in variable refrigerant flow (VRF) systems and magnetic bearings. Air purification and filtration systems are incorporated as a norm, while hybrid and electric propulsion ships are opening up opportunities for integrated energy management systems.

Following the trend of the wider industry, the emphasis on decarbonization and alternative fuels is driving demand for HVAC systems tailored to LNG, hydrogen, and ammonia-fueled ships. Suppliers are creating corrosion-resistant materials and using environmentally friendly manufacturing processes to address changing environmental requirements.

Increasing Global Seaborne Trade and Fleet Expansion

Global seaborne trade is projected to grow at around 2.4%–3.4% per annum through 2030, based on forecasts from maritime trade analysts like UNCTAD and Clarkson Research. This growth is expected to support demand for new shipbuilding and fleet renewal, particularly expanding container shipping, bulk carrier, and specialized vessel fleets. Currently, the world’s merchant fleet comprises more than 98,000 ships, with approximately 2,500 to 3,000 new vessels delivered annually, fueling steady demand for marine HVAC systems across vessel types.

Advanced climate control systems are needed for modern ships to preserve cargo integrity, keep the crew safe, and meet international comfort levels. Increased container ship and bulk carrier size demands higher-powered and more efficient HVAC systems with greater capability to cool larger enclosed spaces while conserving energy.

The move towards larger, more fuel-efficient ships has added complexity to HVAC requirements, with systems having to deal with multiple climate zones, changing load conditions, and built-in air quality management. Such sophisticated systems usually cost 8-12% of overall shipbuilding expenditure but are essential for operational effectiveness and regulatory compliance.

Emerging trends in autonomous and semi-autonomous shipping also are driving demand for HVAC systems with more remote monitoring features and lower maintenance needs as human intervention becomes increasingly less feasible over longer journeys.

Rising Demand for Energy-Efficient and Environmentally Compliant Solutions

The IMO Energy Efficiency Design Index (EEDI) regulations and the future Carbon Intensity Indicator (CII) requirements are compelling shipowners to spend on energy-efficient HVAC technologies. In line with DNV GL's Maritime Forecast to 2050, ships constructed after 2025 need to be 30% more energy efficient than the 2008 baselines.

Heat recovery ventilation systems and variable frequency drive (VFD) technology are able to decrease HVAC energy usage by 25-40% when compared with traditional systems. The use of magnetic bearing chillers and heat pump technologies is being used as standard in new vessel designs to achieve efficiency targets and minimize maintenance needs.

Installation of the IMO sulfur cap regime has raised the focus on alternative fuels, and there is a demand for HVAC systems designed for LNG, methanol, and hydrogen-fueled ships. Alternative fuel systems have specialized ventilation and gas detection features, which are enhancing innovation in the design of marine HVAC.

Energy management systems that link HVAC controls to overall vessel power management are becoming necessary for meeting new efficiency regulations and optimizing operational expenses in a volatile fuel price environment.

Increased Focus on Crew Comfort and Passenger Safety

The Maritime Labour Convention (MLC) 2006 and related amendments set strict standards for crew accommodations such as temperature, air quality, and noise levels. These standards must be complied with for certification of the vessel and access to ports, and therefore competent HVAC systems are a regulatory requirement rather than a choice.

The post-COVID-19 recovery and growth of the cruise industry have increased interest in air quality control and ventilation systems with the ability to create healthy indoor spaces. HVAC systems in contemporary cruise ships need to support up to 6,000 passengers while still enjoying personal cabin climate control and optimizing energy usage.

Improved air filtration and purification technologies have become minimum requirements based on health and safety issues experienced during the pandemic. HEPA filtration and UV-C sterilization technology are becoming more integrated in marine HVAC designs to maintain air quality standards.

The expanding luxury yacht market, worth more than USD 8 billion each year, requires high-end HVAC solutions offering individual zone control, whispering silence operation, and integration with advanced vessel management systems.

Base CAGR: 5.8%

|

Category |

Key Factor |

Short-Term Impact (2025–2028) |

Long-Term Impact (2029–2035) |

Estimated CAGR Impact |

|

Drivers |

||||

|

1. |

Increasing Global Seaborne Trade & Fleet Expansion |

Strong demand from new vessel construction |

Sustained growth as global trade expands |

▲ +0.5% |

|

2. |

Rising Demand for Energy-Efficient Solutions |

Gradual adoption driven by EEDI/CII regulations |

Accelerated by stricter efficiency mandates |

▲ +0.6% |

|

3. |

Growing Cruise Tourism & Passenger Vessel Market |

Recovery-driven retrofits and upgrades |

Expansion of global cruise capacity |

▲ +0.4% |

|

Restraints |

||||

|

1. |

High Initial Installation & Integration Costs |

Delays in retrofit projects; budget constraints |

Long-term barrier in cost-sensitive segments |

▼ −0.4% |

|

2. |

Cyclical Nature of Shipping Industry |

Volatile newbuild orders affect market demand |

Economic cycles impact long-term growth |

▼ −0.2% |

|

Opportunities |

||||

|

1. |

Offshore Wind & Renewable Energy Platforms |

Growing offshore infrastructure investments |

Major growth driver for specialized marine HVAC |

▲ +0.7% |

|

2. |

Smart Ship Technologies & IoT Integration |

Early adoption in premium vessel segments |

Standard across all vessel types by 2030+ |

▲ +0.7% |

|

Trends |

||||

|

1. |

Modular & Compact System Designs |

Space optimization becomes priority |

Standard design approach for new vessels |

▲ +0.4% |

|

2. |

Heat Recovery & Waste Heat Utilization |

Growing interest in energy optimization |

Essential for regulatory compliance |

▲ +0.4% |

|

Challenges |

||||

|

1. |

Compliance with Evolving IMO Regulations |

Increased development costs and complexity |

Ongoing challenge requiring continuous innovation |

▼ −0.2% |

|

2. |

Skilled Technician Shortage |

Installation and maintenance challenges |

Training programs and automation reduce impact |

~ Neutral |

By Component

By component, the marine HVAC systems market is segmented into compressors, condensers, evaporators, expansion valves, controls and sensors, ductwork and ventilation components, and others. The compressors segment will dominate the market in 2025, accounting for approximately 25-30% of the overall marine HVAC systems market. Compressors are dominant because they play a pivotal role in system performance, have a higher frequency of replacements, and technologically drive toward variable speed and magnetic bearing designs.

Conversely, the controls and sensors segment is likely to expand at the highest CAGR in the forecast period 2025-2035. The increasing use of smart ship technologies, expanding adoption of IoT-based monitoring systems, requirement for predictive maintenance functionality, and growing focus on energy optimization with advanced control techniques are key drivers for the expansion of this segment.

By System Type

On the basis of system type, the market for marine HVAC systems is categorized into centralized HVAC systems, decentralized HVAC systems, and hybrid HVAC systems. In 2025, the largest market share will be held by the centralized HVAC systems segment, with an approximate 60-65% share. This is primarily because of their cost savings on large vessels, proven design practices, and optimal utilization of space for high-capacity applications.

Nevertheless, the hybrid HVAC systems segment is expected to develop with the highest CAGR over the forecast period. This is owing to their capability to maximize energy efficiency by utilizing zone-based control, increased redundancy and system reliability, adaptability to accommodate dynamic load conditions, and minimized environmental effect via integrated heat recovery systems.

By Vessel Type

Based on vessel type, the marine HVAC systems market is classified into commercial vessels (container ships, bulk carriers, tankers, general cargo), passenger vessels (cruise ships, ferries, luxury yachts), offshore vessels (supply vessels, drilling rigs, production platforms), naval vessels, and others. In 2025, the commercial vessels segment will account for the largest share of approximately 45-50%, given the vast global merchant fleet size and ongoing newbuild activity.

However, the offshore vessels segment is anticipated to witness the highest CAGR over the forecast period due to increasing offshore wind power projects, increased demand for floating production storage and offloading (FPSO) units, heightened deep-water exploration activities, and specialized HVAC requirements for severe offshore environments.

By Application

On the basis of application, the marine HVAC systems market has been divided into crew quarters, passenger spaces, cargo compartments, engine spaces, bridge and control spaces, and galley/food service spaces. In 2025, the crew quarters segment is anticipated to lead the overall market with approximately 30-35% share owing to obligatory adherence to Maritime Labour Convention regulations and high frequencies of crew accommodation spaces in every vessel type.

