Resources

About Us

Pharmacovigilance Software Market Size, Share & Trends Analysis by Type, Deployment Mode, Component, End User, and Geography - Global Opportunity Analysis and Industry Forecast (2026-2036)

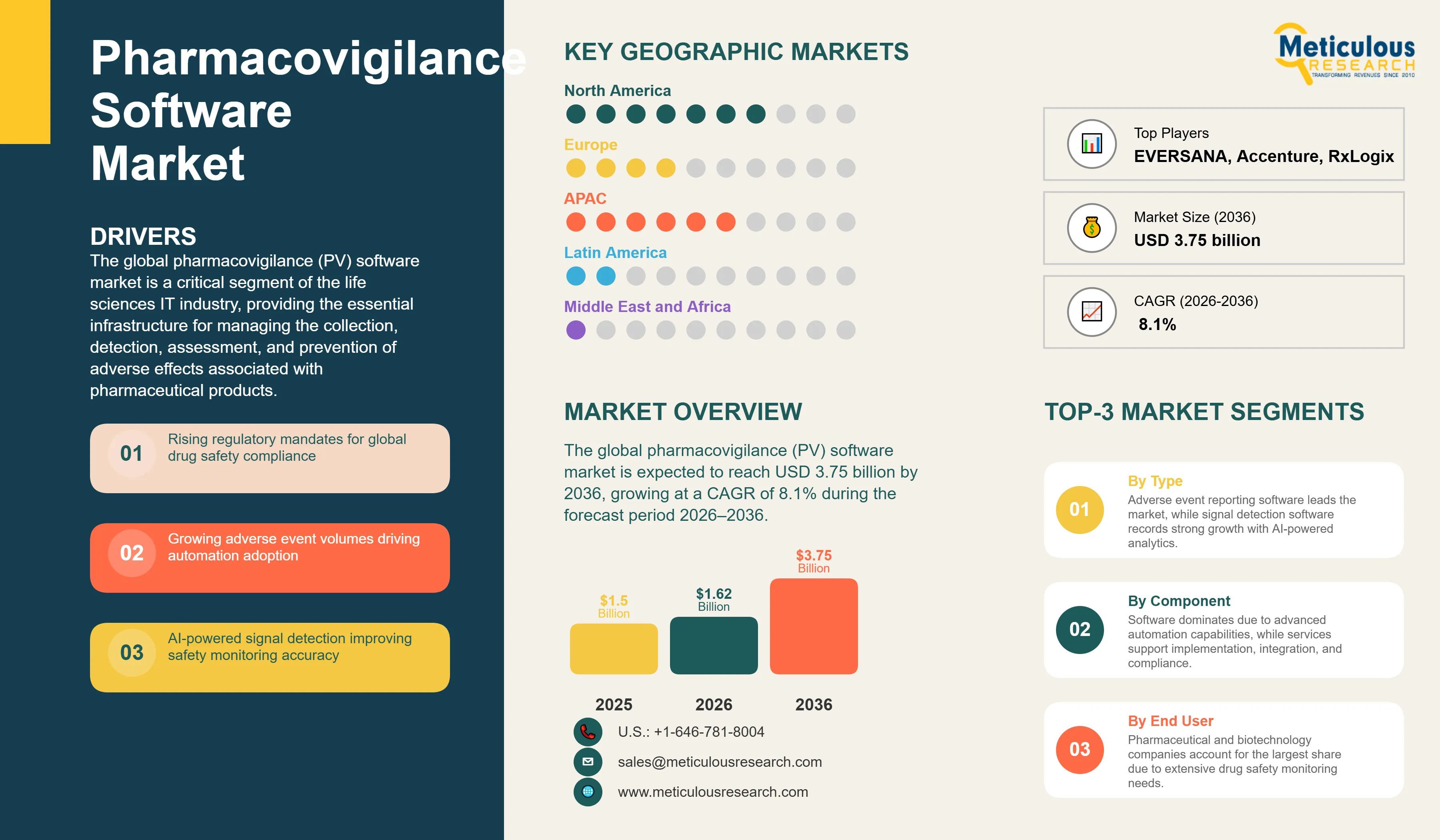

Report ID: MRHC - 1042043 Pages: 306 Jun-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global pharmacovigilance (PV) software market is valued at USD 1.62 billion in 2026. This market is expected to reach USD 3.75 billion by 2036, growing at a CAGR of 8.1% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global pharmacovigilance (PV) software market is a critical segment of the life sciences IT industry, providing the essential infrastructure for managing the collection, detection, assessment, and prevention of adverse effects associated with pharmaceutical products. PV software solutions, including adverse event reporting systems, signal detection platforms, and risk management tools, enable pharmaceutical companies and regulatory bodies to maintain institutional integrity and patient safety. As of 2026, the market is undergoing a significant transformation, driven by the global rise in drug approvals and the increasing volume of safety data from diverse sources, including clinical trials, post-marketing surveillance, and social media.

The transition toward automated and AI-driven PV platforms is essential for improving operational efficiency and regulatory compliance in the pharmaceutical industry. Modern PV software leverages advanced analytics and machine learning to automate routine case processing and identify subtle safety signals that may be missed by manual methods. Furthermore, the integration of PV software with Electronic Health Records (EHRs) and other healthcare IT systems ensures that stakeholders have immediate access to a comprehensive view of the drug's safety profile. As regulatory agencies like the FDA and EMA transition toward more data-intensive monitoring, the demand for PV solutions that can demonstrate improved diagnostic accuracy and reduced time-to-reporting is expected to surge.

Drivers: Escalating Regulatory Stringency and the Integration of AI-Driven Signal Detection

The primary driver for the PV software market is the escalating global regulatory stringency and the increasing volume of adverse event reports, which necessitates a more efficient and data-driven approach to drug safety. According to the FDA Adverse Event Reporting System (FAERS), the number of adverse event reports has increased significantly over the past decade, placing immense pressure on pharmaceutical companies to modernize their safety monitoring infrastructure. Furthermore, the shift toward digital health and the increasing demand for real-time safety insights are significant drivers. Government initiatives promoting the adoption of integrated safety platforms and the exchange of health information are compelling life sciences organizations to invest in PV solutions that can seamlessly integrate with broader healthcare IT ecosystems.

Restraints: High Implementation Costs and Data Privacy Challenges

Market growth is restrained by the high cost of implementing comprehensive PV software solutions and the technical challenges of achieving seamless data interoperability across disparate clinical and regulatory platforms. For many mid-sized pharmaceutical companies, the initial capital investment and ongoing maintenance costs of a PV platform can be a significant barrier. Additionally, the lack of standardized data protocols between different regional regulatory bodies often leads to data silos, making it difficult to achieve a truly unified global safety record. Concerns regarding data privacy and cybersecurity in centralized information hubs also act as deterrents to market expansion. Furthermore, the significant organizational change management and specialized training required for successful PV implementation can lead to slower adoption rates.

Opportunities: Advancing AI-Driven Case Processing and Cloud-Native Platforms

The integration of artificial intelligence (AI) and natural language processing (NLP) into PV platforms offers substantial growth opportunities. AI-powered tools can analyze complex safety reports and clinical evidence to identify subtle safety signals, facilitating more precise risk assessment and prevention. By 2026, AI-driven predictive analytics are being used to forecast the risk of adverse events, enabling proactive intervention and improving patient safety. Furthermore, the shift toward cloud-native (SaaS) PV platforms provides life sciences organizations with superior scalability, flexibility, and lower upfront costs. Cloud-based solutions also facilitate real-time data sharing among global safety teams, supporting multi-disciplinary collaboration, which is particularly beneficial for multinational pharmaceutical corporations.

Evolution toward Holistic and AI-Powered Drug Safety Orchestration

A key trend in 2026 is the transformation of pharmacovigilance platforms from standalone reporting systems into AI-enabled safety orchestration hubs. The U.S. FDA's FAERS database receives millions of adverse event reports and continues to expand its analytics capabilities through the new Adverse Event Monitoring System (AEMS), increasing demand for automated case intake and signal management tools. AI-driven workflows are being adopted to reduce manual processing and improve consistency, supporting a shift toward proactive, enterprise-wide safety management and greater operational efficiency.

Integration of Real-World Evidence and Social Media Monitoring

The integration of real-world evidence (RWE) and digital data sources into pharmacovigilance platforms is gaining momentum. The European Medicines Agency (EMA) has expanded its DARWIN EU network to 40 data partners across 18 countries, providing access to data from approximately 250 million patients to support regulatory decision-making. This growing use of RWE is accelerating the adoption of advanced signal detection and risk management capabilities, enabling earlier identification of safety concerns and strengthening post-marketing surveillance.

Analysis by Type

Based on type, the adverse event reporting software segment is expected to hold the largest share in 2026. This dominance is driven by the foundational role of these platforms in managing and archiving safety reports from various clinical and post-marketing sources. The signal detection software segment is projected to register the highest CAGR, reflecting the increasing demand for structured interpretation and AI-driven documentation to improve clinical productivity and regulatory compliance. Risk management software remains a critical segment, providing the technical expertise necessary for safety data processing.

Analysis by Deployment Mode

Based on deployment mode, the cloud-based segment is expected to account for the largest share in 2026. The advantages of cloud deployment, such as scalability, reduced IT burden, and ease of real-time data sharing among global safety teams, make it highly attractive to pharmaceutical companies. Approximately 70% of new PV installations in 2026 are opting for SaaS models. The on-premises segment continues to serve large organizations with specific data sovereignty requirements and those with significant existing IT infrastructure.

Geographic Analysis: Regional Growth and Regulatory Modernization

North America is expected to dominate the global PV software market in 2026, accounting for around 40% of total revenue. The region's leadership is supported by a high volume of adverse event reports, a mature healthcare IT landscape, and significant investments in AI-driven safety monitoring by major pharmaceutical companies. Favorable reimbursement policies and a strong regulatory focus on drug safety and clinical quality continue to drive market growth in the U.S. and Canada. The presence of leading PV vendors and a robust ecosystem for medical innovation also contribute to North America's dominant position.

The Asia Pacific region is projected to witness the fastest growth during the forecast period. This growth is fueled by the rising burden of clinical research and government initiatives to modernize healthcare infrastructure and expand access to drug safety monitoring across China, India, and Japan. As these countries implement large-scale digital health initiatives and increase their focus on expanding access to specialized safety monitoring, the demand for integrated PV solutions is expected to rise significantly. The increasing adoption of cloud-based platforms and the digital transformation of public health agencies in the region are creating substantial opportunities for global and local PV vendors.

The competitive landscape of the global PV software market is characterized by intense innovation and strategic consolidations as vendors seek to provide end-to-end drug safety orchestration platforms. Leading players are differentiating themselves through the sophistication of their AI engines and their ability to provide seamless integration with EHRs and regulatory platforms. Strategic acquisitions of niche safety and analytics companies are a common trend as vendors seek to enhance their diagnostic capabilities. The market is also seeing increased collaboration between PV vendors and pharmaceutical companies to ensure seamless safety monitoring across the drug lifecycle.

Key players operating in the global PV software market include Oracle Corporation (Argus) (U.S.), ArisGlobal (U.S.), Veeva Systems Inc. (U.S.), IQVIA Holdings Inc. (U.S.), Ennov (France), AB Cube (France), UnitedGenomics (U.S.), Sarjen Systems Pvt. Ltd. (India), Sparta Systems (Honeywell) (U.S.), and various emerging technology providers specializing in safety informatics and AI-driven diagnostic tools.

The market is projected to reach USD 3.75 billion by 2036, growing at a CAGR of 8.1% from 2026 to 2036.

Companies report a significant reduction in case processing times and an improvement in the accuracy of signal detection.

The signal detection software segment is expected to grow the fastest as companies prioritize AI-driven interpretation and documentation.

Approximately 70% of new deployments are cloud-native, enabling real-time data sharing and scalability.

North America holds the largest share of around 40% in 2026, driven by high safety data volumes and mature IT infrastructure.

AI enables the prediction of adverse event risk and automates routine case intake, improving diagnostic consistency and patient safety.

The surge in new drug approvals is driving the demand for integrated PV platforms to manage the high volume of safety data and regulatory reports.

Pharmaceutical and biotechnology companies are the primary adopters, managing the highest volumes of safety data across diverse product portfolios.

These systems provide the continuous, data-driven safety management necessary to improve clinical outcomes and reduce the total cost of care.

The top 5 players are Oracle Corporation (Argus), ArisGlobal, Veeva Systems Inc., IQVIA Holdings Inc., and Ennov.

Published Date: Jun-2026

Published Date: May-2024

Published Date: Sep-2016

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates