Resources

About Us

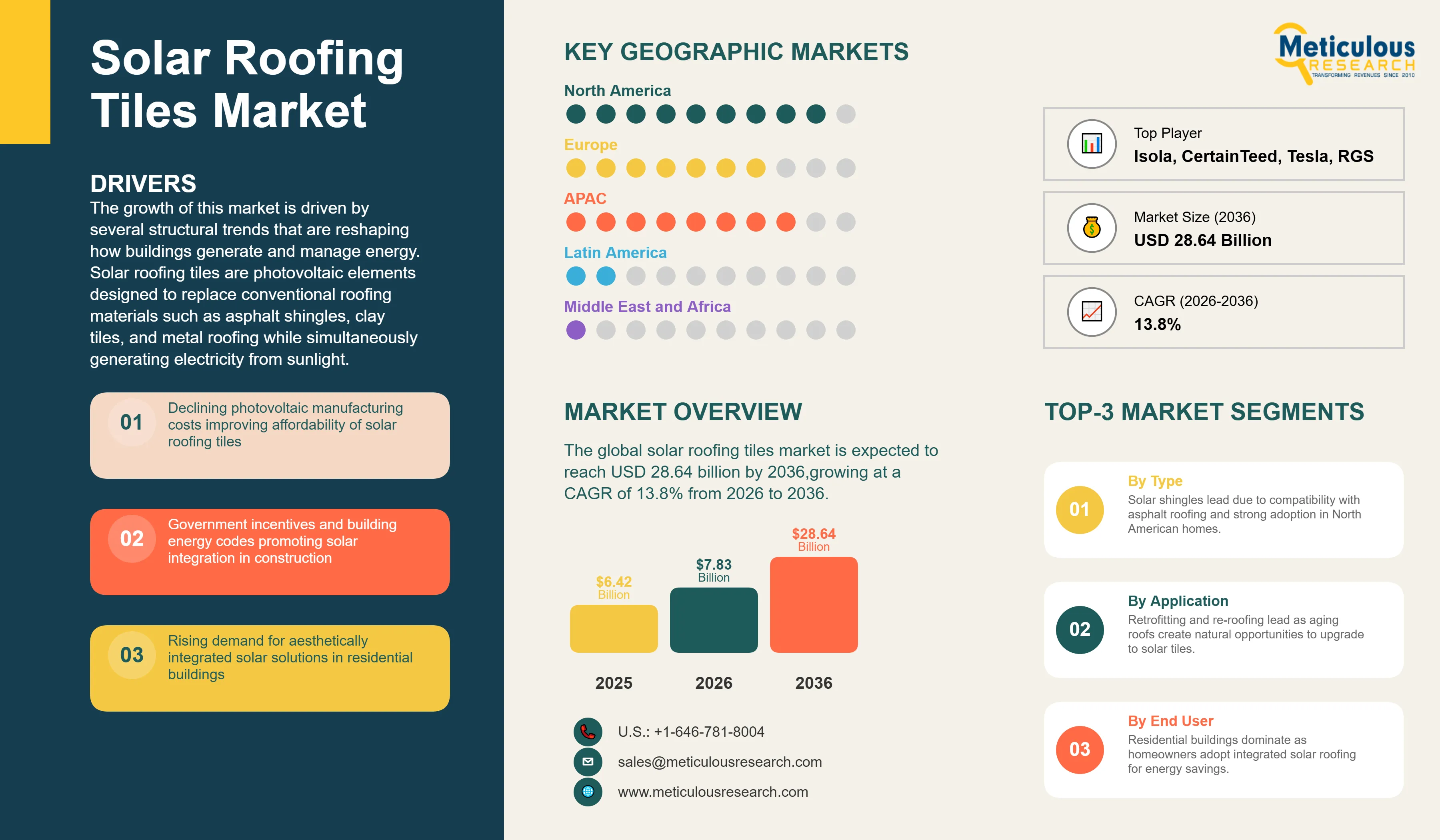

The global solar roofing tiles market was valued at USD 6.42 billion in 2025. This market is expected to reach USD 28.64 billion by 2036 from USD 7.83 billion in 2026, growing at a CAGR of 13.8% from 2026 to 2036.

The growth of this market is driven by several structural trends that are reshaping how buildings generate and manage energy. Solar roofing tiles are photovoltaic elements designed to replace conventional roofing materials such as asphalt shingles, clay tiles, and metal roofing while simultaneously generating electricity from sunlight. Unlike rack-mounted solar panels that are installed above an existing roof surface, solar tiles are integrated directly into the roof structure. This integration allows the tiles to serve as both the weatherproofing layer and a power generation system, making them an attractive alternative for property owners who want to generate solar energy without altering the visual character of their buildings.

Several factors are supporting the growth of this market. The declining cost of photovoltaic cell manufacturing is reducing the price premium of solar tiles over conventional roofing materials, making the investment more financially viable for a broader range of buyers. At the same time, growing adoption of net-zero energy building standards in national construction codes is increasing demand for integrated solar roofing in new residential and commercial construction. Rising consumer interest in aesthetically compatible solar solutions is also contributing to adoption, particularly in markets where homeowner association rules or local planning regulations restrict the use of visible rack-mounted panels. In addition, government incentive programs such as the 30% investment tax credit under the U.S. Inflation Reduction Act are reducing the financial burden of solar tile installations for homeowners and developers.

Click here to: Get Free Sample Pages of this Report

Solar roofing tiles are a category of building-integrated photovoltaics designed to replace standard roofing materials while generating electricity. The product category includes several formats. Solar shingles replicate the dimensions and installation method of standard asphalt shingles and are designed to integrate into conventional shingled roofs. Flat solar tiles resemble low-profile slate or concrete tiles and are used in both premium residential and commercial applications. Textured solar tiles mimic the three-dimensional appearance of clay barrel tiles or wood shake profiles. Solar metal roofing products integrate photovoltaic cells into standing seam metal roof panels for applications requiring a modern or industrial aesthetic.

The commercial development of this market has been significantly influenced by Tesla Energy's Solar Roof, which entered production in 2017 and established the solar shingle as a viable consumer product in the residential roofing replacement segment. Tesla's system uses tempered glass tiles that incorporate monocrystalline silicon cells on sun-facing roof sections, paired with non-active glass tiles of identical appearance on shaded sections. This approach provides full roof coverage with a consistent visual appearance from street level. Beyond Tesla, the market includes CertainTeed's Apollo II shingle product, which embeds thin monocrystalline cells into a flexible shingle format compatible with standard roofing contractor installation practices. In Europe, manufacturers such as Wienerberger, Roofit.Solar, and Tegola Solar have developed solar tile products designed for the clay and concrete tile roofing styles common in Mediterranean and Central European residential construction.

The competitive landscape of the solar roofing tiles market includes roofing materials manufacturers that have added solar capability to their product lines, solar energy companies that have developed roofing-integrated products, and specialist building-integrated photovoltaic developers. Established roofing companies benefit from existing distribution networks and contractor relationships, while solar-focused entrants bring strong expertise in photovoltaic technology and system integration. The market also relies on balance-of-system component providers such as Enphase Energy and SolarEdge, which supply microinverters and power optimizers that enable module-level energy harvesting from individual solar tiles and manage output from partially shaded or irregularly shaped roofs.

Perovskite-Silicon Tandem Cells Moving Toward Commercial Deployment

The development of perovskite-silicon tandem solar cells is one of the most significant technology trends shaping the future of the solar roofing tiles market. Tandem cell architectures stack two photovoltaic materials to capture a broader portion of the solar spectrum than single-junction silicon cells can achieve. Laboratory demonstrations of perovskite-silicon tandem cells have reached efficiencies above 33%, which is substantially higher than the 22-24% efficiency of the best commercial monocrystalline silicon cells currently used in solar tile products. Higher efficiency is particularly important for roofing tiles because the physical size of individual tiles limits how much surface area is available for power generation. A meaningful improvement in cell efficiency would allow tiles of the same size to generate significantly more electricity, improving both the system's economic return and its suitability for rooftops with limited unshaded area.

Oxford PV, a UK-based company specializing in perovskite-silicon tandem technology, began commercial production at its manufacturing facility in Brandenburg, Germany in 2023, achieving module efficiencies above 26% in initial production runs. As manufacturing processes improve and costs decline, perovskite-silicon tandem cells are expected to become available to solar tile manufacturers during the forecast period, providing an efficiency advantage over conventional silicon-only products. The main technical challenge remaining is ensuring long-term stability of perovskite materials under outdoor conditions, but progress in encapsulation techniques and perovskite composition engineering has significantly improved durability, with products demonstrating stability consistent with the 25-year performance warranties typical in the solar industry.

Building Energy Codes Driving Solar Integration in New Construction

Mandatory solar requirements in building energy codes are becoming an increasingly important demand driver for the solar roofing tiles market, particularly in the new residential construction segment. California's Title 24 energy efficiency standard, which has required solar photovoltaic systems on new low-rise residential buildings since 2020, was one of the first examples of this type of regulation and created a large market for solar roofing products in one of the world's most active residential construction markets. This regulatory approach is being adopted in other jurisdictions as governments pursue net-zero energy building targets.

In Europe, the revised Energy Performance of Buildings Directive requires member states to implement nearly zero-energy building standards across new construction, and several countries are incorporating solar generation requirements into national building regulations. Germany, France, and the Netherlands have been among the more active in developing policies that encourage or require solar installation on new buildings. Japan's revised Building Energy Efficiency Act introduced solar installation requirements for new residential construction from 2025, representing a significant new demand driver in a market known for high construction quality standards and consumer preference for clean architectural aesthetics. These regulatory developments create structural demand for solar roofing products in new construction projects, particularly where architects and developers prefer solutions that blend with the building's design rather than adding visible panel systems after the fact.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 28.64 Billion |

|

Market Size in 2026 |

USD 7.83 Billion |

|

Market Size in 2025 |

USD 6.42 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 13.8% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Product Format, System Output Range, Installation Type, Building Type, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Driver: Declining Manufacturing Costs and Favorable Roofing Replacement Economics

One of the primary drivers of the solar roofing tiles market is the sustained decline in photovoltaic cell and module manufacturing costs. Solar module prices have fallen by approximately 90% over the past decade, driven largely by scale expansion and efficiency improvements in Chinese manufacturing. This cost reduction is narrowing the price gap between solar roofing tiles and conventional roofing materials on a lifetime cost basis. For homeowners who are already planning to replace an aging roof, the incremental cost of upgrading to a solar tile system is becoming more financially manageable, particularly in markets with high electricity prices or strong net metering policies that provide good economic returns on solar generation.

The roofing replacement market creates a natural entry point for solar tile adoption. When a roof reaches the end of its service life, typically after 20 to 30 years, the homeowner must invest in replacement regardless of any interest in solar energy. At this point, choosing a solar tile system instead of a conventional roof adds solar generation capability to what would otherwise be a purely maintenance-driven expenditure. This dynamic makes the replacement roofing market a key demand channel for solar tiles, separate from the segment of homeowners who proactively seek to add solar to an otherwise serviceable roof. Government financial incentives such as the U.S. Inflation Reduction Act's 30% clean energy credit further improve the economics of solar tile adoption, reducing the effective incremental cost for eligible homeowners.

Opportunity: Heritage and Planning-Restricted Building Segments

Solar roofing tiles offer a specific capability that conventional rack-mounted panel systems cannot provide: solar energy generation from buildings where appearance regulations, listed building consent requirements, or planning permission restrictions prohibit the installation of visible panel systems. In many European cities with substantial historic building stock, planning authorities routinely reject applications for roof-mounted solar panels on buildings within conservation areas or on structures with architectural significance. This creates a defined market of property owners who are motivated to reduce energy costs and carbon emissions but have been unable to do so through conventional solar installations.

Manufacturers have responded to this opportunity by developing solar tile products that closely replicate the appearance of historic roofing materials including natural slate, plain clay tiles, and clay pantiles. Companies such as Marley Solartile and Redland Solar Slate in the United Kingdom have developed products that have received planning authority approval for use on listed buildings and in conservation areas. As the heritage and architecturally sensitive building segment represents a large number of buildings across Europe and other regions with significant historic building stock, it provides a valuable niche market where solar tiles can command premium pricing and face no direct competition from conventional panel installations.

Why Do Solar Shingles Lead the Market?

In 2026, the solar shingles segment is expected to hold the largest share of the solar roofing tiles market. The dominant position of this segment is primarily due to its strong adoption in North America, where asphalt shingles are the most widely used residential roofing material. Solar shingles are designed to install in a similar manner to conventional asphalt shingles, allowing roofing contractors familiar with standard shingle installation to work with solar tile products without extensive retraining. Tesla Energy's Solar Roof uses tempered glass shingles incorporating monocrystalline silicon cells, and CertainTeed's Apollo II embeds thin monocrystalline cells into a flexible shingle substrate. Both companies distribute their products through roofing contractor networks that already serve the large North American asphalt shingle replacement market, which makes the shingle format the most commercially accessible product format for solar tile adoption in the region.

However, the flat solar roof tiles segment is expected to witness the fastest growth during the forecast period. This growth is driven by increasing adoption in European and Asia-Pacific markets where flat tile profiles are more compatible with local roofing traditions. Manufacturers including Wienerberger with its Koramic Solesia product and Tegola Solar have developed flat solar tile lines specifically for clay and concrete tile markets that dominate residential roofing in France, Germany, Italy, Spain, and Japan. European building energy regulations requiring solar generation in new residential construction are accelerating adoption of flat solar tile formats in these markets, as architects and developers prefer products that integrate naturally with regional roofing aesthetics rather than adding a visually distinct system on top of a conventional roof.

How Does the 3 kW to 6 kW Segment Lead the Market?

In 2026, the 3 kW to 6 kW system output range is expected to hold the largest share of the solar roofing tiles market. This range corresponds to the standard residential solar tile system configuration that meets the energy consumption requirements of a typical single-family home in major markets. Most solar roofing tile manufacturers, including Tesla Energy and CertainTeed, design their residential product lines and installer training programs around this capacity range as the default system size for an average homeowner. A standard mid-sized home in the United States, Europe, or Australia typically consumes between 8,000 and 14,000 kilowatt-hours of electricity annually, and a 3 kW to 6 kW solar tile system sized to the available sun-facing roof area meets a significant portion of that demand under typical irradiance conditions. This capacity range also represents the most effective range for financial returns under most net metering tariff structures, allowing homeowners to offset a substantial share of their electricity bill without generating beyond what the grid connection allows at favorable export rates.

However, the 6 kW to 12 kW segment is expected to witness the fastest growth during the forecast period. This growth is driven by two converging trends. First, increasing household electricity consumption due to the adoption of electric vehicles and heat pumps is raising the energy offset target that homeowners want from a solar tile system, pushing average system sizing upward from the traditional 3 to 5 kW range toward 7 to 10 kW and above. Second, the growing availability of home battery storage systems such as Tesla Powerwall and Enphase IQ Battery is encouraging homeowners to install larger solar tile arrays to maximize self-consumption and battery charging. Tesla Energy actively promotes combined Solar Roof and Powerwall packages as an integrated energy system, and this bundled product strategy is increasing average system sizes across the markets where Tesla operates.

How Does Retrofit and Re-Roofing Drive the Largest Market Share?

In 2026, the retrofit and re-roofing segment is expected to hold the largest share of the solar roofing tiles market. This segment dominates because the existing stock of residential and commercial buildings far exceeds the volume of new construction in any given year, and a significant portion of that stock reaches roofing end-of-life every year, creating a continuous flow of replacement projects. Asphalt shingle roofs typically require replacement after 20 to 30 years, clay and concrete tile roofs after 30 to 50 years, and metal roofs after 40 to 70 years. This replacement cycle creates a recurring demand channel that solar tile manufacturers address by positioning their products as a premium upgrade at the point when a homeowner must invest in a new roof regardless of any interest in solar energy. The retrofit channel is also the core commercial model of established roofing manufacturers such as CertainTeed, Marley, and Redland that have added solar tile products to their existing contractor distribution networks built around the replacement roofing market.

However, the new construction segment is expected to witness the fastest growth during the forecast period. Building energy code requirements mandating solar installation on new residential construction in California, Japan, and a growing number of European jurisdictions are creating regulatory-driven demand for solar roofing in new build projects. New construction offers a more efficient installation context than retrofit because the roof deck is bare, electrical rough-in can be planned from the outset, and the combined cost of roofing and solar is evaluated together in the initial project budget rather than as a separate upgrade decision. Large production homebuilders including D.R. Horton and Lennar have developed dedicated solar tile procurement programs for their California communities, creating volume purchasing relationships with manufacturers that are beginning to produce meaningful scale effects in product cost and installer availability.

Why Do Residential Buildings Lead the Market?

In 2026, the residential buildings segment is expected to hold the largest share of the solar roofing tiles market. Residential buildings represent the primary target market for all major solar roofing tile manufacturers, as the product category was conceived and commercially developed specifically to address the residential roofing replacement market. Tesla Energy's Solar Roof is marketed exclusively to homeowners and residential developers. CertainTeed's Apollo II is distributed through residential roofing contractor networks. European manufacturers including Wienerberger, Marley, Tegola Solar, and Roofit.Solar similarly focus their go-to-market activity on residential roofing channels and consumer-facing marketing that addresses homeowner concerns about aesthetics, energy bills, and home value. The residential segment also benefits from strong government financial support in key markets, including the U.S. Inflation Reduction Act's residential clean energy credit, German KfW home improvement loan programs covering building-integrated solar, and UK home energy retrofit grant schemes that are specifically structured to support individual homeowner investments.

However, the commercial and institutional buildings segment is expected to witness the fastest growth during the forecast period. As solar tile product lines expand to include larger-format tiles and higher-wattage system configurations suitable for commercial roof areas, and as building energy regulations increasingly require solar generation on new commercial construction, developers of retail, office, hospitality, and institutional buildings are beginning to specify solar tile systems as part of their building envelope design. The heritage and architecturally sensitive sub-segment within institutional buildings is a particularly significant growth area. Schools, museums, local government offices, and places of worship that are subject to planning restrictions preventing conventional panel installations are under increasing pressure to reduce energy costs and demonstrate environmental responsibility. Specialist solar tile products approved for use on listed and heritage buildings, such as those offered by Marley Solartile and Redland Solar Slate, are gaining traction in this institutional sub-segment across the United Kingdom and Europe.

How is North America Maintaining Market Leadership?

In 2026, North America is expected to hold the largest share of the global solar roofing tiles market. This leadership is primarily driven by strong demand in the United States, where Tesla Energy's Solar Roof has established broad consumer awareness of the solar tile product category, California's Title 24 building code requirements have created a large regulatory-driven market for solar roofing in new residential construction, and the Inflation Reduction Act's 30% investment tax credit provides meaningful financial support for homeowners investing in building-integrated solar systems.

California is the largest single state market for solar roofing in the United States, driven by its solar mandate for new residential construction and its high retail electricity prices, which shorten the payback period for solar installations. Other high-solar states including Texas, Florida, Arizona, and Colorado also contribute to regional demand. Tesla's installer network, which has grown significantly since the Solar Roof's commercial launch, covers major metropolitan areas across the United States and provides installation services that are critical to consumer adoption of what is a more technically complex installation than conventional solar panels. Canada contributes to regional demand through provincial net metering programs and home retrofit incentives in provinces such as Ontario and British Columbia.

Which Factors Drive Asia-Pacific's Rapid Growth?

Asia-Pacific is expected to witness the highest growth rate in the solar roofing tiles market during the forecast period. This growth is primarily driven by regulatory developments in Japan, expanding manufacturing and deployment in China, and favorable consumer conditions in Australia.

Japan is a particularly significant growth market. The country's revised Building Energy Efficiency Act introduces solar installation requirements for new residential construction from 2025, creating large-scale demand for solar roofing products in a market known for high construction quality and consumer preference for aesthetically refined solutions. Japanese consumers and architects are likely to favor solar tile formats over conventional panel systems for new residential projects, given the strong emphasis on building aesthetics in the Japanese housing market.

China is contributing to regional growth both as a manufacturing base and as an increasingly active deployment market. Chinese manufacturers of building-integrated photovoltaic products are expanding production capacity for solar tiles, supported by domestic green building policy requirements and growing consumer interest in energy-efficient housing. LONGi Green Energy's BIPV division and other domestic producers are developing products for both the Chinese market and export.

Australia has one of the highest residential solar adoption rates in the world, with solar panels installed on more than one-third of homes. As early solar adopters in Australia approach roof replacement cycles, the combination of an existing interest in solar energy and the need for roof replacement creates a favorable environment for solar tile adoption. South Korea and India also represent growing markets, with South Korea's premium residential construction sector creating demand for advanced building materials and India's rapidly expanding residential construction market offering greenfield opportunities as green building standards develop.

Some of the key companies operating in the global solar roofing tiles market are Tesla Energy, Inc., CertainTeed LLC (Saint-Gobain), Brava Roof Tile LLC, Wienerberger AG, Roofit.Solar OY, Tegola Solar S.p.A., Isola Group AS, Marley Eternit Ltd., Redland Roofing Systems (Etex Group), LONGi Green Energy Technology Co. Ltd. (BIPV Division), Oxford PV Ltd., SunRoof Technologies sp. z o.o., RGS Energy, Soltech Energy Sweden AB, and Enphase Energy, Inc.

The global solar roofing tiles market is expected to grow from USD 7.83 billion in 2026 to USD 28.64 billion by 2036.

The global solar roofing tiles market is projected to grow at a CAGR of 13.8% from 2026 to 2036.

The solar shingles segment is expected to dominate the overall market in 2026. However, the flat solar roof tiles segment is expected to witness the fastest CAGR, driven by growing adoption in European markets where flat tile formats align with regional roofing styles and where building energy regulations are increasing demand for architecturally integrated solar solutions.

The 3 kW to 6 kW segment is expected to dominate the overall market in 2026, as it represents the standard residential system size that most manufacturers configure and quote by default. However, the 6 kW to 12 kW segment is expected to witness the fastest CAGR, driven by increasing household electricity demand from electric vehicle and heat pump adoption and by growing consumer uptake of combined solar tile and home battery storage packages.

The retrofit and re-roofing segment is expected to dominate the overall market in 2026, reflecting the large annual volume of existing roofs reaching end-of-life. However, the new construction segment is expected to witness the fastest CAGR, driven by mandatory solar requirements in building energy codes across California, Japan, and Europe that are creating structural demand for solar roofing in new residential and commercial build projects.

North America is expected to lead the global market in 2026. However, Asia-Pacific is expected to witness the fastest CAGR, driven by Japan's building code solar requirements for new residential construction, China's expanding domestic solar tile manufacturing and deployment, and Australia's strong residential solar culture creating favorable conditions for solar tile adoption during roof replacement cycles.

The major players are Tesla Energy, CertainTeed LLC (Saint-Gobain), Brava Roof Tile LLC, Wienerberger AG, Roofit.Solar OY, Tegola Solar S.p.A., Isola Group AS, Marley Eternit Ltd., Redland Roofing Systems (Etex Group), LONGi Green Energy Technology Co. Ltd., Oxford PV Ltd., SunRoof Technologies, RGS Energy, Soltech Energy Sweden AB, and Enphase Energy, Inc.

1. Introduction

1.1 Market Definition

1.2 Market Scope

1.3 Research Methodology

1.4 Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1 Introduction

3.2 Market Dynamics

3.2.1 Drivers

3.2.2 Restraints

3.2.3 Opportunities

3.2.4 Challenges

3.3 Regulatory Landscape: Building Energy Codes, Net-Zero Standards, and Solar Mandates

3.4 Technology Overview: From Silicon Cells to Perovskite-Silicon Tandem

3.5 Porter's Five Forces Analysis

4. Global Solar Roofing Tiles Market, by Product Format

4.1 Introduction

4.2 Solar Shingles

4.2.1 Glass-Faced Solar Shingles (e.g. Tesla Solar Roof)

4.2.2 Flexible Laminate Solar Shingles (e.g. CertainTeed Apollo II)

4.3 Flat Solar Roof Tiles

4.3.1 Slate-Profile Solar Tiles

4.3.2 Plain Clay and Concrete Profile Solar Tiles

4.4 Textured and Profiled Solar Roof Tiles

4.4.1 Clay Barrel and Roman Profile Solar Tiles

4.4.2 Dimensional and Wood Shake Profile Solar Tiles

4.5 Solar Metal Roofing

4.5.1 Standing Seam Integrated Solar Metal Panels (e.g. Roofit.Solar)

4.5.2 Corrugated and Trapezoidal Solar Metal Sheets

5. Global Solar Roofing Tiles Market, by System Output Range

5.1 Introduction

5.2 Below 3 kW (Small Residential and Supplementary Systems)

5.3 3 kW to 6 kW (Standard Residential Systems)

5.4 6 kW to 12 kW (Large Residential and Premium Systems)

5.5 Above 12 kW (Commercial and Multi-Family Systems)

6. Global Solar Roofing Tiles Market, by Installation Type

6.1 Introduction

6.2 New Construction

6.3 Retrofit and Re-Roofing

6.4 Renovation of Heritage and Planning-Restricted Buildings

7. Global Solar Roofing Tiles Market, by Building Type

7.1 Introduction

7.2 Residential Buildings

7.3 Commercial and Industrial Buildings

7.4 Heritage and Architecturally Sensitive Buildings

8. Global Solar Roofing Tiles Market, by Region

8.1 Introduction

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 Germany

8.3.2 United Kingdom

8.3.3 France

8.3.4 Italy

8.3.5 Spain

8.3.6 Netherlands

8.3.7 Rest of Europe

8.4 Asia-Pacific

8.4.1 China

8.4.2 Japan

8.4.3 Australia

8.4.4 South Korea

8.4.5 India

8.4.6 Rest of Asia-Pacific

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Rest of Latin America

8.6 Middle East & Africa

8.6.1 UAE

8.6.2 Saudi Arabia

8.6.3 South Africa

8.6.4 Rest of Middle East & Africa

9. Competitive Landscape

9.1 Overview

9.2 Key Growth Strategies

9.3 Competitive Benchmarking

9.4 Competitive Dashboard

9.4.1 Industry Leaders

9.4.2 Market Differentiators

9.4.3 Vanguards

9.4.4 Emerging Companies

9.5 Market Ranking/Positioning Analysis of Key Players, 2025

10. Company Profiles

(Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1 Tesla Energy, Inc. (Solar Roof)

10.2 CertainTeed LLC (Saint-Gobain) - Apollo II Solar Shingles

10.3 Brava Roof Tile, LLC

10.4 Wienerberger AG (Koramic Solesia Solar Roof Tile)

10.5 Roofit.Solar OY

10.6 Tegola Solar S.p.A.

10.7 Isola Group AS (Isola Solar)

10.8 Marley Eternit Ltd. (Marley Solartile)

10.9 Redland Roofing Systems (Etex Group)

10.10 LONGi Green Energy Technology Co., Ltd. (BIPV Division)

10.11 Oxford PV Ltd.

10.12 SunRoof Technologies sp. z o.o.

10.13 RGS Energy

10.14 Soltech Energy Sweden AB

10.15 Enphase Energy, Inc.

11. Appendix

11.1 Questionnaire

11.2 Related Reports

Published Date: May-2024

Published Date: Jun-2024

Subscribe to get the latest industry updates