Resources

About Us

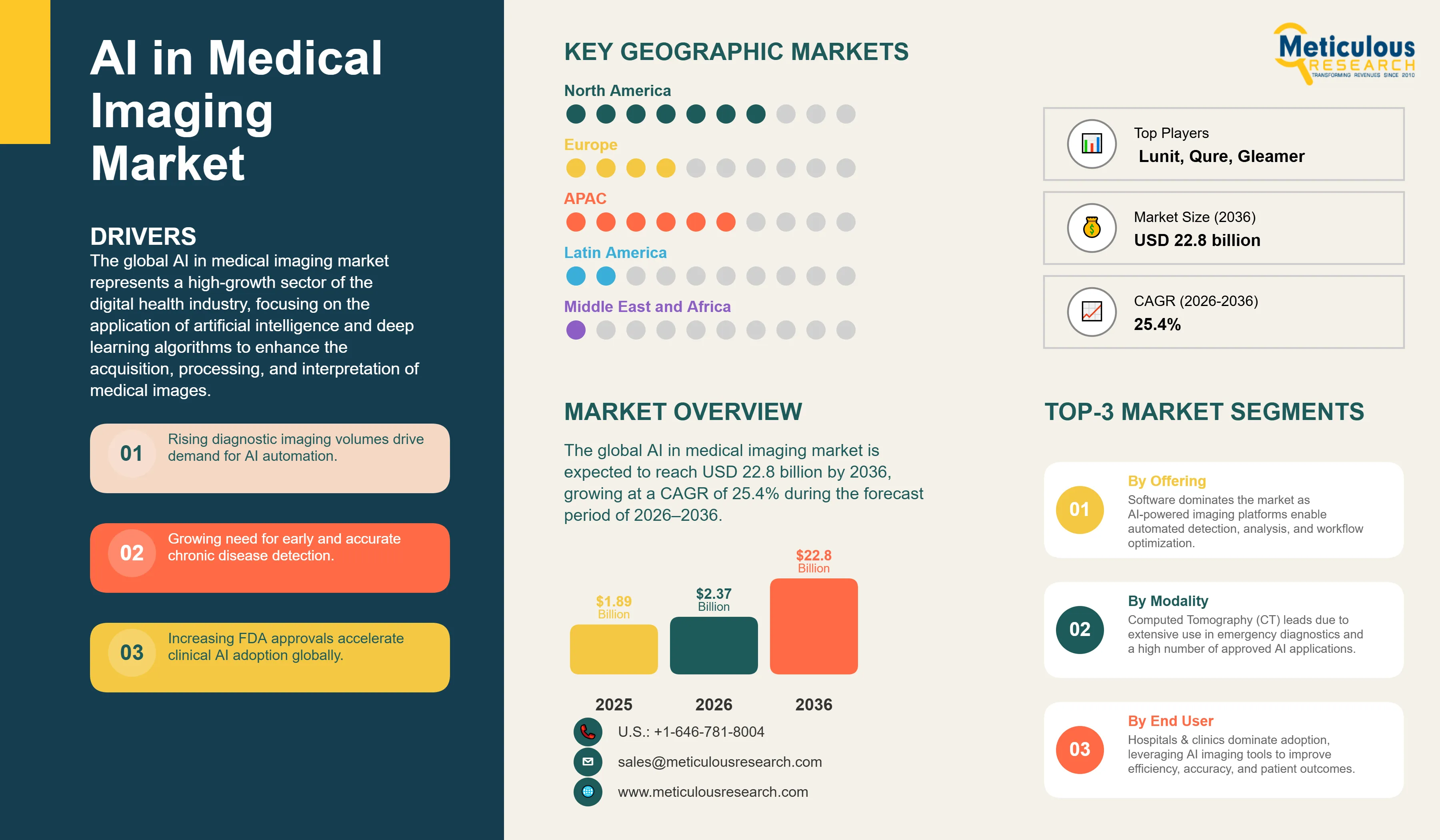

The global AI in medical imaging market was valued at USD 2.37 billion in 2026. This market is expected to reach USD 22.8 billion by 2036, growing at a CAGR of 25.4% during the forecast period of 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global AI in medical imaging market represents a high-growth sector of the digital health industry, focusing on the application of artificial intelligence and deep learning algorithms to enhance the acquisition, processing, and interpretation of medical images. These technologies are increasingly integrated into various imaging modalities, including Computed Tomography (CT), Magnetic Resonance Imaging (MRI), and X-ray, to assist radiologists in identifying subtle clinical findings and streamlining diagnostic workflows. The market is witnessing a surge in adoption as healthcare providers seek to manage the exponential growth of imaging data and address the global shortage of specialized radiologists. AI medical imaging tools range from automated detection systems for tumors and fractures to advanced software for image reconstruction and clinical triage.

The rapid growth of the overall AI in medical imaging market is primarily driven by the record volume of regulatory authorizations for AI-enabled radiology software. As of March 2026, the FDA has authorized 1,451 AI-enabled medical devices, with radiology dominating the landscape at 1,104 clearances, or approximately 76% of the total. This concentration reflects the suitability of computer vision and deep learning for analyzing structured imaging data. The FDA cleared 295 AI-enabled devices in 2025 alone, highlighting the accelerating pace of innovation and the maturing of AI algorithms for clinical use. CT and MRI remain the leading modalities for AI integration, as they provide high-resolution data that is ideal for training complex neural networks.

However, the market faces significant restraints, including the complexity of integrating AI tools into existing radiology information systems (RIS) and picture archiving and communication systems (PACS). For AI to be effective, it must be seamlessly embedded into the radiologist's daily workflow without causing disruptions. Furthermore, the high initial capital expenditure for software licenses and the necessary hardware upgrades can be a barrier for smaller diagnostic imaging centers. Despite these challenges, the shift toward triage and workflow optimization presents substantial growth opportunities. AI algorithms that can automatically flag urgent cases, such as intracranial hemorrhage or pulmonary embolism, can significantly reduce diagnostic turnaround times and improve patient outcomes in emergency settings.

Geographically, North America is expected to dominate the global AI in medical imaging market in 2026, driven by a robust ecosystem of AI startups and high clinical adoption rates in large academic medical centers. Meanwhile, the Asia-Pacific AI in medical imaging market is projected to witness the fastest growth, driven by government-led digital health initiatives and the increasing need for automated diagnostic tools in power-constrained and rural healthcare settings. The competitive landscape is characterized by intense collaboration between established medical imaging manufacturers like GE HealthCare and Siemens Healthineers and specialized AI software providers. As the industry moves toward 2036, the focus is expected to shift toward multi-modal AI and the integration of generative AI to further personalize diagnostic pathways.

The major driver for the AI in medical imaging market is the surging volume of diagnostic imaging data. As medical imaging becomes more integrated into standard clinical pathways, the number of images generated per patient has increased exponentially. AI algorithms assist radiologists by automating the detection of common findings, allowing them to focus on more complex cases. The RSNA (Radiological Society of North America) has highlighted that AI is essential for managing this 'data deluge' and maintaining diagnostic quality in an environment of increasing radiologist burnout.

Another key driver is the demand for early and more accurate diagnosis of chronic diseases. AI-enabled imaging tools have demonstrated high sensitivity in screening for conditions such as breast cancer, lung cancer, and cardiovascular diseases. By identifying subtle patterns that may be overlooked by the human eye, AI can lead to earlier interventions and significantly improved patient survival rates. Meditech Insights reports that the rising prevalence of chronic diseases globally is a fundamental driver for the adoption of AI-based screening programs.

A major restraint is the difficulty of integrating AI software into existing radiology workflows. For AI to be clinically useful, it must interact seamlessly with the PACS and RIS systems that radiologists use daily. Incompatibility between different software platforms and the lack of standardized data formats can lead to operational inefficiencies. Furthermore, the high cost of implementing AI solutions, including software licensing and the need for high-performance computing hardware, can be prohibitive for smaller hospitals and private diagnostic centers, limiting the market's reach in cost-sensitive regions.

The emergence of AI-driven clinical triage and workflow optimization presents a significant growth opportunity. AI algorithms can automatically analyze incoming scans and prioritize those with critical findings for immediate radiologist review. This is particularly valuable in emergency departments for detecting time-sensitive conditions like stroke or pulmonary embolism. Additionally, the expansion of healthcare infrastructure in emerging economies like China and India provides a large market for AI tools that can provide high-quality diagnostic support in areas with a limited number of specialized radiologists.

Ensuring the generalizability and lack of bias in AI algorithms remains a critical challenge. AI models trained on data from a single institution or demographic may not perform as well when deployed in different clinical settings or on different patient populations. Regulatory bodies like the FDA are increasingly requiring manufacturers to demonstrate the performance of their algorithms across diverse datasets. Furthermore, the evolving legal and ethical landscape regarding 'algorithmic transparency' and the liability for AI-assisted diagnostic errors poses a long-term challenge for the industry.

There is a growing trend toward using AI for image reconstruction, mainly in MRI and CT. AI algorithms can significantly speed up scan times and reduce radiation dose by reconstructing high-quality images from undersampled or low-dose data. This trend not only improves patient comfort and safety but also increases the throughput of imaging departments, allowing more patients to be scanned per day. Leading manufacturers are increasingly integrating these AI reconstruction tools directly into their imaging hardware.

The integration of generative AI and large language models (LLMs) into radiology reporting is an emerging trend. These tools can assist radiologists by automatically generating structured reports from imaging findings and providing summaries for referring physicians and patients. This has the potential to further streamline the diagnostic workflow and improve the clarity and consistency of clinical documentation.

Based on modality, the overall AI in imaging market is segmented into Computed Tomography (CT), Magnetic Resonance Imaging (MRI), X-ray, Ultrasound, and others. In 2026, the CT segment is expected to hold the largest share of the overall market. This dominance is due to the high clinical utility of CT in acute care settings and the large number of cleared AI applications for detecting vascular issues, fractures, and tumors in CT images. AI-enabled CT triage tools have become a standard of care in many emergency departments.

MRI is projected to register the highest CAGR during the forecast period. This growth is driven by the increasing adoption of AI for image reconstruction and advanced neuroimaging applications. AI's ability to reduce MRI scan times by 30-50% while maintaining image quality is a major driver for this segment, as it significantly improves the economic viability and patient experience of MRI procedures.

North America is expected to dominate the global AI in medical imaging market in 2026, primarily due to its advanced healthcare infrastructure and the high rate of clinical adoption for AI tools. The U.S. is the leading hub for radiology AI innovation, with a robust ecosystem of technology providers and research institutions. The presence of major imaging manufacturers and a supportive regulatory environment for digital health are key drivers for the region. The key companies operating in the North American market are GE HealthCare, Siemens Healthineers, Philips, Aidoc, and Viz.ai.

Asia-Pacific is projected to witness the fastest growth during the forecast period. This is driven by rapid digitalization in healthcare, increasing investments in medical technology in China and India, and government initiatives to address the radiologist shortage. China's rapid adoption of AI in screening programs and its growing base of medical imaging AI startups are major drivers for the region. The key companies operating in the Asia-Pacific market are Canon Medical Systems, Fujifilm Holdings, Samsung Medison, and various emerging AI specialists in the region.

The market is projected to reach USD 22.8 billion by 2036, growing at a CAGR of 25.4% from 2026 to 2036.

The Computed Tomography (CT) segment is expected to hold the largest share in 2026 due to its widespread clinical utility.

The surging volume of diagnostic imaging data and the global shortage of radiologists are the primary drivers.

Asia-Pacific is projected to witness the highest CAGR due to rapid digital transformation and expanding healthcare infrastructure.

AI automates routine detection tasks and triages critical cases, allowing radiologists to prioritize urgent patients and manage high workloads.

Challenges include the complexity of integration with PACS/RIS and the high initial cost of implementation.

AI algorithms can reconstruct high-quality images from less data, significantly speeding up scan times and reducing radiation dose.

Generative AI is emerging as a tool for automated clinical reporting and providing structured summaries of imaging findings.

Regulators are focusing on the generalizability of AI models across diverse populations and the transparency of 'black box' algorithms.

Leading companies include GE HealthCare, Siemens Healthineers, Philips, Canon Medical, and Fujifilm.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency and Pricing

2. Research Methodology

2.1. Research Process

2.2. Data Collection & Sources

2.2.1. Primary Research

2.2.2. Secondary Research

2.3. Market Sizing & Forecasting

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Data Triangulation & Validation

2.5. Assumptions & Limitations

3. Executive Summary

3.1. Market Overview

3.2. Segmental Analysis

3.3. Geographic Outlook

3.4. Competitive Insights

4. Market Insights

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Exponential Growth of Diagnostic Imaging Data and Radiologist Burnout

4.2.1.2. Increasing Demand for Early and Accurate Diagnosis of Chronic Diseases

4.2.2. Restraints

4.2.2.1. Complexity of Integration with PACS/RIS and Clinical Workflows

4.2.2.2. High Initial Capital Expenditure and Software Licensing Costs

4.2.3. Opportunities

4.2.3.1. Emergence of AI-Driven Clinical Triage and Workflow Prioritization

4.2.3.2. Expansion of Healthcare Infrastructure in Emerging Asia-Pacific Markets

4.2.4. Challenges

4.2.4.1. Ensuring Generalizability and Addressing Algorithmic Bias

4.2.4.2. Regulatory Complexity for Adaptive and Learning AI Algorithms

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. AI in Medical Imaging Market Assessment, by Offering

5.1. Introduction

5.2. Software

5.3. Services

6. AI in Medical Imaging Market Assessment, by Modality

6.1. Introduction

6.2. Computed Tomography (CT)

6.3. Magnetic Resonance Imaging (MRI)

6.4. X-ray

6.5. Ultrasound

6.6. Others

7. AI in Medical Imaging Market Assessment, by Application

7.1. Introduction

7.2. Diagnostic Imaging (Detection & Classification)

7.3. Triage & Workflow Optimization

7.4. Image Reconstruction & Enhancement

8. AI in Medical Imaging Market Assessment, by End User

8.1. Introduction

8.2. Hospitals & Clinics

8.3. Diagnostic Imaging Centers

8.4. Academic & Research Institutions

9. AI in Medical Imaging Market Assessment, by Geography

9.1. Introduction

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. UK

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. India

9.4.3. Japan

9.4.4. Singapore

9.4.5. Australia

9.4.6. South Korea

9.4.7. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

9.6.1. UAE

9.6.2. Saudi Arabia

9.6.3. South Africa

9.6.4. Rest of MEA

10. Competitive Landscape

10.1. Introduction

10.2. Market Share Analysis

10.3. Competitive Benchmarking

10.4. Strategic Developments

10.4.1. Product Launches & Enhancements

10.4.2. Partnerships & Collaborations

10.4.3. Mergers & Acquisitions

11. Company Profiles

11.1. GE HealthCare Technologies Inc.

11.2. Siemens Healthineers AG

11.3. Koninklijke Philips N.V.

11.4. Canon Medical Systems Corporation

11.5. Fujifilm Holdings Corporation

11.6. Agfa-Gevaert Group

11.7. Carestream Health

11.8. Hologic, Inc.

11.9. Aidoc Medical Ltd.

11.10. Viz.ai, Inc.

11.11. Tempus AI, Inc.

11.12. Nanox AI Ltd.

11.13. Lunit Inc.

11.14. Qure.ai

11.15. ScreenPoint Medical

11.16. Gleamer

11.17. ContextVision AB

11.18. DeepHealth, Inc.

11.19. Subtle Medical, Inc.

11.20. Samsung Medison Co., Ltd.

11.21. Others

12. Appendix

Published Date: Jul-2026

Published Date: Jun-2026

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: Jan-2025

Subscribe to get the latest industry updates