Resources

About Us

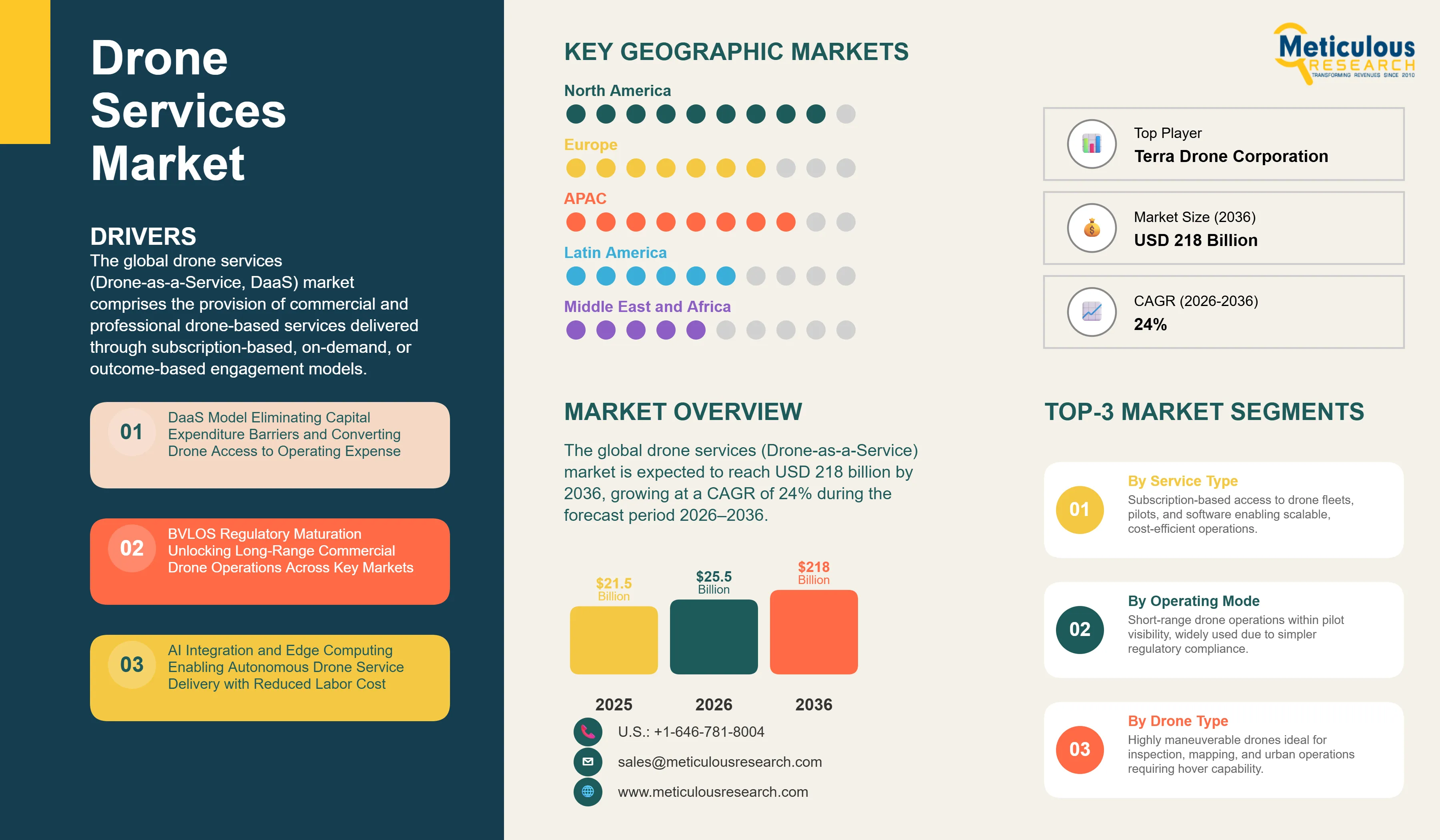

The global drone services (Drone-as-a-Service) market was valued at USD 21.5 billion in 2025. This market is expected to reach USD 218 billion by 2036 from an estimated USD 25.5 billion in 2026, growing at a CAGR of 24% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global drone services (Drone-as-a-Service, DaaS) market comprises the provision of commercial and professional drone-based services delivered through subscription-based, on-demand, or outcome-based engagement models. These services enable organizations to access capabilities such as aerial data collection, inspection, surveillance, mapping, delivery, and analytics without the need to own or manage drone hardware, pilot resources, software platforms, or regulatory compliance frameworks.

The DaaS model aligns with the broader shift toward as-a-service business models across enterprise operations. Instead of investing in drone fleet procurement, pilot hiring and certification, flight operations software, and multi-jurisdictional regulatory approvals, organizations increasingly rely on specialized service providers that deliver defined outputs, such as inspection reports, geospatial datasets, delivery execution, or agricultural insights. These services are typically priced on a per-mission, per-flight-hour, or subscription basis, offering greater cost flexibility, scalability, and operational efficiency.

The growth of the drone services (Drone-as-a-Service) market is primarily driven by the increasing adoption of subscription-based and on-demand drone service models across commercial, industrial, and government sectors. These models eliminate the need for significant upfront investments in drone fleet ownership, pilot training, maintenance infrastructure, and regulatory compliance, enabling organizations to convert capital expenditure into predictable operating expenses. This cost-efficient and scalable access to drone capabilities is accelerating enterprise adoption across applications such as inspection, surveying, and logistics.

In addition, the evolving regulatory landscape supporting Beyond Visual Line of Sight (BVLOS) operations is significantly enhancing the commercial viability of drone services. Regulatory developments, including the anticipated Federal Aviation Administration Part 108 framework, are expected to streamline approval processes and reduce operational barriers, enabling long-range and high-frequency drone deployments across infrastructure inspection, delivery, and precision agriculture use cases.

Furthermore, the integration of artificial intelligence (AI) and edge computing into drone platforms is expanding the functional capabilities of drone services. Advanced features such as autonomous navigation, real-time defect detection, AI-driven analytics, and swarm coordination are reducing reliance on manual intervention and enhancing operational efficiency, thereby broadening the addressable market across industries.

Despite strong growth prospects, the market faces challenges due to the fragmented and complex regulatory environment across regions. Drone operations often require multiple approvals, including airspace authorization, pilot certification, remote identification compliance, and BVLOS-specific permissions, which vary significantly across countries. Additionally, concerns related to cybersecurity, data privacy, and safe integration of drones into shared airspace continue to limit widespread adoption, particularly in sensitive sectors.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 218 Billion |

|

Market Size in 2026 |

USD 25.5 Billion |

|

Market Size in 2025 |

USD 21.5 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 24% |

|

Dominating Service Type |

Drone Platform Services (Inspection & Monitoring) |

|

Fastest Growing Service Type |

Training & Simulation |

|

Dominating Operating Mode |

Visual Line of Sight (VLOS) |

|

Fastest Growing Operating Mode |

Beyond Visual Line of Sight (BVLOS) |

|

Dominating Drone Type |

Rotary-Wing (Multi-Rotor) |

|

Fastest Growing Drone Type |

Hybrid VTOL |

|

Dominating End-Use Industry |

Infrastructure & Energy Inspection |

|

Fastest Growing End-Use Industry |

Delivery & Logistics |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

BVLOS Regulatory Unlocking Creating Transformative Operational Scale Expansion

BVLOS regulatory maturation, driven by evolving frameworks from authorities such as the Federal Aviation Administration and European Union Aviation Safety Agency, is emerging as a key factor driving the growth of the drone services market over the forecast period. Regulatory developments, such as the anticipated Part 108 BVLOS rulemaking in the U.S., which is expected to significantly reduce approval timelines, along with advancements in powered-lift certification frameworks and U-space/UTM integration across Europe, are enabling more scalable and commercially viable drone operations across regions.

The transition from Visual Line of Sight (VLOS) to Beyond Visual Line of Sight (BVLOS) operations transforms the cost structure and scalability of drone services. While VLOS operations remain labor-intensive, requiring continuous pilot visibility and proximity, BVLOS enables long-range, automated missions across linear infrastructure, large geographic areas, and urban delivery networks.

For instance, AI-enabled BVLOS inspection drones can cover approximately 50–100 kilometers of pipelines or power lines per day, compared to 2–5 kilometers under VLOS operations that rely on ground-based inspection teams. This indicates a 20x–50x increase in operational productivity, significantly improving service economics. Similarly, BVLOS-based delivery models expand serviceable coverage exponentially, enabling access to a substantially larger customer base within a given radius and supporting the commercialization of last-mile drone delivery at scale.

AI Integration and Autonomy Enabling Drone-in-a-Box and Fully Automated Inspection Services

The integration of artificial intelligence (AI), mainly through edge computing and advanced autonomy in aerial and ground systems, is enabling the emergence of drone-in-a-box (DIB) solutions and fully automated drone service models. These advancements significantly reduce reliance on human intervention, thereby lowering per-mission labor costs, which have historically constrained the scalability and profitability of drone service operations.

DIB systems, comprising weather-resistant docking stations for automated charging, storage, and scheduled deployment, are facilitating continuous and repeatable operations across applications such as infrastructure monitoring, perimeter security, and utility inspections. These systems support persistent, high-frequency data collection without requiring on-site pilots, improving operational efficiency and coverage.

Recent enterprise deployments of autonomous drone platforms from companies such as Skydio highlight the growing maturity of AI-driven navigation and obstacle avoidance technologies, enabling reliable large-scale operations. In parallel, edge AI capabilities are enabling real-time, in-flight defect detection—including corrosion, structural cracks, and thermal anomalies—directly from captured imagery.

As a result, drone-based inspection services are evolving from standalone data collection processes into integrated, insight-driven asset management workflows. Processed outputs can be seamlessly integrated into enterprise platforms such as SAP and IBM Maximo, enabling predictive maintenance, faster decision-making, and improved asset lifecycle management.

By Service Type: In 2026, Drone Platform Services to Dominate

Based on service type, the global drone services market is segmented into drone platform services, inspection & monitoring services, mapping & surveying services, precision agriculture services, delivery & logistics services, data analytics & reporting services, maintenance, repair & overhaul (MRO) services, and training & simulation services.

In 2026, drone platform services are expected to account for the largest market share. This segment, comprising subscription-based fleet access, managed drone operations, and on-demand deployment models, forms the foundation of the Drone-as-a-Service (DaaS) business model. The dominance of this segment is driven by increasing enterprise preference for integrated service offerings that bundle drone hardware, pilot operations, software platforms, and regulatory compliance within a single contract, enabling cost efficiency and operational scalability across industries such as construction, energy, agriculture, and logistics.

However, training & simulation services are projected to register the highest CAGR during the forecast period. The growth of this segment is primarily driven by the shortage of skilled commercial drone pilots, particularly for advanced operations such as BVLOS missions, swarm deployments, and complex payload handling. This is driving demand for simulation-based training platforms that enable faster, cost-effective, and risk-free pilot certification compared to conventional field training methods.

By Operating Mode: VLOS Dominant; BVLOS Fastest Growing

Based on operating mode, the global drone services market is segmented into visual line of sight (VLOS), extended visual line of sight (EVLOS), and beyond visual line of sight (BVLOS).

In 2026, VLOS operations are expected to hold the largest market share, primarily due to their alignment with existing regulatory frameworks across major markets. VLOS operations require relatively lower certification complexity and are widely adopted for short-range applications such as aerial photography, localized infrastructure inspections, and precision agriculture activities. The concentration of commercial drone deployments within limited operational radii further supports the dominance of VLOS-based services.

However, BVLOS operations are projected to register the highest CAGR during the forecast period. The growth of this segment is driven by ongoing regulatory advancements, including initiatives by the Federal Aviation Administration and the European Union Aviation Safety Agency, which are enabling more scalable and automated drone operations. BVLOS is critical for unlocking high-value use cases such as long-distance infrastructure inspection and commercial drone delivery networks, where VLOS-based operations are economically unviable due to the need for continuous human oversight. Increasing regulatory approvals across key regions are enabling a transition from pilot-scale deployments to network-level operations, significantly expanding the addressable market for drone services.

By Drone Type: Rotary-Wing Dominant; Hybrid VTOL Fastest Growing

Based on drone type, the global drone services market is segmented into rotary-wing (multi-rotor), fixed-wing, and hybrid VTOL.

In 2026, rotary-wing drones are expected to account for the largest market share. The dominance of this segment is primarily attributed to their ability to hover and perform stable, close-range inspections of vertical and complex infrastructure such as cell towers, wind turbines, and building facades. In addition, their vertical take-off and landing (VTOL) capability enables operations in confined or urban environments without the need for runways. Advancements in obstacle avoidance, autonomous flight control, and ruggedized (IP-rated) airframes have further enhanced their suitability for commercial service deployments. As a result, multi-rotor drones are widely used across inspection, public safety, and urban delivery applications where maneuverability and positional accuracy are critical.

However, hybrid VTOL drones are projected to register the highest CAGR during the forecast period. The growth of this segment is driven by their ability to combine the vertical take-off capability of rotary systems with the endurance and range efficiency of fixed-wing platforms. Regulatory developments, including powered-lift certification advancements led by the Federal Aviation Administration, are supporting the commercialization of such platforms. Hybrid VTOL systems are particularly suited for long-range delivery missions and linear infrastructure inspection, where multi-rotor drones face endurance limitations, thereby enabling more cost-effective and scalable operations.

By End-Use Industry: Infrastructure & Energy Inspection Dominant; Delivery & Logistics Fastest Growing

Based on end-use industry, the global drone services market is segmented into construction & infrastructure, agriculture & forestry, energy & utilities, logistics & transportation, media & entertainment, defense & public safety, mining, and healthcare.

In 2026, construction & infrastructure and energy & utilities inspection are expected to account for the largest share of the global drone services market. This segment includes applications such as power line inspection, pipeline monitoring, cell tower inspection, bridge and dam assessment, and wind turbine blade inspection. The dominance of this segment is driven by the high value per mission, supported by the use of advanced sensor payloads—including thermal imaging, LiDAR, and high-resolution optical systems, and AI-driven analytics that enable predictive maintenance and asset optimization. Specialized service providers such as VOLT Inspection demonstrate the emergence of vertical-specific, high-margin service models in this segment.

However, delivery & logistics is projected to register the highest CAGR during the forecast period. The growth of this segment is driven by the scaling of commercial drone delivery networks led by companies such as Amazon, Alphabet, and Zipline. These companies are expanding operations from pilot projects to commercial-scale deployments, supported by increasing regulatory approvals for BVLOS operations. For instance, Zipline has expanded its drone delivery services in regions such as North Carolina to support medical supply logistics, demonstrating the transition toward operational, network-based drone delivery ecosystems.

North America: Largest Market in 2026

North America is expected to account for the largest share of the global drone services market in 2026. The region’s dominance is driven by a favorable regulatory environment, led by advancements from the Federal Aviation Administration, including ongoing progress in BVLOS rulemaking and powered-lift certification frameworks introduced in 2025.

In addition, the widespread deployment of advanced communication infrastructure, including 5G networks, is enabling real-time telemetry, edge computing, and AI-driven drone operations at scale. The presence of leading ecosystem players such as DroneDeploy, Skydio, AgEagle Aerial Systems, ZenaTech, Zipline, and Alphabet further strengthens the region’s leadership.

Strong demand across end-use industries, including energy & utilities (pipeline and power line inspection), construction & infrastructure (surveying and monitoring), agriculture (precision farming), and defense & public safety, continues to drive market growth.

Asia-Pacific: Fastest-growing Market

Asia-Pacific is projected to register the highest CAGR during the forecast period, driven by rapid technological adoption, supportive government initiatives, and large-scale commercial deployments across key countries.

China remains a dominant force in the regional ecosystem, driven by companies such as DJI, which accounts for a substantial share of global drone hardware, along with logistics players such as JD.com and Alibaba Group that are advancing drone-based delivery networks, particularly in rural and semi-urban areas.

India is emerging as a high-growth market, driven by government initiatives such as the Kisan Drone program and production-linked incentive (PLI) schemes introduced in 2022, which are driving adoption across agriculture and infrastructure inspection applications. Meanwhile, Japan is leveraging drone technologies to address labor shortages in logistics and rural connectivity, with companies such as Rakuten and All Nippon Airways deploying BVLOS-enabled drone delivery networks in remote regions.

The global drone services (DaaS) market is characterized by a dynamic competitive landscape comprising managed drone service operators, drone delivery network providers, and specialized vertical service companies offering inspection, surveying, mapping, and analytics services across industries. These players generate revenue through service-based business models, including subscription-based, on-demand, and outcome-based contracts.

Leading companies such as Zipline operate large-scale drone delivery networks, particularly in healthcare and commercial logistics, with millions of deliveries completed globally. Similarly, Wing has established commercial drone delivery operations with Beyond Visual Line of Sight (BVLOS) capabilities across multiple regions.

Service providers such as Terra Drone Corporation and Aerodyne Group offer integrated drone solutions spanning inspection, surveying, and industrial asset monitoring across global markets. Companies, including Cyberhawk and SkySpecs specialize in high-value infrastructure and energy asset inspections, leveraging advanced analytics and AI-driven insights.

In addition, players such as Zeitview and DroneUp provide scalable enterprise drone services across multiple industries, while emerging companies such as Percepto and American Robotics are advancing fully autonomous drone operations, including drone-in-a-box (DIB) solutions for continuous monitoring and inspection.

The report provides a comprehensive competitive analysis based on an assessment of key players’ service portfolios, geographic presence, operational scale, and strategic initiatives undertaken over the past few years. Some of the key players operating in the global drone services (DaaS) market include Zipline International Inc. (U.S.), Wing Aviation LLC (Alphabet Inc.) (U.S.), Terra Drone Corporation (Japan), Cyberhawk Innovations Limited (U.K.), Zeitview, Inc. (U.S.), Aerodyne Group (Malaysia), SkySpecs, Inc. (U.S.), DroneUp, LLC (U.S.), Percepto Ltd. (Israel), American Robotics, Inc. (Ondas Holdings Inc.) (U.S.), PrecisionHawk, Inc. (U.S.), Volatus Aerospace Corp. (Canada), Flytrex Aviation Ltd. (Israel), Manna Drone Delivery Ltd. (Ireland), and Delair SAS (France) among others.

The global drone services market is expected to reach USD 218 billion by 2036 from an estimated USD 25.5 billion in 2026, at a CAGR of 24% during the forecast period 2026–2036.

In 2026, drone platform services (subscription-based fleet access and on-demand managed drone operations) is expected to hold the largest market share of the global drone services market.

Training and simulation services is expected to register the highest CAGR during the forecast period 2026–2036, driven by severe drone pilot labor shortfalls creating intense demand for BVLOS, swarm, and advanced payload operation simulation training.

BVLOS (Beyond Visual Line of Sight) operations are expected to register the highest CAGR during the forecast period, driven by progressive regulatory frameworks including the FAA's Part 108 rulemaking and EASA's U-space framework that are enabling commercial-scale long-range drone operations.

The delivery and logistics segment is expected to register the highest CAGR during the forecast period, driven by the commercial scaling of drone delivery networks by Amazon Prime Air, Wing, Zipline, and regional operators, supported by BVLOS approvals enabling citywide delivery network operations.

The growth of this market is primarily driven by the DaaS model eliminating capital expenditure barriers to drone adoption, BVLOS regulatory maturation unlocking long-range commercial drone operations, and AI integration enabling autonomous drone service delivery at scale.

Key players in the global drone services (Drone-as-a-Service) market include Zipline International Inc. (U.S.), Wing Aviation LLC (Alphabet Inc.) (U.S.), Terra Drone Corporation (Japan), Cyberhawk Innovations Limited (U.K.), Zeitview, Inc. (U.S.), Aerodyne Group (Malaysia), SkySpecs, Inc. (U.S.), DroneUp, LLC (U.S.), Percepto Ltd. (Israel), American Robotics, Inc. (Ondas Holdings Inc.) (U.S.), PrecisionHawk, Inc. (U.S.), Volatus Aerospace Corp. (Canada), Flytrex Aviation Ltd. (Israel), Manna Drone Delivery Ltd. (Ireland), and Delair SAS (France).

Asia Pacific is expected to register the highest growth rate in the global drone services market during the forecast period 2026–2036, driven by China's dominant commercial drone ecosystem, India's Kisan Drone initiative and infrastructure expansion, and Japan's drone-led logistics transformation to address labor shortages.

1. Introduction

1.1 Market Definition and Scope

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

3.1 Market Overview

3.2 Market Analysis by Service Type

3.3 Market Analysis by Operating Mode

3.4 Market Analysis by Drone Type

3.5 Market Analysis by End-Use Industry

3.6 Market Analysis by Geography

4. Market Dynamics

4.1 Overview

4.2 Drivers

4.2.1 DaaS Model Eliminating Capital Expenditure Barriers and Converting Drone Access to Operating Expense

4.2.2 BVLOS Regulatory Maturation Unlocking Long-Range Commercial Drone Operations Across Key Markets

4.2.3 AI Integration and Edge Computing Enabling Autonomous Drone Service Delivery with Reduced Labor Cost

4.2.4 Enterprise Digital Transformation Driving Demand for Aerial Data Analytics and Digital Twin Integration

4.3 Restraints

4.3.1 Complex Fragmented Regulatory Landscape Requiring Jurisdiction-Specific Airspace Approvals and Pilot Certifications

