Resources

About Us

Clocks and Timing Devices Market by Product Type (Oscillators, Resonators, Clock Generators, Clock Buffers, Jitter Attenuators), Technology (Crystal/Quartz, MEMS, SAW, Atomic Clocks), Application, and Geography — Global Forecast to 2035

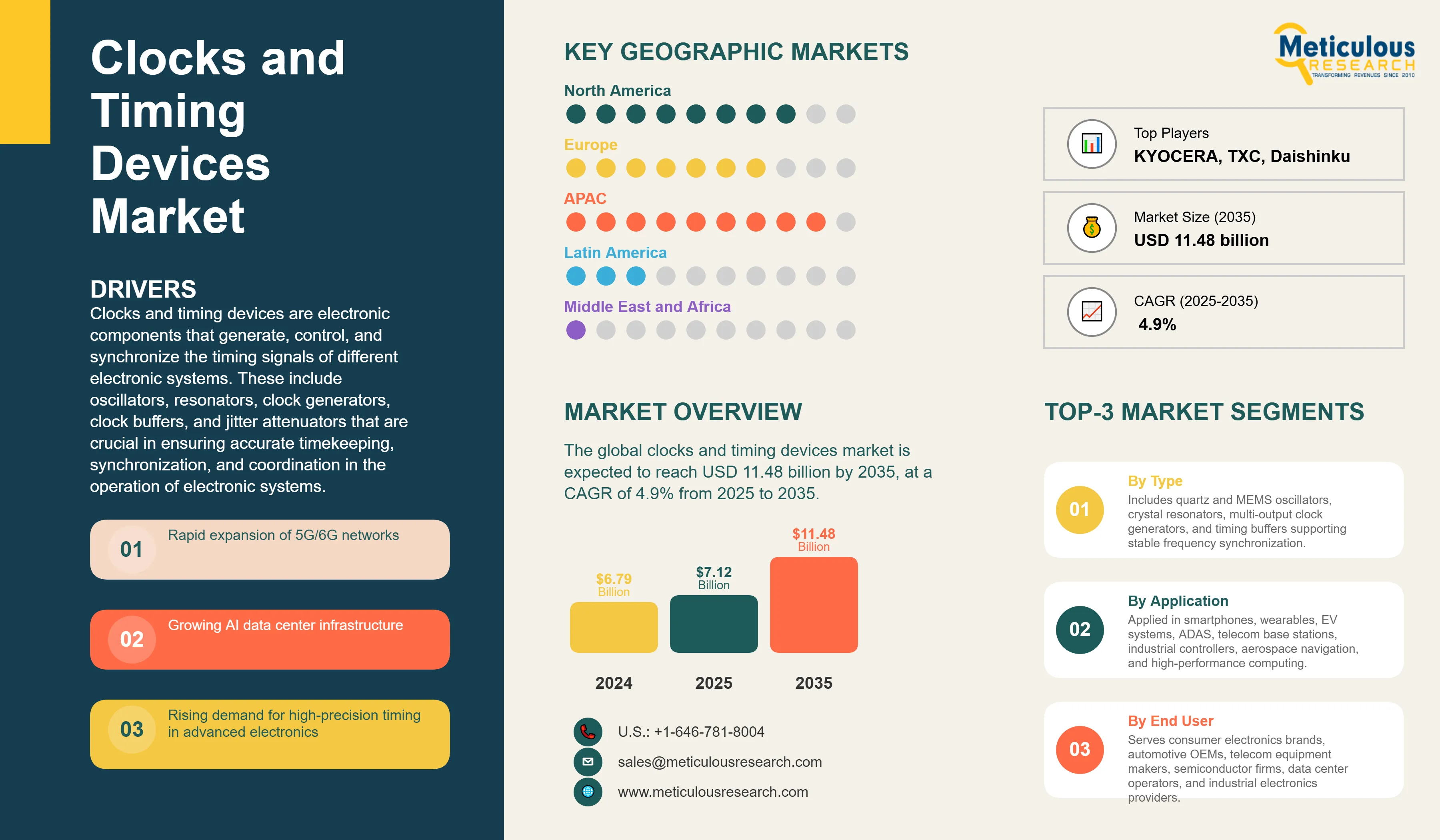

Report ID: MRSE - 1041634 Pages: 213 Dec-2025 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global clocks and timing devices market is expected to reach USD 11.48 billion by 2035 from USD 7.12 billion in 2025, at a CAGR of 4.9% from 2025 to 2035.

Clocks and timing devices are electronic components that generate, control, and synchronize the timing signals of different electronic systems. These include oscillators, resonators, clock generators, clock buffers, and jitter attenuators that are crucial in ensuring accurate timekeeping, synchronization, and coordination in the operation of electronic systems. Using the principles of the piezoelectric effect in quartz crystals, MEMS resonators, and atomic properties, timing devices produce oscillations at stable frequencies that become imperative for telecommunications networks, consumer electronics, automotive systems, industrial automation, and aerospace applications.

Key Market Highlights:

Click here to: Get Free Sample Pages of this Report

Clocks and timing devices form the fundamental technological infrastructure for precision synchronization across advanced technology applications. These electronic components provide the delivery of accurate time measurements and synchronization for complex systems, forming the basis of modern digital communication and the support of telecommunications networks, satellite navigation, automation, and scientific research. As technologies become increasingly interconnected and microsecond-level precision becomes relevant, timing devices evolve from basic mechanisms of timekeeping to integrated systems that enable technological advancement in nearly every electronic application.

A number of technological trends are revolutionizing the timing devices market, from the deployment of 5G/6G networks that require tight synchronization to the electrification and automation of vehicles demanding robust AEC-qualified timing solutions. Expansion of AI data centers, proliferation of IoT devices, and increasing electronic system complexity requiring real-time processing with continuous connectivity have made timing devices a critically important component in nearly all industry segments.

|

Parameter |

Details |

|---|---|

|

Market Size Value in 2025 |

USD 7.12 Billion |

|

Revenue Forecast in 2035 |

USD 11.48 Billion |

|

Growth Rate |

CAGR of 4.9% from 2025 to 2035 |

|

Base Year for Estimation |

2024 |

|

Historical Data |

2023–2024 |

|

Forecast Period |

2025–2035 |

|

Quantitative Units |

Revenue in USD Billion and CAGR from 2025 to 2035 |

|

Report Coverage |

Revenue forecast, company ranking, competitive landscape, growth factors, and trends |

|

Segments Covered |

Product Type, Technology, Application, End-User Industry, Region |

|

Regional Scope |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Countries Covered |

U.S., Canada, Germany, U.K., France, Italy, Netherlands, China, Japan, South Korea, Taiwan, India, Australia, Brazil, Mexico, Saudi Arabia, UAE, South Africa |

|

Key Companies Profiled |

Seiko Epson Corporation, NIHON DEMPA KOGYO CO., LTD. (NDK), KYOCERA Corporation, TXC Corporation, Daishinku Corp (KDS), SiTime Corporation, Microchip Technology Inc., Murata Manufacturing Co. Ltd., Rakon Limited, Texas Instruments Incorporated, Analog Devices Inc., Infineon Technologies AG, STMicroelectronics N.V., Renesas Electronics Corporation, Silicon Laboratories Inc., Abracon LLC, Diodes Incorporated, CTS Corporation, IQD Frequency Products Ltd., Crystek Corporation |

Key Trends Shaping the Market:

·Timing devices market is primarily driven by the rapid adoption of MEMS technology. Compared to the traditional quartz solution, MEMS oscillators offer 20× better vibration immunity and up to 50% lower power consumption for superior reliability, especially when deploying into high-volume automotive, IoT, and AI servers. SiTime Corporation's Chorus family of MEMS-based clock generators for AI data centers is said to provide up to 10× higher performance compared to discrete oscillators while shrinking board area by up to 50%.

