Resources

About Us

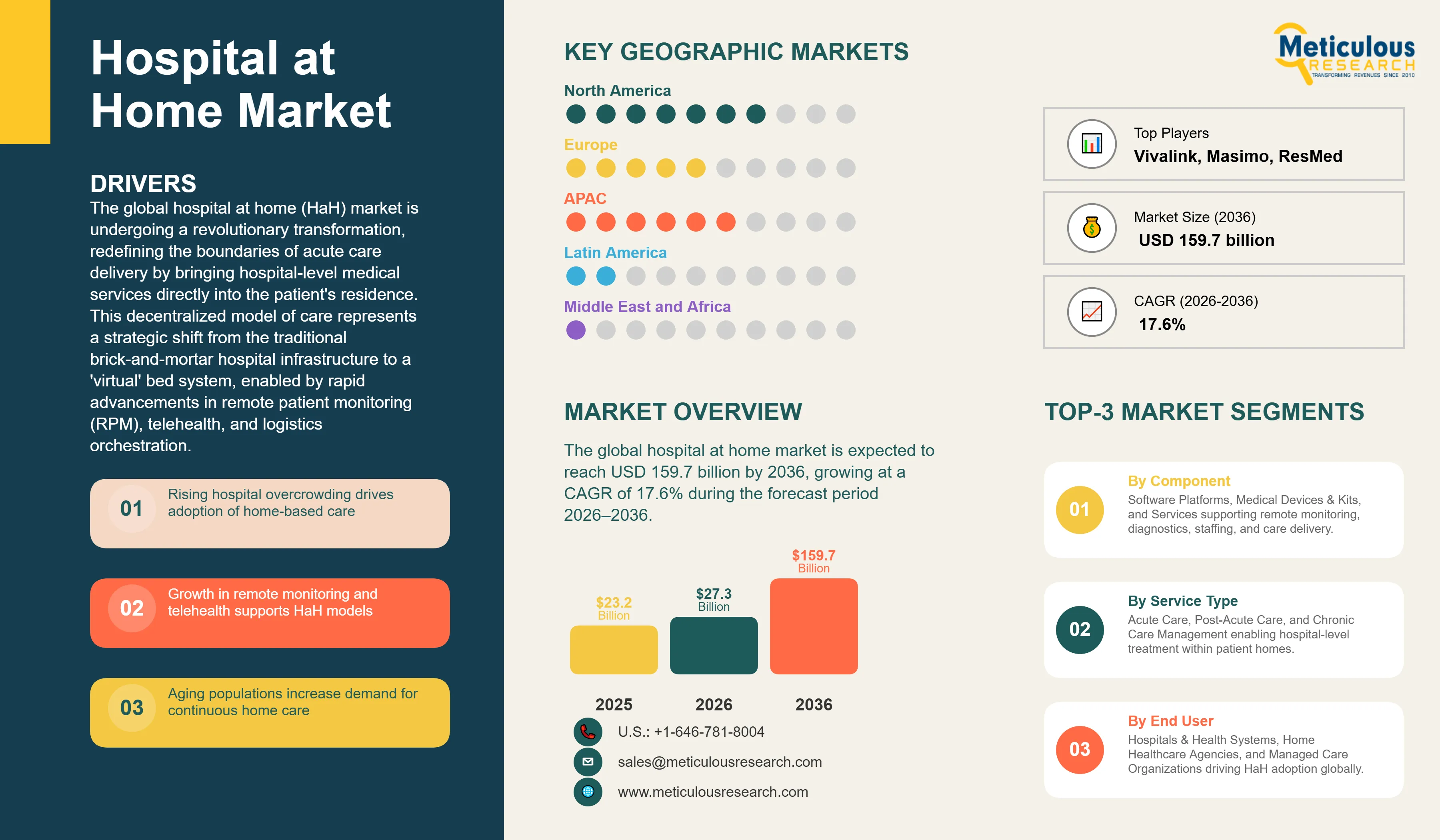

The global hospital at home market is valued at USD 27.3 billion in 2026. This market is expected to reach USD 159.7 billion by 2036, growing at a CAGR of 17.6% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global hospital at home (HaH) market is undergoing a revolutionary transformation, redefining the boundaries of acute care delivery by bringing hospital-level medical services directly into the patient's residence. This decentralized model of care represents a strategic shift from the traditional brick-and-mortar hospital infrastructure to a 'virtual' bed system, enabled by rapid advancements in remote patient monitoring (RPM), telehealth, and logistics orchestration. The market's growth is primarily fueled by the global imperative to address hospital overcrowding, rising inpatient costs, and the increasing preference of patients for home-based care. By leveraging high-acuity monitoring technology and coordinated clinical staffing, HaH programs can safely treat conditions such as heart failure, pneumonia, and cellulitis in the comfort of the home, often with superior clinical outcomes.

The efficacy of the hospital-at-home (HaH) model is supported by a growing body of clinical evidence and regulatory momentum. Studies indicate that appropriately selected patients enrolled in HaH programs experience significantly lower or comparable mortality rates and reduced hospital readmissions, typically in the range of 10% to 25%, compared to conventional inpatient care. In addition, multiple program evaluations have demonstrated cost savings of approximately 15% to 30% per acute care episode, driven by reduced facility utilization and optimized resource allocation. In the United States, the CMS Acute Hospital Care at Home (AHCaH) waiver has played a critical enabling role, with more than 200 hospitals across over 30 states participating in approved programs as of the mid-2020s, accelerating institutional adoption of home-based acute care delivery. This regulatory support, combined with demographic aging trends and the rising burden of chronic diseases, is positioning the HaH model as an increasingly integral component of modern healthcare delivery systems.

The HaH ecosystem is characterized by complex logistical and technological integration. Successful implementation requires a seamless coordination of RPM software platforms, medical device kits, clinical staffing, and supply chain logistics for the delivery of oxygen, infusion therapy, and laboratory services. The market is witnessing a high level of strategic activity, with major health systems forming partnerships with specialized HaH technology and service providers. Additionally, the integration of artificial intelligence for predictive analytics is enhancing patient safety by allowing clinicians to identify subtle signs of deterioration before they escalate into an emergency. As the logistical hurdles are overcome and reimbursement frameworks become more standardized, the global HaH market is poised for sustained, high-velocity growth over the next decade.

Geographically, North America leads the global HaH market, accounting for a significant share of the total revenue in 2026. This dominance is driven by the advanced healthcare infrastructure in the United States and the strong regulatory support for home-based acute care models. However, the European market is also highly developed, with countries like the UK and Spain having long-established 'hospital in the home' programs. The Asia-Pacific region is projected to witness the fastest growth, as governments invest in digital health to manage the healthcare needs of rapidly aging populations in Japan, China, and Australia. With global healthcare spending shifting toward value-based care, the hospital at home market is set to become a cornerstone of the future healthcare landscape.

The primary driver for the hospital at home market is the critical need to manage hospital capacity and reduce the high overhead costs associated with inpatient care. As health systems face increasing overcrowding and staff shortages, the ability to 'create' virtual beds in the home is a major strategic advantage. Furthermore, rapid advancements in remote patient monitoring and telehealth have made high-acuity care at home both safe and feasible. The growing global aging population and the rising prevalence of chronic conditions that require frequent hospitalization are also significant catalysts for market adoption.

Dependency on regulatory waivers and reimbursement uncertainties remains a significant restraint for the long-term sustainability of HaH programs. The logistical complexity of coordinating in-home nursing, physician visits, and the timely delivery of medical equipment in a decentralized environment is also a major hurdle. Furthermore, there is a degree of clinician resistance and the need for significant change management to shift traditional hospital-based workflows to the home. Ensuring patient eligibility and maintaining safety standards in a non-controlled home environment also presents persistent challenges.

Significant opportunities exist in the expansion of HaH programs into rural and underserved areas, where access to traditional hospital facilities is limited. The integration of AI-driven predictive analytics into RPM platforms offers a major opportunity to enhance patient safety by predicting clinical deterioration before it requires a re-hospitalization. Additionally, the development of specialized home-based infusion and diagnostic technologies presents a growth path for medical device manufacturers. The expansion of HaH models into new therapeutic areas, such as oncology and complex post-surgical care, also offers high potential for market expansion.

A critical challenge for HaH providers is the integration of diverse technological platforms with existing hospital EHR systems to ensure seamless data flow and clinical coordination. Maintaining a high level of patient engagement and adherence to monitoring protocols in the home environment is also a persistent challenge. Furthermore, as the market scales, ensuring a consistent quality of care across a geographically dispersed patient population requires robust quality assurance frameworks. Addressing the digital divide and ensuring that patients with limited technological literacy or internet access can participate in HaH programs is also a major social and clinical challenge.

The integration of AI and machine learning into remote patient monitoring (RPM) is a key enabler of hospital-at-home (HaH) scalability. AI-enabled systems can continuously analyze multi-parameter physiological data (heart rate, SpO₂, respiration, temperature) and detect early clinical deterioration, reducing reliance on episodic hospital assessments. According to the U.S. Centers for Medicare & Medicaid Services (CMS), hospital-at-home programs supported by digital monitoring infrastructure have demonstrated comparable outcomes to inpatient care for over 60 acute conditions, reinforcing the safety of remote acuity management when supported by continuous monitoring frameworks.

Industry evidence from health systems such as the NHS England virtual ward program shows that predictive monitoring tools can reduce avoidable hospital escalation by 20–30% in high-risk chronic and post-acute cohorts, primarily through early intervention triggers. Similarly, peer-reviewed studies in digital health indicate that AI-driven alert systems can improve deterioration detection time by up to 40–60% compared to conventional vital-sign threshold monitoring, enabling earlier clinical response. This predictive, data-driven care model is significantly improving the safety envelope of HaH programs, allowing healthcare providers to extend hospital-level care to higher-acuity patients while reducing avoidable admissions and clinical risk.

A key driver of Hospital-at-Home (HaH) expansion is the increasing formation of strategic partnerships between health systems and specialized technology, logistics, and virtual care providers. These collaborations enable rapid deployment of acute home care models without requiring hospitals to independently build remote monitoring, command center, and care orchestration infrastructure.

This model is strongly validated by adoption trends under the U.S. Centers for Medicare & Medicaid Services (CMS) Acute Hospital Care at Home (AHCaH) waiver, where over 200+ hospitals across 30+ states have partnered with external enablers such as RPM, telehealth, and logistics platforms to operationalize HaH programs. Similarly, the NHS England Virtual Ward program has demonstrated that system–technology partnerships can support large-scale deployment, enabling care delivery for tens of thousands of patients monthly across integrated virtual ward networks.

Industry evidence also shows that partnership-led HaH models can reduce time-to-deployment significantly, with health systems reporting program launch acceleration of 6–12 months compared to in-house builds, while improving operational scalability through outsourced care coordination, staffing, and device logistics. This shift is driving the emergence of integrated “virtual hospital” ecosystems, where hospitals, payers, and technology vendors operate as unified care networks embedded within the broader healthcare continuum.

Based on component, the market is segmented into Software Platforms, Medical Devices & Kits, and Services. In 2026, the Services segment is expected to hold the largest share of the market. Clinical staffing, logistical coordination, and technical support represent the highest recurring costs in the HaH model. The need for specialized nursing care and the physical delivery of medical supplies to the home drive the dominance of this segment.

The Software Platforms segment is projected to register the fastest CAGR during the forecast period. This growth is fueled by the increasing adoption of AI-driven monitoring dashboards and the integration of logistics orchestration software that can manage complex decentralized workflows in real-time.

Based on indication, the market is segmented into Cardiovascular Diseases, Respiratory Diseases, Infectious Diseases, Neurological Disorders, and others. In 2026, the Cardiovascular Diseases segment is expected to hold the largest share of the market. Conditions like congestive heart failure are high-volume drivers of hospital readmissions and are ideally suited for home-based management with high-acuity monitoring.

The Infectious Diseases segment is projected to witness the fastest growth during the forecast period. The standardization of protocols for in-home intravenous antibiotic therapy for conditions like cellulitis and sepsis is driving increased adoption of the HaH model for acute infectious cases.

North America is expected to hold the largest share of the global hospital at home market in 2026, driven by the strong regulatory support of the CMS waiver program and the high concentration of HaH technology vendors in the United States. The region accounts for a significant global share, supported by a mature healthcare infrastructure and a strong focus on reducing inpatient overhead. Key companies operating in the North American market include Medically Home, Biofourmis, and Best Buy Health.

Asia-Pacific is projected to witness the fastest growth during the forecast period. Governments in countries like Australia, Japan, and China are aggressively investing in digital health to manage the healthcare needs of their aging populations. Australia's long-standing 'Hospital in the Home' programs and China's rapid expansion of AI-enabled healthcare services are major growth drivers in the region. Key companies operating in the Asia-Pacific market include Philips Healthcare, GE HealthCare, and local digital health providers.

The global hospital at home market is highly competitive and is characterized by a mix of specialized technology startups, established medical device manufacturers, and major retail health players. Medically Home and Biofourmis are market leaders in the technology and logistics space, while companies like Best Buy Health are leveraging their retail and technical support infrastructure to enter the home-based care market. The competitive landscape is also shaped by large health systems that are developing their own internal HaH capabilities.

Strategic acquisitions and partnerships are the primary growth strategies in the market. Established healthcare companies are acquiring HaH startups to rapidly gain access to RPM platforms and clinical staffing networks. Evidence of clinical outcomes, cost savings, and patient satisfaction are critical for market positioning. Key players in the global hospital at home market include Medically Home, Biofourmis, Best Buy Health (Current Health), DispatchHealth, Contessa Health (Amedisys), Masimo, GE HealthCare, Philips Healthcare, Baxter International, ResMed, Humana, and UnitedHealth Group (Optum).

The market is projected to reach USD 159.7 billion by 2036, growing at a CAGR of 17.6% from 2026 to 2036.

The Services segment is expected to hold the largest share in 2026 due to clinical staffing and logistical costs.

HaH models have demonstrated a significant reduction in 30-day readmission rates, typically in the range of ~10%–25% compared to traditional inpatient care, depending on patient cohort and program design.

Infectious Diseases is expected to grow the fastest due to standardized protocols for home-based IV antibiotic therapy.

HaH models typically result in a 15-30% reduction in the cost of an acute care episode.

The CMS Acute Hospital Care at Home waiver has been a major catalyst, authorizing over 200 hospitals to provide home-based acute care.

North America holds the largest share, driven by advanced infrastructure and strong regulatory support in the U.S.

Reimbursement uncertainties, logistical complexity, and clinician resistance are the main restraints.

By using RPM and AI-driven predictive analytics to identify clinical deterioration early and providing a lower-risk home environment.

The market is led by Medically Home, Biofourmis, Best Buy Health, and major health systems and home health providers.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Component

3.2.2. Market Analysis, by Service Type

3.2.3. Market Analysis, by Indication

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Critical Need to Manage Hospital Capacity and Overcrowding

4.2.1.2. Advancements in Remote Patient Monitoring and Telehealth Technology

4.2.1.3. Aging Global Population and Rising Prevalence of Chronic Conditions

4.2.2. Restraints

4.2.2.1. Dependency on Regulatory Waivers and Reimbursement Uncertainties

4.2.2.2. Logistical Complexity of Coordinating Decentralized Care Delivery

4.2.3. Opportunities

4.2.3.1. Expansion of HaH Programs into Rural and Underserved Areas

4.2.3.2. Integration of AI-Driven Predictive Analytics for Enhanced Safety

4.2.4. Challenges

4.2.4.1. Integration of Decentralized Tech Platforms with Hospital EHR Systems

4.2.4.2. Clinician Resistance and the Need for Significant Change Management

4.2.5. Trends

4.2.5.1. Integration of AI and Machine Learning for High-Acuity Monitoring

4.2.5.2. Strategic Partnerships between Health Systems and HaH Tech Providers

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.4.1. CMS Acute Hospital Care at Home Waiver (U.S.)

4.4.2. International Regulatory Frameworks

4.5. Value Chain Analysis

5. Global Hospital at Home Market, by Component

5.1. Overview

5.2. Software Platforms

5.2.1. RPM Dashboards & Telemedicine Portals

5.2.2. Logistics Orchestration Software

5.3. Medical Devices & Kits

5.3.1. Wearable Sensors & Physiological Monitors

5.3.2. Point-of-Care Testing (POCT) & Infusion Pumps

5.4. Services

5.4.1. Clinical Staffing & Nursing Services

5.4.2. Logistics & Supply Chain Management

6. Global Hospital at Home Market, by Service Type

6.1. Overview

6.2. Acute Care

6.3. Post-Acute Care

6.4. Chronic Care Management

7. Global Hospital at Home Market, by Indication

7.1. Overview

7.2. Cardiovascular Diseases (Heart Failure, Arrhythmia)

7.3. Respiratory Diseases (COPD, Pneumonia)

7.4. Infectious Diseases (Sepsis, Cellulitis)

7.5. Neurological Disorders (Stroke, Dementia)

7.6. Orthopedic Post-Surgical Care

8. Global Hospital at Home Market, by End User

8.1. Overview

8.2. Hospitals & Health Systems

8.3. Home Healthcare Agencies

8.4. Managed Care Organizations (MCOs)

9. Global Hospital at Home Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. U.K.

9.3.2. Spain

9.3.3. Germany

9.3.4. France

9.3.5. Italy

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. Australia

9.4.2. China

9.4.3. Japan

9.4.4. India

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Dashboard

10.4. Vendor Market Positioning

10.5. Market Share Analysis, 2025

11. Company Profiles

11.1. Medically Home

11.2. Biofourmis

11.3. Best Buy Health (Current Health)

11.4. DispatchHealth

11.5. Contessa Health (Amedisys)

11.6. Vivalink

11.7. Masimo

11.8. GE HealthCare

11.9. Philips Healthcare

11.10. Baxter International

11.11. ResMed

11.12. Humana (CenterWell)

11.13. UnitedHealth Group (Optum)

11.14. CVS Health (Signify Health)

11.15. VitalConnect

11.16. Swift Medical

12. Appendix

Published Date: Oct-2024

Published Date: Sep-2023

Published Date: Jun-2023

Published Date: Feb-2023

Published Date: Sep-2013

Subscribe to get the latest industry updates