Resources

About Us

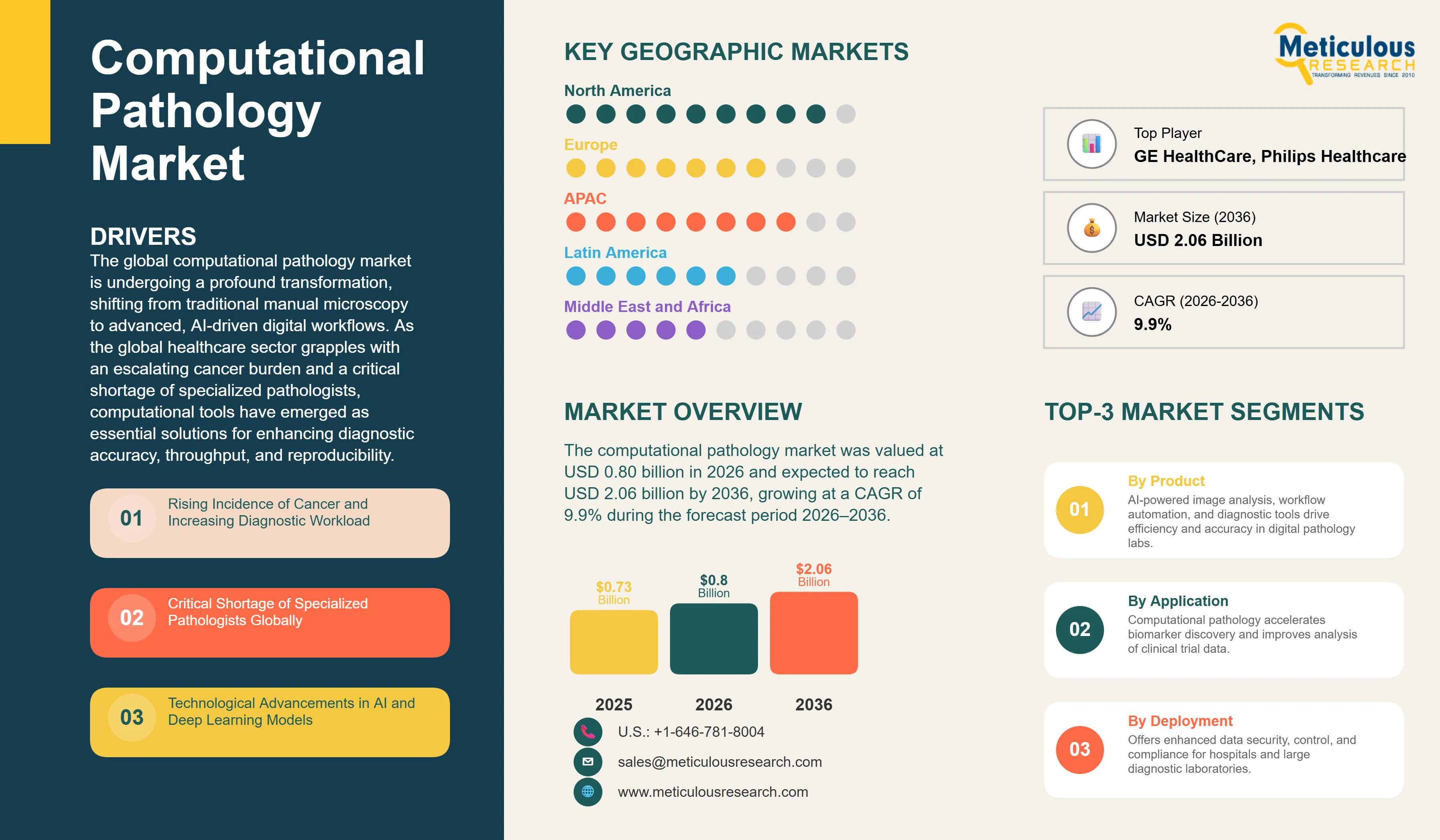

The global computational pathology market was valued at USD 0.80 billion in 2026. This market is expected to reach USD 2.06 billion by 2036, growing at a CAGR of 9.9% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global computational pathology market is undergoing a profound transformation, shifting from traditional manual microscopy to advanced, AI-driven digital workflows. As the global healthcare sector grapples with an escalating cancer burden and a critical shortage of specialized pathologists, computational tools have emerged as essential solutions for enhancing diagnostic accuracy, throughput, and reproducibility. These systems utilize sophisticated image analysis algorithms to interpret whole-slide images (WSI), enabling the identification of subtle morphological features that may be missed by the human eye. The market's growth is fundamentally anchored by the rising incidence of chronic diseases, particularly cancer, cardiovascular disorders, and neurological conditions. According to the International Agency for Research on Cancer, approximately 20 million new cancer cases and 9.7 million cancer-related deaths were reported globally in 2022, while the global cancer burden is projected to increase by 77% by 2050, reaching more than 35 million new cases annually. This growing disease burden is accelerating the adoption of AI-enabled medical devices for early detection, diagnosis, treatment planning, and patient monitoring.

Technological advancements in artificial intelligence (AI) and machine learning (ML) are the primary catalysts for market expansion. Modern computational pathology platforms now incorporate deep learning models capable of performing complex tasks such as tissue segmentation, cell counting, and biomarker quantification with unprecedented precision. These tools can reduce slide review time by up to 30%, allowing pathologists to focus on more complex cases while maintaining a high standard of care. Furthermore, the integration of computational pathology with other multi-omics data—including genomics and proteomics—is paving the way for holistic precision medicine, where diagnostic insights are personalized to the individual patient's biological profile.

The market is also benefiting from the widespread adoption of digital scanners, which create the foundational digital data needed for computational analysis. While on-premise deployment remains the dominant choice for large academic medical centers due to data control and security requirements, cloud-based SaaS models are witnessing the fastest growth. These cloud solutions offer the scalability and interoperability needed for multidisciplinary care settings and reduce the significant capital investment required for high-performance computing infrastructure. The competitive landscape is characterized by a mix of established medical device giants and agile AI startups, all vying to secure regulatory approvals and prove the clinical validity of their diagnostic algorithms.