Conversely, the passenger areas segment is anticipated to achieve the maximum CAGR between the forecast period of 2025-2035. This is largely driven by cruise tourism recovery and growth, a greater focus on passenger comfort and experience, an expanding luxury yacht market, and higher air quality standards post-health and safety issues.

Regional Analysis

By geography, the market for marine HVAC systems is divided into North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. In 2025, the Asia-Pacific region will account for the highest share of approximately 40-45% of the worldwide marine HVAC systems market. The region's leadership in shipbuilding, widespread merchant fleet activity, increasing offshore energy projects, and growing cruise tourism in Southeast Asia are among the main market growth drivers.

This region is also anticipated to increase at the highest CAGR of the forecasting period from 2025-2035. The reason behind this growth is the increase in shipbuilding capacity in China and South Korea, investments in offshore wind power projects, regional trade and shipping activity, government support for green shipping technologies, and the increasing demand for LNG carriers and niche ships.

Europe is also exhibiting high demand for environmentally sustainable and energy-efficient marine HVAC systems. Environmental regulations, offshore wind energy leadership, and the location of influential cruise operators are fueling uptake of advanced HVAC technology and sustainable design approaches.

Key Players in the Global Marine HVAC Market

Major companies leading the global marine HVAC market include Carrier Corporation, Daikin Industries, Johnson Controls International plc, Heinen & Hopman Engineering B.V., Bronswerk Marine Inc., Drews Marine GmbH, Mitsubishi Electric Corporation, Dometic Group AB (including Marine Air Systems), Novenco Marine & Offshore A/S, GEA Group, Horn International AS, Teknotherm Marine AS, Brownswerk Marine Inc., AF Group ASA, Webasto SE, Thermo King Corporation, Climma Marine Air Conditioning, Veco S.p.A., Frigomar Srl, Aqua-Air Manufacturing, Nauticool Ltd., HFL Marine Air Conditioning, Marinaire LLC, Condaria Srl, and YORK Marine Systems. These companies together contribute significantly to innovation, energy-efficient solutions, and comprehensive product offerings that serve a wide range of vessel types and marine HVAC needs worldwide.

|

Particulars |

Details |

|

Number of Pages |

285 |

|

Forecast Period |

2025–2035 |

|

Base Year |

2024 |

|

CAGR (Value) |

5.8% |

|

Market Size 2024 |

USD 2.85 billion |

|

Market Size 2025 |

USD 3.01 billion |

|

Market Size 2035 |

USD 5.28 billion |

|

Segments Covered |

By Component, System Type, Vessel Type, Application, and Technology |

|

Countries Covered |

North America (U.S., Canada, Mexico), Europe (Germany, France, U.K., Italy, Spain, Netherlands, Norway, Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Singapore, Australia, Rest of Asia-Pacific), Latin America (Brazil, Argentina, Rest of Latin America), and the Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa) |

The global marine HVAC systems market is projected to reach USD 5.28 billion by 2035 from USD 3.01 billion in 2025, at a CAGR of 5.8% during the forecast period. The market was valued at USD 2.85 billion in 2024.

In 2025, the compressors segment is projected to hold the major share of the marine HVAC systems market, while the controls and sensors segment is slated to record the highest growth rate.

Key factors driving the growth include increasing global seaborne trade and fleet expansion, rising demand for energy-efficient and environmentally compliant solutions, growing emphasis on crew comfort and passenger safety, expansion of offshore renewable energy projects, and implementation of stringent IMO regulations for emissions control.

Asia-Pacific leads the market with the highest share and is projected to record the highest growth rate during the forecast period, offering significant opportunities for marine HVAC systems vendors.

Major opportunities include expansion of offshore wind energy platforms, development of smart ship technologies and IoT integration, growth in alternative fuel vessels requiring specialized HVAC solutions, modular and compact system designs for space optimization, and enhanced air quality systems for passenger vessels.

Key trends include adoption of heat recovery and waste heat utilization systems, integration of advanced air filtration and purification technologies, development of magnetic bearing and variable speed compressor technologies, implementation of predictive maintenance through IoT sensors, and focus on lightweight and corrosion-resistant materials.

The hybrid HVAC systems segment is anticipated to record the highest growth rate during the forecast period, driven by energy optimization capabilities, improved system redundancy, flexible load handling, and integrated heat recovery features.

Published Date: Sep-2025

Published Date: Aug-2025

Published Date: Jul-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates