Resources

About Us

Vibration Monitoring Systems Market Size, Share & Trends Analysis, by Offering (Hardware, Software, Services), System Type (Online/Continuous Monitoring Systems, Portable/Handheld Monitoring Systems), End-use Industry, and Geography — Global Opportunity Analysis & Forecast (2026–2036)

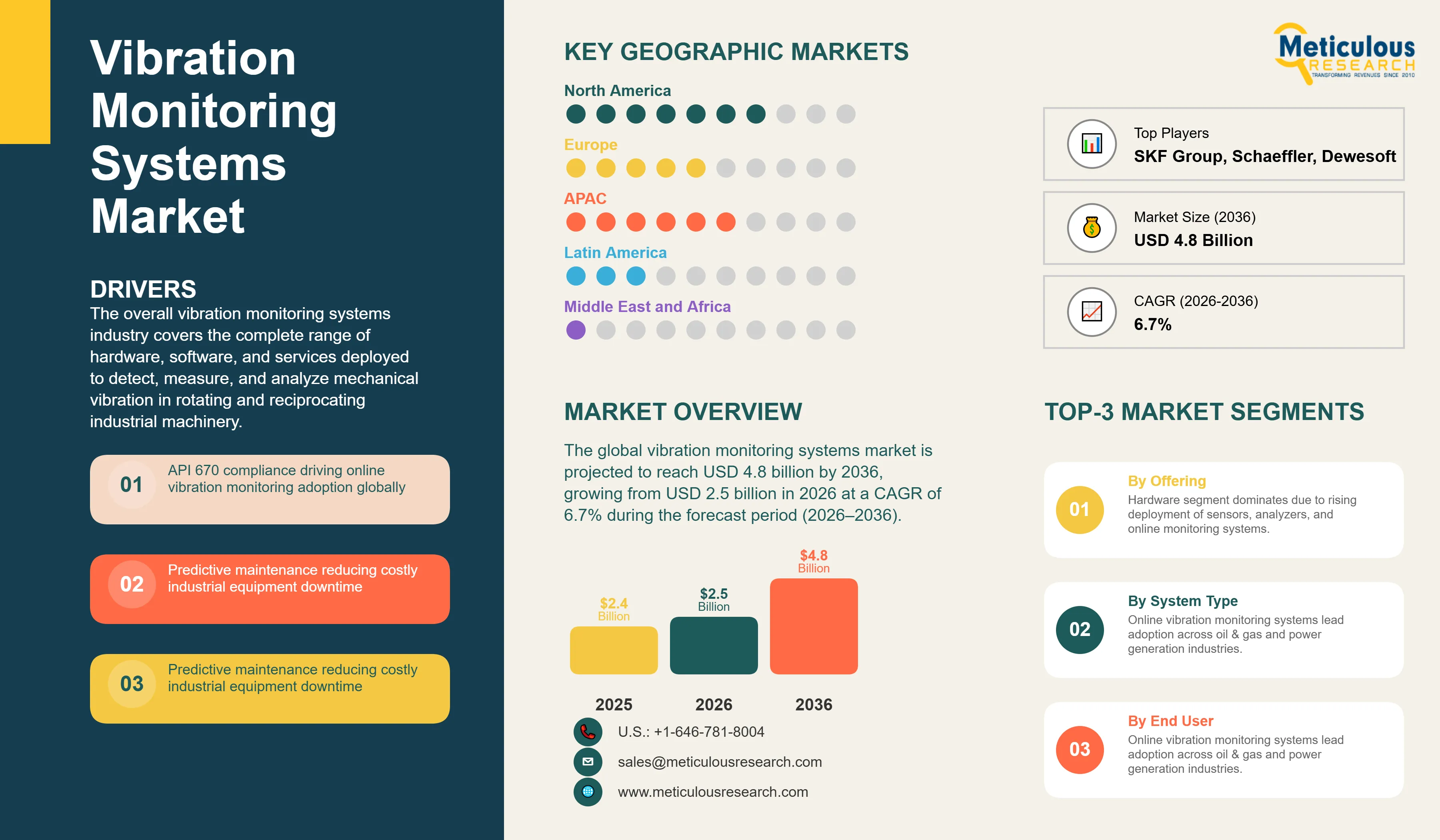

Report ID: MRSE - 1041976 Pages: 278 May-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global vibration monitoring systems market was valued at USD 2.4 billion in 2025. The market is projected to reach USD 4.8 billion by 2036, growing from USD 2.5 billion in 2026 at a CAGR of 6.7% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

The overall vibration monitoring systems industry covers the complete range of hardware, software, and services deployed to detect, measure, and analyze mechanical vibration in rotating and reciprocating industrial machinery. The market encompasses vibration sensors and transducers including accelerometers, velocity sensors, and displacement probes, along with data acquisition systems, signal conditioners, online monitoring units, portable handheld analyzers, and the associated software platforms used for vibration data analysis, machine diagnostics, and asset performance management. These systems are deployed across a broad range of end-use industries including oil and gas, power generation, automotive and transportation, aerospace and defense, chemical and petrochemical processing, food and beverage manufacturing, and mining and metals.

Vibration monitoring systems are central to predictive and condition-based maintenance programs in industrial facilities where the unexpected failure of rotating equipment including compressors, turbines, pumps, fans, gearboxes, and electric motors can trigger costly unplanned production outages, safety incidents, and regulatory compliance exposure. By continuously or periodically measuring vibration signatures at key machinery bearing and structural measurement points, these systems provide maintenance and operations teams with early warning of developing mechanical faults including imbalance, misalignment, rolling element bearing defects, gear mesh anomalies, and structural resonance conditions before they progress to catastrophic failure.

The growth of the vibration monitoring systems market is primarily driven by the non-discretionary adoption requirements embedded in internationally recognized machinery protection and condition monitoring standards. The American Petroleum Institute's API 670 standard, which is widely adopted by operators and engineering contractors in the petroleum, petrochemical, and natural gas industries globally, defines specific requirements for permanently installed online vibration, position, and speed monitoring systems for critical rotating machinery. Compliance with this standard, which governs the design, installation, and performance of machinery protection systems on equipment such as gas compressors, steam turbines, and centrifugal pumps, drives a large and structurally recurring base of capital investment in online vibration monitoring hardware and software. The ISO 20816 series of standards, which replaced ISO 10816 and provides internationally accepted criteria for measuring and evaluating mechanical vibration in machines including industrial fans, pumps, compressors, and gas turbines, reinforces this compliance-led procurement pattern across a broader range of industries and geographies beyond the oil and gas sector.

Beyond mandatory compliance requirements, the business case for vibration monitoring systems has been substantially strengthened by documented operational cost reductions from predictive maintenance programs. According to the U.S. Department of Energy's Operations and Maintenance Best Practices Guide, predictive maintenance programs built around condition monitoring technologies, including vibration analysis, have demonstrated reductions in overall maintenance costs of between 10% and 25%, reductions in unplanned equipment downtime of 35% to 45%, and a 70% to 75% reduction in the frequency of catastrophic machinery breakdowns compared to purely reactive maintenance approaches. These economic performance improvements are increasingly visible in industrial capital allocation decisions, particularly among larger operators where a single unplanned compressor or turbine failure can result in millions of dollars in lost production and emergency repair expenditure.

The integration of industrial IoT connectivity, cloud computing, and advanced analytics into vibration monitoring system platforms is a further and increasingly prominent driver of market growth. Connected vibration sensors feeding real-time measurement data to cloud-hosted analytics platforms are enabling industrial operators to implement continuous, fleet-scale machinery health monitoring without the full capital commitment of traditional hardwired online monitoring systems. Wireless vibration sensors compatible with industrial communication protocols including WirelessHART and ISA100.11a are reducing installation complexity and cost in retrofit applications where wired infrastructure would require significant facility modification. These developments are extending the addressable market for continuous vibration monitoring beyond the large, capital-intensive process industry operators who have historically been the primary customers for online monitoring systems, and into mid-size and smaller industrial facilities where condition monitoring has traditionally been limited to periodic portable measurements.

Despite these strong growth fundamentals, the market faces challenges related to the complexity of integrating new monitoring systems with existing distributed control systems and asset management platforms in industrial facilities, particularly in legacy environments where data protocols and system architectures were not designed for the connectivity requirements of modern IIoT-enabled monitoring deployments. The growing volume of vibration data generated by continuous online monitoring systems at scale also presents operational challenges in data storage, management, and analysis, requiring industrial operators to invest in analytics software and data engineering capabilities that extend beyond the vibration monitoring system itself. Additionally, the increasing connectivity of industrial monitoring infrastructure is expanding the cybersecurity attack surface of critical operational technology environments, creating a new layer of risk management requirements that system manufacturers and end users must address as part of connected monitoring deployments.

The structural expansion of global wind energy capacity represents one of the most commercially significant long-term growth opportunities in the vibration monitoring systems market. Wind turbines depend on continuous vibration monitoring of the main shaft bearing, gearbox input and output bearings, and generator bearings as a core component of turbine asset management practice, with each utility-scale turbine typically requiring between six and ten permanently installed vibration measurement points. The volume of new wind capacity being added globally creates a sustained and growing installed base requirement for wind-specific continuous monitoring systems. In addition, the growing pharmaceutical and food processing manufacturing sectors, where hygiene, contamination control, and equipment reliability requirements mandate systematic machinery health monitoring, are creating a structurally new and expanding demand segment for vibration monitoring systems across both North American and Asia Pacific manufacturing markets.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 4.8 Billion |

|

Market Size in 2026 |

USD 2.5 Billion |

|

Market Size in 2025 |

USD 2.4 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 6.7% |

|

Dominating Offering |

Hardware |

|

Fastest Growing Offering |

Software |

|

Dominating System Type |

Online/Continuous Vibration Monitoring Systems |

|

Fastest Growing System Type |

Portable/Handheld Vibration Monitoring Systems |

|

Dominating End-use Industry |

Oil & Gas |

|

Fastest Growing End-use Industry |

Power Generation |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

API 670 and ISO 20816 Compliance Requirements Establishing Mandatory Continuous Vibration Monitoring as Standard Practice in Critical Process Industries

The widespread global adoption of API 670 and the ISO 20816 series of vibration measurement and evaluation standards has established continuous online vibration monitoring as a non-negotiable operational requirement for critical rotating equipment across the oil and gas, petrochemical, power generation, and chemical processing industries, creating a structurally recurring and growing base of compliance-driven capital investment in vibration monitoring infrastructure.

API 670, now in its fifth edition, defines the specific design, installation, and performance requirements for machinery protection systems covering radial shaft vibration, axial position, speed, and phase reference measurements on critical rotating machines including centrifugal and reciprocating compressors, steam turbines, expanders, and large centrifugal pumps. The scope of this standard is broadly applied across new plant construction and major equipment upgrade projects globally, and engineering procurement and construction contractors working in the oil, gas, and petrochemical sectors treat API 670 compliance as a baseline specification requirement. The ISO 20816 series, which has progressively replaced ISO 10816 across its various parts covering industrial fans, pumps, compressors, steam turbines, and coupled industrial machines since 2016, provides internationally recognized vibration severity and evaluation criteria that are referenced in machinery procurement specifications, insurance assessments, and operational maintenance protocols across European and Asian industrial markets where ISO standards carry primary normative weight.

Beyond these machinery-specific standards, the European Union's Machinery Directive and its successor, the EU Machinery Regulation (EU) 2023/1230, which takes full effect in January 2027, reinforces the engineering obligation for documented machinery health monitoring as part of safe machine operation throughout the product lifecycle. This regulatory development is prompting European industrial facilities and equipment original equipment manufacturers to more formally document vibration monitoring requirements in machine safety design and operational maintenance frameworks, creating incremental procurement activity for both online and portable monitoring systems. In the United States, OSHA's Process Safety Management (PSM) standard under 29 CFR 1910.119, which governs the management of highly hazardous chemicals in process industry facilities, includes mechanical integrity requirements that effectively support systematic condition monitoring of rotating equipment as part of documented safety management practice. Taken together, these intersecting standards and regulatory frameworks are converting vibration monitoring system investment from an operationally discretionary capital expenditure into a compliance-linked requirement, substantially widening the addressable market and providing procurement justification across a broader base of industrial operators.

IIoT Integration and Cloud-Based Asset Performance Management Platforms Reshaping the Commercial Model and Expanding the Addressable Market for Vibration Monitoring Systems

The convergence of wireless sensing technology, industrial IoT connectivity, and cloud-hosted analytics platforms is fundamentally transforming both the economics and the operational model of vibration monitoring system deployment, expanding the addressable market beyond the large capital-intensive process industry operators that have historically represented the core customer base for continuously installed monitoring infrastructure.

Traditionally, online vibration monitoring systems required dedicated wired signal cabling from each sensor to centralized monitoring hardware, a installation approach that involved significant civil and electrical works, particularly in retrofit applications, and that effectively limited the commercial viability of continuous monitoring to critical machinery assets where the capital investment was clearly justified by the failure consequence severity. The availability of industrial-grade wireless vibration sensors, such as the SKF Enlight Collect IMx-1, the Schaeffler OPTIME wireless sensor system, and Emerson's AMS Wireless Vibration Sensor, which use WirelessHART, Bluetooth, or proprietary radio protocols to transmit measurement data without dedicated wired infrastructure, has dramatically reduced the installation cost and complexity of deploying continuous monitoring on secondary and balance-of-plant equipment that was previously monitored only during periodic manual rounds.

Cloud-based asset performance management platforms built on top of this connected sensor infrastructure are creating a further commercial shift by enabling industrial operators to access fleet-level vibration analytics, automated fault detection, and remaining useful life estimation through software-as-a-service subscription models that have substantially lower upfront cost than traditional enterprise software deployments. Platforms such as Emerson's AMS Machinery Manager, Baker Hughes System 1, and SKF Enlight Asset Management are embedding machine learning-based diagnostic algorithms capable of automatically classifying bearing defect signatures, gear mesh anomalies, and rotor imbalance conditions, reducing the dependence on specialist vibration analysts and making condition monitoring programs practically viable for facilities and organizations that lack dedicated reliability engineering resources. According to the U.S. Department of Energy's Operations and Maintenance Best Practices Guide, predictive maintenance programs supported by condition monitoring technologies can reduce total maintenance costs by 10% to 25% and eliminate up to 70% to 75% of unplanned equipment breakdowns, a documented return on investment that is increasingly supporting capital allocation decisions in favor of connected monitoring deployments across a broadening spectrum of industrial operators. The net effect of these developments is a market that is growing in total revenue, expanding in addressable customer base, and shifting its commercial center of gravity from hardware-centric transactional equipment sales toward longer-term recurring software and service engagement models.

Wind Energy Expansion and Renewable Power Generation Growth Creating Structurally New and Sustained Demand for Continuous Vibration Monitoring Systems

The accelerating global expansion of wind energy capacity is establishing wind turbine condition monitoring as one of the fastest growing and most commercially significant application segments within the vibration monitoring systems market, creating a new and structurally recurring demand base that is expected to grow substantially over the forecast period as annual wind energy additions continue at scale across Asia Pacific, Europe, and North America.

Wind turbines are among the most demanding applications for continuous vibration monitoring because the main drivetrain components, including the main shaft bearing, gearbox input shaft bearing, intermediate shaft bearings, high-speed shaft bearing, generator drive-end and non-drive-end bearings, are subject to complex, variable loading conditions driven by fluctuating wind speeds and turbulent airflow. Gearbox failures are consistently identified as the highest-cost cause of unplanned turbine downtime, with repair and replacement work on an offshore turbine gearbox requiring specialized marine logistics that can take weeks and cost several hundred thousand dollars per incident. A standard utility-scale wind turbine requires between six and ten permanently installed vibration measurement points covering the complete drivetrain bearing set, making each new turbine installation a direct and predictable requirement for a continuous vibration monitoring system.

According to the Global Wind Energy Council's Global Wind Report 2024, the world added approximately 117 GW of new wind generation capacity in 2023, bringing cumulative global installed capacity to approximately 1,017 GW by the end of that year. With annual capacity additions expected to remain at or above this level through the mid-2030s driven by energy transition commitments across major economies, the volume of new turbine installations requiring integrated condition monitoring systems represents a compelling and durable source of market demand for vibration monitoring hardware and software suppliers with wind-specific product capabilities. The emergence of offshore wind as a rapidly growing share of new installations further amplifies the economic value of continuous monitoring, as the remote access constraints and high marine logistics costs of offshore operations make unplanned maintenance interventions significantly more expensive than in onshore environments, strengthening the return on investment case for continuous monitoring systems that can extend service intervals and prevent unplanned failures. Leading manufacturers including SKF, Schaeffler AG, and Emerson Electric Co. have each developed dedicated product lines and application expertise targeting wind turbine condition monitoring, reflecting the scale of the commercial opportunity in this application segment. Outside of wind energy, the ongoing construction of combined cycle gas turbine power plants and the life extension and refurbishment programs at nuclear and large hydropower facilities are creating additional demand for high-reliability continuous vibration monitoring systems in power generation applications.

By Offering: In 2026, the Hardware Segment to Dominate the Global Vibration Monitoring Systems Market

Based on offering, the vibration monitoring systems industry is segmented into hardware, software, and services. In 2026, the hardware segment is expected to account for the largest share of this market. The leading position of this segment reflects the fundamental requirement for a physical sensing and data acquisition infrastructure at every machinery asset that is brought under condition monitoring coverage. Every monitored bearing or structural location in an industrial facility requires a dedicated sensor, and large rotating equipment in oil and gas and power generation facilities typically carries multiple measurement points per machine. The hardware requirement scales directly with the volume of monitored assets, and the combination of accelerometers, velocity sensors, displacement probes, data acquisition systems, and online monitoring units across large industrial plant installations represents a significant capital expenditure at the facility level. Major hardware suppliers including Emerson Electric Co., SKF Group, HBK (Hottinger Brüel & Kjær), Baker Hughes Company's Bently Nevada product line, PCB Piezotronics, Inc., and Kistler Group maintain dominant positions in this segment through broad sensor portfolios, strong application engineering capabilities, and deep integration with the monitoring software platforms that complete the system value proposition.

However, the software segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the transition from one-time perpetual software licensing toward cloud-hosted subscription-based analytics platforms that generate recurring revenue, the growing integration of machine learning and artificial intelligence-based fault detection and diagnostic capabilities into vibration analysis software, and the expanding adoption of enterprise-scale asset performance management platforms that consolidate vibration data alongside thermographic, oil analysis, and process data streams into unified predictive maintenance intelligence applications. As more industrial operators seek to extract actionable machine health insights from the increasing volumes of continuous vibration data generated by expanding sensor networks, the commercial value of the software layer in vibration monitoring system deployments is growing faster than the underlying hardware base, and system providers that can deliver compelling analytics capabilities are gaining pricing power and customer retention advantages over hardware-only competitors.

By System Type: In 2026, the Online/Continuous Vibration Monitoring Systems Segment to Account for the Largest Share

Based on system type, the vibration monitoring systems industry is segmented into online and continuous vibration monitoring systems and portable and handheld vibration monitoring systems. In 2026, the online and continuous vibration monitoring systems segment is expected to account for the largest share of this market. The dominant position of this segment is driven by the mandatory deployment of permanently installed continuous monitoring infrastructure on critical rotating machinery under API 670 and ISO 20816 standards across oil and gas, power generation, and chemical processing facilities, where the consequence severity of an undetected developing fault on a critical compressor, turbine, or pump justifies the full capital investment of dedicated online monitoring hardware, signal conditioning, and real-time protection logic. Online systems command significantly higher per-deployment revenue than portable alternatives because they encompass not only the sensor hardware but also dedicated online monitoring units, signal cabling or wireless network infrastructure, and enterprise-licensed analysis and asset management software integrated with plant control systems.

However, the portable and handheld vibration monitoring systems segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the broadening adoption of route-based portable condition monitoring programs at small and mid-size industrial facilities that are implementing structured maintenance practices for the first time, the growing regulatory and insurance pressure for documented periodic vibration assessments on secondary and balance-of-plant rotating equipment that does not carry permanently installed monitoring, and the availability of increasingly capable portable analyzers with embedded diagnostic software, wireless data upload, and cloud synchronization features that are reducing the skill threshold and workflow friction associated with running a cost-effective route-based monitoring program.

By End-use Industry: In 2026, the Oil & Gas Segment to Hold the Largest Share

Based on end-use industry, the vibration monitoring systems industry is segmented into oil and gas, power generation, automotive and transportation, aerospace and defense, chemical and petrochemical, food and beverage, mining and metals, and other end-use industries. In 2026, the oil and gas segment is expected to account for the largest share of this market, reflecting the unmatched density of high-value, critical rotating equipment in upstream, midstream, and downstream oil and gas facilities globally and the industry's decades-long adoption of API 670-compliant machinery protection as a fundamental plant engineering standard. Gas compressor trains, steam and gas turbines, centrifugal pumps, and expanders in refinery, liquefied natural gas, and pipeline applications each carry multiple permanently installed vibration monitoring channels, and the capital value of the rotating equipment being protected, combined with the production and safety consequences of an undetected failure, sustains the highest per-facility investment levels in vibration monitoring systems across all end-use segments. The continued expansion of LNG export infrastructure in North America, the Middle East, and Australia, alongside the ongoing operational demands of the global refining and petrochemical processing base, ensures that oil and gas will remain the single largest end-use market for vibration monitoring systems throughout the forecast period.

However, the power generation segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven predominantly by the structural expansion of global wind energy capacity, where each new turbine installation requires a permanently installed drivetrain condition monitoring system covering the main bearing, gearbox bearing set, and generator bearings as a standard operational requirement. The continued commissioning of combined cycle gas turbine power plants across Asia and the Middle East, the life extension and asset optimization programs underway at nuclear and large conventional thermal power stations globally, and the rapid growth of offshore wind with its elevated condition monitoring value proposition are collectively creating a broad and durable growth demand base across the power generation segment. Beyond wind, the integration of vibration monitoring data with power plant SCADA and digital twin platforms is further expanding the functional scope and commercial value of monitoring systems in this sector.

Based on geography, the overall vibration monitoring systems market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of this market. This position is supported by the world's most extensive adoption of API 670-compliant machinery protection infrastructure in the U.S. oil and gas and petrochemical processing sectors, a large and aging installed base of continuous monitoring systems across refineries, chemical plants, and power facilities that generates a steady flow of technology refresh and aftermarket demand, and the presence of leading system manufacturers and analytics platform providers including Emerson Electric Co., Baker Hughes Company, Fluke Corporation, PCB Piezotronics, Inc., and Wilcoxon Sensing Technologies that maintain strong customer relationships and deep application engineering capabilities across North American industrial markets. The United States' extensive and maturing wind energy fleet is also generating growing demand for turbine condition monitoring system upgrades and integration services as operators seek to maximize asset performance from an expanding installed base of wind generation capacity.

However, the Asia Pacific vibration monitoring systems market is expected to grow at the fastest rate from 2026 to 2036. The rapid growth of this market is driven by the massive expansion of petrochemical, steel, cement, automotive parts, and electronics manufacturing capacity across China, India, South Korea, Japan, and Southeast Asia, all of which operate rotating machinery requiring structured condition monitoring programs. China's industrial modernization drive and its ambitious renewable energy expansion, which is making it the world's largest installer of new wind energy capacity on an annual basis, are creating simultaneous demand for both plant-level rotating equipment monitoring and large-scale wind turbine condition monitoring system installations. India's National Clean Air Programme, manufacturing sector growth under government industrial promotion initiatives, and expanding pharmaceutical and food processing capacity are collectively strengthening demand for vibration monitoring systems across multiple industrial segments. In Japan and South Korea, the advanced semiconductor, automotive, and electronics manufacturing sectors are driving adoption of precision vibration monitoring for highly sensitive production equipment where even minor machinery anomalies can affect product quality, creating a premium application segment for high-accuracy monitoring hardware and analytics software.

Europe is a mature and well-established market for vibration monitoring systems, supported by a regulatory environment that includes the EU Machinery Directive's mechanical integrity requirements, ISO 20816 adoption as the standard specification basis for rotating equipment procurement and operation, and national occupational health and safety frameworks across major industrial economies that reinforce systematic machinery condition monitoring practice. European manufacturers including Schaeffler AG, HBK (Hottinger Brüel & Kjær), Kistler Group, IMC Test & Measurement GmbH, and Dewesoft d.o.o. maintain strong competitive positions in their home region through deep application engineering expertise, close customer collaboration in industrial and automotive testing applications, and technology differentiation in high-precision sensing hardware and advanced signal analysis software. Europe's mature wind energy fleet and the accelerating growth of offshore wind development in the North Sea and Baltic are additional demand drivers for continuous turbine monitoring systems and associated remote diagnostics services across the region.

The global vibration monitoring systems market is characterized by a blend of large, diversified industrial technology companies competing with specialist condition monitoring and precision measurement suppliers, with competitive differentiation primarily determined by sensor accuracy and reliability, the analytical capability and integration flexibility of associated software platforms, the ability to support API 670 and ISO 20816 compliance requirements in specific end-use applications, and the depth of aftermarket calibration, service, and technical support capabilities.

Large diversified industrial technology companies such as Emerson Electric Co. and Honeywell International Inc. compete through comprehensive portfolios spanning sensors, online monitoring hardware, portable instruments, and enterprise asset management software, supported by global distribution and service networks that serve multinational industrial operators across multiple facilities simultaneously. Baker Hughes Company, through its Bently Nevada machinery protection and System 1 condition monitoring software business, holds a particularly strong position in the oil and gas and power generation segments where API 670 compliance is a primary procurement driver. SKF Group competes across the full spectrum of the market from individual bearing sensors to complete online monitoring systems and cloud-based fleet analytics, leveraging its deep expertise in rotating machinery tribology and bearing diagnostics as a core differentiator in condition monitoring applications. Parker Hannifin Corporation has significantly expanded its vibration monitoring capabilities through the acquisition of Meggitt PLC, strengthening its position in aerospace, defense, and high-value industrial monitoring applications requiring specialized high-temperature and high-frequency sensing capability.

Specialist manufacturers including Schaeffler AG, Kistler Group, HBK (Hottinger Brüel & Kjær), and PCB Piezotronics, Inc. compete on the basis of measurement precision, sensor technology leadership, and application-specific expertise in demanding environments including turbomachinery, wind energy, automotive testing, and structural dynamics. Fluke Corporation, which expanded its industrial condition monitoring portfolio through the acquisition of PRUFTECHNIK's alignment and condition monitoring business, is strengthening its position in route-based portable monitoring and precision alignment markets. Dewesoft d.o.o. and IMC Test & Measurement GmbH serve precision testing and monitoring applications across industrial, automotive, and aerospace sectors with advanced data acquisition hardware and signal analysis software.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global vibration monitoring systems market include Emerson Electric Co. (U.S.), SKF Group (Sweden), Honeywell International Inc. (U.S.), Parker Hannifin Corporation (U.S.), Baker Hughes Company (U.S.), HBK (Hottinger Brüel & Kjær) (Denmark), Schaeffler AG (Germany), PCB Piezotronics, Inc. (U.S.), Rockwell Automation, Inc. (U.S.), Fluke Corporation (U.S.), Kistler Group (Switzerland), Wilcoxon Sensing Technologies (U.S.), Analog Devices, Inc. (U.S.), Dewesoft d.o.o. (Slovenia), and IMC Test & Measurement GmbH (Germany), among others.

The global vibration monitoring systems market is expected to reach USD 4.8 billion by 2036 from an estimated USD 2.5 billion in 2026, at a CAGR of 6.7% during the forecast period 2026–2036.

In 2026, the hardware segment is expected to hold the largest share of this market, driven by the fundamental requirement for physical sensing and data acquisition infrastructure at every machinery asset brought under condition monitoring coverage across oil and gas, power generation, and industrial manufacturing facilities.

The software segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the accelerating transition toward cloud-based subscription analytics platforms, the integration of machine learning-based fault diagnostics into asset performance management applications, and the growing commercial value of recurring software and analytics services within vibration monitoring system deployments.

In 2026, the online and continuous vibration monitoring systems segment is expected to hold the largest share of this market, driven by the mandatory deployment of permanently installed monitoring infrastructure for critical rotating machinery under API 670 and ISO 20816 standards across oil and gas, power generation, and chemical processing industries.

In 2026, the oil and gas segment is expected to hold the largest share of this market, reflecting the high density of API 670-regulated critical rotating equipment in upstream, midstream, and downstream operations and the severe operational and safety consequences associated with undetected machinery failure in process industry environments.

The power generation segment is expected to register the highest CAGR during the forecast period, driven by the structural expansion of global wind energy capacity requiring continuous drivetrain vibration monitoring, combined with ongoing demand from combined cycle gas turbine construction and nuclear and conventional thermal power plant life extension programs.

The growth of this market is primarily driven by mandatory compliance requirements under API 670 and ISO 20816 standards in process industry applications, the growing adoption of predictive and condition-based maintenance programs supported by documented operational cost reduction benefits, the integration of IIoT connectivity and cloud analytics into vibration monitoring platforms, the structural expansion of global wind energy capacity, and the expanding adoption of cost-effective wireless monitoring solutions among small and mid-size industrial facilities previously underserved by conventional wired monitoring infrastructure.

Key players in the global vibration monitoring systems market include Emerson Electric Co. (U.S.), SKF Group (Sweden), Honeywell International Inc. (U.S.), Parker Hannifin Corporation (U.S.), Baker Hughes Company (U.S.), HBK (Hottinger Brüel & Kjær) (Denmark), Schaeffler AG (Germany), PCB Piezotronics, Inc. (U.S.), Rockwell Automation, Inc. (U.S.), Fluke Corporation (U.S.), Kistler Group (Switzerland), Wilcoxon Sensing Technologies (U.S.), Analog Devices, Inc. (U.S.), Dewesoft d.o.o. (Slovenia), and IMC Test & Measurement GmbH (Germany).

Asia Pacific is expected to register the highest growth rate in the global vibration monitoring systems market during the forecast period 2026–2036, driven by rapid industrial and manufacturing capacity expansion, accelerating adoption of condition-based maintenance practices, the world's highest rate of annual wind energy capacity additions, and growing demand for precision monitoring in semiconductor, automotive, and pharmaceutical manufacturing across the region.

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates