Resources

About Us

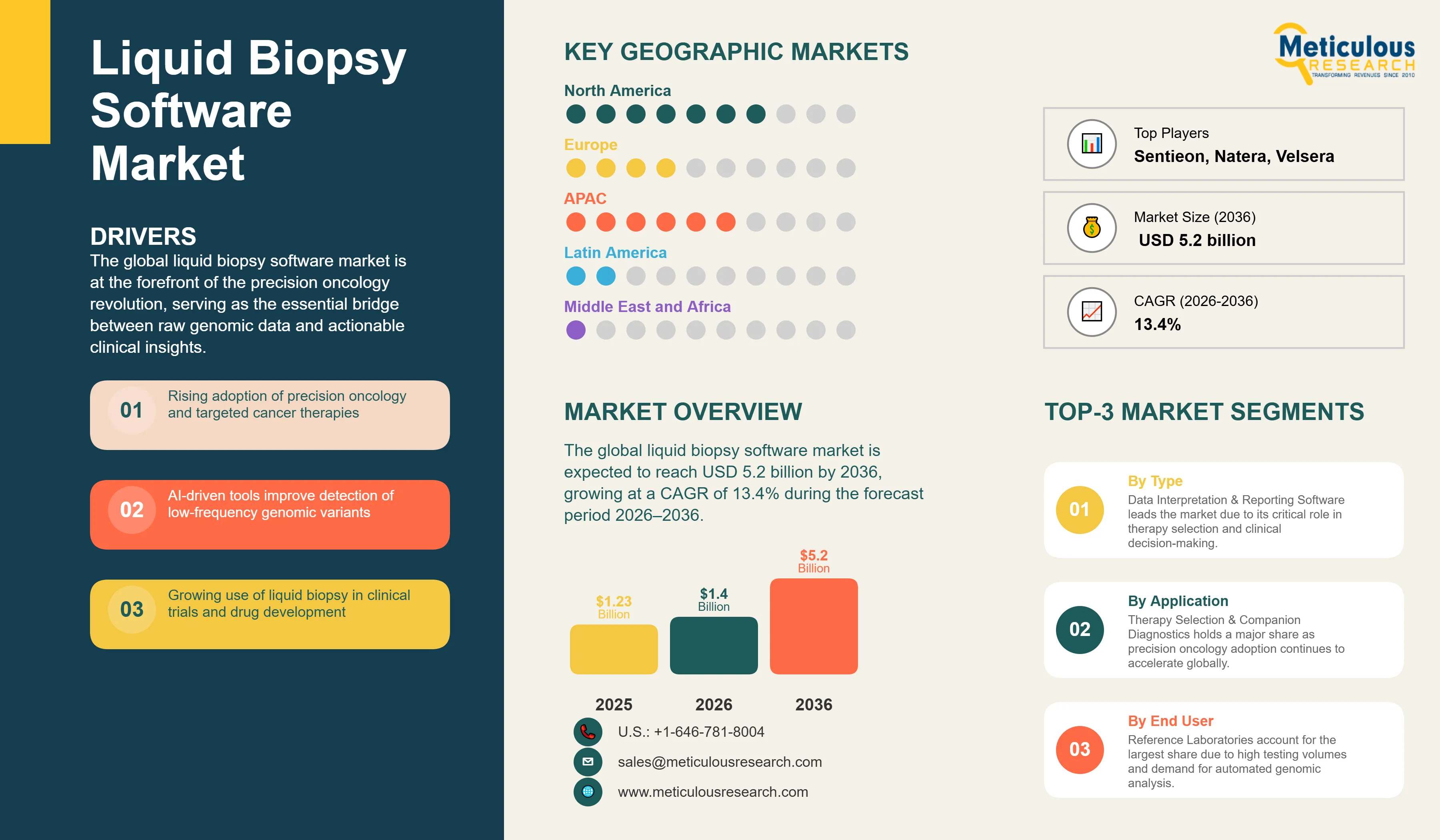

The global liquid biopsy software market was valued at USD 1.4 billion in 2026. This market is expected to reach USD 5.2 billion by 2036, growing at a CAGR of 13.4% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global liquid biopsy software market is at the forefront of the precision oncology revolution, serving as the essential bridge between raw genomic data and actionable clinical insights. As cancer continues to be a leading cause of mortality worldwide with approximately 20 million new cases diagnosed in 2024 the demand for minimally invasive diagnostic tools has surged. Liquid biopsy, which analyzes circulating tumor DNA (ctDNA), circulating tumor cells (CTCs), and other biomarkers from a simple blood draw, offers a transformative alternative to traditional tissue biopsies. However, the clinical utility of these assays is entirely dependent on sophisticated liquid biopsy bioinformatics and analytics software capable of detecting low-frequency variants amidst a vast background of healthy genetic material.

Modern oncology genomics software is designed to manage and analyze the large volumes of data generated by next-generation sequencing (NGS) platforms used in liquid biopsy workflows. Depending on sequencing depth and panel size, these workflows can generate datasets ranging from several gigabytes to hundreds of gigabytes, creating the need for robust data management, interpretation, and reporting solutions. Advanced bioinformatics pipelines automate sequence processing and variant interpretation, improving analytical efficiency and supporting more cost-effective assay development. These capabilities are particularly important for applications such as early cancer detection, where extremely low-frequency genomic alterations must be distinguished from background noise. Furthermore, the integration of precision oncology software into clinical workflows enables oncologists to identify targeted therapies and monitor treatment response and disease recurrence over time through minimal residual disease (MRD) analysis.

The market is also being shaped by the increasing regulatory clearance of companion diagnostics software. The FDA has cleared multiple liquid biopsy assays that include proprietary molecular diagnostics software for therapy selection. These tools not only automate liquid biopsy data interpretation but also ensure that reporting is standardized and compliant with global healthcare regulations. As pharmaceutical companies increasingly integrate liquid biopsy into clinical trials for biomarker discovery and patient stratification, the demand for robust cancer genomics software is expected to remain on a strong upward trajectory.

Geographically, North America is expected to lead the global liquid biopsy software market, accounting for approximately 45% of the market in 2026. This dominance is supported by a mature precision medicine ecosystem, widespread adoption of comprehensive genomic profiling, and favorable reimbursement frameworks. Meanwhile, Asia-Pacific is projected to register the fastest growth during the forecast period, with a CAGR of around 15.2%, driven by expanding genomic testing capabilities and increasing investments in precision oncology. As the broader liquid biopsy market continues to expand, software and analytics solutions are expected to play an increasingly important role in enabling data interpretation, clinical decision support, and treatment monitoring, positioning them as a high-value component of the oncology diagnostics ecosystem.

A primary driver for the liquid biopsy software market is the rapid adoption of precision oncology and targeted therapies. As the number of FDA-approved targeted cancer treatments grows, the need for companion diagnostics software to match patients with the right therapy becomes critical. Furthermore, the increasing prevalence of cancer worldwide—expected to reach 35 million new cases annually by 2050—is creating a massive demand for minimally invasive monitoring tools. The shift toward decentralized testing in hospitals and oncology centers is also driving the need for user-friendly liquid biopsy reporting software that can be integrated directly into local clinical workflows.

The primary restraint for the market is the extreme complexity of genomic data interpretation, particularly for liquid biopsy samples where tumor-derived DNA is present in very low concentrations. This high burden of proof for clinical validity and utility can slow the adoption of new bioinformatics tools. Additionally, data privacy and security concerns remain a significant hurdle. Managing sensitive patient genomic information in cloud-based liquid biopsy data management systems requires robust cybersecurity measures and compliance with stringent global regulations like GDPR and HIPAA, which can increase operational costs for software providers.

The integration of liquid biopsy software with broader digital health ecosystems presents a substantial growth opportunity. Connecting molecular diagnostics software directly to electronic health records (EHRs) and oncology decision support systems can streamline the patient journey and improve outcomes. Furthermore, the expansion into Multi-Cancer Early Detection (MCED) is a major frontier. MCED assays require highly complex cancer genomics software capable of analyzing multi-omic signals, including DNA methylation and fragmentomics, which offers a significant high-value opportunity for specialized software developers.

A major challenge in the market is the lack of standardization in bioinformatics workflows. Different variant calling and alignment strategies can lead to inconsistent results across platforms, complicating the clinical validation of liquid biopsy assays. Regulatory hurdles for AI-driven modules also persist, as the path to clearance for Software as a Medical Device (SaMD) is often complex and evolving. Manufacturers must continuously demonstrate that their liquid biopsy analytics software remains accurate and reliable as underlying sequencing technologies and clinical knowledge bases evolve.

Artificial intelligence and machine learning are increasingly being integrated into liquid biopsy analytics to improve the detection of low-frequency variants and reduce sequencing noise. According to the U.S. National Cancer Institute (NCI), approximately 70% of cancer patients may harbor actionable genomic alterations, increasing the need for advanced computational tools to support precision oncology. AI-enabled bioinformatics platforms are becoming essential for applications such as early cancer detection and minimal residual disease (MRD) monitoring.

Cloud-native genomic data management solutions are gaining traction as next-generation sequencing (NGS) adoption expands. According to the National Human Genome Research Institute (NHGRI), a single whole human genome sequence can generate around 100–200 GB of raw data, creating significant storage and computational requirements. Consequently, laboratories and pharmaceutical companies are increasingly adopting scalable cloud-based platforms to enable secure, multi-site genomic data analysis and collaboration.

Based on solution type, the market is segmented into Bioinformatics Pipelines, Data Interpretation & Reporting Software, and Data Management & Storage Solutions. In 2026, the Data Interpretation & Reporting Software segment is expected to hold the largest share. This is because the primary value of liquid biopsy in a clinical setting lies in its ability to provide actionable reports that guide therapy selection and patient management.

The Bioinformatics Pipelines segment is projected to witness the fastest growth, driven by the increasing complexity of NGS-based liquid biopsy assays and the need for highly sensitive algorithms to process raw sequencing data.

Based on end user, the market is segmented into Pharmaceutical & Biotechnology Companies, Reference Laboratories, and Hospitals & Oncology Centers. In 2026, the Reference Laboratories segment is expected to hold the largest share. These facilities handle the majority of high-volume clinical testing and require robust software for automated data processing and reporting.

The Pharmaceutical & Biotechnology Companies segment is projected to witness the fastest growth. This reflects the surging use of liquid biopsy software in drug development, clinical trial patient enrollment, and the identification of novel biomarkers for precision oncology.

North America is expected to hold the largest share of the global liquid biopsy software market in 2026, accounting for approximately 45% of total revenue. This position is supported by the region's advanced precision medicine infrastructure and the fact that U.S. Medicare covers comprehensive liquid biopsy profiling for advanced cancers. The presence of leading innovators like Illumina and Guardant Health further solidifies North America's leadership position.

In Europe, Germany, the UK, and France are the key markets, driven by the rising adoption of liquid biopsy in national cancer care plans. Meanwhile, Asia-Pacific is projected to be the fastest-growing region, with a CAGR of 15.2%. China's massive patient pool and increasing investment in genomic infrastructure are primary growth drivers. The key companies operating in the Asia-Pacific market include Illumina, Thermo Fisher Scientific, and regional players like Strand Life Sciences.

The global liquid biopsy software market is highly competitive, characterized by a mix of sequencing platform providers, specialized diagnostic companies, and pure-play bioinformatics firms. Competition is focused on the sensitivity of variant detection, the depth of clinical annotation, and the ease of integration into clinical workflows. Strategic partnerships between software developers and pharmaceutical companies for companion diagnostics development are a key competitive strategy.

Key players in the global market include Illumina, Inc. (U.S.), Thermo Fisher Scientific Inc. (U.S.), Guardant Health, Inc. (U.S.), Foundation Medicine, Inc. (U.S.), QIAGEN N.V. (Netherlands), Roche Molecular Systems, Inc. (U.S.), Agilent Technologies, Inc. (U.S.), Sophia Genetics SA (Switzerland), Tempus Labs, Inc. (U.S.), Natera, Inc. (U.S.), Adaptive Biotechnologies Corporation (U.S.), PierianDx (Velsera) (U.S.), Fabric Genomics, Inc. (U.S.), Golden Helix, Inc. (U.S.), Strand Life Sciences (India), Freenome Holdings, Inc. (U.S.), GRAIL, LLC (U.S.), Exact Sciences Corporation (U.S.), Bio-Rad Laboratories, Inc. (U.S.), and ArcherDX, Inc. (Invitae) (U.S.).

The market is projected to reach USD 5.2 billion by 2036, growing at a CAGR of 13.4% from 2026 to 2036.

Key terms include Liquid Biopsy Bioinformatics, Analytics, Data Interpretation, Reporting Software, and Precision Oncology Software.

Advanced bioinformatics software improves workflow efficiency and reduces operational complexity, enabling more cost-effective liquid biopsy assay development while maintaining high analytical sensitivity.

The Asia-Pacific region is projected to witness the fastest growth, with a CAGR of approximately 15.2%.

It transforms raw sequencing data into actionable reports that match cancer patients with targeted therapies and monitor treatment response.

The surge in precision oncology, advancements in AI for variant detection, and the growing pipeline of liquid biopsy assays are the primary drivers.

The market is expected to grow at a CAGR of 13.4% during the forecast period 2026–2036.

Data Interpretation & Reporting Software holds the largest share as it provides the direct clinical value required for patient management.

Challenges include the complexity of low-frequency variant detection and the lack of standardization in bioinformatics workflows.

Leading players include Illumina, Thermo Fisher Scientific, Guardant Health, Foundation Medicine, QIAGEN, SOPHiA Genetics, Tempus AI, and Roche Molecular Systems.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Solution Type

3.2.2. Market Analysis, by Technology

3.2.3. Market Analysis, by Application

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Surge in Precision Oncology and Targeted Therapy Adoption

4.2.1.2. Advancements in AI and ML for Low-VAF Variant Detection

4.2.1.3. Increasing Regulatory Clearance of Companion Diagnostics Software

4.2.1.4. Rising Use of Liquid Biopsy in Drug Development and Clinical Trials

4.2.2. Restraints

4.2.2.1. Extreme Complexity of Genomic Data Interpretation and Validation

4.2.2.2. Data Privacy and Security Concerns in Cloud Environments

4.2.3. Opportunities

4.2.3.1. Integration with Digital Health and Oncology Decision Support Systems

4.2.3.2. Expansion into Multi-Cancer Early Detection (MCED) Analytics

4.2.3.3. Untapped Potential in Emerging Genomic Infrastructure in APAC

4.2.4. Challenges

4.2.4.1. Lack of Standardization in Bioinformatics Workflows and Reporting

4.2.4.2. Complex Regulatory Pathways for AI-Driven SaMD Modules

4.2.5. Trends

4.2.5.1. Mainstreaming of AI-Enhanced Automated Variant Detection

4.2.5.2. Shift Toward Cloud-Native Scalable Genomic Data Platforms

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Liquid Biopsy Software Market, by Solution Type

5.1. Overview

5.2. Bioinformatics Pipelines

5.3. Data Interpretation & Reporting Software

5.4. Data Management & Storage Solutions

6. Global Liquid Biopsy Software Market, by Technology

6.1. Overview

6.2. Next-Generation Sequencing (NGS)-based Software

6.3. PCR-based Software

7. Global Liquid Biopsy Software Market, by Application

7.1. Overview

7.2. Early Cancer Detection

7.3. Therapy Selection/Companion Diagnostics

7.4. Treatment Monitoring/MRD Detection

8. Global Liquid Biopsy Software Market, by End User

8.1. Overview

8.2. Pharmaceutical & Biotechnology Companies

8.3. Reference Laboratories

8.4. Hospitals & Oncology Centers

9. Global Liquid Biopsy Software Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. Australia

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Dashboard

10.4. Vendor Market Positioning

10.5. Market Share Analysis, 2025

11. Company Profiles

11.1. Illumina, Inc.

11.2. Thermo Fisher Scientific Inc.

11.3. Guardant Health, Inc.

11.4. Foundation Medicine, Inc.

11.5. QIAGEN N.V.

11.6. Roche Molecular Systems, Inc.

11.7. Agilent Technologies, Inc.

11.8. SOPHiA Genetics SA

11.9. Tempus AI, Inc.

11.10. Natera, Inc.

11.11. Adaptive Biotechnologies Corporation

11.12. Velsera (PierianDx)

11.13. Fabric Genomics, Inc.

11.14. Golden Helix, Inc.

11.15. Strand Life Sciences

11.16. Exact Sciences Corporation

11.17. GRAIL, LLC

11.18. Bio-Rad Laboratories, Inc.

11.19. Sentieon, Inc.

11.20. BGI Genomics Co., Ltd.

12. Appendix

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: May-2026

Published Date: Nov-2022

Published Date: Sep-2016

Subscribe to get the latest industry updates