Resources

About Us

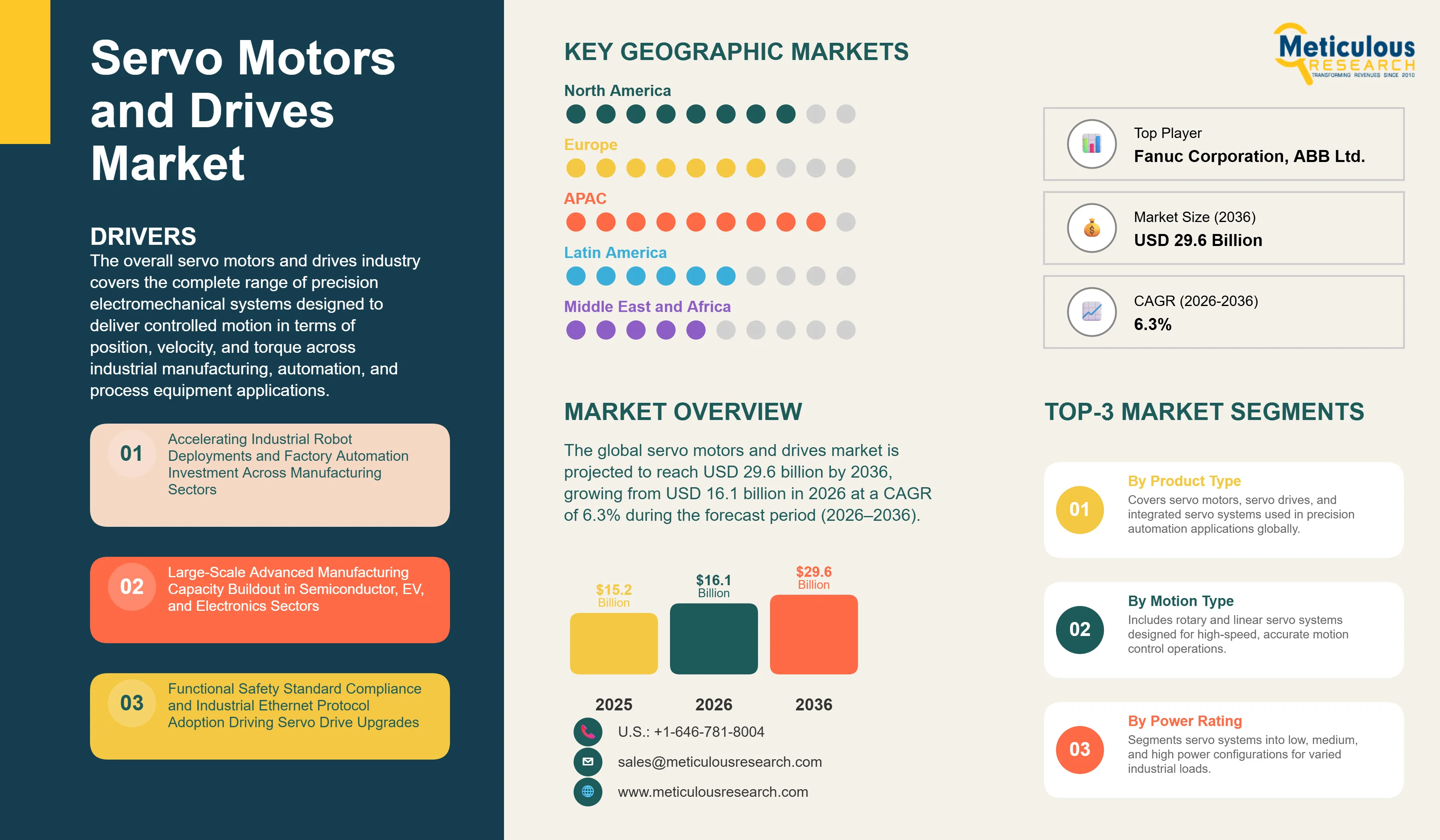

The global servo motors and drives market was valued at USD 15.2 billion in 2025. The market is projected to reach USD 29.6 billion by 2036, growing from USD 16.1 billion in 2026 at a CAGR of 6.3% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The overall servo motors and drives industry covers the complete range of precision electromechanical systems designed to deliver controlled motion in terms of position, velocity, and torque across industrial manufacturing, automation, and process equipment applications. The market encompasses servo motors, servo drives (also referred to as servo amplifiers or servo controllers), and integrated servo systems that combine motor, drive, and control functionality within a unified hardware platform. Within the servo motors segment, the market includes AC synchronous servo motors, AC induction servo motors, brushless DC servo motors, and linear servo motors, while the servo drives segment spans single-axis and multi-axis drive configurations offering analog, pulse, fieldbus, and industrial Ethernet communication interfaces. These systems are deployed across a wide range of end-use industries including machine tool and industrial machinery, automotive and transportation, electronics and semiconductor manufacturing, food and beverage processing, packaging and labeling, aerospace and defense, medical devices and healthcare, and robotics and automation.

Servo motors and drives are differentiated from general-purpose motors and variable frequency drives by their ability to deliver closed-loop feedback control with high dynamic response, positioning accuracy, and repeatability, making them the preferred motion control solution for applications where process quality, production throughput, and machine reliability depend directly on precision motion performance. The closed-loop architecture of servo systems, relying on encoder or resolver feedback to continuously correct positional error, provides capabilities that open-loop stepper motor systems and standard induction motor drives cannot match in terms of responsiveness, torque consistency across the speed range, and the ability to maintain accuracy under varying load conditions.

The growth of the servo motors and drives market is primarily driven by the sustained global expansion of factory automation, the accelerating deployment of industrial robots across manufacturing industries, and the large-scale buildout of advanced manufacturing capacity in semiconductor, electric vehicle, and renewable energy sectors. The International Federation of Robotics (IFR) reported that global industrial robot installations reached approximately 541,000 units in 2023, the second-highest annual figure on record, with each multi-axis industrial robot requiring multiple servo motor and drive assemblies per joint axis. This directly translates servo adoption into a structurally growing end market. Concurrently, the increasing integration of functional safety capabilities into servo drive platforms, driven by the adoption of IEC 61800-5-2 safety function standards and the upcoming application of the EU Machinery Regulation 2023/1230, is compelling machine builders and system integrators to upgrade servo drive specifications to meet documented safety performance requirements across industrial machinery platforms.

In addition to automation-led demand, growing regulatory and commercial pressure to improve industrial energy efficiency is creating a meaningful upgrade cycle for servo motor technology. The International Energy Agency (IEA) estimates that electric motors and motor-driven systems account for approximately 45% of global electricity consumption, making efficiency improvements in servo motor technology a material lever for industrial operators seeking to reduce energy costs and meet sustainability commitments. The adoption of IE4 Super Premium and IE5 Ultra Premium efficiency class permanent magnet synchronous servo motors, as defined under IEC 60034-30-1, offers efficiency gains of 2% to 4% over IE3-class motors, representing significant energy cost savings in high-utilization production environments. The integration of industrial IoT connectivity and real-time motion analytics into servo drive platforms is further accelerating adoption by enabling predictive maintenance, remote diagnostics, and automated parameter optimization that reduce servo system commissioning time and unplanned downtime in production environments.

Despite strong growth fundamentals, the market faces challenges related to the technical complexity of servo system specification and commissioning, particularly in multi-axis coordinated motion applications requiring precise tuning of control loop parameters, electronic gearing ratios, and safety function configurations across heterogeneous machine architectures. Supply chain constraints for rare earth permanent magnets, specifically neodymium-iron-boron materials used in high-efficiency servo motor construction, continue to influence production cost and lead time variability for servo motor manufacturers. The increasing fragmentation of industrial communication protocols across major automation platforms also introduces integration complexity for machine builders sourcing servo components across competing vendor ecosystems.

The transition of advanced manufacturing capacity to North America and Europe through industrial policy instruments including the U.S. CHIPS and Science Act, the EU Chips Act, and domestic electric vehicle manufacturing incentives is creating structurally new capital investment cycles in automation-intensive industries that represent significant incremental addressable markets for servo system manufacturers. The rapid expansion of collaborative robot and autonomous mobile robot markets, both of which rely heavily on compact, high-efficiency servo motor and drive assemblies, is opening a growing demand segment that was not served by traditional industrial servo system product lines. The integration of servo drives into digital twin and model-based commissioning workflows is additionally creating opportunities for manufacturers offering software-enabled motion control platforms that reduce time-to-market for machine builders and improve lifecycle performance for end users.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 29.6 Billion |

