Resources

About Us

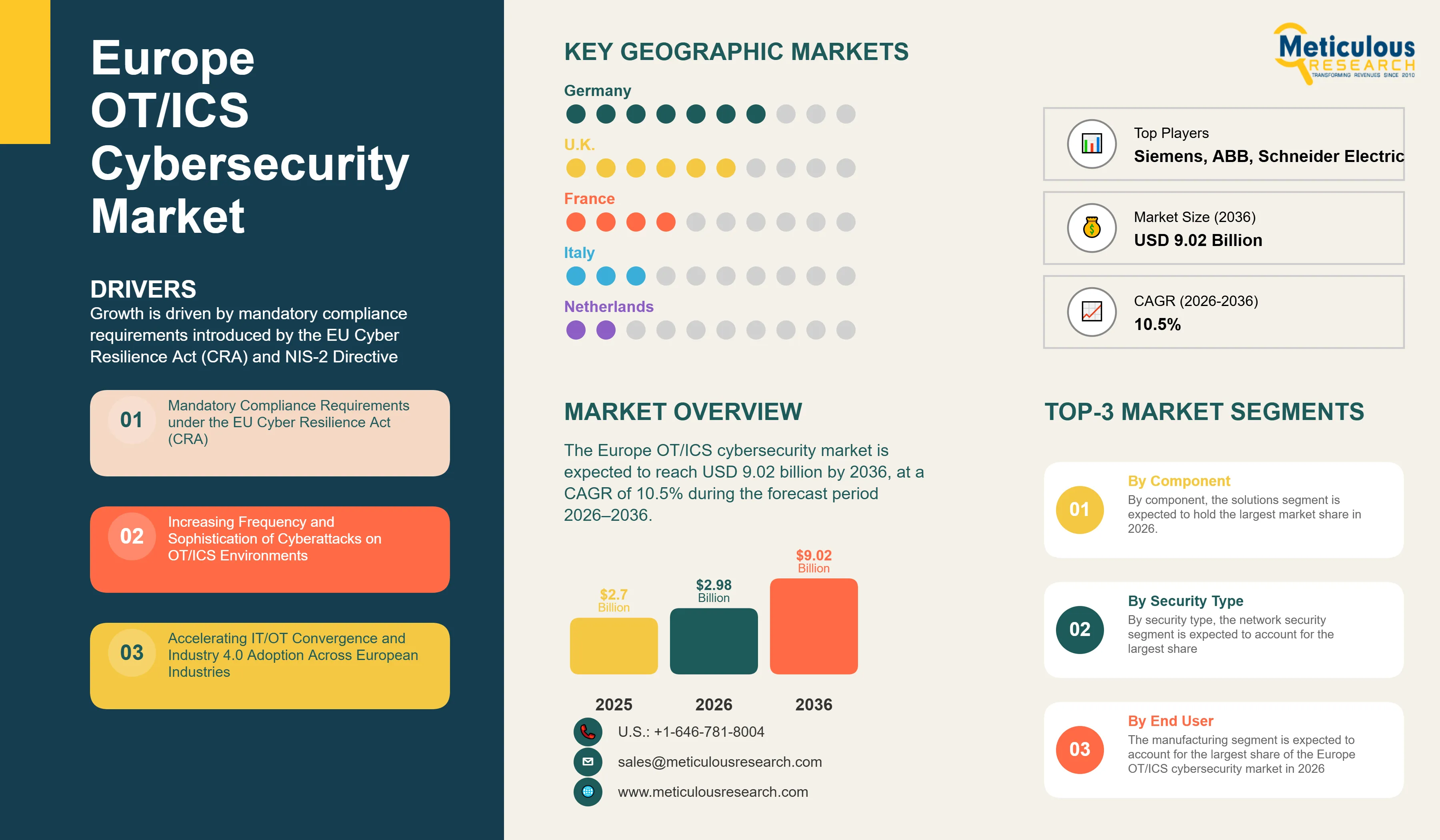

The Europe OT/ICS cybersecurity market was valued at USD 2.70 billion in 2025. This market is expected to reach USD 9.02 billion by 2036 from an estimated USD 2.98 billion in 2026, growing at a CAGR of 10.5% during the forecast period 2026–2036.