Geographically, North America leads the global market. This dominance is driven by robust NIH funding, a high concentration of leading pharmaceutical companies, and a proactive regulatory environment for digital health tools. However, the Asia-Pacific region is projected to witness the fastest growth through 2036. Countries like China and India are rapidly modernizing their diagnostic infrastructure and adopting AI-driven solutions to manage their massive patient populations. As computational pathology becomes the standard of care, the market is poised for sustained growth, reaching over USD 2 billion by the end of the forecast period.

The primary driver for the computational pathology market is the rising global incidence of cancer, which is creating significant demand for faster, more accurate, and scalable diagnostic solutions. According to the International Agency for Research on Cancer, approximately 20 million new cancer cases and 9.7 million cancer-related deaths were reported globally in 2022, and the global cancer burden is projected to increase by 77% by 2050, reaching more than 35 million new cases annually. This growing disease burden is increasing pathology testing volumes and accelerating the need for AI-enabled diagnostic technologies.

Furthermore, the shortage of trained pathology professionals remains a major challenge for healthcare systems worldwide. According to the World Health Organization, the world is projected to face a shortage of approximately 10 million health workers by 2030, including laboratory and diagnostic specialists. Computational pathology solutions help laboratories manage increasing workloads through automation, image analysis, and decision support. Technological advances in artificial intelligence and deep learning have further improved the ability of algorithms to identify complex tissue patterns with high consistency and reproducibility. In addition, the growing adoption of digital pathology is expanding the foundation for computational analysis, with the U.S. Food and Drug Administration having authorized multiple whole-slide imaging systems for primary diagnostic use, supporting broader implementation across pathology laboratories.

Restraint

A major restraint is the high capital investment required for implementing a full computational pathology workflow, including high-speed scanners, high-performance computing servers, and massive storage solutions. Furthermore, the complex and evolving regulatory landscapes for clinical AI algorithms, such as FDA and CE-IVD approvals, can slow down the time-to-market for new products. Concerns regarding the interoperability of different image formats and the integration of these tools into existing laboratory information systems (LIS) also pose significant challenges.

Significant opportunities exist in the integration of computational pathology with other precision medicine data, such as genomics and proteomics, to provide holistic diagnostic insights. The expansion of AI-driven diagnostic tools into emerging markets, where healthcare infrastructure is rapidly modernizing, presents a massive growth path. Furthermore, the development of companion diagnostics that utilize computational pathology to identify patients most likely to respond to specific targeted therapies offers high potential for pharmaceutical partnerships. The use of AI for predicting treatment toxicity and long-term outcomes is also a major emerging opportunity.

A key challenge is the lack of standardized image formats across different scanner manufacturers, which complicates the development of universal AI algorithms. Ensuring the data security and privacy of massive amounts of sensitive patient information is also a critical concern for healthcare providers. Furthermore, manufacturers must overcome pathologist skepticism regarding the 'black box' nature of AI and prove the long-term clinical and economic benefits of these systems to secure broad adoption and reimbursement from insurance providers.

There is a clear trend toward the adoption of cloud-based SaaS platforms for computational pathology. These solutions offer lower upfront costs, easier collaboration between remote pathologists, and the scalability needed to manage the petabytes of data generated by whole-slide imaging. This model is particularly attractive for small to mid-sized laboratories.

AI is moving from the research lab into routine clinical practice. Regulatory approvals for AI algorithms that assist in primary diagnosis for cancers such as prostate, breast, and skin are increasing. This trend is driving a shift in the market toward software that can be used for clinical decision support rather than just research-oriented image analysis.

Based on product, the market is segmented into Software and Services. In 2026, the Software segment is expected to hold the largest share of the market. This segment includes whole-slide imaging software, AI-based image analysis tools, and case management systems. The dominance is driven by the critical role of these tools in enabling digital workflows and automated diagnostics.

The AI-based Image Analysis Software sub-segment is projected to witness the fastest growth, as laboratories increasingly seek to automate complex diagnostic tasks and improve the reproducibility of tissue-based assessments.

Based on application, the market is segmented into Drug Discovery & Development, Clinical Diagnostics, and Education & Research. In 2026, the Drug Discovery & Development segment is expected to hold the largest share of the market. Pharmaceutical companies were the earliest adopters of computational pathology for biomarker discovery and quantifying treatment effects in clinical trials.

The Clinical Diagnostics segment is projected to witness the fastest growth during the forecast period, as regulatory approvals expand the use of computational tools for routine cancer diagnosis in hospital settings.

North America is expected to hold the largest share of the global computational pathology market in 2026, accounting for approximately 45% of total revenue. This dominance is due to robust NIH funding for cancer research, a high concentration of leading pharmaceutical companies, and the early adoption of digital health technologies. The presence of major industry players like Danaher (Leica) and Roche also strengthens the regional market.

Asia-Pacific is projected to witness the fastest growth during the forecast period. The region is modernizing its diagnostic infrastructure at an unprecedented pace, with countries like China and India investing heavily in AI-driven healthcare solutions. The rising incidence of cancer and the need for efficient data management in large-scale clinical settings are the primary growth drivers. Key companies operating in the Asia-Pacific market include major global vendors and emerging local tech firms.

The global computational pathology market is characterized by intense competition between established medical device giants and specialized AI startups. Danaher (Leica Biosystems) and Roche (Ventana) maintain strong positions through their integrated scanner and software platforms, while firms like Proscia, Paige.AI, and PathAI lead in developing advanced AI algorithms. Competition is focused on the clinical validity of AI models, interoperability with different scanner types, and the ability to provide actionable insights at the point of care.

Strategic partnerships between scanner manufacturers and software developers are critical for creating seamless digital workflows. Companies are also investing in cloud-native architectures to improve the speed and scalability of their offerings. Key players in the global market include Roche (Ventana Medical Systems), Danaher Corporation (Leica Biosystems), Siemens Healthineers, GE HealthCare, Philips Healthcare, Nikon Corporation, Olympus Corporation (Evident), Hamamatsu Photonics K.K., Proscia Inc., Paige.AI, PathAI, Ibex Medical Analytics, Akoya Biosciences, Visiopharm A/S, and Indica Labs.

The market is projected to reach USD 2.06 billion by 2036, growing at a CAGR of 9.9% from 2026 to 2036.

AI algorithms can reduce slide review time by up to 30% while maintaining high diagnostic accuracy and reproducibility.

Cloud platforms offer lower upfront costs, easier collaboration, and the scalability needed to manage massive whole-slide image data.

The Asia-Pacific region is projected to witness the fastest growth due to rapid modernization and heavy investment in AI healthcare.

By integrating with multi-omics data, it provides holistic insights that allow for more personalized and targeted cancer treatments.

The market is expected to grow at a CAGR of 9.9% during the forecast period 2026–2036.

Drug Discovery & Development holds the largest share, as pharmaceutical companies use these tools for biomarker research.

The high capital investment for scanners and computing infrastructure is the primary restraint for smaller laboratories.

AI assists in tissue segmentation and identifying morphological features, providing critical decision support for cancer diagnosis.

The market is led by Roche, Danaher (Leica Biosystems), Siemens Healthineers, Proscia, and Paige.AI.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Product & Service

3.2.2. Market Analysis, by Deployment Mode

3.2.3. Market Analysis, by Application

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Rising Incidence of Cancer and Increasing Diagnostic Workload

4.2.1.2. Critical Shortage of Specialized Pathologists Globally

4.2.1.3. Technological Advancements in AI and Deep Learning Models

4.2.2. Restraints

4.2.2.1. High Capital Investment for Scanners and Computing Infrastructure

4.2.2.2. Complex and Evolving Regulatory Landscapes for Clinical AI

4.2.3. Opportunities

4.2.3.1. Integration with Multi-Omics Data for Holistic Precision Medicine

4.2.3.2. Expansion into Rapidly Modernizing Emerging Markets in APAC and LATAM

4.2.4. Challenges

4.2.4.1. Lack of Standardized Image Formats Across Different Manufacturers

4.2.4.2. Data Security and Privacy Concerns for Massive Patient Datasets

4.2.5. Trends

4.2.5.1. Shift Toward Cloud-Based SaaS Models for Scalability and Collaboration

4.2.5.2. Increasing Regulatory Approvals for AI in Primary Clinical Diagnosis

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Computational Pathology Market, by Product & Service

5.1. Overview

5.2. Software

5.2.1. Whole Slide Imaging (WSI) Software

5.2.2. AI-based Image Analysis Software

5.2.3. Case Management Systems

5.3. Services

5.3.1. Consulting & Implementation

5.3.2. Training & Technical Support

6. Global Computational Pathology Market, by Deployment Mode

6.1. Overview

6.2. On-premise

6.3. Cloud-based (SaaS)

7. Global Computational Pathology Market, by Application

7.1. Overview

7.2. Drug Discovery & Development

7.3. Clinical Diagnostics

7.4. Education & Research

8. Global Computational Pathology Market, by End User

8.1. Overview

8.2. Hospitals & Diagnostic Labs

8.3. Pharmaceutical & Biotechnology Companies

8.4. Academic & Research Institutes

9. Global Computational Pathology Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Netherlands

9.3.5. Italy

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. South Korea

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Dashboard

10.4. Vendor Market Positioning

10.5. Market Share Analysis, 2025

11. Company Profiles

11.1. Roche (Ventana Medical Systems)

11.2. Danaher Corporation (Leica Biosystems)

11.3. Siemens Healthineers AG

11.4. GE HealthCare Technologies Inc.

11.5. Philips Healthcare

11.6. Nikon Corporation

11.7. Olympus Corporation (Evident)

11.8. Hamamatsu Photonics K.K.

11.9. Proscia Inc.

11.10. Paige.AI

11.11. PathAI

11.12. Ibex Medical Analytics

11.13. Akoya Biosciences, Inc.

11.14. Visiopharm A/S

11.15. Indica Labs, Inc.

12. Appendix

Published Date: Jun-2026

Published Date: Jan-2025

Published Date: Mar-2019

Published Date: Nov-2022

Published Date: Jan-2025

Subscribe to get the latest industry updates