Resources

About Us

Collaborative Robots Market by Type (Power and Force Limiting, Safety Monitored Stop, Speed and Separation, Hand Guiding), Component, Payload, Application, End Use Industry, & Geography - Global Forecast to 2035

Report ID: MRSE - 104313 Pages: 210 May-2025 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 48 Hours Download Free Sample ReportThis report examines the global market for collaborative robots, focusing on how solution providers are responding to the rising labor costs, shortage of skilled workers, and the growing need for flexible automation solutions worldwide. It offers a strategic evaluation of market dynamics, forecasts growth through 2035, and assesses competitive positioning at both global and regional/country levels.

Key Market Drivers & Trends and Insights

Click here to: Get Free Sample Pages of this Report

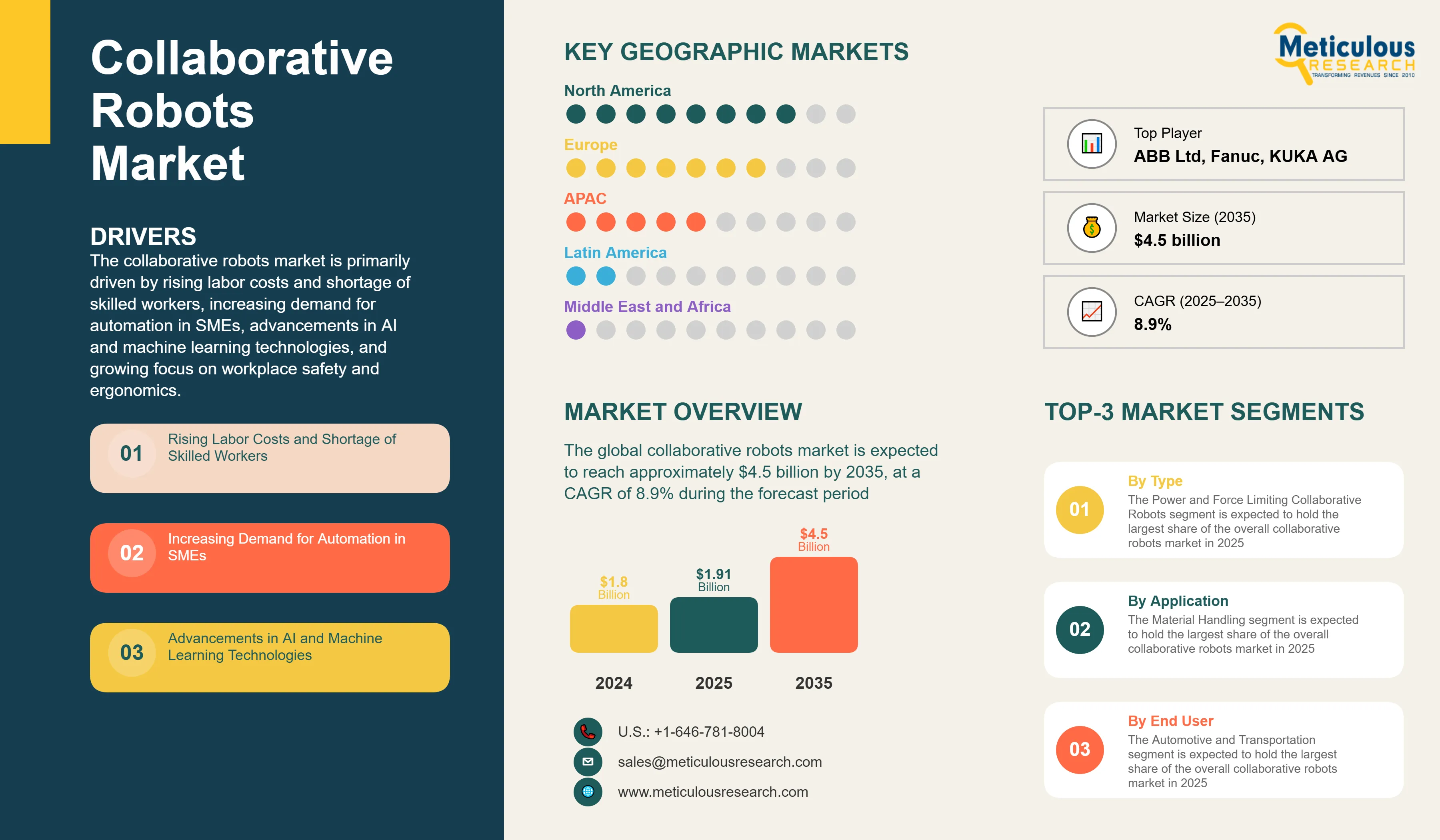

The collaborative robots market is primarily driven by rising labor costs and shortage of skilled workers, increasing demand for automation in SMEs, advancements in AI and machine learning technologies, and growing focus on workplace safety and ergonomics. The shift towards vision-guided and AI-enabled collaborative robots and cloud-based robot programming and management are reshaping the industry, while multi-arm and dual-arm collaborative systems and integration with augmented reality (AR) for training are gaining significant traction. Additionally, integration with IoT and Industry 4.0 technologies and growing applications in healthcare and life sciences are further driving market growth, especially in developed markets with advanced manufacturing infrastructure.

Key Challenges

Although the collaborative robots market holds substantial growth potential, it encounters several challenges such as high initial investment and integration costs, limited payload capacity compared to traditional robots, and slower operating speed requirements for safety. Furthermore, hurdles like safety standards and regulatory compliance across various countries, lack of standardization in safety protocols, and cybersecurity concerns in connected robotics pose significant barriers that could hinder market adoption in different parts of the world.

Growth Opportunities

The collaborative robots market presents numerous avenues for high growth. Emerging markets offer substantial expansion opportunities for market players looking to reach new customer bases. Integration with IoT and Industry 4.0 technologies provides another key opportunity, enhancing the connectivity and intelligence of robotic systems. Moreover, the development of mobile collaborative robots and growing applications in healthcare and life sciences are generating new revenue streams for solution providers as organizations seek efficient alternatives to traditional automation methods.

Market Segmentation Highlights

By Type

