Resources

About Us

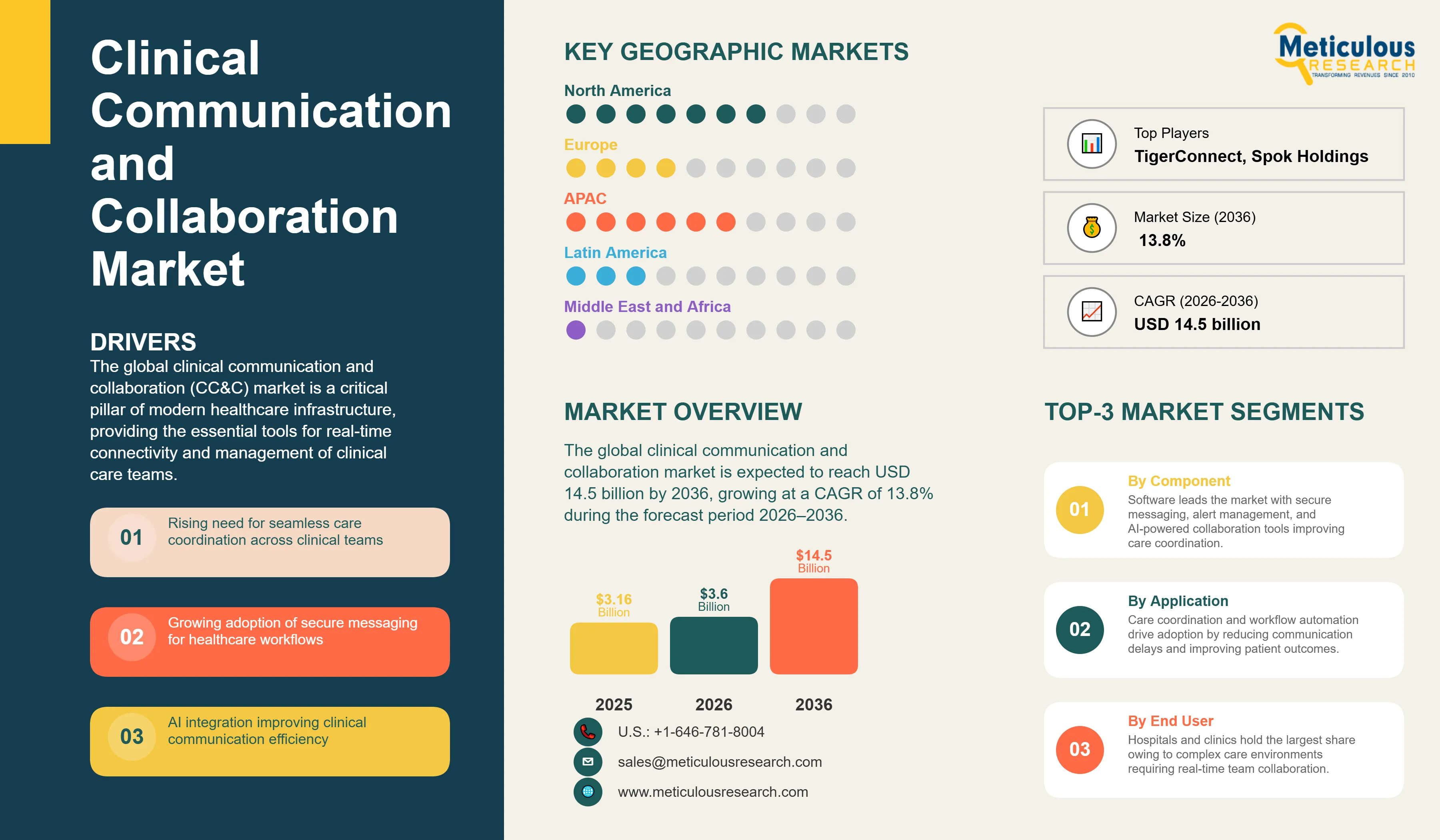

The global clinical communication and collaboration market is valued at USD 3.6 billion in 2026. This market is expected to reach USD 14.5 billion by 2036, growing at a CAGR of 13.8% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global clinical communication and collaboration (CC&C) market is a critical pillar of modern healthcare infrastructure, providing the essential tools for real-time connectivity and management of clinical care teams. CC&C solutions, including secure messaging, unified communications, and clinical alert management, enable healthcare organizations to maintain institutional integrity and clinical productivity. As of 2026, the market is undergoing a significant transformation, driven by the global imperative to address clinical communication gaps and the increasing demand for interdisciplinary care collaboration. According to industry reports, efficient clinical communication is essential for reducing medical errors and improving patient outcomes.

The transition toward integrated and AI-powered clinical collaboration platforms is essential for improving clinical workflows and care coordination in the healthcare industry. Modern CC&C solutions leverage advanced sensors and AI-driven analytics to provide a unified view of the clinical environment, ensuring that stakeholders have immediate access to actionable insights. As healthcare systems transition toward value-based care models, the demand for collaboration solutions that can demonstrably reduce communication delays and improve resource utilization is expected to surge.

Drivers: Optimizing Care Coordination to Address Rising Clinical Complexity and Communication Inefficiencies

The primary driver for the clinical communication and collaboration market is the escalating global cost of healthcare and the increasing volume of high-acuity patients, which necessitates a more efficient and data-driven approach to care team management. According to the AHA, communication failures account for significant annual losses in hospital capital budgets and patient safety. This massive financial burden is driving the adoption of integrated CC&C platforms to manage the high volume of clinical alerts and documentation. Furthermore, the shift toward mobile health (mHealth) and the increasing demand for real-time clinical communication are significant drivers. Government initiatives promoting the adoption of connected health solutions and the exchange of health information are compelling healthcare organizations to invest in CC&C solutions that can seamlessly integrate with broader healthcare IT ecosystems.

Restraints: High Implementation Costs and Technical Integration Challenges

Market growth is restrained by the high cost of implementing comprehensive clinical communication solutions and the technical challenges of achieving seamless data interoperability across disparate healthcare IT systems and EHR platforms. For many mid-sized hospitals, the initial capital investment and ongoing maintenance costs of a facility-wide CC&C network can be a significant barrier. Additionally, the lack of standardized data protocols between different technology providers often leads to data silos, making it difficult to achieve a truly unified clinical record. Concerns regarding data privacy and cybersecurity in centralized information hubs also act as deterrents to market expansion. Furthermore, the significant organizational change management and specialized training required for successful implementation can lead to slower adoption rates.

Opportunities: Advancing AI-Driven Clinical Workflow Intelligence and Connected Care Teams

The integration of artificial intelligence (AI) and machine learning (ML) into clinical communication platforms offers substantial growth opportunities. AI-powered tools can analyze complex clinical data and communication patterns to identify potential workflow bottlenecks, facilitating more precise care coordination. By 2026, AI-driven predictive analytics are being used to forecast clinical demand and optimize staff scheduling, enabling proactive resource distribution and improving patient safety. Furthermore, the shift toward cloud-native (SaaS) CC&C platforms provides healthcare organizations with superior scalability, flexibility, and lower upfront costs. Cloud-based solutions also facilitate real-time data sharing among diverse clinical specialists, supporting multi-disciplinary collaboration, which is particularly beneficial for regional healthcare networks.

Evolution toward Holistic and AI-Powered Clinical Care Orchestration

A defining trend in 2026 is the evolution of CC&C platforms from standalone messaging tools into AI-powered clinical care orchestration hubs that integrate EHRs, medical devices, monitoring systems, and care-team workflows. The shift is being driven by growing patient-safety and operational-efficiency requirements, as the World Health Organization (WHO) estimates that approximately 1 in 10 patients experiences harm during healthcare delivery, with more than 50% of such incidents considered preventable. Communication breakdowns, workflow fragmentation, and care-coordination inefficiencies remain major contributors to adverse events. As a result, healthcare providers are increasingly deploying unified collaboration platforms that leverage AI for intelligent alert prioritization, workflow automation, and clinical decision support, helping reduce administrative burden while improving care coordination and response times.

Integration of Ambient Clinical Intelligence and Virtual Nursing

The integration of ambient clinical intelligence and virtual nursing capabilities into CC&C solutions is gaining significant momentum. AI-powered ambient technologies automatically capture clinical conversations, generate documentation, and support real-time care coordination, enabling clinicians to spend more time on direct patient care. Adoption is being accelerated by persistent workforce constraints and administrative burden across healthcare systems. Recent studies of ambient documentation platforms report substantial reductions in clinician cognitive load and documentation effort, highlighting their potential to alleviate burnout and improve workflow efficiency. Combined with advances in AI-enabled sensors, edge computing, and remote patient monitoring technologies, ambient intelligence is increasingly becoming a core component of next-generation clinical collaboration platforms, particularly in high-acuity and resource-constrained care environments.