·Another transformative trend is the integration of AI and machine learning capabilities into timing solutions. The AI-enabled timing devices will automatically tune themselves within dynamic environments so that precision timing performance is maintained for these complex systems. These solutions optimize power consumption and device responsiveness, while enabling predictive maintenance and better system performance for telecommunications, automotive, and industrial applications.

·Miniaturization continues to drive innovation in these time and frequency standards; ultra-compact oscillators are now reaching 2.0 × 1.6 mm packages without compromising ±1 ppm performance. Development of chip-scale atomic clocks (CSAC) is expanding applications in GPS-denied environments, military systems, and other critical infrastructure requiring holdover when GNSS signals are unavailable or compromised.

Market Dynamics:

Driver: 5G/6G Network Deployment and Telecommunications Expansion

The telecommunications industry is one of the largest and fastest-growing application segments for timing devices. Deployment of 5G networks and anticipation of 6G technologies require very precise timing and synchronization to accommodate higher data rates, low latency, and higher network capacity. 5G networks necessitate frequency and phase alignment within 1.5 µs to avoid uplink-downlink interference, thus fueling the adoption of TCXO/OCXO and GPS-or PTP-synchronized clocks. China's mobile operators have deployed 4.71 million 5G base stations as of September 2025, supported by cumulative investments exceeding USD 180 billion from telcos since 2020, all requiring sophisticated timing synchronization systems for performance.

Driver: AI Data Center Expansion & High-Performance Computing

The demand for precision timing solutions is being driven by the rapid growth of AI data centers. AI training fabrics integrate low-jitter MEMS oscillators per network interface card to support microsecond-grade orchestration across GPU pods. A single 64T/64R massive-MIMO panel in data centers requires up to eight high-accuracy oscillators to curb spatial stream interference. Major cloud providers have invested billions in the infrastructure of data centers, with Amazon announcing USD 13 billion for expanding data centers in Australia alone, which creates a sustained demand for advanced timing solutions to facilitate synchronized operation across distributed applications.

Opportunity: Automotive Electronics and Autonomous Driving Systems

Automotive electronics are the fastest-growing vertical for timing devices, expected to expand at more than 5.5% CAGR through 2035. The move toward electric and autonomous vehicles drives the need for robust AEC-Q100 qualified timing solutions with extended temperature ranges from -40°C to +125°C and EMI resilience for sensor fusion and domain controllers. Timing devices in modern vehicles are used in engine control, ADAS systems, infotainment, battery management, and vehicle-to-everything (V2X) communication. The shift to 77-79 GHz automotive radar invites substantial opportunities for timing device makers to utilize OCXOs with sub-100 fs jitter to avoid ghost targets.

Opportunity: IoT Ecosystem Expansion and Wearable Technology

The proliferation of IoT devices across industrial, consumer, and commercial environments presents great opportunities for growth. Connected devices require highly accurate timing for synchronization, clocking, and frequency control. Wearable health monitoring devices including smartwatches and smart rings integrate timing solutions such as real-time clocks, event counters, and timers for data timestamping, health activity monitoring, and sensor readings. Ultra-low power kHz references paired with high-accuracy MHz/GHz clocks balance sleep current targets and wake-up latency for battery-powered applications.

Segment Analysis:

By Product Type:

In 2025, the oscillators segment holds the largest share of the overall timing devices market, accounting for around 50-55% of revenue. The largest share of oscillators can be attributed to their critical function of providing accurate frequency signals in an array of electronic devices and systems. The segment includes Temperature-Compensated Crystal Oscillators (TCXOs), Voltage-Controlled Crystal Oscillators (VCXOs), Oven-Controlled Crystal Oscillators (OCXOs), and MEMS oscillators. TCXOs are the dominating type within the oscillator segment since it offers the best cost-to-performance ratio for telecom equipment that requires up to ±100 ppb stability. However, MEMS oscillators segment is the fastest-growing subsegment owing to its much-improved vibration immunity and digital programmability.

The resonators segment, meanwhile, continues to advance at a stable pace, with crystal resonators (quartz crystal units) remaining an indispensable component due to their frequency determination in cost-sensitive applications. Clock generators are gradually finding acceptance in complex systems where multiple synchronized outputs are needed.

By Technology:

Crystal/quartz technology dominates the overall market in 2025, driven by decades of reliability records and mature global fabrication capabilities. Quartz crystals provide high Q-factor and superior phase noise performance and inherent frequency stability, making them indispensable for precision applications. MEMS technology, however, is expected to grow at a higher CAGR as OEMs focus on smaller footprints, high temperature shock resistance, and digital programmability.

By Application:

Consumer electronics holds the largest market share in 2025 due to the growing demand for smartphones, tablets, wearables, smart home devices, and portable electronics that require precision timekeeping for communication and other functions. However, the automotive segment is projected to be the fastest-growing because of the increasing electronic content per vehicle, EV adoption, and autonomous driving technologies.

Regional Insights:

In 2025, the Asia-Pacific region holds the largest share of the global market for timing devices. This is due to the presence of extensive electronics manufacturing capabilities, key timing device manufacturers such as Seiko Epson, NDK, Kyocera, TXC in Japan and Taiwan, combined with fast-growing regional demand for 5G and EVs.

Key Players:

The major players in the clocks and timing devices market include Seiko Epson Corporation (Japan), NIHON DEMPA KOGYO CO., LTD. (Japan), KYOCERA Corporation (Japan), TXC Corporation (Taiwan), Daishinku Corp (Japan), SiTime Corporation (U.S.), Microchip Technology Inc. (U.S.), Murata Manufacturing Co. Ltd. (Japan), Rakon Limited (New Zealand), Texas Instruments Incorporated (U.S.), Analog Devices Inc. (U.S.), Infineon Technologies AG (Germany), STMicroelectronics N.V. (Switzerland), Renesas Electronics Corporation (Japan), Silicon Laboratories Inc. (U.S.), Abracon LLC (U.S.), Diodes Incorporated (U.S.), CTS Corporation (U.S.), IQD Frequency Products Ltd. (U.K.), and Crystek Corporation (U.S.), among others.

The market remains moderately concentrated, with the top five vendors - Seiko Epson, Kyocera, NDK, SiTime, and TXC controlling global shipments. Legacy quartz manufacturers retain share through vertically integrated operations spanning crystal growth to packaged oscillators, while MEMS-focused companies like SiTime are gaining share through design wins in AI data centers and automotive applications.

The clocks and timing devices market is expected to grow from USD 7.12 billion in 2025 to USD 11.48 billion by 2035.

The clocks and timing devices market is expected to grow at a CAGR of 4.9% from 2025 to 2035.

The major players include Seiko Epson Corporation, NIHON DEMPA KOGYO CO., LTD., KYOCERA Corporation, TXC Corporation, Daishinku Corp, SiTime Corporation, Microchip Technology Inc., Murata Manufacturing Co. Ltd., Rakon Limited, Texas Instruments Incorporated, Analog Devices Inc., Infineon Technologies AG, STMicroelectronics N.V., Renesas Electronics Corporation, Silicon Laboratories Inc., Abracon LLC, Diodes Incorporated, CTS Corporation, IQD Frequency Products Ltd., and Crystek Corporation, among others.

The main factors driving the market include 5G/6G network deployment requiring precise synchronization, expansion of AI data centers and high-performance computing infrastructure, growing adoption of automotive electronics for ADAS and autonomous vehicles, proliferation of IoT devices and smart connected products, increasing demand for consumer electronics including smartphones and wearables, and industrial automation and Industry 4.0 adoption.

Asia-Pacific region is expected to hold the largest share of the global clocks and timing devices market during the forecast period 2025 to 2035.

The oscillators segment dominates the market with around 50-55% revenue share in 2025, driven by their critical role in generating stable clock signals for precise communication and data processing across electronic devices.

Published Date: May-2026

Published Date: Mar-2026

Published Date: Feb-2026

Published Date: Apr-2026

Published Date: Dec-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates