Resources

About Us

Smart Surveillance Systems Market by Component (Hardware, Software, Services), Device Type (Smart IP Cameras, Video Doorbells, NVR/DVR Systems), Technology (AI & Deep Learning, Edge Computing, Cloud-based Analytics), Application (Public Safety & Smart Cities, Commercial Security, Residential Monitoring), and Geography – Global Forecast to 2036

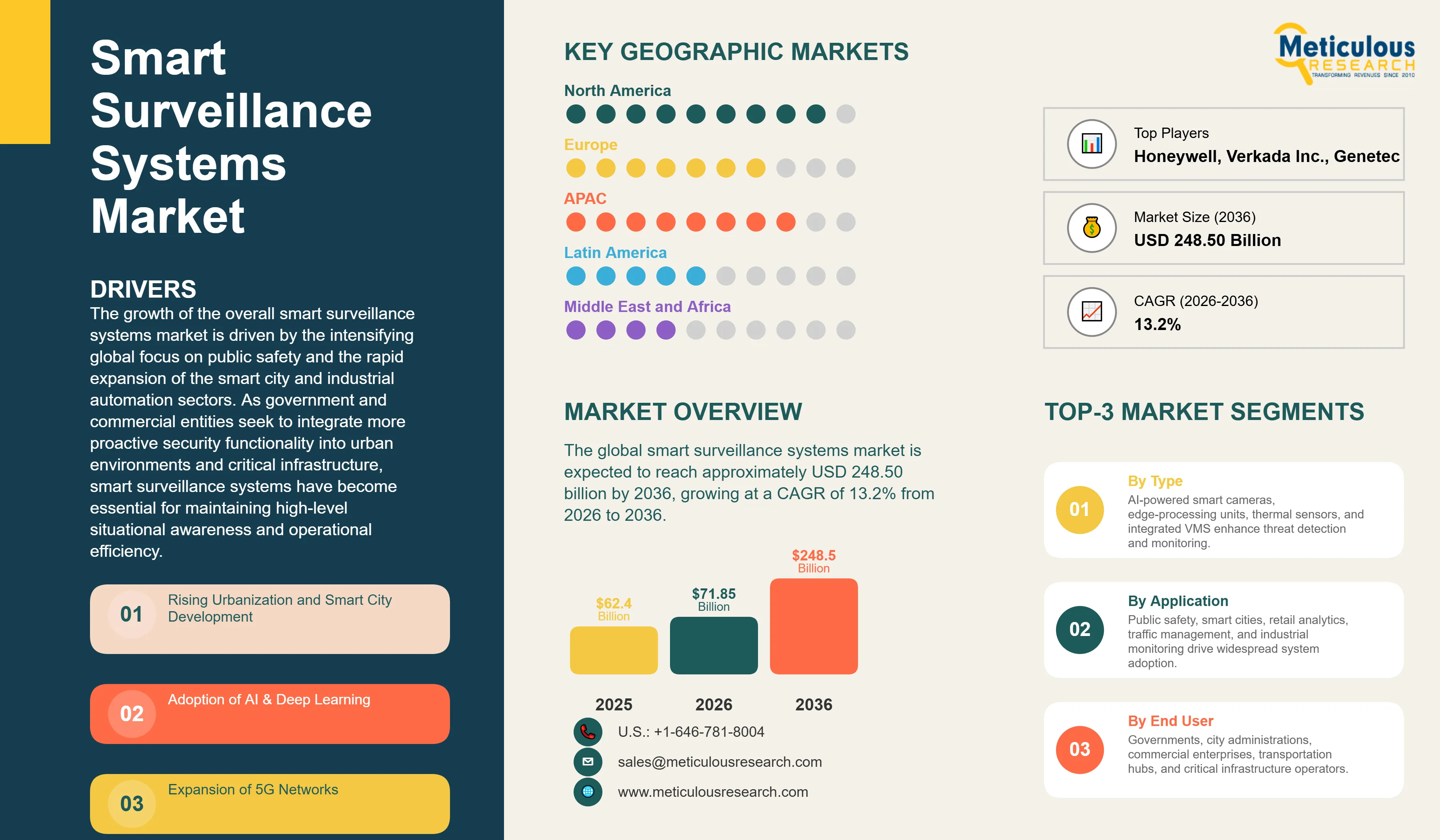

Report ID: MRSE - 1041736 Pages: 251 Feb-2026 Formats*: PDF Category: Semiconductor and Electronics Delivery: 24 to 72 Hours Download Free Sample ReportThe global smart surveillance systems market was valued at USD 62.40 billion in 2025. The market is expected to reach approximately USD 248.50 billion by 2036 from USD 71.85 billion in 2026, growing at a CAGR of 13.2% from 2026 to 2036. The growth of the overall smart surveillance systems market is driven by the intensifying global focus on public safety and the rapid expansion of the smart city and industrial automation sectors. As government and commercial entities seek to integrate more proactive security functionality into urban environments and critical infrastructure, smart surveillance systems have become essential for maintaining high-level situational awareness and operational efficiency. The rapid expansion of 5G infrastructure and the increasing need for real-time edge analytics in autonomous monitoring and forensic investigations continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

mart surveillance systems are critical security environments that leverage advanced vision technologies to provide optimized monitoring processes and improved safety experiences through a connected digital infrastructure. These systems include integrated hardware, software, and services designed to automate threat detection and enhance decision-making across the security continuum. The market is defined by high-efficiency technologies such as AI-powered object recognition and edge-enabled video analytics, which significantly enhance forensic precision and resource utilization in high-pressure security environments. These systems are indispensable for facility administrators seeking to optimize their internal security operations and meet aggressive public safety and efficiency targets.

The market includes a diverse range of solutions, ranging from simple residential smart cameras for basic property monitoring to complex multi-sensor city-wide surveillance networks and AI-driven forensic platforms. These systems are increasingly integrated with advanced components such as cloud-based video management systems (VMS) and 5G-enabled connectivity to provide services such as real-time anomaly detection and predictive maintenance of security hardware. The ability to provide stable, high-precision visual data while minimizing manual monitoring intervention has made smart surveillance technology the choice for institutions where security accuracy and operational reliability are paramount.

The global security sector is pushing hard to modernize facility capabilities, aiming to meet AI-driven safety targets and proactive crime prevention goals. This drive has increased the adoption of high-speed connectivity solutions, with advanced 5G networks helping to stabilize data transmission for ultra-high-definition video feeds. At the same time, the rapid growth in the retail analytics and autonomous traffic markets is increasing the need for high-reliability, secure digital solutions.

Proliferation of Edge AI and Proactive Threat Detection

Security providers across the industry are rapidly shifting to edge-optimized workflows, moving well beyond traditional central recording toward proactive and localized AI setups. Axis Communications’ latest edge-powered camera platforms deliver significantly higher detection accuracy, while Hanwha Vision’s recent installations have slashed false alarm rates in commercial complexes. The real game-changer comes with “agentic” surveillance systems featuring integrated deep learning that maintains peak detection efficiency even in high-volume public environments. These advancements make high-precision security support practical and cost-effective for everyone from small retail shops to global transportation hubs chasing excellence in public safety and lower operational costs.

Innovation in Hybrid Cloud VMS and Digital Twin Integration

Innovation in hybrid cloud video management and digital twin integration is rapidly driving the smart surveillance systems market, as security procedures become more data-driven and facility operations more virtualized. Equipment suppliers are now designing units that combine the reliability of on-premise storage with the intelligence of cloud-based analytics in a single platform, saving valuable investigative time and simplifying security logistics. These systems often involve advanced spatial mapping and 3D visualization capable of handling complex multi-site monitoring without compromising data privacy or system reliability.

At the same time, growing focus on ethical AI is pushing manufacturers to develop smart surveillance solutions tailored to privacy-by-design and data encryption principles. These systems help reduce privacy risks through automated redaction and the use of secure communication protocols. By combining high-density visual connectivity with robust privacy performance, these new designs support both technological advancement and corporate responsibility, strengthening the resilience of the broader security value chain.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 248.50 Billion |

|

Market Size in 2026 |

USD 71.85 Billion |

|

Market Size in 2025 |

USD 62.40 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 13.2% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Component, Device Type, Technology, Application, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

Drivers: Urbanization and the Rise of Proactive Security Models

A key driver of the smart surveillance systems market is the rapid movement of the global security industry toward proactive, AI-first safety models. Global demand for seamless urban monitoring, real-time threat detection, and data-driven forensics has created significant incentives for the adoption of smart surveillance infrastructure. The trend toward “safe cities” and the integration of security devices into unified digital platforms drive providers toward scalable solutions that smart surveillance can uniquely provide. It is estimated that as urban adoption of IoT-enabled cameras rises and security tools become more decentralized through 2036, the need for robust, connected infrastructure increases significantly; therefore, AI-driven software and high-speed connectivity, with their ability to ensure high-density data processing, are considered a crucial enabler of modern security delivery strategies.

Opportunity: 5G Expansion and Integration with Smart City Ecosystems

The rapid growth of the 5G network market and smart city infrastructure technologies provides great opportunities for the smart surveillance systems market. Indeed, the global surge in 5G deployment has created a compelling demand for systems that can handle massive video throughput and provide ultra-low latency for mobile surveillance. These applications require high reliability, data security, and the ability to handle high-bandwidth imaging, all attributes that are met with advanced smart surveillance solutions. The autonomous security market is set to expand significantly through 2036, with smart surveillance poised for an expanding share as providers seek to maximize investigative precision and minimize response times. Furthermore, the increasing demand for AI-driven retail analytics and smart traffic management is stimulating demand for modular digital solutions that provide high-speed data transmission and operational flexibility.

Why Does the Hardware Segment Lead the Market?

The hardware segment accounts for a significant portion of the overall smart surveillance systems market in 2026. This is mainly attributed to the essential role of physical devices such as high-resolution IP cameras, thermal sensors, and edge-processing units within modern security environments. These components offer the most direct way to ensure high-quality data capture across diverse surveillance applications. The public safety and commercial sectors alone consume a large share of surveillance hardware, with major projects in North America and Asia-Pacific demonstrating the technology’s capability to handle high-density visual requirements. However, the software segment is expected to grow at a rapid CAGR during the forecast period, driven by the growing need for robust AI analytics, video management, and cloud-based platforms in complex security digital transformations.

How Does the Public Safety & Smart Cities Segment Dominate?

Based on application, the public safety & smart cities segment holds the largest share of the overall market in 2026. This is primarily due to the massive volume of connected security nodes and the rigorous monitoring standards required for urban crime prevention and emergency response. Current large-scale city administrations are increasingly specifying high-density digital platforms to ensure compliance with global safety standards and citizen expectations for secure urban environments.

The commercial security and retail analytics segment is expected to witness the fastest growth during the forecast period. The shift toward AI-enhanced business intelligence and the complexity of multi-site retail monitoring are pushing the requirement for advanced smart systems that can handle varied data formats and high-resolution video while ensuring absolute reliability for safety-critical and business-critical decisions.

Why Does AI & Deep Learning Lead the Market?

The AI & deep learning segment commands the largest share of the global smart surveillance systems market in 2026. This dominance stems from its superior ability to process vast amounts of visual data, provide predictive analytics, and automate routine monitoring tasks, making it the technology of choice for high-performance smart surveillance. Large-scale operations in facial recognition, behavioral analysis, and automated license plate recognition (ALPR) drive demand, with advanced algorithms from providers like Hikvision, Dahua, and Axis enabling reliable performance in complex security environments.

However, the edge computing segment is poised for steady growth through 2036, fueled by expanding applications in real-time response and bandwidth optimization. Manufacturers face mounting pressure to optimize costs for high-volume, decentralized applications, where edge processing provides a cost-effective alternative for localized security intelligence.

How is North America Maintaining Dominance in the Global Smart Surveillance Systems Market?

North America holds the largest share of the global smart surveillance systems market in 2026. The largest share of this region is primarily attributed to the advanced security infrastructure and the presence of the world’s leading technology innovators, particularly in the United States. The U.S. alone accounts for a significant portion of global smart surveillance investment, with its position as a leading adopter of AI and cloud-based security driving sustained growth. The presence of leading manufacturers like Motorola Solutions (Avigilon) and a well-developed security IT supply chain provides a robust market for both standard and high-density smart solutions.

Which Factors Support Asia-Pacific and Europe Market Growth?

Asia-Pacific and Europe together account for a substantial share of the global smart surveillance systems market. The growth of these markets is mainly driven by the need for technological modernization in the public security and commercial sectors. The demand for advanced smart systems in Asia-Pacific is mainly due to its large-scale smart city infrastructure projects and the presence of innovators in China, Japan, and South Korea.

In Europe, the leadership in security engineering and the push for data privacy innovation (GDPR-compliant AI) are driving the adoption of high-reliability smart solutions. Countries like Germany, the UK, and France are at the forefront, with significant focus on integrating smart digital solutions into security workflows and advanced urban management systems to ensure the highest levels of performance and reliability.

The companies such as Hikvision Digital Technology Co., Ltd., Dahua Technology Co., Ltd., Axis Communications AB, and Motorola Solutions, Inc. (Avigilon) lead the global smart surveillance systems market with a comprehensive range of AI-driven and edge-powered solutions, particularly for large-scale urban and commercial applications. Meanwhile, players including Bosch Service Solutions, Hanwha Vision Co., Ltd., Panasonic Holdings Corporation, and Honeywell International Inc. focus on specialized security hardware, integrated VMS, and thermal imaging platforms targeting the industrial and critical infrastructure sectors. Emerging manufacturers and integrated players such as Verkada Inc., Genetec Inc., Milestone Systems A/S, and VIVOTEK Inc. are strengthening the market through innovations in hybrid cloud solutions and modular AI-driven platforms.

The global smart surveillance systems market is expected to grow from USD 71.85 billion in 2026 to USD 248.50 billion by 2036.

The global smart surveillance systems market is projected to grow at a CAGR of 13.2% from 2026 to 2036.

Hardware is expected to dominate the market in 2026 due to its essential role in high-resolution data capture. However, the software segment is projected to be the fastest-growing segment owing to the increasing need for AI analytics and cloud-based management in complex security environments.

AI and 5G are transforming the landscape by demanding higher data integrity, lower latency, and improved proactive threat detection. These technologies drive the adoption of advanced platforms like edge-AI cameras and cloud-based VMS, enabling security providers to support the complex workflows and high-frequency requirements of next-generation smart cities.

North America holds the largest share of the global smart surveillance systems market in 2026. The largest share of this region is primarily attributed to the advanced security infrastructure and the presence of leading AI innovators in the U.S. Asia-Pacific is expected to witness the fastest growth, driven by massive investments in smart city modernization.

The leading companies include Hikvision, Dahua, Axis Communications, Motorola Solutions, and Hanwha Vision.

Published Date: Aug-2024

Published Date: Jan-2025

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates