Resources

About Us

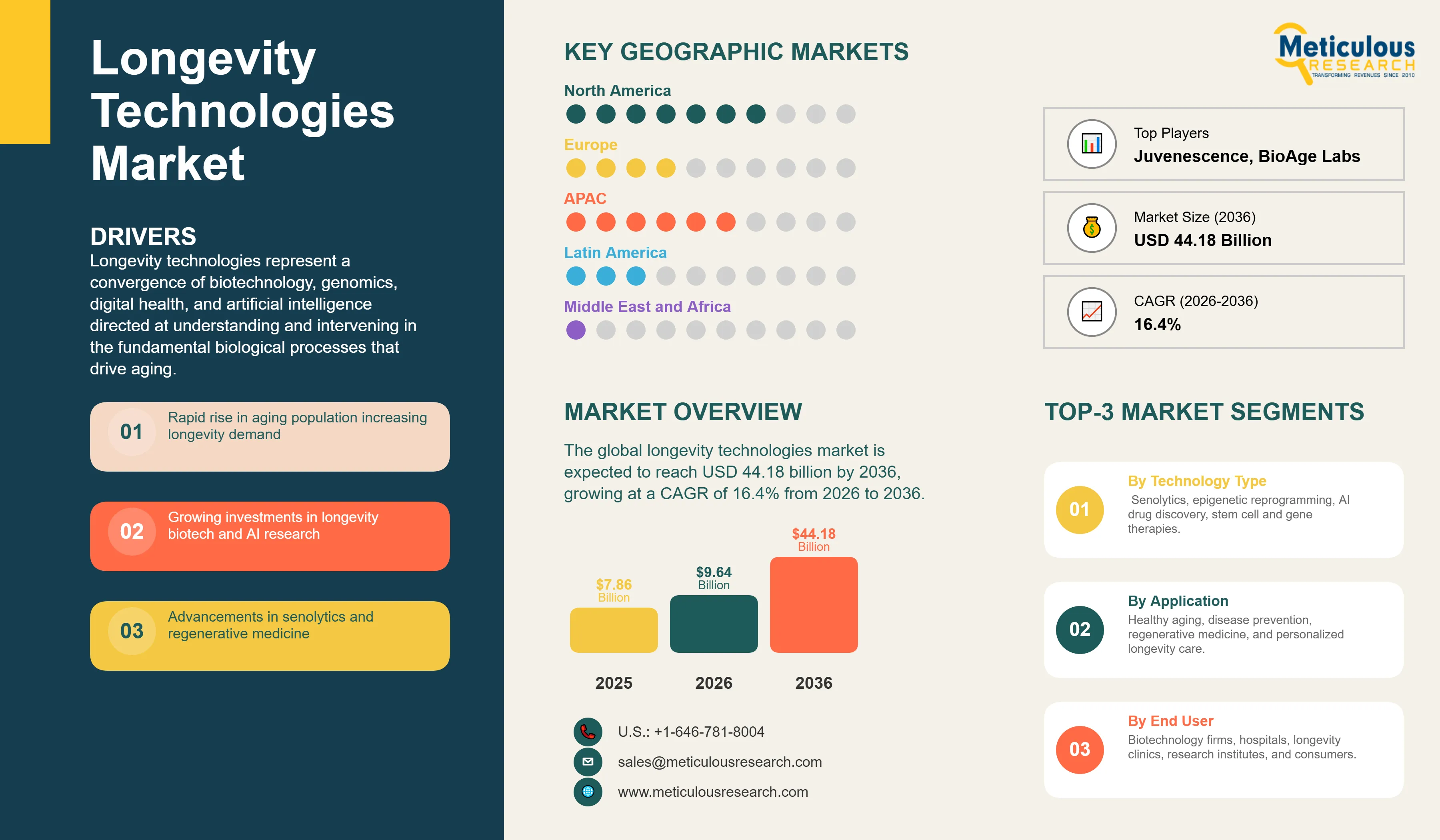

The global longevity technologies market was valued at USD 7.86 billion in 2025. This market is expected to reach USD 44.18 billion by 2036 from USD 9.64 billion in 2026, growing at a CAGR of 16.4% from 2026 to 2036.

