Resources

About Us

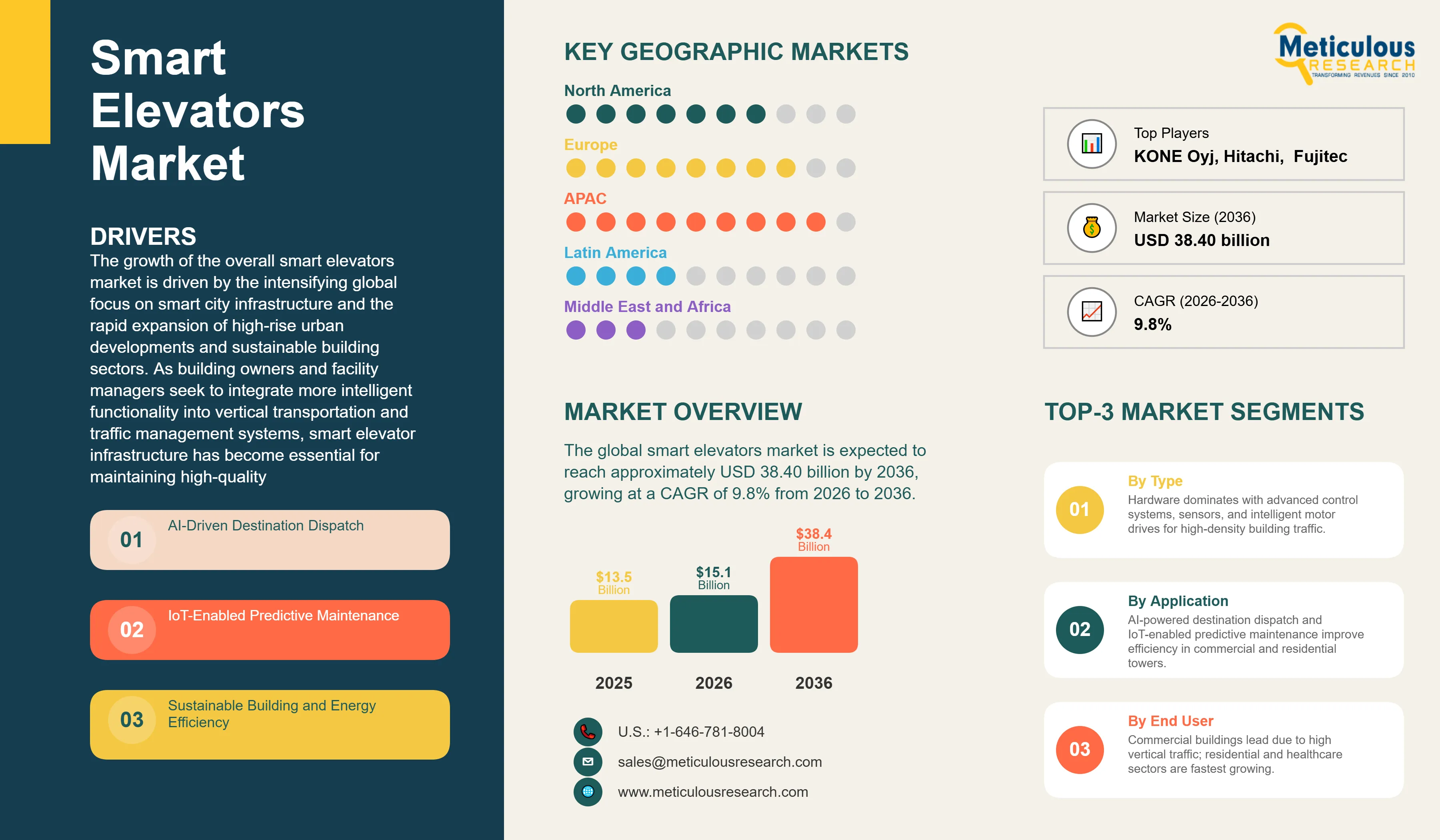

The global smart elevators market was valued at USD 13.50 billion in 2025. The market is expected to reach approximately USD 38.40 billion by 2036 from USD 15.10 billion in 2026, growing at a CAGR of 9.8% from 2026 to 2036. The growth of the overall smart elevators market is driven by the intensifying global focus on smart city infrastructure and the rapid expansion of high-rise urban developments and sustainable building sectors. As building owners and facility managers seek to integrate more intelligent functionality into vertical transportation and traffic management systems, smart elevator infrastructure has become essential for maintaining high-quality user experiences and operational efficiency. The rapid expansion of 5G infrastructure and the increasing need for real-time predictive maintenance in high-traffic commercial and residential buildings continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Smart elevators are critical vertical transportation environments that leverage advanced digital technologies to provide optimized transit processes and improved passenger experiences through a connected building infrastructure. These systems include integrated hardware, software, and services designed to automate traffic flows and enhance decision-making across the building management continuum. The market is defined by high-efficiency technologies such as AI-powered destination dispatch and IoT-enabled predictive diagnostics, which significantly enhance transit precision and resource utilization in high-pressure urban environments. These systems are indispensable for facility administrators seeking to optimize their internal operations and meet aggressive passenger safety and efficiency targets.

The market includes a diverse range of solutions, ranging from simple touchless control panels for residential buildings to complex multi-car systems and AI-driven traffic management platforms for mega-tall skyscrapers. These systems are increasingly integrated with advanced components such as cloud-based data platforms and 5G-enabled connectivity to provide services such as real-time elevator tracking and predictive maintenance of mechanical components. The ability to provide stable, high-precision transit while minimizing wait times has made smart elevator technology the choice for institutions where vertical mobility and operational reliability are paramount.

The global construction sector is pushing hard to modernize facility capabilities, aiming to meet AI-driven smart building targets and carbon-neutral goals. This drive has increased the adoption of high-speed connectivity solutions, with advanced 5G networks helping to stabilize data transmission for real-time diagnostics. At the same time, the rapid growth in the luxury residential and premium commercial markets is increasing the need for high-reliability, secure digital solutions.

Proliferation of AI-Driven Destination Dispatch and Predictive Analytics

Building managers across the industry are rapidly shifting to AI-optimized traffic workflows, moving well beyond traditional floor calling toward predictive and intelligent dispatch setups. Otis’s latest AI-powered platforms deliver significantly higher transit efficiency, while Schindler’s recent installations have slashed wait times in busy office towers. The real game-changer comes with “smart” dispatch systems featuring integrated behavioral analytics that maintains peak transit efficiency even in high-volume urban environments. These advancements make high-precision vertical mobility practical and cost-effective for everyone from luxury apartments to global financial centers chasing excellence in user experience and lower operational costs.

Innovation in Touchless Interfaces and Sustainable Power Solutions

Innovation in touchless interfaces and sustainable power solutions is rapidly driving the smart elevators market, as building operations become more hygiene-sensitive and facility operations more automated. Equipment suppliers are now designing units that combine the reliability of traditional hoistways with the intelligence of gesture-based or mobile-app controls in a single platform, saving valuable transit time and simplifying building logistics. These systems often involve advanced regenerative drives and integrated energy management capable of handling complex power requirements without compromising passenger safety or mechanical reliability.

At the same time, growing focus on sustainable building is pushing manufacturers to develop smart elevator solutions tailored to energy efficiency and waste reduction principles. These systems help reduce environmental impact through smart building automation and the use of recyclable mechanical components. By combining high-density data connectivity with robust environmental performance, these new designs support both technological advancement and corporate sustainability, strengthening the resilience of the broader construction value chain.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 38.40 Billion |

|

Market Size in 2026 |

USD 15.10 Billion |

|

Market Size in 2025 |

USD 13.50 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 9.8% |

|

Dominating Region |

Asia-Pacific |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Component, Service, Technology, End-user Industry, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Smart City Initiatives and the Rise of High-Rise Urbanization

A key driver of the smart elevators market is the rapid movement of the global construction industry toward digital-first, sustainable urban models. Global demand for seamless passenger journeys, real-time transit monitoring, and data-driven maintenance has created significant incentives for the adoption of smart elevator infrastructure. The trend toward “smart buildings” and the integration of building devices into unified digital platforms drive owners toward scalable solutions that smart elevators can uniquely provide. It is estimated that as urban adoption of IoT-enabled devices rises and management tools become more decentralized through 2036, the need for robust, connected infrastructure increases significantly; therefore, AI-driven software and high-speed connectivity, with their ability to ensure high-density data processing, are considered a crucial enabler of modern vertical mobility delivery strategies.

Opportunity: 5G Integration and Expansion of Modernization Projects

The rapid growth of the 5G network market and building modernization technologies provides great opportunities for the smart elevators market. Indeed, the global surge in 5G deployment has created a compelling demand for systems that can handle massive data throughput and provide ultra-low latency for remote monitoring. These applications require high reliability, data security, and the ability to handle high-bandwidth diagnostics, all attributes that are met with advanced smart elevator solutions. The modernization market is set to expand significantly through 2036, with smart elevators poised for an expanding share as owners seek to maximize building value and minimize operational costs. Furthermore, the increasing demand for AI-driven traffic analytics and smart security integration is stimulating demand for modular digital solutions that provide high-speed data transmission and operational flexibility.

Why Does the Hardware Segment Lead the Market?

The hardware segment accounts for a significant portion of the overall smart elevators market in 2026. This is mainly attributed to the versatile use of this technology in supporting advanced control systems, high-precision sensors, and intelligent motor drives within modern building environments. These systems offer the most comprehensive way to ensure physical transit across diverse building applications. The commercial and residential sectors alone consume a large share of smart elevator hardware, with major projects in Asia-Pacific and North America demonstrating the technology’s capability to handle high-density traffic requirements. However, the software segment is expected to grow at a rapid CAGR during the forecast period, driven by the growing need for robust AI-driven dispatch, remote monitoring platforms, and cybersecurity consulting in complex building digital transformations.

How Does the Commercial Segment Dominate?

Based on end-user industry, the commercial segment holds the largest share of the overall market in 2026. This is primarily due to the massive volume of vertical traffic and the rigorous transit standards required for premium office towers and hotels. Current large-scale commercial developments are increasingly specifying high-density digital platforms to ensure compliance with global building standards and tenant expectations for efficient transit services.

The residential and healthcare segment is expected to witness the fastest growth during the forecast period. The shift toward AI-enhanced safety and the complexity of multi-modal building suites are pushing the requirement for advanced smart systems that can handle varied traffic formats and high-resolution monitoring while ensuring absolute reliability for safety-critical vertical mobility decisions.

Why Does the Internet of Things (IoT) Lead the Market?

The Internet of Things (IoT) segment commands the largest share of the global smart elevators market in 2026. This dominance stems from its superior ability to connect vast amounts of sensor data, provide real-time monitoring, and automate routine maintenance tasks, making it the technology of choice for high-performance smart elevators. Large-scale operations in traffic management, remote diagnostics, and energy optimization drive demand, with advanced platforms from providers like Otis and Kone enabling reliable performance in complex building environments.

However, the artificial intelligence (AI) segment is poised for steady growth through 2036, fueled by expanding applications in predictive analytics and behavioral traffic modeling. Manufacturers face mounting pressure to optimize costs for high-volume, less demanding applications, where AI provides a high-value alternative for advanced facility connectivity.

How is Asia-Pacific Maintaining Dominance in the Global Smart Elevators Market?

Asia-Pacific holds the largest share of the global smart elevators market in 2026. The largest share of this region is primarily attributed to the massive urban infrastructure and the presence of the world’s leading construction innovators, particularly in China. China alone accounts for a significant portion of global smart elevator investment, with its position as a leading adopter of smart city technologies driving sustained growth. The presence of leading manufacturers like Mitsubishi Electric and a well-developed building supply chain provides a robust market for both standard and high-density smart solutions.

Which Factors Support North America and Europe Market Growth?

North America and Europe together account for a substantial share of the global smart elevators market. The growth of these markets is mainly driven by the need for technological modernization in the aging building sectors. The demand for advanced smart systems in North America is mainly due to its large-scale high-rise infrastructure projects and the presence of innovators in the U.S.

In Europe, the leadership in precision engineering and the push for green building innovation are driving the adoption of high-reliability smart solutions. Countries like Germany, France, and the UK are at the forefront, with significant focus on integrating smart digital solutions into building workflows and advanced urban management systems to ensure the highest levels of performance and reliability.

The companies such as Otis Worldwide Corporation, Schindler Group, KONE Oyj, and ThyssenKrupp Elevator (TK Elevator) lead the global smart elevators market with a comprehensive range of digital and AI-driven solutions, particularly for large-scale urban applications and high-speed transit. Meanwhile, players including Mitsubishi Electric Corporation, Hitachi, Ltd., Fujitec Co., Ltd., and Toshiba Elevator and Building Systems Corporation focus on specialized control systems, regenerative drives, and IoT platforms targeting the premium commercial and high-rise sectors. Emerging manufacturers and integrated players such as Hyundai Elevator Co., Ltd., Delfar Elevator Co., Ltd., Joylive Elevator, and Sigma Elevator Company are strengthening the market through innovations in connected devices and modular digital platforms.

The global smart elevators market is expected to grow from USD 15.10 billion in 2026 to USD 38.40 billion by 2036.

The global smart elevators market is projected to grow at a CAGR of 9.8% from 2026 to 2036.

Hardware is expected to dominate the market in 2026 due to its superior ability to support advanced control systems and sensors. However, the software segment is projected to be the fastest-growing segment owing to the increasing need for AI-driven dispatch and remote monitoring in complex building environments.

AI and 5G are transforming the smart elevator landscape by demanding higher data integrity, lower latency, and improved predictive maintenance. These technologies drive the adoption of advanced platforms like cloud-based data lakes and real-time monitoring systems, enabling building owners to support the complex workflows and high-frequency requirements of next-generation digital buildings.

Asia-Pacific holds the largest share of the global smart elevators market in 2026. The largest share of this region is primarily attributed to the massive urban infrastructure and the presence of leading construction innovators in China. Asia-Pacific is also expected to witness the fastest growth, driven by massive investments in smart city modernization.

The leading companies include Otis Worldwide Corporation, Schindler Group, KONE Oyj, TK Elevator, and Mitsubishi Electric.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Research Methodology

1.4. Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1. Introduction

3.2. Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.2.4. Challenges

3.3. Impact of Smart City Initiatives on Vertical Transportation

3.4. Regulatory Landscape & Building Safety Standards (EN 81, ASME A17.1)

3.5. Porter’s Five Forces Analysis

4. Global Smart Elevators Market, by Component

4.1. Introduction

4.2. Hardware

4.2.1. Control Systems

4.2.2. Sensors & Actuators

4.2.3. Motors & Drives

4.2.4. Display & Interface Units

4.3. Software

4.3.1. Traffic Management Software

4.3.2. Maintenance & Diagnostic Software

4.3.3. Security & Access Control Software

4.4. Services

4.4.1. Installation & Integration

4.4.2. Maintenance & Support

4.4.3. Consulting & Training

5. Global Smart Elevators Market, by Service

5.1. Introduction

5.2. New Installation

5.3. Modernization

5.4. Maintenance & Repair

6. Global Smart Elevators Market, by Technology

6.1. Introduction

6.2. Internet of Things (IoT)

6.3. AI & Predictive Analytics

6.4. Cloud Computing

6.5. Biometrics & Access Control

6.6. 5G & High-speed Connectivity

7. Global Smart Elevators Market, by End-user Industry

7.1. Introduction

7.2. Residential

7.3. Commercial (Office, Hotel, Retail)

7.4. Industrial

7.5. Institutional (Healthcare, Education, Government)

8. Global Smart Elevators Market, by Application

8.1. Introduction

8.2. Passenger Elevators

8.3. Freight & Service Elevators

9. Global Smart Elevators Market, by Region

9.1. Introduction

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. France

9.3.3. U.K.

9.3.4. Italy

9.3.5. Spain

9.3.6. Russia

9.3.7. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. India

9.4.3. Japan

9.4.4. South Korea

9.4.5. Australia

9.4.6. Southeast Asia (Singapore, Thailand, Indonesia)

9.4.7. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Argentina

9.5.4. Chile

9.5.5. Colombia

9.5.6. Peru

9.5.7. Rest of Latin America

9.6. Middle East & Africa

9.6.1. Saudi Arabia

9.6.2. UAE

9.6.3. South Africa

9.6.4. Israel

9.6.5. Egypt

9.6.6. Nigeria

9.6.7. Kenya

9.6.8. Rest of Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Benchmarking

10.4. Competitive Dashboard

10.4.1. Industry Leaders

10.4.2. Market Differentiators

10.4.3. Vanguards

10.4.4. Emerging Companies

10.5. Market Ranking/Positioning Analysis of Key Players, 2025

11. Company Profiles (Active Manufacturers & Service Providers)

11.1. Otis Worldwide Corporation

11.2. Schindler Group

11.3. KONE Oyj

11.4. ThyssenKrupp Elevator (TK Elevator)

11.5. Mitsubishi Electric Corporation

11.6. Hitachi, Ltd.

11.7. Fujitec Co., Ltd.

11.8. Toshiba Elevator and Building Systems Corporation

11.9. Hyundai Elevator Co., Ltd.

11.10. Delfar Elevator Co., Ltd.

11.11. Joylive Elevator

11.12. Sigma Elevator Company

12. Appendix

12.1. Questionnaire

12.2. Related Reports

Published Date: Mar-2025

Subscribe to get the latest industry updates