Resources

About Us

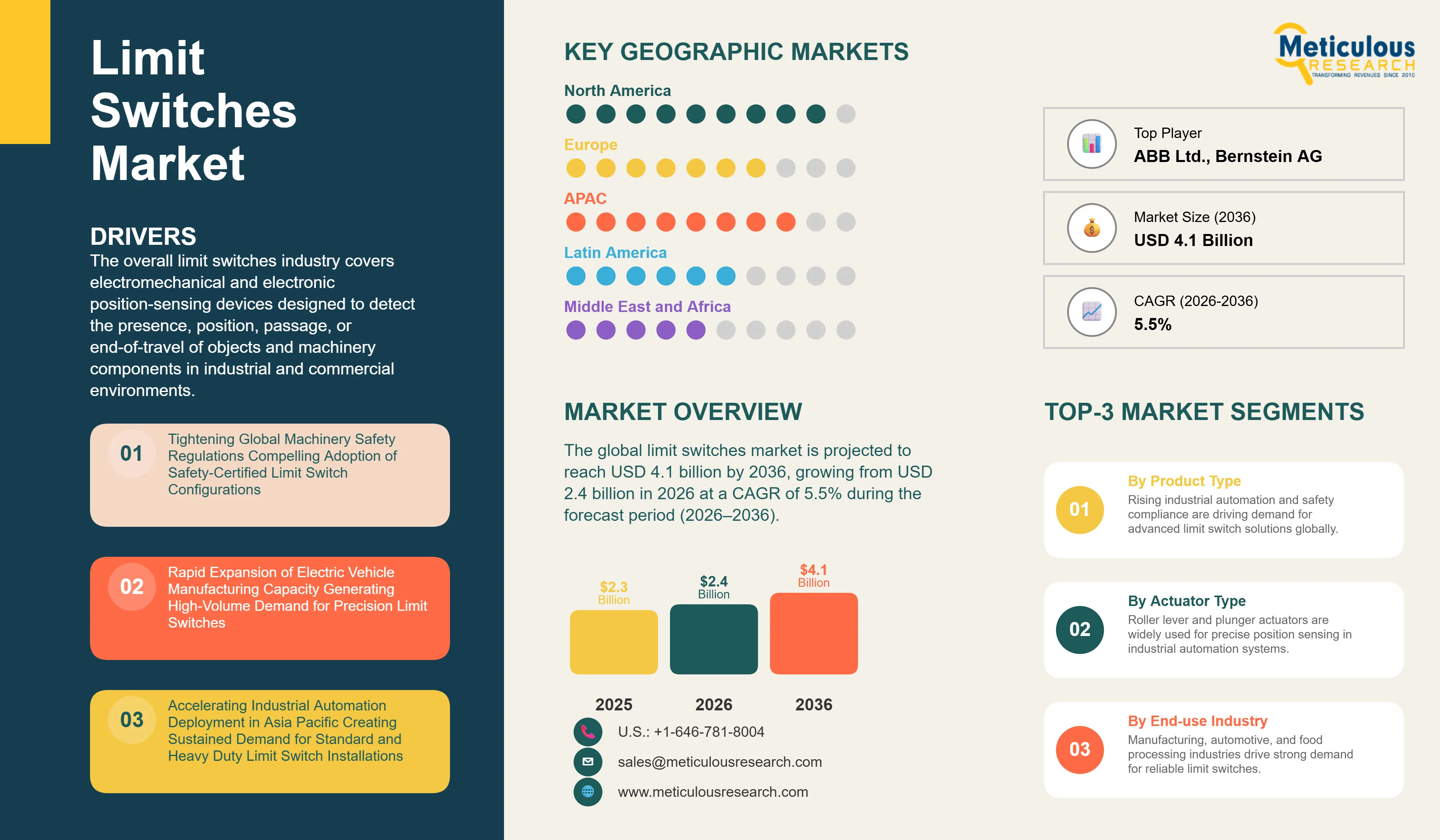

The global limit switches market was valued at USD 2.3 billion in 2025. This market is projected to reach USD 4.1 billion by 2036, growing from USD 2.4 billion in 2026 at a CAGR of 5.5% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

The overall limit switches industry covers electromechanical and electronic position-sensing devices designed to detect the presence, position, passage, or end-of-travel of objects and machinery components in industrial and commercial environments. The market encompasses standard general purpose limit switches, heavy duty limit switches, safety limit switches, explosion-proof and hazardous location limit switches, and miniature limit switches, differentiated by actuator type, housing material, switching capacity, environmental protection rating, and safety certification level. These products are deployed across a broad range of end-use industries including manufacturing and industrial automation, automotive, food and beverage processing, pharmaceutical manufacturing, oil and gas and petrochemical, mining and mineral processing, power generation, and aerospace and defense, where reliable position detection and control circuit switching are foundational to process automation, machine safety, and operational continuity.

Limit switches serve as critical control circuit components in applications ranging from conveyor end-of-travel detection and crane hoist overtravel protection to machine tool door interlocking, robotic cell guarding, and valve position indication in process plants. Their integration into safety-related control systems is governed by international standards including IEC 60947-5-1, which defines the performance and testing requirements for control circuit devices and switching elements including limit switches, and ISO 13849-1:2023, which establishes the framework for designing safety-rated control system architectures incorporating position-sensing devices to achieve defined Performance Levels for machine safeguarding applications. These standards, alongside IEC 62061:2021 for functional safety of safety-related control systems, collectively define the certification requirements that govern the specification and procurement of safety-rated limit switch products across regulated industrial markets globally.

The growth of the limit switches market is primarily driven by the continued global expansion of industrial automation infrastructure, the tightening of machinery safety and hazardous area regulations across major industrial economies, and the growing adoption of IO-Link enabled smart limit switch configurations that deliver sensor diagnostics and remote parameterization capabilities compatible with Industry 4.0 control architectures. In Europe, the EU Machinery Regulation (EU) 2023/1230, published in the Official Journal of the European Union on June 29, 2023, and scheduled to apply across all EU member states from January 20, 2027, represents the most significant update to European machinery safety legislation in nearly two decades. This regulation replaces the Machinery Directive 2006/42/EC and introduces updated conformity assessment requirements for machinery and safety components, including interlocking devices and position sensors incorporated into guard monitoring and emergency stop circuits, creating a broad compliance-driven investment cycle for safety-rated limit switch upgrades across European industrial facilities. In the United States, OSHA's machine guarding regulations under 29 CFR 1910.212 establish mandatory requirements for guarding machinery with exposed moving parts, with position-sensing interlocks representing a widely specified engineering control for guard monitoring applications. NFPA 79: Electrical Standard for Industrial Machinery and NFPA 70E: Standard for Electrical Safety in the Workplace further reinforce the specification of appropriately rated and classified limit switch products in North American industrial machinery installations.

Beyond regulatory compliance, the accelerating adoption of automated manufacturing systems across automotive, electronics, and consumer goods sectors is generating sustained incremental demand for limit switches as essential position-sensing components in robotic welding cells, automated guided vehicles, precision stamping press lines, and high-speed assembly equipment. The rapid global expansion of electric vehicle manufacturing capacity across China, the United States, and Europe is a particularly significant driver, as EV battery module assembly and body-in-white production lines are highly automated and require large quantities of precision position-sensing and interlocking devices with stringent performance and durability requirements. The integration of IO-Link communication interfaces, standardized under IEC 61131-9, into modern limit switch designs is enabling manufacturers to differentiate through smart diagnostics, remote parameterization, and real-time device health monitoring that reduce maintenance costs and unplanned downtime in automated production environments.

Despite strong growth fundamentals, the market faces competitive pressure from non-contact sensing technologies including inductive proximity sensors, photoelectric sensors, and laser displacement sensors, which offer longer service life in high-cycle applications where electromechanical contact wear has historically been a maintenance concern. The displacement of conventional electromechanical limit switches by solid-state sensing technologies in new high-speed machinery installations represents an ongoing structural challenge that is moderating volume growth in standard product categories, while simultaneously driving product development investment toward more durable, IP69K-rated, and electronically enhanced limit switch designs. Price pressure in standard and commodity product segments, particularly across Asian markets, continues to compress margins for manufacturers relying on conventional electromechanical product lines without differentiated safety or connectivity features.

The tightening of machinery safety regulations globally and the compliance obligations introduced by the EU Machinery Regulation across European industrial sectors represent the most significant near-term growth opportunity for manufacturers of safety-rated and guard-locking limit switch products. The growing deployment of automated manufacturing capacity in emerging markets across Asia Pacific, the Middle East, and Latin America is creating structurally new demand for both standard and safety-certified limit switch configurations across automotive, food processing, and pharmaceutical industries where greenfield manufacturing investment is concentrated. The continued expansion of oil, gas, and chemical processing infrastructure globally, combined with growing chemical manufacturing capacity in Asia Pacific, is sustaining demand for ATEX Directive (EU) 2014/34/EU and IECEx certified explosion-proof limit switch variants in hazardous area applications where non-contact sensing alternatives face environmental and reliability limitations.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 4.1 Billion |

|

Market Size in 2026 |

USD 2.4 Billion |

|

Market Size in 2025 |

USD 2.3 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 5.5% |

|

Dominating Product Type |

Standard/General Purpose Limit Switches |

|

Fastest Growing Product Type |

Safety Limit Switches |

|

Dominating Actuator Type |

Roller Lever Actuator |

|

Fastest Growing Actuator Type |

Plunger/Push Rod Actuator |

|

Dominating End-use Industry |

Manufacturing & Industrial Automation |

|

Fastest Growing End-use Industry |

Automotive |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

EU Machinery Regulation (EU) 2023/1230 and Evolving Global Machinery Safety Standards Accelerating Adoption of Safety-Certified Limit Switches

The EU Machinery Regulation (EU) 2023/1230, published in the Official Journal of the European Union on June 29, 2023, marks the most consequential revision to European machinery safety legislation since the original Machinery Directive 2006/42/EC came into effect. The regulation applies across all EU member states from January 20, 2027, and introduces a substantially updated conformity assessment framework governing the design, manufacture, and certification of machinery and associated safety components, including the interlocking and guard monitoring devices that represent one of the most commercially significant application categories for safety limit switches. Unlike its predecessor directive, the regulation directly addresses emerging technologies including collaborative robotics, AI-integrated machinery control systems, and self-evolving machine architectures, and requires that safety-related position sensing devices incorporated into these systems satisfy updated Performance Level and Safety Integrity Level requirements under ISO 13849-1:2023 and IEC 62061:2021. This creates a broad and structurally new compliance investment cycle for European industrial operators, who are required to assess the safety architecture of their machinery installations and upgrade interlocking and position detection devices to certified safety limit switch solutions that satisfy the regulation's expanded essential health and safety requirements before the application date.

Outside Europe, equivalent regulatory developments are reinforcing safety-certified limit switch adoption across other major industrial markets. In the United States, OSHA's machine guarding regulations under 29 CFR 1910.212 establish mandatory general industry requirements for guarding machinery with exposed moving parts, with position-sensing interlocks serving as a widely used engineering control solution. OSHA's ongoing enforcement activities in metalworking, food processing, and packaging machinery industries continue to drive compliance-led procurement of appropriately rated limit switch configurations. In Japan, the Industrial Safety and Health Act and associated ministerial ordinances governing machinery safety sustain demand for JIS-certified limit switch configurations across Japanese manufacturing sectors. In China, GB standards for machinery safety and the State Administration for Market Regulation's enforcement of safety component certification requirements are progressively raising the minimum specification level applicable to limit switches in new machinery installations. Collectively, these regulatory developments are shifting limit switch procurement in new industrial installations from commodity-grade standard configurations toward higher-value safety-certified products, consistently expanding the addressable revenue opportunity for manufacturers with established safety-rated product portfolios.

IO-Link Integration and Smart Sensing Capabilities Reshaping the Competitive Landscape for Industrial Limit Switches

The adoption of IO-Link communication interfaces, standardized under IEC 61131-9 as the first internationally standardized input/output technology for sensor and actuator communication, is fundamentally reshaping the value proposition and competitive differentiation framework of the global limit switches market. Traditional electromechanical limit switches communicated only a binary switching signal, providing no capability for remote diagnostics, parameter adjustment, or operating condition monitoring. IO-Link enabled limit switches, by contrast, transmit real-time data on switching status, total accumulated operating cycles, ambient temperature conditions, and device health diagnostics to programmable logic controllers and industrial IoT gateways, enabling condition-based maintenance scheduling and reducing unplanned downtime in automated production environments.

Leading manufacturers including Schmersal Group, Balluff GmbH, ifm electronic gmbh, and Pepperl+Fuchs SE have integrated IO-Link interfaces into their safety and standard limit switch product lines, enabling these devices to function as intelligent nodes within Industry 4.0 manufacturing architectures. Schmersal's AZM series safety switches and Balluff's BNS safety position switches incorporate diagnostic communication capabilities that allow maintenance teams to monitor device condition remotely and anticipate replacement needs before switch failure causes unplanned production stoppages. This shift from binary signal devices to digitally communicating intelligent sensors is broadening the competitive advantage for manufacturers with established connectivity portfolios while creating displacement risk for conventional hardware-only suppliers competing primarily on price in standard product categories.

The business case for IO-Link integrated limit switches is strongest in high-throughput manufacturing environments where unplanned downtime costs are significant and where distributed sensor networks across large production facilities benefit most from centralized remote monitoring and predictive maintenance capabilities. Automotive body shops, electronics assembly plants, and pharmaceutical packaging lines represent the application environments where the productivity benefits of smart limit switch connectivity translate most directly into measurable return on investment. As IO-Link master module adoption expands across control cabinet installations globally and as smart manufacturing investment continues to grow across North America, Europe, and Asia Pacific, demand for IO-Link capable limit switches is expected to grow materially faster than the overall market during the forecast period, creating a structural shift in the revenue mix of leading manufacturers toward higher-value connected product configurations.

Rapid Electric Vehicle Manufacturing Expansion Generating High-Volume Demand for Precision Limit Switches in Automotive Applications

The global electric vehicle industry has entered a phase of accelerated production capacity expansion, with major automotive manufacturers and battery producers investing heavily in new assembly plants, battery module production facilities, and supporting component supply chains across China, the United States, Europe, and emerging production hubs in Southeast Asia and Latin America. This expansion is generating significant incremental demand for precision limit switches as essential position-sensing and interlocking components in EV-specific manufacturing processes including battery cell assembly, module and pack production, battery management system testing, body-in-white stamping and robotic welding, and final vehicle assembly operations.

EV battery manufacturing processes in particular require large quantities of precision limit switches for detecting tray and module positions in automated assembly lines, monitoring press positions during cell stacking and compression operations, and providing interlocking protection on enclosures housing high-voltage components. The combination of cleanroom environment requirements in cell manufacturing facilities and the chemical exposure risks associated with electrolyte handling in battery production creates a specific demand profile for stainless steel housing, IP69K-rated, and chemically resistant limit switch variants that command meaningful price premiums over standard industrial configurations.

In China, the world's largest electric vehicle market and the country with the most extensive EV manufacturing infrastructure, state-backed programs including the New Energy Vehicle Industrial Development Plan have supported the rapid scaling of domestic EV production capacity, targeting sustained growth in annual EV output through 2030 and beyond. In the United States, the Inflation Reduction Act of 2022 included significant provisions for domestic EV manufacturing investment, catalyzing new automotive assembly and battery plant construction projects across multiple states. In Europe, the combination of EU fleet emissions regulations targeting zero-emission new passenger car sales by 2035 and national industrial policy support has driven substantial OEM and Tier 1 supplier investment in EV production infrastructure, all of which represent addressable demand for precision limit switch manufacturers holding appropriate automotive quality management and IATF 16949 certification credentials.

By Product Type: In 2026, the Standard/General Purpose Limit Switches Segment to Dominate the Global Limit Switches Market

Based on product type, the limit switches industry is segmented into standard/general purpose limit switches, heavy duty limit switches, safety limit switches, explosion-proof/hazardous location limit switches, and miniature limit switches. In 2026, the standard/general purpose limit switches segment is expected to account for the largest share of this market. The dominant position of this segment reflects the pervasive deployment of standard limit switch configurations across the broadest range of industrial automation applications globally, including conveyor systems, material handling equipment, machine tool end-of-travel detection, overhead crane overtravel protection, elevator shaft position sensing, and general-purpose position interlocking across manufacturing and processing facilities. Standard limit switches manufactured under Honeywell's MICRO SWITCH brand, Schneider Electric's Telemecanique Sensors brand, OMRON Corporation, Rockwell Automation's Allen-Bradley brand, and Eaton Corporation represent the core volume category of the global market, with well-established distribution channels, broad global availability, and competitive pricing that reinforces their selection as the default specification across the majority of new and replacement industrial automation projects worldwide.

However, the safety limit switches segment is projected to register the highest growth during the forecast period. The growth of this segment is driven by the compliance requirements introduced by the EU Machinery Regulation (EU) 2023/1230, which applies from January 20, 2027, and mandates that safety-rated interlocking devices incorporated into machinery control systems demonstrate compliance with updated Performance Level requirements; the ongoing global adoption of ISO 13849-1:2023 and IEC 62061:2021 across machinery manufacturers in North America, Asia Pacific, and other markets; and the growing awareness among industrial operators of the liability and operational risks associated with substandard or uncertified guard interlocking configurations. Manufacturers including Schmersal Group, Pilz GmbH & Co. KG, SICK AG, and Honeywell International Inc. are well positioned to capture this growth through their established safety-rated product portfolios, and the segment is expected to consistently outpace the broader market throughout the forecast period as compliance-driven replacement of legacy non-safety-rated limit switch configurations accelerates across regulated industrial markets.

By Actuator Type: In 2026, the Roller Lever Actuator Segment to Account for the Largest Share

Based on actuator type, the limit switches industry is segmented into roller lever actuator, adjustable roller lever actuator, plunger/push rod actuator, wobble stick/adjustable rod actuator, fork lever actuator, and rotary actuator. In 2026, the roller lever actuator segment is expected to account for the largest share of this market. The dominant position of this actuator configuration reflects its status as the industry-standard mechanical interface for the majority of industrial position detection applications, where the roller tip design provides reliable actuation by a moving workpiece or machine component from a defined direction while offering durability against repetitive contact loads. Roller lever actuated limit switches are the default specification across conveyor systems, transfer lines, stamping press safety guarding, and overhead material handling systems in virtually all global manufacturing and processing sectors, and their continued high-volume installation in both new and replacement applications sustains their market leadership position through the forecast period.

However, the plunger/push rod actuator segment is projected to register the highest growth during the forecast period. The growth of this segment is driven by the expanding adoption of precision plunger-type limit switches in applications requiring highly accurate and repeatable position detection with minimal mechanical overtravel, including pharmaceutical tablet press position monitoring, semiconductor wafer handler position sensing, food processing packaging line registration detection, and precision tooling position verification in aerospace component manufacturing. Plunger actuator switches offer shorter operating differential and more precise switching point repeatability compared to lever-type configurations, making them the preferred selection for applications where tight positional tolerances are critical to product quality and process consistency. The growth of pharmaceutical, semiconductor, and specialty food processing manufacturing capacity globally is creating an expanding addressable market for precision plunger-actuated limit switches with stainless steel housings, FDA-compliant sealing materials, and cleanroom-compatible construction.

By End-use Industry: In 2026, the Manufacturing & Industrial Automation Segment to Hold the Largest Share

Based on end-use industry, the limit switches industry is segmented into manufacturing and industrial automation, automotive, food and beverage processing, pharmaceutical, oil and gas and petrochemical, mining and mineral processing, power generation, and other end-use industries. In 2026, the manufacturing and industrial automation segment is expected to account for the largest share of this market, reflecting the pervasive use of limit switches as fundamental position-sensing components across machine tools, conveyor systems, robotic assembly cells, automated guided vehicles, palletizers, winding machines, and a broad range of industrial automation equipment. The continued global expansion of manufacturing capacity across diverse industries, combined with the widespread aging of existing automation infrastructure in mature industrial economies generating replacement demand, sustains the dominant revenue position of this segment through the forecast period. The accelerating rollout of robotic automation and automated material handling systems across North America, Europe, and Asia Pacific is generating incremental new installation demand for limit switches as essential position-sensing and interlocking devices within automated cell architectures.

However, the automotive segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the unprecedented expansion of electric vehicle manufacturing capacity globally, which is generating high-volume demand for precision limit switches in battery module assembly automation, stamping and welding body shop operations, and final assembly line equipment; the accelerating adoption of robotic welding, laser cutting, and automated assembly systems in automotive manufacturing that incorporate large quantities of position-sensing and interlocking limit switches in their safety and control architectures; and the tightening of automotive supplier quality requirements including IATF 16949 certification, which mandates the use of appropriately rated and documented position-sensing components in machinery and automation systems across the automotive supply chain. The geographic expansion of automotive and EV manufacturing capacity into new production hubs across Southeast Asia, Eastern Europe, and Mexico is additionally creating new addressable market territory for limit switch suppliers with established automotive qualification programs and local technical support capabilities.

Based on geography, the overall limit switches market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of this market. The dominant revenue position of North America reflects the combination of the highest average unit values driven by stringent OSHA machine guarding and hazardous location compliance requirements, a large installed base of aging industrial automation infrastructure across manufacturing, oil and gas, and food processing sectors requiring replacement and upgrade, and the presence of leading limit switch manufacturers including Honeywell International Inc. and Rockwell Automation, Inc. alongside major system integrators and OEM machinery builders that represent a concentrated and high-value procurement base. The United States benefits from continued investment in reshoring and nearshoring of manufacturing capacity driven by supply chain resilience priorities and domestic manufacturing incentive programs, contributing to new installation demand for limit switches and associated control devices. Canada's significant oil sands and petrochemical processing sector sustains specialized demand for explosion-proof and heavy-duty limit switch configurations in hazardous area applications requiring ATEX and IECEx certification equivalents.

However, the Asia Pacific limit switches market is expected to grow at the fastest rate from 2026 to 2036. The rapid growth of this market is driven by the massive expansion of manufacturing capacity across China, India, Japan, South Korea, and Southeast Asia in sectors including automotive, electronics, consumer goods, food processing, and pharmaceuticals, all of which represent significant and growing demand for limit switches as foundational automation components. China's position as the world's largest automotive market and the dominant global EV production hub is generating particularly concentrated demand for precision limit switches in EV battery assembly and vehicle manufacturing. India's Production Linked Incentive scheme, which has committed substantial capital incentives to electronics, automotive components, and pharmaceutical manufacturing sectors, is accelerating the buildout of new automated manufacturing capacity that generates limit switch installation demand across multiple industries. Japan and South Korea's advanced electronics and semiconductor manufacturing industries represent a structurally sophisticated demand base for high-precision and cleanroom-compatible limit switch configurations. The rapid growth of food and beverage processing and pharmaceutical manufacturing across Southeast Asia, driven by foreign direct investment inflows and regional supply chain diversification, is additionally expanding addressable demand for food-grade and pharmaceutical-grade limit switch variants across these markets.

Europe is a well-established and technically advanced market for limit switches, supported by a strong machinery safety regulatory framework anchored by the EU Machinery Regulation (EU) 2023/1230, the ATEX Directive (EU) 2014/34/EU for hazardous location equipment, and a large installed base of high-precision manufacturing, automotive, and food and beverage processing industries. European manufacturers including Schmersal Group, Bernstein AG, Balluff GmbH, ifm electronic gmbh, and Pepperl+Fuchs SE maintain strong regional market positions through deep application expertise and close customer relationships with European OEM machinery builders and automotive Tier 1 suppliers. The widespread adoption of machinery safety standards across European industrial markets sustains a structurally higher proportion of safety-rated and IO-Link capable limit switch procurement relative to global averages, supporting above-average revenue per unit and favorable aftermarket positions for established regional manufacturers.

Latin America and the Middle East and Africa, while smaller in absolute revenue terms, are progressively expanding addressable markets for limit switches driven by industrial capacity investment in automotive, food processing, and mining sectors. In Latin America, Mexico's established automotive manufacturing base and expanding EV supply chain investment, as well as Brazil's significant agricultural processing and mining sectors, represent the primary demand drivers. In the Middle East, ongoing investment in petrochemical and gas processing infrastructure across Saudi Arabia and the UAE sustains demand for explosion-proof and heavy-duty limit switch configurations in upstream and downstream oil and gas applications.

The global limit switches market is moderately consolidated, with competition primarily driven by product breadth across actuator configurations and housing variants, safety certification coverage, application engineering support capabilities, and the strength and geographic reach of distribution networks serving industrial OEM machinery builders and end-user maintenance procurement channels. Key differentiators include the availability of explosion-proof variants certified to ATEX Directive (EU) 2014/34/EU and IECEx standards for hazardous location applications, safety-rated product lines certified to Performance Level d or e under ISO 13849-1:2023 for machinery safety applications, IO-Link digital communication capability for Industry 4.0 compatible installations, and housing options in plastic, die-cast zinc, aluminum, and stainless steel for food, pharmaceutical, and wash-down environments.

Large diversified automation manufacturers including Honeywell International Inc., Schneider Electric SE, Siemens AG, Rockwell Automation, Inc., ABB Ltd., and Eaton Corporation plc compete through comprehensive product portfolios spanning standard, heavy duty, safety, and explosion-proof limit switch categories, extensive global distribution networks, and strong OEM program relationships that position their limit switch brands as preferred specifications within major machinery platforms. Specialty limit switch manufacturers including Schmersal Group and Bernstein AG compete through superior safety certification depth and application engineering expertise, with Schmersal in particular maintaining a leading position in safety-rated interlocking switches for machinery guarding applications across European and international markets. Japanese manufacturers including OMRON Corporation, Panasonic Corporation, and IDEC Corporation maintain strong positions across Asia Pacific and international markets through reliable product performance, broad actuator type and housing variant availability, and established relationships with Japanese OEM machinery builders that export globally. Connectivity-focused manufacturers including Balluff GmbH, ifm electronic gmbh, and Pepperl+Fuchs SE are gaining competitive traction through IO-Link integrated limit switch solutions that address growing industrial demand for smart sensor capabilities within Industry 4.0 architectures, shifting competitive engagement from price-led to value-led procurement conversations with industrial automation decision-makers.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global limit switches market include Honeywell International Inc. (U.S.), Schneider Electric SE (France), Siemens AG (Germany), Rockwell Automation, Inc. (U.S.), ABB Ltd. (Switzerland), Eaton Corporation plc (Ireland), OMRON Corporation (Japan), Schmersal Group (Germany), Panasonic Corporation (Japan), IDEC Corporation (Japan), Bernstein AG (Germany), Balluff GmbH (Germany), ifm electronic gmbh (Germany), Pepperl+Fuchs SE (Germany), Carlo Gavazzi Holding AG (Switzerland), TE Connectivity Ltd. (Switzerland), Crouzet (France), Azbil Corporation (Japan), and SICK AG (Germany), among others.

The global limit switches market is expected to reach USD 4.1 billion by 2036 from an estimated USD 2.4 billion in 2026, at a CAGR of 5.5% during the forecast period 2026–2036.

In 2026, the standard/general purpose limit switches segment is expected to hold the largest share of this market, driven by its pervasive deployment across the broadest range of industrial automation, conveyor, material handling, and machine tool applications globally.

The safety limit switches segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the compliance requirements introduced by the EU Machinery Regulation (EU) 2023/1230 and the ongoing adoption of ISO 13849-1:2023 and IEC 62061:2021 machinery safety standards across industrial markets globally.

In 2026, the roller lever actuator segment is expected to hold the largest share of this market, reflecting its status as the default actuator configuration across the majority of industrial position detection and end-of-travel sensing applications.

The plunger/push rod actuator segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by growing adoption in precision position detection applications across pharmaceutical, semiconductor, and food processing automation environments.

In 2026, the manufacturing and industrial automation segment is expected to hold the largest share of this market, reflecting the pervasive use of limit switches as foundational position-sensing components across machine tools, conveyors, robotic cells, and automated assembly systems.

The growth of this market is primarily driven by the continued global expansion of industrial automation infrastructure, the tightening of machinery safety and hazardous area regulations including the EU Machinery Regulation (EU) 2023/1230, the rapid global growth of electric vehicle manufacturing capacity and associated automation investment, the adoption of IO-Link enabled smart limit switch configurations compatible with Industry 4.0 architectures, and the ongoing expansion of automotive, pharmaceutical, and food processing manufacturing in Asia Pacific.

Key players in the global limit switches market include Honeywell International Inc. (U.S.), Schneider Electric SE (France), Siemens AG (Germany), Rockwell Automation, Inc. (U.S.), ABB Ltd. (Switzerland), Eaton Corporation plc (Ireland), OMRON Corporation (Japan), Schmersal Group (Germany), Panasonic Corporation (Japan), IDEC Corporation (Japan), Bernstein AG (Germany), Balluff GmbH (Germany), ifm electronic gmbh (Germany), Pepperl+Fuchs SE (Germany), Carlo Gavazzi Holding AG (Switzerland), TE Connectivity Ltd. (Switzerland), Crouzet (France), Azbil Corporation (Japan), and SICK AG (Germany).

Asia Pacific is expected to register the highest growth rate in the global limit switches market during the forecast period 2026–2036, driven by rapid industrial expansion, tightening machinery safety and occupational health regulations, and growing automotive, pharmaceutical, and food processing manufacturing capacity across the region.

1. Introduction

1.1 Market Definition and Scope

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

3.1 Market Overview

3.2 Market Analysis by Product Type

3.3 Market Analysis by Actuator Type

3.4 Market Analysis by End-use Industry

3.5 Market Analysis by Geography

4. Market Dynamics

4.1 Overview

4.2 Drivers

4.2.1 Tightening Global Machinery Safety Regulations Compelling Adoption of Safety-Certified Limit Switch Configurations

4.2.2 Rapid Expansion of Electric Vehicle Manufacturing Capacity Generating High-Volume Demand for Precision Limit Switches

4.2.3 Accelerating Industrial Automation Deployment in Asia Pacific Creating Sustained Demand for Standard and Heavy Duty Limit Switch Installations

4.2.4 Integration of IO-Link and Smart Sensing Capabilities Elevating Limit Switch Value Proposition in Industry 4.0 Manufacturing Architectures

4.3 Restraints

4.3.1 Competitive Displacement of Electromechanical Limit Switches by Non-Contact Inductive and Photoelectric Sensing Technologies in High-Cycle Applications

4.3.2 Price Pressure in Standard Product Segments from Low-Cost Manufacturers Compressing Margins for Established Suppliers

4.4 Opportunities

4.4.1 EU Machinery Regulation (EU) 2023/1230 Compliance Driving Broad-Based Upgrade Cycle for Safety-Rated Limit Switch Installations Across European Industrial Facilities

4.4.2 Expansion of Oil, Gas, and Chemical Processing Infrastructure Sustaining Demand for ATEX and IECEx Certified Explosion-Proof Limit Switch Variants

4.4.3 Growth of Pharmaceutical and Food Processing Automation Driving Adoption of Stainless Steel and Cleanroom-Compatible Limit Switch Configurations

4.5 Challenges

4.5.1 Complexity of Managing Diverse Environmental Rating, Certification, and Housing Variant Requirements Across Globally Distributed Manufacturing Installations

4.5.2 Availability of Cost-Competitive Uncertified Substitutes in Price-Sensitive Markets Undermining Compliance-Grade Procurement in Some Regions

4.6 Porter's Five Forces Analysis

5. Limit Switches Market, by Product Type

5.1 Overview

5.2 Standard/General Purpose Limit Switches

5.2.1 Plastic Housing Standard Limit Switches

5.2.2 Metal Housing Standard Limit Switches

5.2.3 Stainless Steel Housing Limit Switches

5.3 Heavy Duty Limit Switches

5.3.1 Cast Iron Housing Heavy Duty Limit Switches

5.3.2 Die-Cast Zinc/Aluminum Heavy Duty Limit Switches

5.4 Safety Limit Switches

5.4.1 Coded Safety Limit Switches

5.4.2 Non-Coded Safety Limit Switches

5.4.3 Guard Locking Safety Switches

5.5 Explosion-Proof/Hazardous Location Limit Switches

5.5.1 ATEX/IECEx Certified Explosion-Proof Limit Switches

5.5.2 NEC/CEC Certified Hazardous Location Limit Switches

5.6 Miniature Limit Switches

6. Limit Switches Market, by Actuator Type

6.1 Overview

6.2 Roller Lever Actuator

6.3 Adjustable Roller Lever Actuator

6.4 Plunger/Push Rod Actuator

6.5 Wobble Stick/Adjustable Rod Actuator

6.6 Fork Lever Actuator

6.7 Rotary Actuator

7. Limit Switches Market, by End-use Industry

7.1 Overview

7.2 Manufacturing & Industrial Automation

7.2.1 Machine Tool Manufacturing

7.2.2 Conveyor & Material Handling Systems

7.2.3 Robotic & Automated Assembly

7.2.4 Packaging Machinery

7.3 Automotive

7.3.1 Body-in-White & Stamping Operations

7.3.2 Powertrain & Assembly Automation

7.3.3 Electric Vehicle Battery Manufacturing

7.4 Food & Beverage Processing

7.5 Pharmaceutical

7.6 Oil & Gas & Petrochemical

7.7 Mining & Mineral Processing

7.8 Power Generation

7.9 Other End-use Industries

8. Limit Switches Market, by Geography

8.1 Overview

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 Germany

8.3.2 U.K.

8.3.3 France

8.3.4 Italy

8.3.5 Sweden

8.3.6 Netherlands

8.3.7 Poland

8.3.8 Rest of Europe

8.4 Asia Pacific

8.4.1 China

8.4.2 Japan

8.4.3 India

8.4.4 South Korea

8.4.5 Australia

8.4.6 Southeast Asia

8.4.7 Rest of Asia Pacific

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Rest of Latin America

8.6 Middle East and Africa

8.6.1 UAE

8.6.2 Saudi Arabia

8.6.3 South Africa

8.6.4 Rest of Middle East and Africa

9. Competitive Landscape

9.1 Overview

9.2 Key Growth Strategies

9.3 Competitive Benchmarking

9.4 Competitive Dashboard

9.4.1 Industry Leaders

9.4.2 Market Differentiators

9.4.3 Vanguards

9.4.4 Emerging Companies

9.5 Market Share/Ranking Analysis (2025)

10. Company Profiles

10.1 Honeywell International Inc.

10.2 Schneider Electric SE

10.3 Siemens AG

10.4 Rockwell Automation, Inc.

10.5 ABB Ltd.

10.6 Eaton Corporation plc

10.7 OMRON Corporation

10.8 Schmersal Group

10.9 Panasonic Corporation

10.10 IDEC Corporation

10.11 Bernstein AG

10.12 Balluff GmbH

10.13 ifm electronic gmbh

10.14 Pepperl+Fuchs SE

10.15 Carlo Gavazzi Holding AG

10.16 Others

11. Appendix

11.1 Questionnaire

11.2 Available Customization Options

11.3 Related Reports

Published Date: Feb-2026

Published Date: Sep-2024

Published Date: Jan-2024

Published Date: Apr-2026

Subscribe to get the latest industry updates