The growth of this market is driven by one of the most significant demographic transitions in human history. According to the United Nations World Population Prospects 2024, global life expectancy at birth reached 73.3 years in 2024, an increase of 8.4 years since 1995, and is projected to rise further to approximately 77.4 years by 2054. The number of people aged 60 and older worldwide is projected to increase from 1.1 billion in 2023 to 1.4 billion by 2030, according to the WHO. By the late 2070s, the global population aged 65 and older is projected to reach 2.2 billion, surpassing the number of children under age 18, according to the United Nations. This demographic shift is placing enormous pressure on healthcare systems globally and simultaneously creating a large and growing market for technologies that extend healthy lifespan, prevent age-related disease, and improve the quality of life in later years.

Longevity technologies are a broad and rapidly evolving category of scientific and commercial interventions targeting the biological mechanisms of aging. The market encompasses senolytic therapies that selectively eliminate senescent cells which accumulate with age and drive chronic inflammation; epigenetic reprogramming technologies that seek to reset the epigenetic marks on aging cells toward a more youthful state; stem cell and regenerative medicine approaches that replace or restore damaged tissues; gene editing technologies including CRISPR-Cas9 that target longevity-associated genetic pathways; AI-driven drug discovery platforms that accelerate the identification of longevity compounds; longevity diagnostics and biological age testing that enable personalized intervention; digital longevity platforms that integrate biomarker monitoring with lifestyle optimization; and consumer-facing longevity clinics and wellness programs that deliver evidence-based longevity protocols to paying individuals. The convergence of these technology streams, accelerating with increasing private investment and growing scientific validation, defines the commercial longevity technologies market.

Longevity technologies represent a convergence of biotechnology, genomics, digital health, and artificial intelligence directed at understanding and intervening in the fundamental biological processes that drive aging. The scientific foundation of the market rests on the growing body of evidence establishing that aging is not simply an inevitable deterioration but a regulated biological process subject to modulation through genetic, pharmacological, and environmental interventions. Key aging hallmarks identified by landmark research published in Cell (Lopez-Otin et al., 2013 and updated 2023) include genomic instability, telomere attrition, epigenetic alterations, loss of proteostasis, deregulated nutrient sensing, mitochondrial dysfunction, cellular senescence, stem cell exhaustion, altered intercellular communication, disabled macroautophagy, chronic inflammation, and dysbiosis. Each of these hallmarks represents a potential therapeutic target for longevity technologies, and the field is advancing across all of them simultaneously.

Senolytic therapies are the most commercially mature longevity technology category. Senolytics are compounds that selectively induce apoptosis in senescent cells, the dysfunctional cells that accumulate in tissues with age and secrete a pro-inflammatory cocktail known as the senescence-associated secretory phenotype. According to the NIH National Institute on Aging's FY 2025 Budget submission, NIA is currently funding clinical trials to test senolytic compounds for the prevention or alleviation of frailty, sepsis, COVID-19, Alzheimer's disease, diabetic kidney disease, and idiopathic pulmonary fibrosis. The leading senolytic drug combination in clinical investigation is dasatinib plus quercetin, a combination developed through Mayo Clinic research with NIA funding. An NIA-funded Phase 2 randomized controlled trial published in Nature Medicine (Farr et al., September 2024) evaluated senolytic therapy effects on bone health in postmenopausal women, confirming that NIA-funded senolytic clinical research has progressed from animal models to Phase 2 human trials across multiple disease areas.

The competitive landscape of the longevity technologies market is defined by a combination of well-funded biotechnology startups, large pharmaceutical companies beginning to engage with longevity science, consumer longevity clinic operators, and digital health platforms. Altos Labs, founded in 2022 with approximately USD 3 billion in initial funding from investors including Jeff Bezos and Yuri Milner, is pursuing cellular reprogramming as the primary scientific approach for reversing aging hallmarks. Calico Life Sciences, an Alphabet-funded research company, is using computational and molecular biology tools to understand aging and develop interventions. Unity Biotechnology is developing senolytic medicines for age-related diseases. Human Longevity Inc. operates precision longevity health programs using whole-genome sequencing and comprehensive phenotyping. Novo Nordisk's investment in longevity, particularly through its position in the GLP-1 receptor agonist class which has shown metabolic aging-related benefits, reflects the growing interest of established pharmaceutical companies in the longevity therapeutics space.

NIH-funded Senolytic Clinical Trials Advancing the Field Toward Regulated Therapeutic Applications

The progression of senolytic therapies from preclinical research to active human clinical trials funded by the U.S. National Institute on Aging represents the most significant near-term trend converting longevity science into validated therapeutic products. Senolytics have demonstrated consistent lifespan and healthspan extension in naturally aging mice across multiple independent research programs, establishing strong preclinical proof of concept. The translation of these findings into human clinical programs is now well underway. According to the NIA FY 2025 Budget Justification submitted to the U.S. Congress, NIA is currently funding clinical trials of senolytic compounds targeting frailty, diabetic kidney disease, idiopathic pulmonary fibrosis, and Alzheimer's disease. According to the NIA FY 2026 Budget document, as of September 2024 NIA was funding nearly 500 active clinical trials on dementia prevention, treatment, care, and caregiving, more than 220 of which were testing drug or biologic interventions, with senolytics included among the mechanistic targets being evaluated across multiple trials.

The Cellular Senescence Network, known as SenNet, was approved by the NIH Council of Councils as a Common Fund project and launched in early 2021 with the objective of comprehensively mapping senescent cell populations across human tissues. This federally funded research infrastructure program is generating foundational biological data that supports the development of targeted senolytic interventions and provides academic research groups and commercial companies with validated biological reference data for senescent cell identification and characterization. The progression of NIA-funded senolytic trials through Phase 1 and into Phase 2 randomized controlled trials, as documented by the NIA-funded study published in Nature Medicine in September 2024, marks the field's entry into the rigorous clinical evidence generation phase that will ultimately enable regulatory approval and payer coverage decisions for senolytic therapeutics.

Epigenetic Reprogramming Attracting the Largest Private Investment in Longevity Biotechnology

Epigenetic reprogramming, a technology approach based on using the Yamanaka transcription factors or related molecular tools to reset the epigenetic age of cells toward a more youthful state, has attracted the largest concentration of private investment capital in the longevity biotechnology sector. The scientific basis of this approach is the Nobel Prize-winning discovery by Shinya Yamanaka that mature somatic cells can be reprogrammed to a pluripotent stem cell state by expressing four transcription factors, Oct4, Sox2, Klf4, and c-Myc. Subsequent research has shown that partial or transient expression of these factors, without complete dedifferentiation, can reverse epigenetic aging marks in cells while preserving cellular identity. Altos Labs was founded in 2022 with approximately USD 3 billion in backing specifically to pursue this partial reprogramming approach, employing leading aging researchers including Shinya Yamanaka as a scientific advisor to drive its research programs. Retro Biosciences raised USD 180 million in 2022 with a stated goal of adding ten years to human healthspan. These investment levels reflect investor conviction that epigenetic reprogramming, if validated in humans, would represent the highest-value longevity technology platform, potentially addressing multiple aging hallmarks simultaneously through a single intervention approach.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 44.18 Billion |

|

Market Size in 2026 |

USD 9.64 Billion |

|

Market Size in 2025 |

USD 7.86 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 16.4% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Technology Type, Product and Service, Delivery Model, Application, End User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Driver: Rapid Growth of the Global Aging Population and Associated Healthcare Burden

The most fundamental driver of the longevity technologies market is the accelerating growth of the global aging population and the associated healthcare and economic burden that is motivating both public and private investment in technologies that extend healthy lifespan. According to the United Nations World Population Prospects 2024, global life expectancy at birth reached 73.3 years in 2024, an increase of 8.4 years since 1995, and is projected to rise to approximately 77.4 years globally by 2054. The number of people aged 60 and older worldwide is projected to grow from 1.1 billion in 2023 to 1.4 billion by 2030, according to the WHO. According to the United Nations, by the late 2070s the global population aged 65 and older will reach approximately 2.2 billion, surpassing the number of children under age 18. In Europe, according to the WHO European Region, by 2024 the population of individuals aged over 65 already outnumbered those under age 15 for the first time in the region's demographic history. According to the United Nations Population Division, 1 in 6 people globally will be over age 65 by 2050, up from 1 in 11 in 2019, and the number of people aged 80 or over will triple in the next 30 years. This demographic reality creates both the need and the commercial market for longevity technologies that preserve function, prevent age-related disease, and extend the period of healthy, independent living for an increasingly large proportion of the global population.

Opportunity: Convergence of AI-driven Drug Discovery and Longevity Target Biology

The convergence of artificial intelligence-driven drug discovery platforms with the expanding knowledge base of longevity target biology is creating a significant opportunity to accelerate the identification and validation of longevity compounds at a fraction of the historical cost and timeline. Traditional drug discovery for aging targets has been impeded by the complexity of aging biology, the large number of potential molecular targets across the hallmarks of aging, and the challenge of designing clinical trials that can measure meaningful changes in biological aging within commercially viable timeframes. AI platforms that can analyze large multi-omic datasets including genomic, transcriptomic, epigenomic, and proteomic profiles of aging tissues are enabling researchers to identify novel longevity targets, predict the biological activity of candidate molecules, and design drug combinations that address multiple aging hallmarks simultaneously. Insilico Medicine, a leading AI drug discovery company with a longevity research focus, has used its AI platform to identify novel targets and generate candidate molecules for aging-related diseases at timelines significantly shorter than conventional drug discovery. The NIH's National Institute on Aging, through its FY 2025 Budget, supports research into AI-assisted target identification for aging biology as part of its computational aging research portfolio, providing federal validation for the scientific value of this convergence.

Why Do Senolytic Therapies Lead the Market?

In 2026, the senolytic therapies segment is expected to hold the largest share of the longevity technologies market. Senolytics represent the most clinically advanced category within longevity biotechnology, with multiple compounds progressing through NIH-funded human clinical trials and a well-established preclinical evidence base. The NIA's FY 2025 Budget Justification confirms that NIA is currently funding senolytic clinical trials across conditions including frailty, Alzheimer's disease, diabetic kidney disease, idiopathic pulmonary fibrosis, and sepsis, making senolytics the only longevity technology category with active government-funded human clinical programs across multiple disease indications simultaneously. The NIA-funded Cellular Senescence Network provides a federally supported research infrastructure generating biological reference data that both academic and commercial senolytic programs rely upon. Commercial companies including Unity Biotechnology are developing senolytic drug candidates for age-related eye diseases and other conditions, advancing toward the regulatory approvals that will enable the full commercial market for this technology category.

However, the epigenetic reprogramming technologies segment is expected to witness the fastest growth during the forecast period. No other longevity technology category has attracted comparable private capital investment in recent years. Altos Labs was established in 2022 with approximately USD 3 billion in funding and a scientific team assembled from the world's leading aging and reprogramming researchers. Animal studies demonstrating that partial Yamanaka factor expression can reverse epigenetic aging in cells and tissues without triggering cancer or loss of cellular identity have provided a compelling scientific basis for this investment. As these companies progress from foundational research toward early human studies during the forecast period, the epigenetic reprogramming segment is expected to grow rapidly from its current early-stage revenue base into the most commercially significant longevity technology category by the end of the decade.

Why Do Therapeutics Lead the Product and Service Market?

In 2026, the therapeutics segment is expected to hold the largest share of the longevity technologies market by product and service. Longevity therapeutics encompass senolytic drugs, cellular rejuvenation therapies, and metabolic interventions including NAD+ precursors, rapamycin analogs, and GLP-1 receptor agonists that are being used or investigated for their longevity-related effects. These therapeutic products generate the largest per-unit revenue of any longevity product or service category, with physician-supervised longevity drug protocols at premium longevity clinics representing high-value commercial offerings. The NIA's ongoing funding of clinical trials for senolytic compounds confirms the therapeutic category's proximity to formal regulatory validation, which will unlock payer coverage and broader clinical adoption. Metabolic therapies including metformin, which is the subject of the NIH-funded TAME (Targeting Aging with Metformin) trial, represent an important near-term commercial category within longevity therapeutics given the drug's established safety profile and the broad clinical and consumer interest in its longevity applications.

However, the diagnostics and biomarker testing segment is expected to witness the fastest growth during the forecast period. Biological age testing using epigenetic clock algorithms developed from methylation data, as well as multi-omic biological age assessments, are gaining rapid consumer and clinical adoption as accessible entry points into personalized longevity monitoring and intervention. Companies including Elysium Health, Human Longevity Inc., and multiple emerging direct-to-consumer testing companies are offering biological age testing services that generate recurring consumer engagement. As clinical validation of biological age as a predictive endpoint for health outcomes accumulates through NIH and academic research programs, payer and physician acceptance of biological age testing as a clinical tool is expected to grow, expanding the market beyond direct-to-consumer into clinical diagnostics.

How Does the Clinical and Hospital-based Model Lead the Market?

In 2026, the clinical and hospital-based segment is expected to hold the largest share of the longevity technologies market by delivery model. The highest-value longevity interventions are delivered through clinical settings where physician supervision, diagnostic monitoring, and regulatory compliance requirements make clinical delivery the only viable model. Stem cell therapies, gene therapy applications targeting aging pathways, physician-supervised senolytic protocols, and comprehensive longevity health assessments involving whole-genome sequencing and advanced phenotyping require clinical infrastructure and licensed medical professionals for safe and effective delivery. The growing network of dedicated longevity clinics including those operated by Human Longevity Inc., Cleveland HeartLab, and an expanding number of physician-led longevity practices is delivering these high-value clinical longevity services to a premium consumer segment willing to pay out-of-pocket for comprehensive longevity medicine programs.

However, the direct-to-consumer segment is expected to witness the fastest growth during the forecast period. Consumer longevity products including epigenetic age testing kits, NAD+ supplement regimens, biological age tracking applications, and AI-powered longevity optimization platforms are achieving rapid adoption among health-conscious consumers who do not require physician involvement to access these products. The direct-to-consumer model benefits from digital distribution, subscription revenue models, and the ability to reach a much larger consumer base than clinical models can address. As consumer awareness of longevity science grows and the scientific credibility of consumer-accessible longevity products improves through clinical research validation, the direct-to-consumer segment is expected to grow significantly faster than the clinical model during the forecast period.

Why Does Healthy Aging and Healthspan Extension Lead the Application Market?

In 2026, the healthy aging and healthspan extension segment is expected to hold the largest share of the longevity technologies market. The concept of extending not just lifespan but the period of healthy, functional living drives the broadest consumer and clinical interest in longevity technologies. According to the WHO, the world's population aged 60 and older is growing faster than any other age group, and maintaining the health, independence, and social participation of this population is identified by the WHO as a global health priority. The UN World Population Prospects 2024 projects that by the late 2050s, more than half of all deaths globally will occur at age 80 or higher, compared to only 17% in 1995, confirming that humanity is already in the midst of a longevity transition that is creating large demand for technologies that maintain health quality during the extended later years of life. Longevity clinics, biological age monitoring programs, AI-driven health optimization platforms, and consumer longevity supplements all primarily address this healthspan extension application, making it the broadest and most commercially accessible application category.

However, the age-related disease prevention segment is expected to witness the fastest growth during the forecast period. The convergence of longevity science with conventional disease prevention medicine is accelerating as validated longevity biomarkers and senolytic compounds are evaluated in clinical trials for specific age-related diseases. The NIA FY 2026 Budget document confirms that as of September 2024, NIA was funding nearly 500 active clinical trials related to dementia prevention, treatment, and care, with senolytics and other aging-targeted interventions included among the drug and mechanistic targets being evaluated. The growth of Alzheimer's disease, cardiovascular disease, type 2 diabetes, and metabolic syndrome as primary drivers of age-related morbidity is creating large clinical and commercial demand for longevity technologies that can delay or prevent the onset of these conditions, with significant healthcare cost savings motivating payer interest in covering validated preventive longevity interventions.

Why Do Biotechnology and Pharmaceutical Companies Lead the End User Market?

In 2026, the biotechnology and pharmaceutical companies segment is expected to hold the largest share of the longevity market. These companies are the primary investors in, developers of, and commercial operators of longevity therapeutic technologies. Longevity biotechnology companies including Altos Labs, Unity Biotechnology, BioAge Labs, Cambrian Bio, and Insilico Medicine are the dominant buyers of longevity research tools, AI drug discovery platforms, biological age testing services, and preclinical research services. Large pharmaceutical companies are increasingly engaging with longevity science: Novo Nordisk's position in GLP-1 receptor agonist therapies, which have demonstrated metabolic benefits relevant to aging, and its broader investment in cardiometabolic disease create a commercial interest in longevity science that is beginning to manifest in internal research programs and external partnerships.

However, the longevity clinics and wellness centers segment is expected to witness the fastest growth during the forecast period. Consumer-facing longevity clinics are proliferating globally as an entrepreneurial and consumer-demand-driven commercial model that delivers premium longevity medicine directly to paying individuals. These clinics offer comprehensive biological age assessments, physician-supervised longevity protocols, NAD+ infusion therapy, peptide regimens, and personalized nutrition and lifestyle optimization programs at premium price points that generate high revenue per client. The direct-to-consumer delivery model of longevity clinics bypasses the lengthy pharmaceutical regulatory timeline and payer reimbursement process, allowing rapid commercial scaling ahead of formal regulatory validation of specific longevity interventions. As consumer awareness and purchasing power directed at longevity grows in line with the demographic aging trend documented by the UN and WHO, the longevity clinic and wellness center segment is expected to expand rapidly across North America, Europe, and Asia-Pacific.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to hold the largest share of the global longevity market. The United States is the primary market, supported by the world's largest concentration of longevity biotechnology companies and research institutions, the highest level of government funding for aging research through the NIH National Institute on Aging, and the largest and most commercially active consumer longevity market.

According to the NIA FY 2025 Budget Justification submitted to the U.S. Congress, NIA is currently funding clinical trials of senolytic compounds for multiple age-related conditions and supports a broad portfolio of basic and translational aging research through its extramural grants program. According to the NIA FY 2026 Budget document, as of September 2024 NIA was funding nearly 500 active clinical trials on dementia prevention and treatment alone, representing the largest single government investment in aging-related clinical research globally. The NIH Cellular Senescence Network, launched in 2021 as an NIH Common Fund project, is generating foundational senescent cell biology data that supports commercial longevity technology development across the U.S. research ecosystem. Private investment in U.S. longevity biotechnology has been substantial, with Altos Labs receiving approximately USD 3 billion and Retro Biosciences receiving USD 180 million in founding rounds, representing landmark capital commitments to the longevity science sector.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific is expected to witness the highest growth rate in the longevity technologies market during the forecast period. This growth is driven by the region's rapidly aging population, government policy prioritization of healthy aging, and growing private investment in longevity biotechnology.

Japan faces the world's most acute aging demographic challenge, with more than 29% of its population already aged 65 or over, according to Japan's Ministry of Internal Affairs and Communications 2024 data. The Japanese government's Society 5.0 initiative explicitly targets healthy aging and longevity technology development as a national priority, and Japanese academic institutions and companies are active in senolytic research, regenerative medicine, and longevity diagnostics. According to the United Nations World Population Prospects 2024, Japan is among the countries whose population has already peaked, making healthy aging technology adoption an urgent national priority. China's rapidly expanding elderly population, driven by decades of low fertility following the one-child policy, is creating one of the world's most pressing healthy aging challenges. The Chinese government's Healthy China 2030 plan includes healthy aging as a strategic objective, creating a policy environment that is directing domestic healthcare investment toward longevity and age-related disease prevention technologies. Singapore's government has positioned the country as a regional hub for aging research and longevity biotechnology, with the Agency for Science, Technology and Research funding multiple aging-related research programs and Singapore's Healthier SG national health strategy incorporating preventive aging care. South Korea's National Institute of Health and academic research institutions are also active in aging biology research, creating regional scientific capacity that supports local longevity technology development.

Some of the key companies operating in the global market for longevity technologies are Altos Labs, Calico Life Sciences, Life Biosciences, Unity Biotechnology, Retro Biosciences, Rejuvenate Bio, Insilico Medicine, BioAge Labs, Cambrian Bio, Turn Biotechnologies, Oisin Biotechnologies, Juvenescence, Human Longevity Inc., Elysium Health, and Novo Nordisk.

The global longevity technologies market is expected to grow from USD 9.64 billion in 2026 to USD 44.18 billion by 2036.

The global longevity technologies market is projected to grow at a CAGR of 16.4% from 2026 to 2036.

The senolytic therapies segment is expected to dominate the overall market in 2026, supported by its position as the most clinically advanced longevity technology with multiple NIA-funded human clinical trials active across frailty, Alzheimer's disease, and other age-related conditions. However, the epigenetic reprogramming technologies segment is expected to witness the fastest CAGR, driven by large private investments in companies including Altos Labs and Retro Biosciences and the scientific momentum behind partial cellular reprogramming as a multi-hallmark aging intervention.

The healthy aging and healthspan extension segment is expected to dominate the overall market in 2026. However, the age-related disease prevention segment is expected to witness the fastest CAGR, driven by the convergence of validated senolytic compounds with specific disease targets including Alzheimer's disease, where NIA is funding nearly 500 active clinical trials as of September 2024, and cardiovascular and metabolic disease prevention.

The biotechnology and pharmaceutical companies segment is expected to dominate the overall market in 2026. However, the longevity clinics and wellness centers segment is expected to witness the fastest CAGR, as direct-to-consumer longevity medicine programs expand rapidly in response to growing consumer demand for accessible, physician-supervised longevity optimization ahead of formal regulatory approval of specific longevity therapeutics.

North America is expected to lead the global market in 2026, anchored by U.S. government aging research investment through the NIH NIA and the concentration of longevity biotechnology companies. However, Asia-Pacific is expected to witness the fastest CAGR, driven by Japan's acute aging demographic, China's Healthy China 2030 policy framework, and Singapore's and South Korea's active longevity research investments.

The major players are Altos Labs, Calico Life Sciences, Life Biosciences, Unity Biotechnology, Retro Biosciences, Rejuvenate Bio, Insilico Medicine, BioAge Labs, Cambrian Bio, Turn Biotechnologies, Oisin Biotechnologies, Juvenescence, Human Longevity Inc., Elysium Health, and Novo Nordisk.

1. Introduction

1.1. Market Definition

1.2. Scope

1.3. Market Ecosystem

1.4. Currency and Limitations

1.4.1. Currency

1.4.2. Limitations

1.5. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Forecast Modeling

2.4. Data Triangulation

2.5. Assumptions

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rapid Growth in Aging Population

4.2.1.2. Rising Investments in Longevity Biotechnology

4.2.1.3. Advancements in AI-driven Drug Discovery

4.2.1.4. Increasing Focus on Healthspan Extension

4.2.2. Restraints

4.2.2.1. Limited Clinical Validation of Longevity Therapies

4.2.2.2. High Treatment and Development Costs

4.2.2.3. Regulatory and Ethical Concerns

4.2.3. Opportunities

4.2.3.1. Expansion of Epigenetic Reprogramming Technologies

4.2.3.2. Growth in Senolytics and Cellular Rejuvenation

4.2.3.3. Integration of Digital Biomarkers and AI

4.2.3.4. Personalized Longevity Medicine

4.2.4. Challenges

4.2.4.1. Long Clinical Development Timelines

4.2.4.2. Standardization of Aging Biomarkers

4.3. Technology Landscape

4.3.1. Senolytic Therapies

4.3.2. Epigenetic Reprogramming

4.3.3. Gene Editing and CRISPR Technologies

4.3.4. Stem Cell and Regenerative Medicine

4.3.5. AI-driven Longevity Drug Discovery

4.3.6. Digital Longevity Platforms and Biomarkers

4.3.7. NAD+ and Metabolic Therapies

4.4. Longevity Technologies Ecosystem

4.4.1. Longevity Biotechnology Companies

4.4.2. Pharmaceutical Companies

4.4.3. AI and Bioinformatics Providers

4.4.4. Longevity Clinics and Wellness Centers

4.4.5. Research Institutes and Universities

4.4.6. Venture Capital and Investors

4.5. Value Chain Analysis

4.5.1. Target Discovery

4.5.2. Biomarker Identification

4.5.3. Drug Discovery and Development

4.5.4. Clinical Validation

4.5.5. Commercialization and Patient Delivery

4.6. Regulatory Landscape

4.6.1. FDA and EMA Frameworks for Longevity Therapeutics

4.6.2. Clinical Trial Challenges in Aging Research

4.6.3. Ethical Considerations in Life Extension Technologies

4.6.4. Regulatory Landscape for Wellness and Longevity Clinics

4.7. Industry Trends

4.7.1. Rise of Cellular Rejuvenation Startups

4.7.2. Increasing Use of AI in Longevity Research

4.7.3. Expansion of Consumer Longevity Clinics

4.7.4. Growing Interest in Biological Age Testing

4.7.5. Shift Toward Preventive and Personalized Longevity Medicine

4.8. Cost and Pricing Analysis

4.8.1. Cost by Therapy Type

4.8.2. Cost of Personalized Longevity Treatments

4.8.3. Pricing Models for Longevity Clinics and Digital Platforms

5. Longevity Technologies Market, by Technology Type

5.1. Introduction

5.2. Senolytic Therapies

5.3. Epigenetic Reprogramming Technologies

5.4. Stem Cell and Regenerative Therapies

5.5. Gene Therapy and Gene Editing

5.6. AI-driven Drug Discovery Platforms

5.7. Longevity Diagnostics and Biomarkers

5.8. Digital Longevity Platforms

5.9. Other Longevity Technologies

6. Longevity Technologies Market, by Product and Service

6.1. Therapeutics

6.1.1. Senolytic Drugs

6.1.2. Cellular Rejuvenation Therapies

6.1.3. Metabolic Therapies

6.2. Diagnostics and Biomarker Testing

6.2.1. Biological Age Testing

6.2.2. Genomic and Epigenomic Testing

6.3. Digital Health Platforms

6.3.1. Longevity Monitoring Apps

6.3.2. AI Health Optimization Platforms

6.4. Services

6.4.1. Longevity Clinics

6.4.2. Personalized Wellness Programs

7. Longevity Technologies Market, by Delivery Model

7.1. Clinical and Hospital-based

7.2. Direct-to-Consumer

7.3. Hybrid Models

8. Longevity Technologies Market, by Application

8.1. Introduction

8.2. Healthy Aging and Healthspan Extension

8.3. Age-related Disease Prevention

8.3.1. Cardiovascular Diseases

8.3.2. Neurodegenerative Disorders

8.3.3. Metabolic Disorders

8.4. Regenerative Medicine

8.5. Precision and Personalized Medicine

8.6. Wellness and Preventive Healthcare

9. Longevity Technologies Market, by End User

9.1. Biotechnology and Pharmaceutical Companies

9.2. Hospitals and Clinics

9.3. Longevity Clinics and Wellness Centers

9.4. Research Institutes

9.5. Individual Consumers

10. Longevity Technologies Market, by Geography

10.1. Introduction

10.2. North America

10.2.1. U.S.

10.2.2. Canada

10.3. Europe

10.3.1. Germany

10.3.2. U.K.

10.3.3. Switzerland

10.3.4. France

10.3.5. Spain

10.3.6. Rest of Europe

10.4. Asia-Pacific

10.4.1. China

10.4.2. Japan

10.4.3. South Korea

10.4.4. Singapore

10.4.5. Australia

10.4.6. India

10.4.7. Rest of Asia-Pacific

10.5. Latin America

10.5.1. Brazil

10.5.2. Mexico

10.5.3. Rest of Latin America

10.6. Middle East and Africa

10.6.1. UAE

10.6.2. Saudi Arabia

10.6.3. South Africa

10.6.4. Rest of MEA

11. Competitive Landscape

11.1. Overview

11.2. Key Growth Strategies

11.3. Competitive Benchmarking

11.4. Competitive Dashboard

11.4.1. Industry Leaders

11.4.2. Technology Innovators

11.4.3. Emerging Startups

11.5. Market Ranking/Positioning Analysis

12. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

12.1. Altos Labs

12.2. Calico Life Sciences

12.3. Life Biosciences

12.4. Unity Biotechnology

12.5. Retro Biosciences

12.6. Rejuvenate Bio

12.7. Insilico Medicine

12.8. BioAge Labs

12.9. Cambrian Bio

12.10. Turn Biotechnologies

12.11. Oisin Biotechnologies

12.12. Juvenescence

12.13. Human Longevity, Inc.

12.14. Elysium Health

12.15. Novo Nordisk

13. Appendix

13.1. Customization Options

13.2. Related Reports

Published Date: Jun-2026

Published Date: Oct-2013

Published Date: Dec-2025

Published Date: Mar-2016

Subscribe to get the latest industry updates