The Power and Force Limiting Collaborative Robots segment is expected to hold the largest share of the overall collaborative robots market in 2025, due to its inherent safety features and growing adoption in manufacturing facilities across the globe. However, the Hand Guiding Collaborative Robots segment is expected to grow at the fastest CAGR during the forecast period, driven by increasing demand for intuitive programming, ease of use, and the push for operator-friendly automation solutions.

By Component

The Hardware segment is expected to dominate the overall collaborative robots market in 2025, primarily due to the essential role of robotic arms, EOAT devices, drives, controllers, and sensors in collaborative robotics systems. However, the Software segment is expected to grow at the fastest CAGR through the forecast period, driven by increasing demand for advanced programming platforms, AI integration, and cloud-based robot management solutions.

By Payload

The Up to 5 Kg Payload segment is expected to hold the largest share of the overall collaborative robots market in 2025, due to the high demand for light-duty applications in electronics assembly and precision manufacturing. However, the More than 10 Kg Payload segment is expected to experience the fastest growth rate during the forecast period, driven by expanding applications in automotive manufacturing, heavy machinery, and material handling operations.

By Application

The Material Handling segment is expected to hold the largest share of the overall collaborative robots market in 2025, due to the widespread adoption of cobots for palletizing, depalletizing, and pick-and-place operations across industries. However, the Machine Tending segment is expected to experience the fastest growth rate during the forecast period, driven by increasing automation of CNC machines, injection molding, and other manufacturing equipment.

By End Use Industry

The Automotive and Transportation segment is expected to hold the largest share of the overall collaborative robots market in 2025, due to the high volume of automation applications and early adoption of collaborative robotics technologies. However, the Healthcare segment is expected to experience the fastest growth rate during the forecast period, driven by expanding applications in laboratory automation, pharmaceutical manufacturing, and medical device assembly.

By Geography

North America is expected to hold the largest share of the global collaborative robots market in 2025, driven by advanced manufacturing infrastructure, high labor costs, strong adoption of innovative technologies, and significant investments in industrial automation. Additionally, favorable regulatory environment and high awareness about workplace safety contribute significantly to market dominance. Europe follows as the second-largest market, bolstered by strong manufacturing sectors and increasing focus on Industry 4.0 initiatives. However, Asia-Pacific is witnessing the fastest growth rate during the forecast period, primarily driven by expanding manufacturing facilities, rising labor costs, growing awareness about automation benefits, and the advantages collaborative robots offer in improving productivity and safety.

Competitive Landscape

The global collaborative robots market is characterized by a diverse competitive environment, comprising established industrial automation companies, specialized robotics manufacturers, technology solution providers, and innovative startups, each adopting unique approaches to advancing collaborative robotics technologies.

Within this landscape, solution providers are segmented into industry leaders, market differentiators, vanguards, and emerging companies, with each group implementing distinct strategies to sustain their competitive edge. Leading companies are prioritizing integrated solutions that merge cutting-edge robotics technologies with comprehensive automation platforms, while also addressing manufacturing challenges specific to various industries.

The key players operating in the global collaborative robots market are Universal Robots A/S, Rethink Robots GmbH, ABB Ltd, Fanuc Corporation, KUKA AG, Yaskawa Electric Corporation, Kawasaki Heavy Industries, Ltd., Robert Bosch Manufacturing Solutions GmbH, Stäubli International AG, F&P Robotics AG, TechMan Robot Inc., Precise Automation, Inc., Doosan Robotics Inc., MABI Robotic AG, Energid Technologies Corporation, and AUBO Robotics USA among others.

|

Particulars |

Details |

|

Number of Pages |

210 |

|

Format |

PDF & Excel |

|

Forecast Period |

2025–2035 |

|

Base Year |

2024 |

|

CAGR (Value) |

8.9% |

|

Market Size (Value) in 2025 |

USD 1.91 Billion |

|

Market Size (Value) in 2035 |

USD 4.5 Billion |

|

Segments Covered |

Market Assessment, by Type

Market Assessment, by Component

Market Assessment, by Payload

Market Assessment, by Application

Market Assessment, by End Use Industry

|

|

Countries Covered |

North America (U.S., Canada), Asia-Pacific (China, Japan, India, South Korea, Rest of Asia-Pacific), Europe (Germany, U.K., France, Italy, Spain, Rest of Europe), Latin America, Middle East & Africa |

|

Key Companies |

Universal Robots A/S, Rethink Robots GmbH, ABB Ltd, Fanuc Corporation, KUKA AG, Yaskawa Electric Corporation, Kawasaki Heavy Industries, Ltd., Robert Bosch Manufacturing Solutions GmbH, Stäubli International AG, F&P Robotics AG, TechMan Robot Inc., Precise Automation, Inc., Doosan Robotics Inc., MABI Robotic AG, Energid Technologies Corporation, AUBO Robotics USA |

The global collaborative robots market was valued at $1.8 billion in 2024. This market is expected to reach approximately $4.5 billion by 2035, growing from an estimated $1.91billion in 2025, at a CAGR of 8.9% during the forecast period of 2025–2035.

The global collaborative robots market is expected to grow at a CAGR of 8.9% during the forecast period of 2025–2035.

The global collaborative robots market is expected to reach approximately $4.5 billion by 2035, growing from an estimated $1.91 billion in 2025, at a CAGR of 8.9% during the forecast period of 2025–2035.

The key companies operating in this market include Universal Robots A/S, Rethink Robots GmbH, ABB Ltd, Fanuc Corporation, KUKA AG, Yaskawa Electric Corporation, Kawasaki Heavy Industries, Ltd., Robert Bosch Manufacturing Solutions GmbH, Stäubli International AG, F&P Robotics AG, and others.

Major trends shaping the market include vision-guided and AI-enabled collaborative robots, cloud-based robot programming and management, multi-arm and dual-arm collaborative systems, and integration with augmented reality (AR) for training.

• In 2025, the Power and Force Limiting Collaborative Robots segment is expected to dominate the overall collaborative robots market by type

• Based on component, the Hardware segment is expected to hold the largest share of the overall market in 2025

• Based on payload, the Up to 5 Kg Payload segment is expected to hold the largest share of the overall market in 2025

• Based on application, the Material Handling segment is expected to hold the largest share of the overall market in 2025

• Based on end use industry, the Automotive and Transportation segment is expected to hold the largest share of the global market in 2025

North America is expected to hold the largest share of the global collaborative robots market in 2025, driven by advanced manufacturing infrastructure, high labor costs, and significant investments in industrial automation. Asia-Pacific is witnessing the fastest growth rate during the forecast period.

The growth of this market is driven by rising labor costs and shortage of skilled workers, increasing demand for automation in SMEs, advancements in AI and machine learning technologies, and growing focus on workplace safety and ergonomics.

Published Date: Nov-2024

Published Date: Jul-2024

Published Date: May-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates