Resources

About Us

Industrial Switches & Routers Market by Product (Industrial Ethernet Switches [Managed, Unmanaged], Industrial Routers [Wired, Wireless/Cellular]), Form Factor (DIN Rail Mounted, Rack Mounted, Others), End-use — Global Forecast to 2036

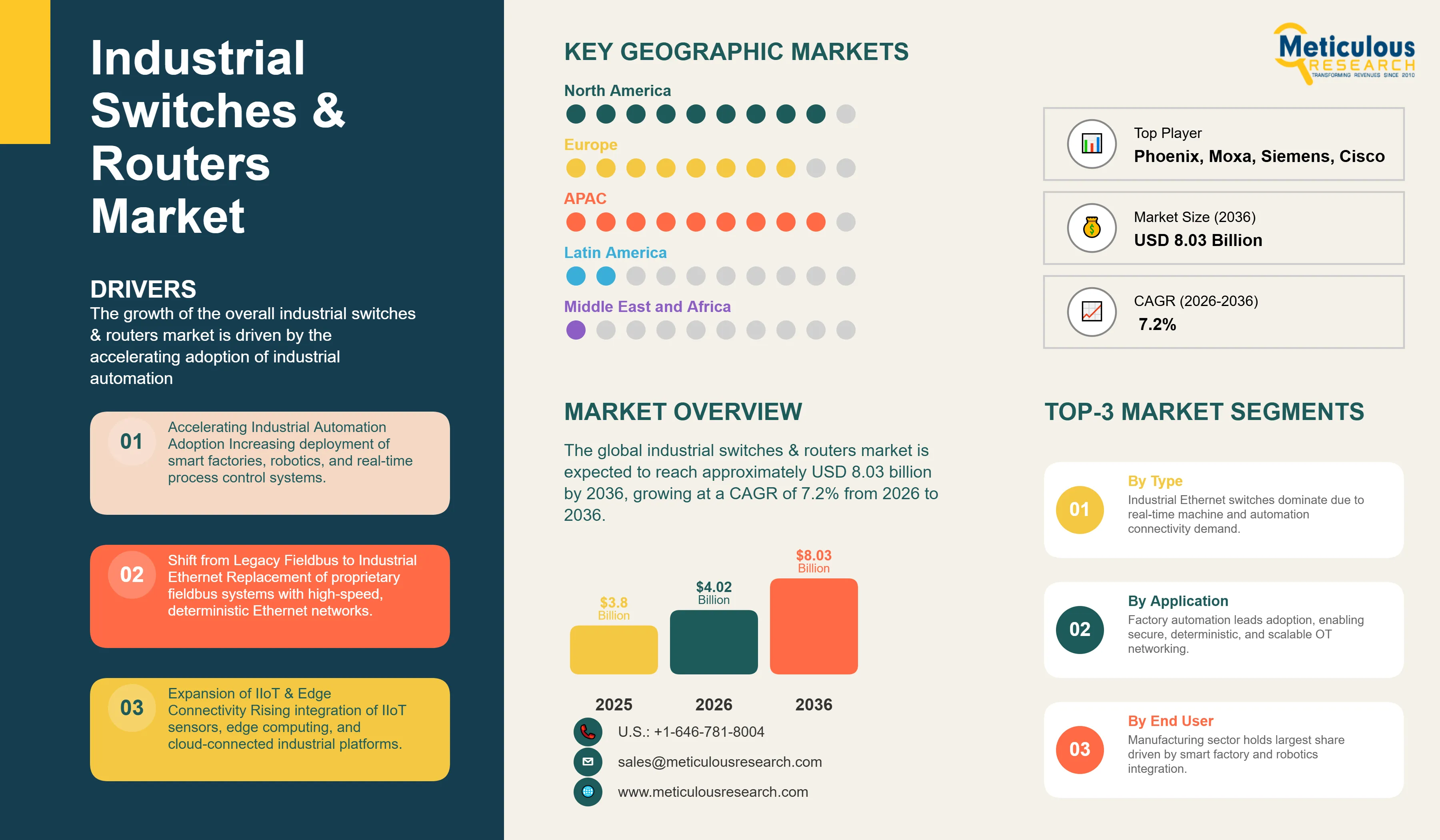

Report ID: MRSE - 1041807 Pages: 278 Feb-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global industrial switches & routers market was valued at USD 3.80 billion in 2025. The market is expected to reach approximately USD 8.03 billion by 2036 from USD 4.02 baillion in 2026, growing at a CAGR of 7.2% from 2026 to 2036. The growth of the overall industrial switches & routers market is driven by the accelerating adoption of industrial automation, the widespread rollout of Industrial Internet of Things (IIoT) platforms, and the urgent need to replace legacy fieldbus infrastructure with high-speed, deterministic Ethernet-based networking solutions. As manufacturers pursue connected factory models and energy companies modernize grid-edge communication, purpose-built switches and routers have become core components of reliable and secure operational technology (OT) networks. The expansion of smart manufacturing initiatives, the push toward Industry 4.0, and the integration of time-sensitive networking (TSN) capabilities continue to fuel consistent growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Industrial switches and routers are purpose-built networking devices designed to meet the demanding requirements of industrial environments, where reliability, operational continuity, and harsh-condition resilience are non-negotiable. Unlike standard commercial networking equipment, industrial switches and routers are engineered to withstand extreme temperatures, vibration, dust, and electromagnetic interference, making them indispensable in factories, substations, offshore platforms, and transportation infrastructure. Industrial Ethernet switches facilitate high-speed, low-latency communication between machines, control systems, and supervisory platforms, while industrial routers manage traffic between separate network segments and enable secure remote connectivity over wired and cellular links.

The market encompasses a broad range of solutions, from simple unmanaged DIN rail switches for small automation cells to fully managed gigabit and multi-gigabit switches with redundancy protocols and built-in cybersecurity features for large-scale process plants. Industrial routers increasingly incorporate 4G LTE and 5G cellular connectivity, SD-WAN capabilities, and integrated firewall and VPN functionality to support remote monitoring, predictive maintenance, and secure IT/OT convergence. The ability to maintain deterministic, always-on communication in mission-critical environments has made these products the networking standard of choice for industries where network downtime translates directly into production losses or safety risks.

The global industrial sector is under considerable pressure to modernize its operational infrastructure, reduce unplanned downtime, and meet ambitious sustainability and productivity targets. This drive has accelerated the replacement of aging fieldbus-based communications with high-performance industrial Ethernet networks, making switches and routers a critical enabler of modern operational architectures. At the same time, the integration of IIoT sensors, edge computing gateways, and cloud-connected analytics platforms is increasing the demand for scalable, secure, and manageable industrial networking infrastructure across all major verticals.

Rise of Managed Industrial Networking and TSN-Enabled Switches for Real-Time Automation

The shift from unmanaged to managed networking infrastructure is fundamentally reshaping the industrial switches & routers market. Managed industrial switches from manufacturers such as Siemens (SCALANCE series), Moxa Technologies, and Cisco Systems (Industrial Catalyst IE series) now offer advanced traffic management, VLAN segmentation, redundancy protocols such as HSR and PRP, and integrated diagnostics that make them essential for smart factory deployments. The integration of Time-Sensitive Networking (TSN) technology is particularly significant, enabling deterministic, low-latency data transmission that supports precision motion control, robotics, and safety systems alongside standard data traffic on a single unified network. These advancements make high-performance industrial network management practical and cost-effective for facilities ranging from small production lines to large, globally distributed manufacturing operations pursuing real-time operational visibility.

Integration of Cellular Connectivity and Cybersecurity in Industrial Routers for Remote OT Environments

The industrial router segment is undergoing a significant transformation as the demand for secure, remote connectivity in distributed operational environments intensifies. Equipment providers such as Moxa, HMS Networks, Robustel, and Digi International are now designing industrial routers that combine 4G LTE and 5G cellular connectivity with embedded firewall, VPN, and intrusion detection capabilities in a single ruggedized device, simplifying deployment in remote field sites, substations, pipelines, and transportation networks. These routers serve as the critical link between operational technology networks and enterprise or cloud platforms, enabling remote diagnostics, over-the-air firmware updates, and real-time process data transmission without compromising network security.

Growing regulatory attention on OT cybersecurity, including the adoption of frameworks such as IEC 62443, is further pushing operators to standardize on routers that provide built-in security features rather than relying on separate appliances. At the same time, the shift toward software-defined WAN (SD-WAN) architectures is enabling centralized network management across geographically dispersed industrial sites, reducing the cost and complexity of network administration. Manufacturers are responding by embedding SD-WAN clients and cloud management platforms into their industrial router portfolios, supporting the move toward unified, policy-driven network governance across enterprise and OT domains.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 8.03 Billion |

|

Market Size in 2026 |

USD 4.02 Billion |

|

Market Size in 2025 |

USD 3.80 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 7.2% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Product, Form Factor, End-use, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Accelerating Industrial Automation and the Shift from Fieldbus to Industrial Ethernet

A key driver of the industrial switches & routers market is the large-scale transition underway across manufacturing, energy, and process industries from legacy fieldbus systems to industrial Ethernet networks. Global demand for real-time machine communication, data-driven process control, and remote operational visibility has created strong and growing incentives for investments in high-reliability industrial networking hardware. The rapid adoption of IIoT platforms, digital twin technologies, and edge computing architectures demands networking infrastructure that can handle significantly higher data volumes, support more connected devices, and deliver deterministic performance that critical automation applications require. It is estimated that by 2030, the proportion of industrial nodes connected via Ethernet-based protocols will exceed 80%, sustaining strong demand for industrial switches and routers as facilities modernize their control and communication infrastructure.

Restraints: High Upfront Costs and Integration Complexity in Legacy Environments

Despite strong growth fundamentals, the market faces meaningful friction from the high initial cost of deploying industrial-grade networking infrastructure, particularly for small and medium-sized manufacturers and facilities in cost-sensitive developing markets. Industrial switches and routers command significant price premiums over commercial networking equipment, reflecting their ruggedized design, extended operational lifespans, and industrial protocol support. Integrating new Ethernet-based networking equipment with existing proprietary control systems, legacy PLCs, and older fieldbus networks introduces additional engineering complexity and project risk, which can slow procurement decisions. These factors require manufacturers and system integrators to clearly demonstrate the long-term operational savings and productivity benefits of modern industrial networking to justify capital expenditure.

Opportunity: Expansion of Smart Grid Infrastructure and Renewable Energy Integration

The global push toward smart grid modernization and the integration of distributed renewable energy sources represents a substantial growth opportunity for the industrial switches & routers market. Utility operators worldwide are investing heavily in substation automation, advanced distribution management systems, and remote monitoring of grid assets, all of which require robust, standards-compliant industrial networking hardware capable of operating reliably in outdoor and harsh electrical environments. Industrial switches compliant with IEC 61850 and routers supporting secure cellular and fiber-based backhaul communications are seeing growing adoption in grid-edge deployments. As renewable energy capacity scales and grid architectures become more distributed, the need for reliable OT networking infrastructure connecting generation assets, storage systems, and control centers will continue to create significant demand across the forecast period.

Why Does the Industrial Ethernet Switches Segment Lead the Market?

The industrial ethernet switches segment accounts for the largest share of the overall industrial switches & routers market in 2026. This is primarily driven by the segment's central role in enabling machine-to-machine communication, real-time process control, and plant-wide data collection within factory and process automation environments. Industrial Ethernet switches serve as the foundational networking layer in practically every modern industrial facility, connecting programmable logic controllers (PLCs), human-machine interfaces (HMIs), sensors, actuators, and supervisory systems into a unified, high-performance communication network. Both managed and unmanaged variants see broad adoption, with managed switches increasingly preferred in complex applications where network visibility, redundancy, and security are essential.

The industrial routers segment is expected to grow at the fastest CAGR during the forecast period, driven by the expanding need for secure WAN connectivity, cellular-based remote access, and IT/OT network bridging in geographically distributed operational environments. The rapid proliferation of IIoT applications and the rising adoption of 5G private networks in manufacturing and energy sectors are accelerating demand for next-generation industrial routers that support high-bandwidth wireless connectivity alongside advanced security and network management capabilities.

How Does the DIN Rail Mounted Segment Dominate?

Based on form factor, the DIN rail mounted segment holds the largest share of the overall market in 2026. This dominance is primarily due to the widespread adoption of DIN rail mounting standards in industrial control panels, electrical cabinets, and automation enclosures across manufacturing, energy, and process industries globally. DIN rail mounted switches and routers offer a compact, space-efficient solution that integrates seamlessly into existing control infrastructure, minimizing installation time and complexity. Leading manufacturers including Phoenix Contact, Moxa, and Weidmüller have built extensive portfolios of DIN rail-form-factor devices spanning unmanaged switches to fully managed gigabit switches with advanced redundancy and cybersecurity features.

The rack mounted segment is expected to witness steady growth during the forecast period, driven by the growing deployment of industrial networking infrastructure in centralized control rooms, data closets within large manufacturing facilities, and substation communication buildings, where higher port density and easier cable management are required.

Why Does the Manufacturing & Industrial Automation Segment Lead the Market?

The manufacturing & industrial automation segment commands the largest share of the global industrial switches & routers market in 2026. This dominance reflects the segment's deep and broad need for reliable, real-time Ethernet communication networks connecting assembly lines, robotic systems, CNC machines, quality inspection platforms, and enterprise resource planning systems. Large-scale manufacturing operations in automotive, electronics, food & beverage, and chemical sectors continue to invest in industrial networking upgrades as they pursue advanced automation, predictive maintenance, and digital twin implementations. Leading networking providers such as Siemens, Rockwell Automation, and Cisco offer tightly integrated industrial switching and routing solutions within their broader automation and control portfolios, reinforcing their strong positions in this segment.

The energy & utilities segment is poised for strong growth through 2036, fueled by the global acceleration of smart grid investments, substation automation programs, and the integration of renewable energy generation into national power networks. Industrial switches and routers certified for power utility communications standards are seeing growing adoption across transmission and distribution infrastructure, with significant projects underway in Europe, North America, and Asia-Pacific.

How is Asia-Pacific Maintaining Dominance in the Global Industrial Switches & Routers Market?

Asia-Pacific holds the largest share of the global industrial switches & routers market in 2026. The region's dominance is primarily attributed to its position as the world's largest manufacturing hub and the rapid pace of industrial modernization underway in China, Japan, South Korea, and India. China alone represents a substantial portion of global industrial networking investment, with government-backed initiatives such as "Made in China 2025" and ongoing investments in smart factory and industrial park infrastructure sustaining high demand for advanced industrial switches and routers. Japan and South Korea contribute significantly through their advanced electronics, automotive, and semiconductor manufacturing sectors, where precision automation and high-density networking requirements drive adoption of cutting-edge industrial networking products. The presence of regional manufacturers such as Moxa, Advantech, and Korenix Technology further strengthens the region's well-developed industrial networking ecosystem.

Which Factors Support North America and Europe Market Growth?

North America and Europe together account for a substantial share of the global industrial switches & routers market. In North America, market growth is primarily driven by the reshoring of manufacturing capacity, significant federal investments in grid modernization and critical infrastructure resilience, and the strong presence of technology leaders including Cisco Systems, Rockwell Automation, Red Lion Controls, and Digi International. The United States has seen particular momentum in smart factory deployments, oil & gas operational technology upgrades, and utility substation automation, all of which demand robust and secure industrial networking solutions.

In Europe, the market benefits from the region's longstanding industrial engineering expertise, strong regulatory focus on OT cybersecurity, and ambitious industrial decarbonization programs. Germany, Sweden, France, and the Netherlands are at the forefront, with leading manufacturers such as Siemens, Phoenix Contact, HMS Networks, and Westermo Network Technologies serving strong domestic demand while also competing globally. Europe's focus on resilient, sustainable industrial operations continues to drive investment in modern networking infrastructure across automotive, chemical, energy, and discrete manufacturing sectors.

Companies such as Cisco Systems, Inc., Siemens AG, Moxa Technologies Inc., and Phoenix Contact GmbH & Co. KG lead the global industrial switches & routers market with comprehensive portfolios of ruggedized, standards-compliant networking hardware for demanding industrial environments. Meanwhile, players including Belden Inc. (Hirschmann), Advantech Co., Ltd., Rockwell Automation, Inc., and HMS Networks AB focus on specialized industrial protocols, modular platform designs, and tightly integrated automation ecosystem solutions targeting manufacturing and process industries. Emerging and specialized manufacturers such as Westermo Network Technologies AB, Red Lion Controls, Digi International Inc., Robustel Technologies Ltd., and Korenix Technology Co., Ltd. (Beijer Electronics Group) are strengthening the market through innovations in cellular router technology, secure remote access, and ruggedized switching solutions for transportation, energy, and harsh-environment applications.

The global industrial switches & routers market is expected to grow from USD 4.02 billion in 2026 to USD 8.03 billion by 2036.

The global industrial switches & routers market is projected to grow at a CAGR of 7.2% from 2026 to 2036.

Industrial ethernet switches are expected to dominate the market in 2026 due to their central role in plant-wide automation networks and real-time machine communication. However, the industrial routers segment is projected to be the fastest-growing segment owing to the rising demand for secure cellular connectivity, SD-WAN-enabled remote access, and IIoT-driven IT/OT network bridging in distributed industrial environments.

IIoT and Industry 4.0 are transforming the industrial switches & routers landscape by demanding higher network throughput, deterministic data delivery, and seamless integration with cloud analytics and edge computing platforms. These requirements are driving adoption of managed switches with advanced redundancy and TSN capabilities, as well as cellular routers with embedded security and remote management functionality, enabling industrial operators to build connected, resilient, and data-driven operational networks.

Asia-Pacific holds the largest share of the global industrial switches & routers market in 2026, primarily driven by the scale of manufacturing activity, rapid smart factory adoption, and strong government support for industrial digitalization in China, Japan, South Korea, and India.

The leading companies include Cisco Systems, Inc., Siemens AG, Moxa Technologies Inc., Phoenix Contact GmbH & Co. KG, Belden Inc. (Hirschmann), Advantech Co., Ltd., Rockwell Automation, Inc., and HMS Networks AB.

Published Date: May-2026

Published Date: Nov-2024

Published Date: Jan-2023

Published Date: Apr-2022

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates