Resources

About Us

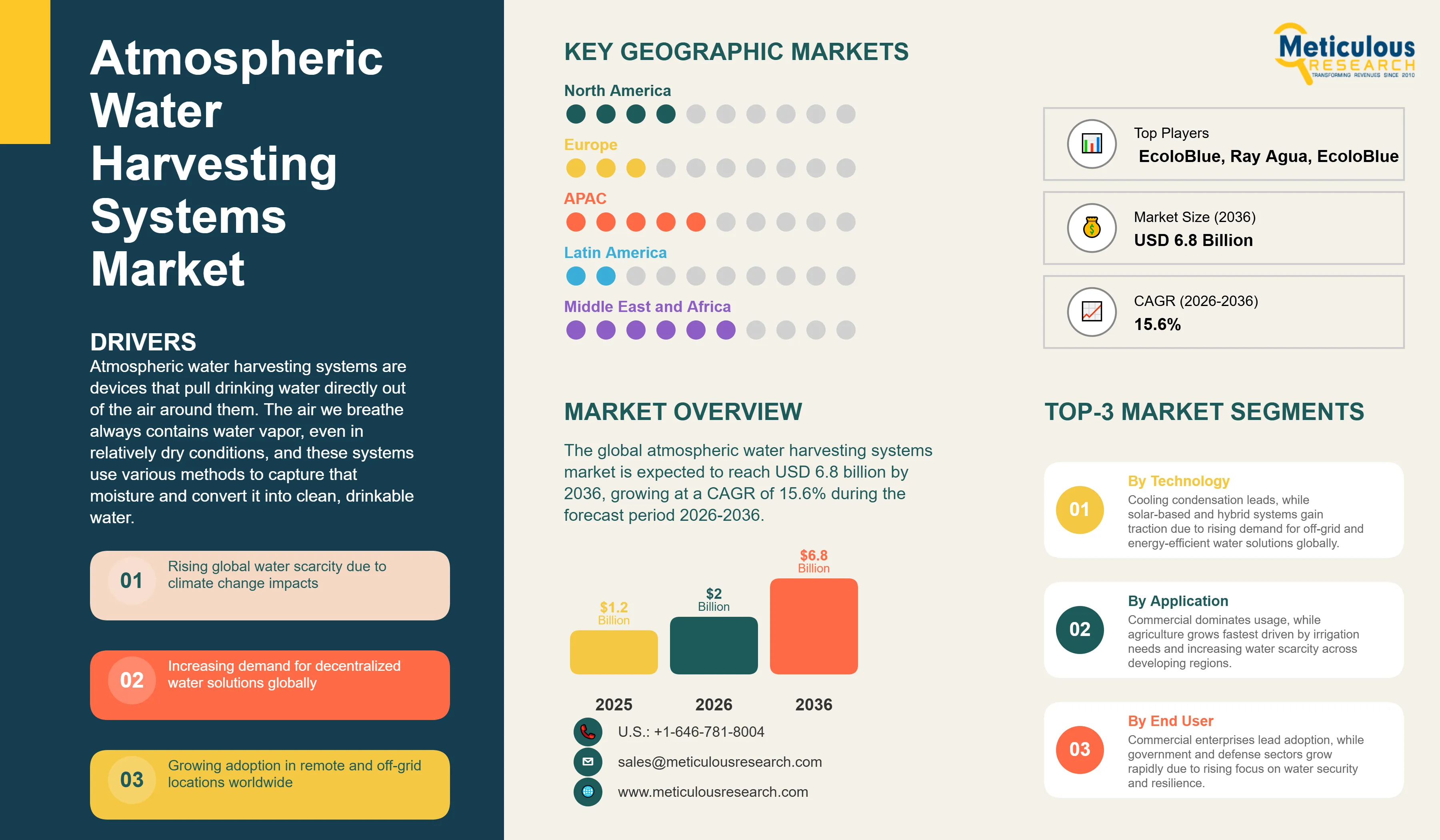

The global atmospheric water harvesting systems market was valued at USD 1.2 billion in 2025. This market is expected to reach USD 6.8 billion by 2036 from an estimated USD 1.6 billion in 2026, growing at a CAGR of 15.6% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Atmospheric water harvesting systems are devices that pull drinking water directly out of the air around them. The air we breathe always contains water vapor, even in relatively dry conditions, and these systems use various methods to capture that moisture and convert it into clean, drinkable water. The most common approach works the same way as a home dehumidifier: the system cools air below its dew point, causing the water vapor to condense into liquid water which is then filtered and purified to drinking water quality. More advanced systems use special chemical materials called desiccants that attract and absorb moisture from the air, which is then released as liquid water when the material is gently heated. The key practical advantage of atmospheric water harvesting is that it can produce clean drinking water anywhere there is air with humidity in it, without needing a well, a river, a pipeline, or a water treatment plant. For communities, military units, disaster response teams, or remote industrial facilities with no reliable water supply, this independence from traditional water infrastructure is extremely valuable.

The market is growing because water scarcity is worsening globally as a direct consequence of climate change, population growth, and the depletion of underground aquifers. The United Nations estimates that by 2030, global water demand will exceed reliable supply by 40%, and the regions most severely affected include many of the world's most populated areas in South Asia, the Middle East, Sub-Saharan Africa, and parts of Latin America and China. Traditional solutions to water scarcity such as building new dams, expanding desalination plants, or drilling deeper wells require very large infrastructure investments, take many years to build, and are not practical for isolated communities or rapidly changing water needs. Atmospheric water harvesting offers a faster and more flexible alternative that can be deployed almost anywhere within weeks, scaled up or down as needed, and operated with minimal connection to external infrastructure.

Two particularly significant opportunities are driving the next phase of market growth. The combination of solar panels with atmospheric water generators is creating water production systems that operate completely off-grid and produce both electricity and water from freely available natural resources. In sunny and humid regions including much of Southeast Asia, South Asia, the Middle East, and Sub-Saharan Africa, a solar-powered water harvesting system can provide a community's entire daily water needs without any fuel costs or grid connection, making clean water access affordable and sustainable even in very remote locations. In addition, the development of new advanced materials called metal-organic frameworks that are specifically engineered to absorb water from even very dry air, with water capture efficiencies far higher than current desiccant materials, promises to make atmospheric water harvesting viable in much drier climates than current technology can serve, significantly expanding the addressable market.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 6.8 Billion |

|

Market Size in 2026 |

USD 1.6 Billion |

|

Market Size in 2025 |

USD 1.2 Billion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 15.6% |

|

Dominating Technology Type |

Cooling Condensation Systems |

|

Fastest Growing Technology Type |

Solar-Based Systems |

|

Dominating System Type |

Standalone Systems |

|

Fastest Growing System Type |

Integrated Systems (with HVAC/Building) |

|

Dominating Application |

Commercial Applications |

|

Fastest Growing Application |

Agricultural Applications |

|

Dominating End User |

Commercial Enterprises |

|

Fastest Growing End User |

Government and Defense |

|

Dominating Capacity |

Medium Capacity Systems (100-1,000 L/Day) |

|

Fastest Growing Capacity |

Large Capacity Systems (Above 1,000 L/Day) |

|

Dominating Power Source |

Grid-Powered Systems |

|

Fastest Growing Power Source |

Solar-Powered Systems |

|

Dominating Geography |

Middle East & Africa |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Watergen Setting the Commercial Benchmark for Large-Scale Deployment

Israel-based Watergen has established itself as the global commercial leader in atmospheric water generation through a combination of proprietary heat-exchange efficiency technology, a broad product range from residential to large industrial capacity systems, and a strong track record of government and humanitarian deployment programs across multiple continents. Watergen's systems have been deployed in disaster relief operations following hurricanes and floods in the United States and Southeast Asia, in permanent installations serving communities and schools in developing countries across Africa and Asia, and in commercial and institutional applications across the Middle East. The company has received investment from South Korean conglomerate SK Group, which has helped fund global expansion, and has established distribution and project development partnerships in numerous countries.

Watergen's commercial success in diverse geographies and applications is providing the proof-of-concept validation that the broader market needs to accelerate adoption. When a major government or humanitarian organization deploys Watergen's systems at scale and reports the operational results and cost per liter of water produced, it provides credible evidence for other potential buyers that atmospheric water generation works reliably in real-world conditions at commercially acceptable cost levels. The growing library of real-world deployment case studies from operating Watergen installations is one of the most commercially important assets in the industry because it reduces the perceived technology and operational risk for new customers considering their first atmospheric water harvesting investment.

Solar Integration Making Off-Grid Water Access Economically Viable

The combination of declining solar panel costs with atmospheric water generation technology is creating a new product category of solar-powered water generators that can provide reliable clean water production in remote and off-grid locations without any ongoing fuel or electricity costs. A solar-powered atmospheric water harvesting system installed in a sunny and humid location such as coastal India, Southeast Asia, or Sub-Saharan Africa can produce hundreds of liters of clean water per day using only free solar energy, with no need for diesel fuel deliveries, grid connection, or water infrastructure. The economics of this combination have improved dramatically over the past decade as solar panel costs have fallen by more than 90%, making the capital cost of a complete solar-powered water generation system affordable for schools, health clinics, agricultural operations, and small communities that cannot access or afford conventional water supply infrastructure.

Source Global, formerly Zero Mass Water, has developed what it calls hydropanels, which are roof-mounted panels that use solar energy to drive a desiccant-based water harvesting process and produce bottled-quality drinking water with no grid connection or plumbing required. The company has deployed hydropanels at thousands of locations across dozens of countries including in schools, homes, and community buildings in water-stressed areas of the Middle East, Africa, and rural United States. The hydropanel concept demonstrates that solar-integrated atmospheric water harvesting can be packaged as a simple consumer and institutional product that delivers water independence with minimal installation complexity, representing a potentially very large mass-market product category as costs continue to fall.

Military and Disaster Relief Creating High-Value Early Adopter Markets

Military forces and humanitarian organizations represent two of the most commercially important early adopter markets for atmospheric water harvesting systems because both have urgent and recurring needs for reliable water supply in locations where conventional water infrastructure is absent or has been destroyed, and both are willing to pay premium prices for proven, deployable technology that solves a critical operational problem. A military unit operating in a remote desert environment cannot rely on civilian water supply infrastructure and faces real operational risks if its water supply is interrupted. An atmospheric water generator that can be transported by vehicle or aircraft, set up quickly, and produce safe drinking water from the ambient air regardless of the local water table conditions provides a strategically important water supply independence that military planners value highly.

The United States Department of Defense has tested and in some cases procured atmospheric water generation equipment through DARPA programs and special operations procurement, and the Israeli Defense Forces have extensive experience with Watergen's technology through their own military operations. For humanitarian organizations responding to natural disasters, the ability to deploy water generation capacity within hours of arrival at a disaster site where water infrastructure has been destroyed is operationally critical and can save lives in the critical first days and weeks after a disaster. UNICEF, the Red Cross, and several national disaster response agencies have incorporated atmospheric water generation into their emergency response equipment inventories. These high-profile military and humanitarian deployments generate important visibility and credibility for the technology and are driving increasing commercial interest from governments, municipalities, and commercial operators looking for water supply resilience solutions.

Rising Global Water Scarcity and Climate Change Impact

The most powerful driver of the atmospheric water harvesting market is the worsening global water supply situation driven by climate change, population growth, and resource depletion. More than 2 billion people currently live in countries experiencing high water stress, and the number of people facing water scarcity is projected to grow substantially through 2036 as changing rainfall patterns reduce water availability in already dry regions, glaciers and snowpack that supply river systems in Asia and South America shrink, and groundwater aquifers that took thousands of years to fill are depleted by agricultural and urban pumping at rates far exceeding natural recharge. The cities and regions most severely affected include large population centers in India, Pakistan, China, the Middle East, North Africa, and sub-Saharan Africa, which collectively represent enormous potential markets for water harvesting technology. Climate change is not a distant threat in these regions but an immediate operational reality that is already driving governments, corporations, and communities to invest urgently in water supply alternatives that do not depend on rainfall, rivers, or groundwater.

Growing Adoption in Remote and Off-Grid Locations

The practical impossibility of extending conventional water supply infrastructure to every remote settlement, mining site, agricultural operation, military base, disaster-affected community, or tourism facility creates a large and commercially accessible addressable market for self-contained water generation technology. The cost of laying water pipelines across mountainous, desert, or jungle terrain is extremely high, the time required is measured in years, and the ongoing maintenance of long infrastructure networks in remote locations is a significant operational challenge. For a remote mine, a construction camp, an eco-resort, a military forward operating base, or a community of a few hundred people in a dry rural area, the economics of purchasing and operating an atmospheric water harvesting system that produces all needed water on-site often compare very favorably with the alternative of trucking in bottled water or building dedicated water infrastructure. This practical economic advantage in off-grid situations is generating growing commercial adoption across mining companies, defense establishments, resorts, and rural development programs globally, and the addressable market expands significantly as unit costs for atmospheric water generation continue to fall with technology improvements and production scale.

Integration with Solar and Renewable Energy Systems

The pairing of atmospheric water harvesting systems with solar photovoltaic power generation represents the most commercially significant near-term opportunity in the market, creating self-contained water and energy independence packages that can be deployed in virtually any sunny and humid location without any external utility connection. As solar panel costs have fallen dramatically over the past decade to the point where solar electricity is the cheapest form of generation at most locations globally, the energy cost of running an atmospheric water generator is being dramatically reduced for systems that can use on-site solar power, making the economics of water production significantly more attractive than when systems must run on grid electricity or diesel fuel. Companies that develop optimized solar-atmospheric water harvesting packages with intelligent power management, battery storage for overnight and cloudy period operation, and simplified installation for non-technical operators are addressing a large and underserved market of communities, agricultural operations, institutions, and businesses that need both reliable electricity and water supply in locations without reliable grid or water infrastructure.

Technological Advancements in Adsorption Materials

The development of advanced adsorption materials, particularly metal-organic frameworks that can capture water from extremely dry air at relative humidities as low as 10 to 20%, represents the most technically transformative opportunity for expanding the addressable market for atmospheric water harvesting from its current base in humid and semi-humid regions to include the very dry arid and desert regions where water scarcity is most severe. Current cooling condensation systems require relatively high humidity levels of 40% or above to operate efficiently, limiting their applicability in the driest parts of the Middle East, North Africa, the Sahara, and the Atacama Desert where water need is greatest. MOF-based adsorption materials engineered at the molecular level to bind water at low humidity and release it efficiently when warmed by solar heat can operate at humidity levels far below what current technology requires, potentially bringing atmospheric water harvesting to populations in the world's driest and most water-stressed regions. MIT and the University of California Berkeley research programs, along with commercial companies including Infinite Cooling and several others, are advancing MOF-based water harvesting technology toward commercial viability, and successful commercialization could significantly expand the global addressable market for atmospheric water harvesting.

By Technology Type: In 2026, Cooling Condensation Systems to Dominate

Based on technology type, the global atmospheric water harvesting systems market is segmented into cooling condensation systems, desiccant-based systems, hybrid systems, and solar-based systems. In 2026, the cooling condensation systems segment is expected to account for the largest share of the global atmospheric water harvesting systems market. Cooling condensation is the most commercially mature and most widely deployed technology in the market, using a refrigeration cycle similar to an air conditioner to cool incoming air below its dew point and cause water vapor to condense into liquid water that is collected, filtered, and purified. This technology is well understood, uses established components that are widely manufactured and serviced globally, and produces reliable results in humid environments. The majority of commercially available atmospheric water generators from companies including Watergen, EcoloBlue, and Drinkable Air use cooling condensation as their primary water capture mechanism.

However, the solar-based systems segment is projected to register the highest CAGR during the forecast period. The rapid cost reduction of solar photovoltaic technology combined with growing demand for off-grid water solutions is driving strong adoption of solar-powered atmospheric water harvesting systems. These systems appeal to the large and fast-growing market of remote and off-grid customers for whom grid power is unavailable or unreliable, and the combination of zero fuel costs and zero water infrastructure requirements makes solar-based systems the most economically attractive option for many developing market and off-grid applications.

By System Type: In 2026, Standalone Systems to Hold the Largest Share

Based on system type, the global atmospheric water harvesting market is segmented into standalone systems, integrated systems with HVAC and building systems, and portable systems. In 2026, the standalone systems segment is expected to account for the largest share of the global atmospheric water harvesting systems market. Standalone systems that operate independently as dedicated water generation units are the most commercially established product category, covering the widest range of applications from small household units to large industrial systems. Their ability to be deployed in any location without integration with existing building infrastructure makes them the most flexible and immediately deployable option for the diverse range of customers in the market.

However, the integrated systems segment is projected to register the highest CAGR during the forecast period. The integration of atmospheric water harvesting capabilities with HVAC systems in commercial and institutional buildings, where the air handling infrastructure is already in place and the condensate from air conditioning units can be captured and purified for use rather than being drained away, represents a very efficient approach to water harvesting that is gaining traction in water-stressed urban commercial real estate markets. Large commercial buildings in cities like Singapore, Abu Dhabi, and Mumbai that operate extensive HVAC systems can capture significant volumes of water from their existing air conditioning infrastructure with relatively modest additional investment.

By Application: In 2026, Commercial Applications to Hold the Largest Share

Based on application, the global atmospheric water harvesting systems market is segmented into residential, commercial, industrial, agricultural, defense and disaster relief, and institutional applications. In 2026, the commercial applications segment is expected to account for the largest share of the global atmospheric water harvesting systems market. Commercial customers including hotels, office buildings, restaurants, and retail facilities in water-stressed regions represent a well-funded and volume-significant customer category for atmospheric water harvesting systems. Hotels in the Middle East, island resorts in Southeast Asia, and commercial facilities in water-scarce cities across India and China are purchasing water generation systems both to reduce dependence on expensive trucked or bottled water supply and to communicate sustainability credentials to environmentally conscious customers and investors.

However, the agricultural applications segment is projected to register the highest CAGR during the forecast period. Agriculture accounts for approximately 70% of global freshwater consumption, and the growing water stress in major agricultural regions including South and Southeast Asia, the Middle East, and Sub-Saharan Africa is creating strong demand for supplemental water supply technology for irrigation and livestock watering. Small and medium-scale agricultural operations in water-stressed regions that cannot access irrigation water during dry periods represent a large potential customer base for medium to large capacity atmospheric water systems, particularly solar-powered units that can provide water generation at zero ongoing energy cost.

By End User: In 2026, Commercial Enterprises to Hold the Largest Share

Based on end user, the global atmospheric water harvesting market is segmented into households, commercial enterprises, industrial users, government and defense, and NGOs and humanitarian organizations. In 2026, the commercial enterprises segment is expected to account for the largest share of the global atmospheric water harvesting systems market. Commercial businesses, particularly in the hospitality, food service, and building management sectors in water-stressed regions, represent the largest current revenue-generating customer base for atmospheric water harvesting systems. These customers have the financial means to invest in water generation equipment, have clear operational need due to water supply unreliability or high water purchase costs, and value the marketing benefit of being able to communicate that they produce their own water sustainably.

However, the government and defense segment is projected to register the highest CAGR during the forecast period. Government procurement of atmospheric water generation systems for military operations, disaster response stockpiling, rural community water supply programs, and critical infrastructure water security is growing rapidly as governments recognize the strategic importance of water supply resilience. Defense ministries investing in forward operating base water independence and civil emergency preparedness agencies building atmospheric water generation capacity into national disaster response plans represent high-value and high-volume government procurement programs that are expected to be among the fastest-growing end user categories through the forecast period.

Atmospheric Water Harvesting Systems Market by Region: Middle East and Africa Leading by Share, Asia-Pacific by Growth

Based on geography, the global atmospheric water harvesting systems market is segmented into Middle East and Africa, North America, Europe, Asia-Pacific, and Latin America.

In 2026, the Middle East and Africa region is expected to account for the largest share of the global atmospheric water harvesting systems market. This region dominates the market because it is the world's most severely water-stressed region, with many countries in the Arabian Peninsula and North Africa having essentially no renewable freshwater resources and depending entirely on desalination, groundwater depletion, or water imports to meet their needs. Saudi Arabia, the UAE, and Israel are among the most water-scarce nations on Earth on a per-capita renewable water resource basis, and these wealthy Gulf states have both the financial resources to invest in advanced water technology and the urgent operational need to diversify their water supply sources. The UAE in particular has invested heavily in water technology innovation and has been an active adopter of atmospheric water generation systems in both government and commercial applications. Israel's technology sector, home to Watergen, has a natural domestic market for advanced water solutions and the country's sophisticated approach to water resource management has made it a global leader in water technology adoption. Sub-Saharan Africa represents the largest population-weighted demand for affordable atmospheric water generation, with hundreds of millions of people lacking access to safe drinking water, and the combination of NGO, government, and increasingly commercial investment in water access solutions is creating growing procurement activity for systems appropriate for community and humanitarian deployment.

However, the Asia-Pacific atmospheric water harvesting market is expected to grow at the fastest CAGR during the forecast period. Asia-Pacific is home to the majority of the world's population and a very large fraction of the people living under water stress. India's groundwater crisis, with the Central Groundwater Board reporting that water tables in many agricultural states have fallen dramatically over recent decades, is creating acute water security challenges across the country's agricultural sector and increasingly in urban areas as well. The combination of India's very large rural population, extensive areas of water stress, growing government investment in rural water access programs, and a domestic manufacturing base including WaterMaker India and Akvo that can produce cost-competitive atmospheric water systems is making India one of the most important emerging markets for the technology. China's water stress in its northern and western regions, combined with the country's strong government investment in water security technology and its large manufacturing capability for the core components of atmospheric water systems, positions China as both a major market and a potential major production center for the global industry. Southeast Asian countries including Indonesia, Vietnam, and Thailand have high humidity that is favorable for cooling condensation systems and growing water security challenges in their agricultural and peri-urban regions.

North America is a technologically advanced and growing market for atmospheric water harvesting systems, primarily in the United States where prolonged drought conditions in the southwestern states including California, Arizona, Nevada, and Texas are creating both institutional and commercial demand for supplemental and emergency water supply technology. The U.S. military's sustained interest in atmospheric water generation for forward operating base water independence is an important demand driver, and companies including Aqua Sciences have developed products specifically for the U.S. Defense Advanced Research Projects Agency requirements. California's ongoing water crisis is driving adoption of water harvesting technology in agricultural, residential, and commercial applications across the state. Latin America is an emerging market with strong potential in water-stressed Andean and coastal regions, and Chile's mining industry and Peru's agricultural sector both represent meaningful near-term market opportunities for medium and large capacity water generation systems.

The atmospheric water harvesting systems market consists of specialist technology companies that have built water generation products as their primary business, alongside a number of emerging companies with novel technology approaches and established players expanding from adjacent water treatment and solar energy markets. Competition is based on water production efficiency measured in liters per kilowatt-hour of energy consumed, system reliability and durability in field conditions, water quality output meeting drinking water standards, ease of installation and maintenance by non-specialist operators, and price per liter of water produced at the system's intended operating conditions.

Watergen is the market leader by commercial deployment scale, with its GEN-350 and GENNY product family covering capacities from household to large institutional and commercial scales and its deployments across dozens of countries providing strong brand recognition and a growing reference customer network. Source Global, formerly Zero Mass Water, has established a distinctive position in the solar-integrated hydropanel segment with its premium-positioned residential and institutional products. SkyWater produces some of the highest-capacity cooling condensation systems available commercially, targeting large institutional and industrial applications. Genaq Technologies of Spain has built a strong European market position with its range of cooling condensation atmospheric water generators targeting commercial and institutional customers. Akvo Atmospheric Water Systems in India is a significant player in the growing South Asian market, producing cost-effective systems targeted at the Indian market's price sensitivity.

The report provides a comprehensive competitive analysis based on a thorough review of leading players' technology platforms, product portfolios, deployment track records, geographic presence, and recent strategic developments. Some of the key players operating in the global atmospheric water harvesting systems market include Watergen Ltd. (Israel), Source Global/Zero Mass Water (U.S.), SkyWater Air Water Machines (U.S.), Akvo Atmospheric Water Systems Pvt. Ltd. (India), EcoloBlue Inc. (U.S.), Atlantis Solar (Israel), Dew Point Manufacturing (U.S.), Drinkable Air Technologies (U.S.), WaterMaker India Pvt. Ltd. (India), Genaq Technologies S.L. (Spain), Hendrx Water (U.S.), PlanetsWater (Brazil), Ray Agua (Spain), Aqua Sciences (U.S.), and Water Technologies International Inc. (U.S.), among others.

The global atmospheric water harvesting systems market is expected to reach USD 6.8 billion by 2036 from an estimated USD 1.6 billion in 2026, at a CAGR of 15.6% during the forecast period 2026-2036.

In 2026, the cooling condensation systems segment is expected to hold the largest share of the global atmospheric water harvesting systems market, reflecting cooling condensation being the most commercially mature and most widely deployed technology with the largest installed base across commercial, institutional, and humanitarian applications.

The solar-based systems segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the combination of dramatically falling solar panel costs and growing demand for off-grid water solutions creating a compelling economic case for solar-powered water generation in remote and developing market applications.

In 2026, the commercial applications segment is expected to hold the largest share of the global atmospheric water harvesting systems market, driven by hotels, office buildings, and commercial facilities in water-stressed regions representing well-funded customers with clear operational need for reliable supplemental water supply.

The Middle East and Africa region is expected to dominate the global atmospheric water harvesting systems market in 2026, driven by these being the world's most severely water-stressed regions with the most acute operational need for water generation technology, backed by significant government investment and wealthy Gulf state adoption.

The market is primarily driven by worsening global water scarcity caused by climate change, population growth, and aquifer depletion creating urgent demand for water supply alternatives that do not depend on rainfall or conventional infrastructure, and by the practical advantage of atmospheric water harvesting for remote, off-grid, and disaster-affected locations where traditional water supply infrastructure is absent or unreliable.

Key players are Watergen Ltd. (Israel), Source Global/Zero Mass Water (U.S.), SkyWater Air Water Machines (U.S.), Akvo Atmospheric Water Systems Pvt. Ltd. (India), EcoloBlue Inc. (U.S.), Atlantis Solar (Israel), Dew Point Manufacturing (U.S.), Drinkable Air Technologies (U.S.), WaterMaker India Pvt. Ltd. (India), Genaq Technologies S.L. (Spain), Hendrx Water (U.S.), PlanetsWater (Brazil), Ray Agua (Spain), Aqua Sciences (U.S.), and Water Technologies International Inc. (U.S.), among others.

Asia-Pacific is expected to register the highest growth rate in the global atmospheric water harvesting systems market during the forecast period 2026-2036, driven by India's severe and worsening groundwater crisis, Southeast Asia's high humidity creating favorable technology operating conditions, and the region's very large population of people currently without reliable access to safe drinking water representing a massive long-term addressable market.

1. Introduction

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency and Limitations

1.3.1. Currency

1.3.2. Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation Process

2.2.1. Secondary Research

2.2.2. Primary Research & Validation

2.2.2.1. Primary Interviews with Experts

2.2.2.2. Approaches for Country-/Region-Level Analysis

2.3. Market Estimation

2.3.1. Bottom-Up Approach

2.3.2. Top-Down Approach

2.3.3. Growth Forecast

2.4. Data Triangulation

2.5. Assumptions for the Study

3. Executive Summary

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Rising Global Water Scarcity and Climate Change Impact

4.2.1.2. Increasing Demand for Decentralized Water Solutions

4.2.1.3. Growing Adoption in Remote and Off-Grid Locations

4.2.1.4. Government and NGO Initiatives for Clean Water Access

4.2.2. Restraints

4.2.2.1. High Initial Cost of Systems

4.2.2.2. Energy Consumption and Efficiency Limitations

4.2.2.3. Dependence on Humidity and Climate Conditions

4.2.3. Opportunities

4.2.3.1. Integration with Solar and Renewable Energy Systems

4.2.3.2. Expansion in Disaster Relief and Military Applications

4.2.3.3. Adoption in Urban Water-Stressed Regions

4.2.3.4. Technological Advancements in Adsorption Materials

4.2.4. Challenges

4.2.4.1. Scalability and Large-Scale Deployment

4.2.4.2. Maintenance and Operational Reliability

4.3. Technology Landscape

4.3.1. Cooling Condensation Technology

4.3.2. Desiccant-Based (Adsorption/Absorption) Technology

4.3.3. Hybrid Atmospheric Water Generation Systems

4.3.4. Solar-Powered Atmospheric Water Harvesting

4.3.5. Advanced Materials (MOFs, Hygroscopic Materials)

4.4. Atmospheric Water Harvesting System Architecture

4.4.1. Air Intake and Filtration Systems

4.4.2. Condensation/Adsorption Modules

4.4.3. Water Collection and Storage Systems

4.4.4. Purification and Mineralization Systems

4.4.5. Power Supply Systems (Grid/Solar/Hybrid)

4.5. Value Chain Analysis

4.5.1. Component Suppliers

4.5.2. System Manufacturers

4.5.3. Technology Providers

4.5.4. Distribution and Installation Providers

4.5.5. End Users

4.6. Regulatory and Standards Landscape

4.6.1. Drinking Water Quality Standards (WHO, EPA, etc.)

4.6.2. Environmental and Energy Efficiency Regulations

4.6.3. Government Water Sustainability Policies

4.7. Porter's Five Forces Analysis

4.8. Investment and Industry Trends

4.8.1. Investments in Water Sustainability Solutions

4.8.2. Public-Private Partnerships

4.8.3. Expansion in Emerging Markets

4.9. Cost and Pricing Analysis

4.9.1. Cost per Liter of Water Produced

4.9.2. System Cost by Capacity

4.9.3. Operational and Maintenance Costs

5. Atmospheric Water Harvesting Systems Market, by Technology Type

5.1. Introduction

5.2. Cooling Condensation Systems

5.3. Desiccant-Based Systems

5.3.1. Solid Desiccants

5.3.2. Liquid Desiccants

5.4. Hybrid Systems

5.5. Solar-Based Systems

6. Atmospheric Water Harvesting Systems Market, by System Type

6.1. Introduction

6.2. Standalone Systems

6.3. Integrated Systems (with HVAC/Building Systems)

6.4. Portable Systems

7. Atmospheric Water Harvesting Systems Market, by Application

7.1. Introduction

7.2. Residential

7.2.1. Urban Households

7.2.2. Rural and Off-Grid Homes

7.3. Commercial Applications

7.3.1. Hotels and Hospitality

7.3.2. Offices and Commercial Buildings

7.3.3. Retail and Public Spaces

7.4. Industrial Applications

7.4.1. Manufacturing Facilities

7.4.2. Food & Beverage Processing

7.5. Agricultural Applications

7.5.1. Irrigation Support

7.5.2. Livestock Water Supply

7.6. Defense and Disaster Relief

7.6.1. Military Operations

7.6.2. Emergency Response and Humanitarian Aid

7.7. Institutional Applications

7.7.1. Schools and Universities

7.7.2. Hospitals and Healthcare Facilities

8. Atmospheric Water Harvesting Systems Market, by End User

8.1. Introduction

8.2. Households

8.3. Commercial Enterprises

8.4. Industrial Users

8.5. Government and Defense

8.6. NGOs and Humanitarian Organizations

9. Atmospheric Water Harvesting Systems Market, by Capacity

9.1. Introduction

9.2. Small Capacity Systems (Up to 100 Liters/Day)

9.3. Medium Capacity Systems (100-1,000 Liters/Day)

9.4. Large Capacity Systems (Above 1,000 Liters/Day)

10. Atmospheric Water Harvesting Systems Market, by Power Source

10.1. Introduction

10.2. Grid-Powered Systems

10.3. Solar-Powered Systems

10.4. Hybrid Systems

11. Atmospheric Water Harvesting Systems Market, by Geography

11.1. Introduction

11.2. North America

11.2.1. U.S.

11.2.2. Canada

11.3. Europe

11.3.1. Germany

11.3.2. U.K.

11.3.3. France

11.3.4. Italy

11.3.5. Spain

11.3.6. Netherlands

11.3.7. Sweden

11.3.8. Rest of Europe

11.4. Asia-Pacific

11.4.1. China

11.4.2. India

11.4.3. Japan

11.4.4. South Korea

11.4.5. Australia

11.4.6. Indonesia

11.4.7. Thailand

11.4.8. Vietnam

11.4.9. Rest of Asia-Pacific

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Argentina

11.5.4. Chile

11.5.5. Colombia

11.5.6. Rest of Latin America

11.6. Middle East & Africa

11.6.1. Saudi Arabia

11.6.2. UAE

11.6.3. Israel

11.6.4. South Africa

11.6.5. Egypt

11.6.6. Rest of Middle East & Africa

12. Competitive Landscape

12.1. Overview

12.2. Key Growth Strategies

12.3. Competitive Benchmarking

12.4. Competitive Dashboard

12.4.1. Industry Leaders

12.4.2. Market Differentiators

12.4.3. Vanguards

12.4.4. Emerging Companies

12.5. Market Ranking/Positioning Analysis of Key Players, 2025

13. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

13.1. Watergen Ltd.

13.2. Source Global (Zero Mass Water)

13.3. SkyWater Air Water Machines

13.4. Akvo Atmospheric Water Systems Pvt. Ltd.

13.5. EcoloBlue, Inc.

13.6. Atlantis Solar

13.7. Dew Point Manufacturing

13.8. Drinkable Air Technologies

13.9. WaterMaker India Pvt. Ltd.

13.10. Genaq Technologies S.L.

13.11. Hendrx Water

13.12. PlanetsWater

13.13. Ray Agua

13.14. Aqua Sciences

13.15. Water Technologies International, Inc.

14. Appendix

14.1. Additional Customization

14.2. Related Reports

Published Date: Mar-2026

Published Date: Aug-2025

Published Date: May-2024

Published Date: Jan-2026

Subscribe to get the latest industry updates