The growth of this market is primarily driven by mandatory compliance requirements introduced by the EU Cyber Resilience Act (CRA) and NIS-2 Directive, the increasing frequency and sophistication of cyberattacks targeting OT/ICS environments across European industries, and the growing combination of IT and OT networks. However, the shortage of skilled OT cybersecurity professionals and the complexity of securing legacy industrial environments restrain the growth of this market to some extent.

The growing adoption of managed OT security services and AI/ML-driven threat detection for industrial environments are expected to generate significant market growth opportunities for stakeholders operating in this market. Furthermore, the rising integration of connected devices and Industrial Internet of Things (IIoT) technologies across industrial facilities is a major trend shaping this market.

The Europe OT/ICS cybersecurity market includes different types of solutions and services such as network security, endpoint protection, application security, vulnerability management, software bill of materials (SBOM) tooling, identity and access management, and managed security services deployed across European industrial sectors to protect operational technology and industrial control system environments, achieve regulatory compliance, and safeguard operational continuity against escalating cyber threats.

These solutions and services are availed by a broad range of industries such as manufacturing, energy and utilities, chemicals and process, oil and gas, transportation and logistics, and other critical infrastructure sectors. Within the manufacturing segment, machine manufacturers, the OEMs that build and sell industrial machines with embedded digital components, represent a high-growth sub-segment, driven by the unique compliance obligations imposed on them by the EU Cyber Resilience Act (CRA). Unlike end-use plant operators, machine OEMs bear product-level cybersecurity obligations across the entire lifecycle of every connected machine they place on the EU market, including mandatory Secure-by-Design development, SBOM generation, vulnerability management, and incident reporting obligations that apply from 11 September 2026 and fully from 11 December 2027. This creates a distinct and growing demand pool for embedded OT cybersecurity components and compliance services that is separate from, but additive to, the broader OT security spend by plant operators and utilities.

The EU Cyber Resilience Act (CRA), which entered into force on 10 December 2024, establishes mandatory cybersecurity requirements for all products with digital elements placed on the EU market, including machine controllers, HMIs, PLCs, industrial PCs, connected sensors, and embedded software components. According to VDMA, the mechanical and plant engineering sector employs approximately 3 million people in the EU-27, with Germany alone accounting for over 1.2 million, and many products and components in this sector fall under the CRA. Non-compliance exposes manufacturers to fines of up to €15 million or 2.5% of global annual turnover, whichever is higher, and, for the first time under EU product legislation, introduces direct personal liability for management boards.

Across the OT/ICS market, the NIS-2 Directive (Directive (EU) 2022/2555) is expanding obligations for plant operators, utilities, chemical processors, and transportation providers, driving demand for OT network security, incident response, and risk management solutions. Together with the CRA, which impacts OEMs, this dual regulatory pressure on both suppliers and end users distinguishes the European OT/ICS cybersecurity market from other regions and drives its growth during 2026–2036.

A significant proportion of active production systems and installed machines continue to operate on end-of-life or unsupported platforms, such as Windows XP/7-based HMIs, Siemens S7-300/400 PLCs, Allen-Bradley SLC-500 controllers, and legacy SCADA systems, where patching to CRA and NIS-2 conformity requirements is not feasible without hardware replacement. Replacement cycles in heavy machinery and process industries typically extend to 10–25 years due to capital cost constraints and production continuity requirements, creating a durable demand for security overlay and encapsulation solutions that can protect legacy environments without disrupting operations.

Growing Adoption of Managed OT Security Services

The adoption of managed OT security services is increasing across the European industrial sector, driven by the shortage of in-house OT cybersecurity expertise. Most small and mid-size industrial organizations lack the resources to establish dedicated security operations functions, making outsourced monitoring, patch management, PSIRT support, and managed detection and response services increasingly attractive. Subscription-based managed services offer predictable cost structures well-suited to SME budgets and align with CRA's ongoing vulnerability management obligations, which extend throughout the product support lifecycle. According to the European DIGITAL SME Alliance, more than half of small and medium manufacturers plan to adopt zero-trust architectures for shop-floor networks by 2026, reflecting the growing importance of structured, provider-managed security frameworks across the segment.

AI and ML-Driven Threat Detection for OT Environments

The integration of artificial intelligence and machine learning into OT security platforms is a significant trend driving the Europe OT/ICS cybersecurity market. AI-driven anomaly detection establishes behavioral baselines for industrial control systems and identifies deviations in real time without disrupting operational processes, addressing one of the core challenges of OT security, where traditional signature-based approaches cannot be applied to environments running legacy, proprietary, or safety-critical firmware. According to ENISA’s 2025 Threat Landscape report, which analyzed 4,875 cybersecurity incidents between July 2024 and June 2025, more than 80% of observed social engineering activity globally now involves AI-supported or AI-enhanced phishing techniques, significantly increasing the sophistication of initial compromise attempts. This escalation is driving investment in AI-powered OT security platforms capable of detecting advanced threats before they propagate from IT to OT environments.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 9.02 Billion |

|

Market Size in 2026 |

USD 2.98 Billion |

|

Market Size in 2025 |

USD 2.70 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 10.5% |

|

Dominating Component |

Solutions |

|

Fastest Growing Component |

Services |

|

Dominating Security Type |

Network Security |

|

Fastest Growing Security Type |

Endpoint Security |

|

Dominating Deployment Mode |

On-Premises |

|

Fastest Growing Deployment Mode |

Cloud-Based |

|

Dominating End User |

Manufacturing |

|

Fastest Growing End User |

Energy & Utilities |

|

Dominating Country |

Germany |

|

Fastest Growing Countries |

Italy, Poland |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Based on component, the Europe OT/ICS cybersecurity market is segmented into solutions and services. In 2026, the solutions segment is expected to account for the largest share of approximately 55-60% of the Europe OT/ICS cybersecurity market. The large share of this segment is attributed to the heightened priority that industrial organizations are placing on deploying technical controls — network security appliances, endpoint protection platforms, vulnerability management tools, and firewall and intrusion detection systems to meet CRA and NIS-2 requirements. The growing demand for SBOM generation tools, driven by CRA's mandatory software transparency requirements, is further driving the growth of the European OT/ICS cybersecurity solutions market.

However, the services segment is projected to grow at the fastest CAGR during the forecast period 2026–2036. The high growth of this segment is attributed to the growing adoption of managed OT security services, the growing outsourcing of PSIRT and patch management functions, and the rising demand for CRA compliance consulting and conformity assessment support across both machine OEM and plant operator end users.

Based on security type, the Europe OT/ICS cybersecurity market is segmented into network security, endpoint security, application security, and cloud security. In 2026, the network security segment is expected to account for the largest share the Europe OT/ICS cybersecurity market. The large share of this segment is attributed to the foundational priority of IT/OT network segmentation and industrial firewall deployment in protecting OT environments, where historically air-gapped networks are increasingly being connected to enterprise IT infrastructure and cloud systems as part of Industry 4.0 initiatives.

However, the endpoint security segment is poised to grow at the fastest CAGR during the forecast period. The high growth of this segment is driven by the proliferation of connected industrial endpoints, such as HMIs, edge controllers, industrial PCs, and embedded sensors, and the CRA requirement to address vulnerabilities at the individual product level throughout the product support lifecycle.

Based on deployment mode, the Europe OT/ICS cybersecurity market is segmented into on-premises deployment and cloud-based deployment. In 2026, the on-premises deployment segment is expected to account for the largest share of the Europe OT/ICS cybersecurity market. The large share of this segment is mainly due to the strong preference among industrial organizations for on-premises security architectures in OT environments, where data residency, network latency, and operational safety requirements make cloud connectivity a secondary consideration for core production control systems.

However, the cloud-based deployment segment is projected to register the fastest CAGR during the forecast period. The growing adoption of hybrid IT/OT architectures, the increasing availability of OT-specific cloud security platforms, and the rising uptake of cloud-delivered managed security services among SME organizations are expected to drive this growth of this market throughout the forecast period.

Based on end user, the Europe OT/ICS cybersecurity market is segmented into manufacturing, energy and utilities, chemicals and process industry, oil and gas, transportation and logistics, and other end users. In 2026, the manufacturing segment is expected to account for the largest share of the Europe OT/ICS cybersecurity market. The large share of this segment is attributed to the growing demand for OT security solutions across industrial manufacturing base of Europe, including automotive, pharma, FMCG, heavy machinery, electronics, and packaging OEMs, the increasing integration of connected industrial devices on production floors, and the increasing compliance investment cycle driven by the CRA's December 2027 deadline, which applies specifically to machine manufacturers placing products with digital elements on the EU market. According to ENISA’s 2025 Threat Landscape report, manufacturing accounts for around 59.3% of observed cybersecurity incidents among EU industrial sectors, making it the most targeted segment and reinforcing the urgency of OT security investment across industrial environments.

However, the energy and utilities segment is projected to register among the highest CAGRs during the forecast period, driven by the growing digitization of EU power grids, the expansion of renewable energy infrastructure, and NIS-2 compliance obligations that classify energy operators as essential entities subject to mandatory cybersecurity risk management requirements.

Based on geography, the Europe OT/ICS cybersecurity market is segmented into Germany, the Netherlands, Belgium, France, Italy, Spain, Poland, Sweden, Austria, and the Rest of Europe. In 2026, Germany is expected to account for the largest share of the Europe OT/ICS cybersecurity market. The large share of this country is mainly due to its position as the EU’s largest industrial producer, accounting for around 27% of EU manufacturing output (Eurostat), its 3,500+ VDMA member companies, the highest density of CRA-affected machine OEMs in Europe, and a mature OT cybersecurity and compliance posture supported by a strong BSI and TÜV certification ecosystem.

However, Italy and Poland OT/ICS cybersecurity markets are expected to register the highest growth rates during the forecast period. Italy's growth is driven by the world's highest concentration of packaging machinery OEMs in the Bologna machinery cluster, a high legacy OT burden across pharma and food processing sectors, and the accelerating CRA compliance investment cycle among Italian machine manufacturers. The growth in Poland market is driven by its rapidly expanding manufacturing base, the highest legacy OS burden in the EU among Eastern European industrial populations, and growing CRA awareness and investment cycle as the December 2027 deadline approaches.

The Europe OT/ICS cybersecurity market is moderately fragmented, with competition centered on OT/ICS security capabilities, regulatory compliance credentials, and the ability to address the specific operational and technical constraints of industrial environments across diverse end user sectors. The report offers a competitive analysis based on an extensive assessment of the leading players' product portfolios, geographic presence, and key growth strategies adopted in the couple of years. Some of the key players operating in the Europe OT/ICS cybersecurity market are Siemens AG (Germany), Schneider Electric SE (France), ABB Ltd. (Switzerland), Claroty Ltd. (U.S./Israel), Dragos, Inc. (U.S.), Tenable Holdings, Inc. (U.S.), Forescout Technologies, Inc. (U.S.), Nozomi Networks, Inc. (Switzerland/U.S.), TXOne Networks, Inc. (Taiwan), Fortinet, Inc. (U.S.), Palo Alto Networks, Inc. (U.S.), Honeywell International Inc. (U.S.), TRIOVEGA GmbH (Germany), Stormshield SAS (France), and Rhebo GmbH (Germany) among others.

The Europe OT/ICS cybersecurity market is expected to reach USD 9.02 billion by 2036 from an estimated USD 2.98 billion in 2026, at a CAGR of 10.5% during the forecast period 2026–2036.

In 2026, the solutions segment is expected to hold the largest share of the Europe OT/ICS cybersecurity market.

The services segment is expected to register the highest CAGR during the forecast period 2026–2036.

In 2026, the network security segment is expected to hold the largest share of the Europe OT/ICS cybersecurity market.

In 2026, the manufacturing segment is expected to hold the largest share of the Europe OT/ICS cybersecurity market.

The growth of the Europe OT/ICS cybersecurity market is primarily driven by mandatory compliance requirements under the EU Cyber Resilience Act and NIS-2 Directive, the increasing frequency and sophistication of cyberattacks targeting OT/ICS environments in European industrial sectors, and the accelerating convergence of IT and OT networks. The growing adoption of managed OT security services and AI/ML-based threat detection are expected to create significant growth opportunities for market stakeholders.

Key players operating in the Europe OT/ICS cybersecurity market are Siemens AG (Germany), Schneider Electric SE (France), ABB Ltd. (Switzerland), Claroty Ltd. (U.S./Israel), Dragos, Inc. (U.S.), Tenable Holdings, Inc. (U.S.), Forescout Technologies, Inc. (U.S.), Nozomi Networks, Inc. (Switzerland/U.S.), TXOne Networks, Inc. (Taiwan), Fortinet, Inc. (U.S.), Palo Alto Networks, Inc. (U.S.), Honeywell International Inc. (U.S.), TRIOVEGA GmbH (Germany), Stormshield SAS (France), and Rhebo GmbH (Germany).

Italy and Poland are expected to register the highest growth rates in the Europe OT/ICS cybersecurity market during the forecast period 2026–2036.

1. Introduction

1.1. Market Definition and Scope

1.2. Currency & Limitations

1.3. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection Methods — Primary and Secondary Research

2.3. Market Estimation and Forecast Methodology

2.4. Research Assumptions and Limitations

3. Executive Summary

3.1. Market Overview

3.2. Market Analysis by Component

3.3. Market Analysis by Security Type

3.4. Market Analysis by Deployment Mode

3.5. Market Analysis by End User

3.6. Market Analysis by Country

4. Market Dynamics

4.1. Overview

4.2. Drivers

4.2.1. Mandatory Compliance Requirements under the EU Cyber Resilience Act (CRA)

4.2.2. Increasing Frequency and Sophistication of Cyberattacks on OT/ICS Environments

4.2.3. Accelerating IT/OT Convergence and Industry 4.0 Adoption Across European Industries

4.2.4. NIS-2 Directive — Expanding OT Security Obligations Across Critical Infrastructure Sectors

4.3. Restraints

4.3.1. Shortage of OT Cybersecurity Expertise Across European Industrial Organizations

4.3.2. High Complexity and Cost of Securing Legacy Industrial Environments

4.4. Opportunities

4.4.1. Growing Adoption of Managed OT Security Services Among SME Industrial Organizations

4.4.2. Rising Adoption of IEC 62443 as the Preferred CRA and NIS-2 Compliance Pathway

4.4.3. EU Public Funding Initiatives Supporting SME Cybersecurity Investment

4.5. Challenges

4.5.1. Long Asset Replacement Cycles in Industrial OT Environments

4.5.2. Implementation Uncertainty in CRA Technical Standards and Harmonized Norms

5. Europe OT/ICS Cybersecurity Market, by Component

5.1. Overview

5.2. Solutions

5.2.1. Network Security Solutions

5.2.2. Endpoint Security Solutions

5.2.3. Firewall and Intrusion Detection/Prevention Systems

5.2.4. Identity and Access Management

5.2.5. Vulnerability Management and SBOM Tools

5.2.6. Application Security Solutions

5.2.7. Risk and Compliance Management

5.2.8. Other Solutions

5.3. Services

5.3.1. Professional Services

5.3.2. Managed Security Services

6. Europe OT/ICS Cybersecurity Market, by Security Type

6.1. Overview

6.2. Network Security

6.3. Endpoint Security

6.4. Application Security

6.5. Cloud Security

7. Europe OT/ICS Cybersecurity Market, by Deployment Mode

7.1. Overview

7.2. On-Premises Deployment

7.3. Cloud-Based Deployment

8. Europe OT/ICS Cybersecurity Market, by End User

8.1. Overview

8.2. Manufacturing

8.2.1. Automotive & Tier-2 Supply

8.2.2. Pharma & Life Sciences

8.2.3. Chemicals & Process Industry

8.2.4. FMCG & Food Processing

8.2.5. Heavy Machinery & Capital Equipment

8.2.6. Electronics & Semiconductor Equipment

8.2.7. Packaging & Logistics Machinery

8.2.8. Other Manufacturing

8.3. Energy & Utilities

8.4. Oil & Gas

8.5. Transportation & Logistics

8.6. Other End Users

9. Europe OT/ICS Cybersecurity Market, by Country

9.1. Overview

9.2. Germany

9.3. France

9.4. Italy

9.5. Netherlands

9.6. Belgium

9.7. Spain

9.8. Poland

9.9. Sweden

9.10. Austria

9.11. Rest of Europe

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies Adopted by Leading Players

10.3. Competitive Benchmarking by Player

10.4. Market Share Analysis (2026)

11. Company Profiles

11.1. Siemens AG

11.2. Schneider Electric SE

11.3. ABB Ltd.

11.4. Claroty Ltd.

11.5. Dragos, Inc.

11.6. Tenable Holdings, Inc.

11.7. Forescout Technologies, Inc.

11.8. Nozomi Networks, Inc.

11.9. TXOne Networks, Inc.

11.10. Fortinet, Inc.

11.11. Palo Alto Networks, Inc.

11.12. Honeywell International Inc.

11.13. TRIOVEGA GmbH

11.14. Stormshield SAS

11.15. Rhebo GmbH

12. Appendix

12.1. Questionnaire

12.2. Available Customization Options

12.3. Related Reports

Published Date: Feb-2025

Published Date: Jan-2025

Published Date: May-2024

Published Date: Jan-2024

Published Date: Jun-2023

Subscribe to get the latest industry updates