4.3.2 Cybersecurity, Data Privacy, and Airspace Integration Concerns Limiting Adoption in Sensitive Verticals

4.4 Opportunities

4.4.1 5G and Satellite Connectivity Enabling Real-Time High-Bandwidth Telemetry for Wide-Area BVLOS Drone Services

4.4.2 Drone-in-a-Box and Dock-Based Autonomous Inspection Systems Enabling 24/7 Continuous Monitoring Services

4.4.3 Digital Twin Integration Creating Premium Recurring Subscription Revenue from Drone Survey Data Platforms

4.5 Challenges

4.5.1 Drone Pilot Labor Shortage Constraining Operational Scale of VLOS and Advanced Payload Drone Services

4.5.2 Weather Dependency and Limited Endurance Constraining Operational Continuity for Outdoor Drone Service Missions

4.6 Porter’s Five Forces Analysis

5. Drone Services Market, by Service Type

5.1 Overview

5.2 Drone Platform Services

5.3 Inspection & Monitoring Services

5.4 Mapping & Surveying Services

5.5 Precision Agriculture Services

5.6 Delivery & Logistics Services

5.7 Data Analytics & Reporting Services

5.8 Maintenance, Repair & Overhaul (MRO) Services

5.9 Training & Simulation Services

6. Drone Services Market, by Operating Mode

6.1 Overview

6.2 Visual Line of Sight (VLOS)

6.3 Extended Visual Line of Sight (EVLOS)

6.4 Beyond Visual Line of Sight (BVLOS)

7. Drone Services Market, by Drone Type

7.1 Overview

7.2 Rotary-Wing (Multi-Rotor)

7.3 Fixed-Wing

7.4 Hybrid VTOL

8. Drone Services Market, by End-Use Industry

8.1 Overview

8.2 Construction & Infrastructure

8.3 Agriculture & Forestry

8.4 Energy & Utilities

8.5 Logistics & Transportation

8.6 Media & Entertainment

8.7 Defense & Public Safety

8.8 Mining

8.9 Healthcare

9. Drone Services Market, by Geography

9.1 Overview

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.3 Europe

9.3.1 U.K.

9.3.2 Germany

9.3.3 France

9.3.4 Italy

9.3.5 Spain

9.3.6 Netherlands

9.3.7 Rest of Europe

9.4 Asia-Pacific

9.4.1 China

9.4.2 Japan

9.4.3 India

9.4.4 South Korea

9.4.5 Australia

9.4.6 Southeast Asia

9.4.7 Rest of Asia-Pacific

9.5 Latin America

9.5.1 Brazil

9.5.2 Mexico

9.5.3 Argentina

9.5.4 Rest of Latin America

9.6 Middle East & Africa

9.6.1 UAE

9.6.2 Saudi Arabia

9.6.3 South Africa

9.6.4 Rest of Middle East & Africa

10. Competitive Landscape

10.1 Overview

10.2 Key Growth Strategies

10.3 Competitive Benchmarking

10.4 Competitive Dashboard

10.4.1 Industry Leaders

10.4.2 Market Differentiators

10.4.3 Vanguards

10.4.4 Emerging Companies

10.5 Market Share/Ranking Analysis (2025)

11. Company Profiles

11.1 Zipline International Inc.

11.2 Wing Aviation LLC (Alphabet Inc.)

11.3 Terra Drone Corporation

11.4 Cyberhawk Innovations Limited

11.5 Zeitview, Inc.

11.6 Aerodyne Group

11.7 SkySpecs, Inc.

11.8 DroneUp, LLC

11.9 Percepto Ltd.

11.10 American Robotics, Inc. (Ondas Holdings Inc.)

11.11 PrecisionHawk, Inc.

11.12 Volatus Aerospace Corp.

11.13 Flytrex Aviation Ltd.

11.14 Manna Drone Delivery Ltd.

11.15 Delair SAS

11.16 Others

12. Appendix

12.1 Questionnaire

12.2 Available Customization Options

12.3 Related Reports

Published Date: Feb-2025

Published Date: Jul-2024

Published Date: Jun-2023

Subscribe to get the latest industry updates