Software

Based on component, the software segment is expected to hold the largest share in 2026. This dominance is driven by the increasing demand for advanced secure messaging, clinical alert management, and AI-powered collaboration platforms. Integrated software provides a centralized 'source of truth' for clinical communication and device status, enabling more efficient regional care coordination. Key sub-segments include secure clinical messaging software, which manages patient and procedural records, and unified clinical communications platforms, which optimize procedure scheduling and resource allocation. Real-time visualization dashboards are also essential for providing care teams with immediate access to critical procedural data.

Hardware and Services

The hardware segment remains vital, providing the physical infrastructure for data collection and visualization. This includes high-resolution displays and monitors, clinical cameras and lights, and integration gateways that facilitate connectivity between disparate clinical devices. Simultaneously, the services segment—including strategic consulting, custom implementation, and post-deployment support—is growing in importance as healthcare organizations seek expert guidance for organizational change management and technical integration. As CC&C solutions become more complex, the need for comprehensive maintenance and support services is becoming a critical success factor for hospitals.

Analysis by Application

Based on application, the care coordination segment is expected to account for the largest share in 2026, reflecting the critical need for seamless communication and high-definition visualization in complex clinical procedures. Clinical workflow automation and alert management systems are also significant segments, providing the infrastructure for real-time clinical data access and interoperability. The integration of virtual nursing systems and advanced visualization tools is projected to witness the fastest growth, as hospitals prioritize minimally invasive interventions and automated clinical workflows. Patient care coordination platforms are also gaining traction, combining advanced imaging with traditional clinical environments for complex interventions.

North America is expected to dominate the global clinical communication and collaboration (CC&C) market in 2026, accounting for approximately 48.5% of total revenue. The region's leadership is supported by widespread adoption of electronic health records (EHRs), advanced healthcare IT infrastructure, and strong investment in clinical workflow optimization. According to the U.S. Office of the National Coordinator for Health Information Technology (ONC), nearly all non-federal acute care hospitals have adopted certified EHR systems, creating a foundation for integrated communication and care coordination solutions. Growing emphasis on patient safety, alarm management, clinician productivity, and interoperability continues to accelerate deployment of secure messaging and clinical collaboration platforms across hospitals and integrated delivery networks (IDNs). The presence of major vendors, including Stryker (Vocera), Oracle Health, Epic Systems, TigerConnect, and PerfectServe, further strengthens the region's market position.

Asia Pacific is projected to register the fastest growth during the forecast period. Growth is being driven by rapid healthcare digitalization, increasing hospital investments in connected care technologies, and government-led health IT modernization programs. Initiatives such as China's Healthy China strategy, India's Ayushman Bharat Digital Mission, and Australia's ongoing investments in digital health infrastructure are encouraging broader adoption of interoperable healthcare systems and care coordination platforms. Additionally, the region faces rising healthcare demand due to population growth, aging demographics, and increasing chronic disease prevalence, creating a need for more efficient clinical communication and workflow management solutions. Expanding cloud adoption and improving healthcare connectivity are expected to further accelerate CC&C implementation across hospitals and healthcare networks throughout the region.

The competitive landscape of the global clinical communication and collaboration market is characterized by intense innovation and strategic consolidations as vendors seek to provide end-to-end clinical care orchestration platforms. Leading players are differentiating themselves through the sophistication of their AI engines and their ability to provide seamless integration with EHRs and other clinical management platforms. Strategic acquisitions of niche sensor and analytics companies are a common trend as vendors seek to enhance their diagnostic capabilities. The market is also seeing increased collaboration between collaboration vendors and healthcare providers to ensure seamless clinical monitoring across the care continuum.

Key players operating in the global market include Vocera Communications (Stryker) (U.S.), TigerConnect (U.S.), Spok Inc. (U.S.), Hillrom (Baxter) (U.S.), Microsoft Corporation (Healthcare) (U.S.), Cisco Systems, Inc. (U.S.), Oracle Health (Cerner) (U.S.), Epic Systems Corporation (U.S.), Ascom Holding AG (Switzerland), NEC Corporation (Japan), Honeywell International Inc. (U.S.), and various emerging technology providers specializing in AI-driven clinical analytics and virtual nursing tools.

The market is projected to reach USD 14.5 billion by 2036, growing at a CAGR of 13.8% from 2026 to 2036.

Hospitals report a significant reduction in communication delays and an improvement in clinical workflow efficiency and patient safety.

The Artificial Intelligence & Machine Learning (AI/ML) and Clinical Workflow Intelligence segments are expected to grow the fastest.

Approximately 64% of new revenue is driven by software, with a strong shift toward AI-powered workflow orchestration.

North America holds the largest share, estimated at 48.5% in 2026, driven by high adoption of mHealth and HIPAA compliance.

AI enables the prediction of clinical demand and optimizes staff scheduling, improving resource distribution and patient safety.

The pressure to reduce medical errors and communication delays is driving the demand for integrated platforms to manage high volumes.

Hospitals and clinics are the primary adopters, managing the highest volumes of diverse integrated clinical care teams.

These systems provide the continuous, data-driven clinical management necessary to improve clinical outcomes and reduce the total cost of care.

The top 5 players are Vocera (Stryker), TigerConnect, Spok, Hillrom (Baxter), and Microsoft.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/KOL Interviews

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Component

3.2.2. Market Analysis, by Delivery Mode

3.2.3. Market Analysis, by Application

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Optimizing Care Coordination to Address Rising Clinical Complexity

4.2.1.2. Increasing Demand for Secure Clinical Messaging and Mobile Communication

4.2.1.3. Integration of AI and Machine Learning for Clinical Workflow Intelligence

4.2.2. Restraints

4.2.2.1. High Implementation Costs and Technical Integration Challenges

4.2.2.2. Data Interoperability Challenges Across Fragmented Healthcare IT Systems

4.2.3. Opportunities

4.2.3.1. Advancing AI-Driven Clinical Workflow Intelligence and Connected Care Teams

4.2.3.2. Expansion into Regional Healthcare Networks and Specialized Care Facilities

4.2.3.3. Integration of Ambient Clinical Intelligence and Virtual Nursing

4.2.4. Challenges

4.2.4.1. Managing Cybersecurity Risks in Centralized Clinical Hubs

4.2.4.2. Addressing Data Sovereignty and Privacy Regulations (GDPR/HIPAA)

4.2.4.3. Organizational Resistance to Clinical Workflow Modernization

4.2.5. Trends

4.2.5.1. Evolution toward Holistic and AI-Powered Clinical Care Orchestration

4.2.5.2. Integration of Ambient Clinical Intelligence and Virtual Nursing

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Clinical Communication and Collaboration Market, by Component

5.1. Overview

5.2. Software

5.2.1. Secure Clinical Messaging Software

5.2.2. Unified Clinical Communications Platforms

5.2.3. Clinical Alert & Notification Management

5.3. Hardware

5.3.1. Mobile Communication Devices

5.3.2. Clinical Displays and Monitors

5.3.3. Infrastructure and Integration Gateways

5.4. Services

5.4.1. Integration and Deployment Services

5.4.2. Maintenance and Support Services

6. Global Clinical Communication and Collaboration Market, by Delivery Mode

6.1. Overview

6.2. Cloud-based

6.3. On-premise

6.4. Hybrid

7. Global Clinical Communication and Collaboration Market, by Application

7.1. Overview

7.2. Physician & Nurse Communication

7.3. Lab & Radiology Communication

7.4. Clinical Alert & Emergency Notifications

7.5. Workflow Automation

8. Global Clinical Communication and Collaboration Market, by End User

8.1. Overview

8.2. Hospitals & Clinics

8.3. Ambulatory Care Centers

8.4. Long-Term Care Facilities

8.5. Specialized Care Facilities

8.6. Home Healthcare Providers

8.7. Other End Users

9. Global Clinical Communication and Collaboration Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. South Korea

9.4.5. Australia

9.4.6. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

9.6.1. GCC Countries

9.6.2. South Africa

9.6.3. Rest of Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Strategic Developments

10.3. Market Share Analysis

10.4. Competitive Benchmarking

11. Company Profiles

11.1. Vocera Communications (Stryker)

11.2. TigerConnect

11.3. Spok Holdings, Inc.

11.4. Baxter International Inc. (Voalte/Hillrom)

11.5. Microsoft Corporation

11.6. Cisco Systems, Inc.

11.7. Oracle Health (Cerner Corporation)

11.8. Epic Systems Corporation

11.9. Ascom Holding AG

11.10. NEC Corporation

11.11. Spectralink Corporation

11.12. Zebra Technologies Corporation

11.13. Everbridge, Inc.

11.14. PerfectServe, Inc.

11.15. Mobile Heartbeat (HCA Healthcare)

11.16. symplr (Halo Health & PatientSafe Solutions)

11.17. Imprivata, Inc.

11.18. Telstra Health Pty Ltd

11.19. MEDITECH

11.20. QliqSOFT, Inc.

12. Appendix

Published Date: Jun-2024

Published Date: Jun-2024

Published Date: Jan-2024

Subscribe to get the latest industry updates