|

Market Size in 2026 |

USD 16.1 Billion |

|

Market Size in 2025 |

USD 15.2 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 6.3% |

|

Dominating Product Type |

Servo Motors |

|

Fastest Growing Product Type |

Integrated Servo Systems |

|

Dominating Motion Type |

Rotary Servo Systems |

|

Fastest Growing Motion Type |

Linear Servo Systems |

|

Dominating Power Rating |

Medium Power Servo Systems |

|

Fastest Growing Power Rating |

Low Power Servo Systems |

|

Dominating End-use Industry |

Machine Tool & Industrial Machinery |

|

Fastest Growing End-use Industry |

Electronics & Semiconductor |

|

Dominating Geography |

Asia Pacific |

|

Fastest Growing Geography |

North America |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Expanding Industrial Robot Installations, Advanced Manufacturing Reshoring, and Semiconductor Fab Buildout Driving Structural Demand Growth for High-Precision Servo Systems

The sustained expansion of precision manufacturing capacity globally, accelerating industrial robot deployment, and the large-scale policy-driven reshoring of semiconductor and electric vehicle production are together creating a structural demand environment for high-performance servo motors and drives that extends well beyond conventional cyclical capital expenditure patterns. According to the International Federation of Robotics (IFR), global industrial robot installations reached approximately 541,000 units in 2023, the second-highest annual figure on record. Asia Pacific accounted for the majority of these installations, with China alone installing approximately 276,000 robots, representing roughly 51% of global volume. Each articulated industrial robot requires between four and seven servo motor and drive assemblies per axis, making robot production volumes a direct leading indicator for servo system demand. Beyond the installed base of conventional articulated robots, the rapid growth of collaborative robots and autonomous mobile robots, both of which rely on compact, high-efficiency servo assemblies for joint actuation and wheel drive, is expanding the addressable market for servo products beyond traditional heavy industrial applications into lighter manufacturing, logistics, and service sectors.

The reshoring of semiconductor fabrication capacity represents one of the most significant discrete drivers of precision servo system demand over the forecast period. The U.S. CHIPS and Science Act committed USD 52.7 billion in federal funding toward domestic semiconductor manufacturing and research, with additional investments from private sector participants including TSMC, Samsung, Intel, and Micron driving construction of new wafer fabrication facilities across Arizona, Ohio, and Texas. Concurrently, the EU Chips Act committed EUR 43 billion to double Europe's share of global semiconductor production to 20% by 2030. Semiconductor lithography systems, wafer transport equipment, chemical mechanical planarization platforms, and precision metrology tools each require multiple high-performance servo axes to achieve the nanometer-level positioning tolerances required in advanced node fabrication, creating a concentrated source of demand for the highest specification servo systems available. Electric vehicle battery gigafactory construction, with major capacity additions underway in North America, Europe, and Asia, is similarly creating sustained demand for servo-driven automation across electrode coating, cell assembly, module manufacturing, and end-of-line testing processes.

The intersection of reshoring-driven capital investment and accelerating robot adoption is reinforcing demand for servo systems not only in the OEM machine tool and robot manufacturing segments but also in end-user facility-level automation investment as manufacturers rebuild and upgrade production lines with higher levels of automation to offset elevated labor costs and improve production flexibility. Manufacturers including Siemens AG, Yaskawa Electric Corporation, Fanuc Corporation, and Mitsubishi Electric Corporation are actively expanding servo product portfolios and regional application engineering capabilities to capitalize on this structural demand inflection, underscoring the durability of the growth dynamic driving the global servo motors and drives market through the forecast period.

Functional Safety Standard Adoption and Industrial Ethernet Protocol Integration Transforming Servo Drive Architecture and Machine Builder Procurement Criteria

The accelerating adoption of international functional safety standards for machinery and drive systems is fundamentally reshaping servo drive architecture requirements and redefining the procurement criteria applied by machine builders and system integrators selecting servo components for new machine programs. IEC 61800-5-2:2016, the functional safety standard specifically governing adjustable speed electrical power drive systems, defines a comprehensive set of safety functions including Safe Torque Off, Safe Stop 1 and 2, Safe Operating Stop, Safely Limited Speed, Safe Direction, and Safely Limited Acceleration that are increasingly mandated in machine specifications across European, North American, and Japanese markets. The EU Machinery Regulation 2023/1230, which entered into force in January 2024 and will be fully applicable from January 2027, strengthens the documentation and validation requirements for safety-related control functions in machinery, compelling machine builders to select servo drives that carry certified safety function performance ratings to SIL 2 or PLe levels under IEC 62061 and ISO 13849-1 respectively. This regulatory transition is effectively eliminating from competitive consideration servo drive platforms that do not offer certified integrated safety functions, creating a significant technology upgrade cycle within the installed base of machines powered by older servo drive hardware.

In parallel, the widespread migration from traditional analog and pulse-train servo command interfaces to industrial Ethernet-based communication protocols is driving a broad hardware and software transition across the servo drive market. Protocols including EtherCAT, PROFINET, EtherNet/IP, MECHATROLINK-4, and Ethernet POWERLINK are progressively replacing proprietary serial and fieldbus architectures in new machine designs, offering sub-microsecond synchronization between drive axes, deterministic real-time communication, and the ability to transmit motion commands, feedback data, and diagnostic information over a single network infrastructure. This protocol transition requires servo drives that incorporate the appropriate industrial Ethernet slave controllers and protocol stacks, making hardware compatibility with the machine builder's chosen automation platform a central procurement criterion. Leading servo drive manufacturers including Siemens AG (SINAMICS S210), Yaskawa Electric Corporation (Sigma-7), Beckhoff Automation GmbH (AX5000 and AX8000), and Bosch Rexroth AG (IndraDrive) have invested substantially in drives supporting multiple simultaneous industrial Ethernet protocol options, allowing configuration to customer-specific network requirements and reducing the inventory complexity for machine builders operating across heterogeneous automation environments.

The convergence of functional safety certification requirements and industrial Ethernet protocol migration is also accelerating the transition to multi-axis servo drive platforms that consolidate multiple axes within a shared DC link power bus architecture, offering reduced panel space, lower wiring complexity, and improved dynamic energy recovery through regenerative braking shared across axes. Manufacturers including Siemens AG, Bosch Rexroth AG, Parker Hannifin Corporation, and Lenze SE have developed modular multi-axis servo drive platforms specifically engineered for this architecture, targeting machine tool builders, packaging machinery OEMs, and printing and converting machine manufacturers where multi-axis coordinated motion is essential. This shift toward integrated, safety-rated, network-connected multi-axis drive platforms represents a meaningful upgrade in the average selling price and technical content of servo drive systems, positively influencing both revenue growth and aftermarket service engagement over the forecast period.

IE4 and IE5 Motor Efficiency Mandates and Permanent Magnet Synchronous Motor Technology Adoption Creating a Compliance-Led Upgrade Cycle Across Industrial Servo Motor Installations

The shrinking of industrial motor energy-efficiency regulations across major economies, combined with increasing focus on total cost of ownership reduction, is contributing to a gradual replacement cycle across the global installed base of industrial motion systems. According to the International Energy Agency, electric motors and motor-driven systems account for a substantial share of global electricity consumption, positioning motor efficiency as an important component of industrial energy optimization and decarbonization strategies. Within industrial automation applications, this is increasing adoption of high-efficiency permanent magnet synchronous servo systems and advanced digital drive architectures capable of delivering improved dynamic performance with lower energy consumption. Many next-generation servo platforms are designed to align with IE4 Super Premium and emerging IE5-equivalent efficiency performance objectives under evolving IEC efficiency frameworks, enabling measurable reductions in energy consumption, heat generation, and operating costs in high-utilization manufacturing environments operating continuous or multi-shift production cycles.

EU Commission Regulation (EU) 2019/1781 on ecodesign requirements for electric motors and variable speed drives established IE3 as the minimum permissible efficiency class for single-speed three-phase induction motors across the broadest power range applicable to servo applications, with the requirements for motors between 0.12 kW and 0.75 kW taking effect from July 2023. While servo motors operating in closed-loop feedback configurations are subject to different regulatory treatment than general-purpose induction motors, the overall regulatory direction across Europe, China, and North America is toward progressively higher minimum efficiency thresholds that are narrowing the performance gap between general-purpose and servo-specific efficiency standards and compelling manufacturers to invest in advanced permanent magnet rotor designs, precision winding geometries, and optimized lamination materials to meet both market expectations and regulatory baselines. China's GB 18613 mandatory energy efficiency standard for electric motors, which adopted IE3 as the minimum efficiency class for new motor sales in 2021, similarly reinforces efficiency-led procurement across the world's largest servo motor consumption market.

The technical shift toward permanent magnet synchronous motor architecture in servo applications, which offers inherently higher efficiency than induction-based designs due to the elimination of rotor copper losses and the availability of high torque-to-inertia ratios enabling more dynamic machine performance, is further accelerating the adoption of high-efficiency servo motor platforms. Manufacturers including Siemens AG (SIMOTICS S series), Nidec Corporation (Leroy-Somer and Control Techniques platforms), ABB Ltd. (including B&R Industrial Automation servo motor lines), Fanuc Corporation, and Yaskawa Electric Corporation have expanded their permanent magnet synchronous servo motor portfolios to cover a broader power range and a wider variety of frame sizes, cooling configurations, and feedback options, enabling specification into applications that previously relied on less efficient induction motor solutions. The integration of servo motor efficiency data into digital twin and energy monitoring platforms is additionally enabling operators to quantify motor-level energy consumption and build the business case for efficiency upgrade investments, accelerating replacement cycle timing for operators managing large installed bases of aging servo motor hardware.

By Product Type: In 2026, the Servo Motors Segment to Dominate the Global Servo Motors and Drives Market

Based on product type, the servo motors and drives industry is segmented into servo motors, servo drives, and integrated servo systems. In 2026, the servo motors segment is expected to account for the largest share of this market. The leading position of this segment is attributed to the broad and sustained demand for servo motors as the fundamental actuating component across the full spectrum of industrial automation and precision manufacturing equipment, encompassing machine tool axis and spindle drives, industrial robot joint actuators, packaging and labeling machinery, printing and converting equipment, material handling systems, and semiconductor process equipment. AC permanent magnet synchronous servo motors represent the dominant motor technology within this segment, owing to their superior combination of high torque density, compact frame size, low rotor inertia for dynamic responsiveness, and broad constant torque speed range that collectively make them the preferred actuator specification for modern high-performance machine designs. Within the servo drives sub-segment, single-axis and multi-axis configurations together address the full range of machine complexity, from simple point-to-point positioning systems to highly coordinated electronic camming and gearing applications in printing, packaging, and assembly machinery.

However, the integrated servo systems segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the growing adoption of compact, all-in-one servo units that combine the motor, drive electronics, and motion control logic within a unified assembly, eliminating the need for a separate control cabinet drive module and the associated cabling infrastructure between motor and drive. This integration trend is particularly pronounced among small and mid-size machine builders that value reduced system complexity, faster machine commissioning, and lower machine footprint, and is further reinforced by the growing adoption of distributed machine architectures where control intelligence is placed at the machine axis level rather than being centralized in a panel-mounted controller. Manufacturers including Beckhoff Automation GmbH (with its AMP8000 distributed servo drive system), Siemens AG, and Bosch Rexroth AG are actively developing and commercializing integrated servo system platforms that address this architectural preference, reflecting the strong commercial momentum behind this product segment.

By Motion Type: In 2026, the Rotary Servo Systems Segment to Hold the Largest Share

Based on motion type, the servo motors and drives industry is segmented into rotary servo systems and linear servo systems. In 2026, the rotary servo systems segment is expected to account for the largest share of this market. This dominance is driven by the extensive installed base of rotary servo motors across machine tool, industrial robot, packaging, printing, food processing, and general-purpose factory automation applications, where rotary motion is the primary output required and where rotary servo motors provide the most cost-effective, reliable, and well-supported actuator solution. Rotary servo motors benefit from decades of application engineering refinement, widespread servicing infrastructure, and a broad ecosystem of compatible mechanical transmission components including planetary gearheads, timing belt drives, and rack and pinion systems that extend rotary servo output into a wide range of linear and rotational motion requirements across industrial machinery designs.

However, the linear servo systems segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the growing adoption of linear servo motors in applications demanding the highest levels of positioning accuracy, force consistency, and dynamic response, where the mechanical transmission losses, backlash, and compliance introduced by rotary-to-linear conversion mechanisms limit achievable performance. Key growth applications include semiconductor wafer handling and positioning equipment, precision laser cutting and additive manufacturing platforms, high-speed pick-and-place systems for electronics assembly, advanced medical imaging and surgical robotics, and precision metrology equipment, all of which are expanding rapidly in response to increasing product miniaturization requirements and manufacturing quality standards. Manufacturers including Siemens AG, Yaskawa Electric Corporation, Fanuc Corporation, and Beckhoff Automation GmbH have expanded linear servo motor product lines covering a wide range of force ratings, stroke lengths, and cooling configurations to address the broadening application base for linear servo technology.

By Power Rating: In 2026, the Medium Power Servo Systems Segment to Account for the Largest Share

Based on power rating, the servo motors and drives industry is segmented into low power servo systems (up to 750 W), medium power servo systems (750 W to 7.5 kW), and high power servo systems (above 7.5 kW). In 2026, the medium power servo systems segment is expected to account for the largest share of this market. The dominant position of this segment is driven by the broad applicability of medium power servo configurations across the widest range of industrial automation equipment, encompassing machine tool axis drives, six-axis industrial robot joint actuators in the 6–20 kg payload class, packaging and labeling machinery, injection molding machines, and printing equipment. Medium power servo motors in the 750 W to 7.5 kW range provide the combination of torque output, dynamic performance, and physical frame size that aligns with the requirements of the largest number of industrial machine designs worldwide, and as such represent the core product revenue category for all major servo system manufacturers.

However, the low power servo systems segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the rapid expansion of collaborative robot installations, which typically utilize servo motor assemblies in the 100 W to 500 W range per joint axis, and the accelerating adoption of lightweight industrial robots in electronics component assembly, medical device manufacturing, and pharmaceutical production, where space constraints and payload requirements favor compact, lightweight servo assemblies. The proliferation of autonomous mobile robot platforms in warehousing and intralogistics, each requiring compact drive wheel servo assemblies, is additionally expanding the low power servo systems addressable market beyond traditional stationary machine applications. Manufacturers including Panasonic Corporation (MINAS series), Delta Electronics, Inc. (ASDA series), and Beckhoff Automation GmbH are expanding low power servo portfolios with high-resolution encoder feedback options and compact drive formats specifically targeting collaborative robot and light manufacturing automation applications.

By End-use Industry: In 2026, the Machine Tool & Industrial Machinery Segment to Hold the Largest Share

Based on end-use industry, the servo motors and drives industry is segmented into machine tool and industrial machinery, automotive and transportation, electronics and semiconductor, food and beverage processing, packaging and labeling, aerospace and defense, medical devices and healthcare, robotics and automation, and other end-use industries. In 2026, the machine tool and industrial machinery segment is expected to account for the largest share of this market, reflecting the historical centrality of the machine tool sector as the primary end market for precision servo motion systems. CNC machining centers, turning centers, grinding machines, electrical discharge machines, and laser cutting and forming equipment each require multiple servo axes for simultaneous coordinated positioning of axes, spindles, tool changers, and workpiece clamping systems, creating a dense servo motor and drive content per machine unit. The continued expansion of global machine tool production in Asia Pacific, Germany, Italy, and Japan, alongside growing demand for five-axis and multi-tasking machine platforms in aerospace, automotive, and medical component manufacturing, is sustaining strong structural demand for high-performance servo systems within this segment. OSHA and European machinery safety regulations governing guarding, safe-speed monitoring, and axis brake control functions on CNC equipment further reinforce the adoption of safety-rated servo drives across new machine tool programs.

However, the electronics and semiconductor segment is projected to register the highest CAGR during the forecast period. The high growth of this segment is driven by the unprecedented scale of semiconductor manufacturing capacity investment triggered by the U.S. CHIPS and Science Act, the EU Chips Act, Japan's semiconductor revitalization program, and equivalent national policies across South Korea and Taiwan, all of which are directing hundreds of billions of dollars of capital toward the construction of new wafer fabrication and advanced packaging facilities. Each advanced semiconductor fabrication facility incorporates thousands of servo-driven process and handling equipment units, from wafer transfer robots and reticle stages in lithography systems to precision positioning platforms in chemical vapor deposition and inspection tools, making semiconductor capital equipment manufacturing one of the highest servo content categories across the entire industrial end-user landscape. The simultaneous expansion of electronics manufacturing capacity in PCB fabrication, surface mount technology assembly, and display panel production across Asia Pacific and North America is providing additional demand depth within this high-growth end-use segment.

Based on geography, the overall servo motors and drives market is segmented into Asia Pacific, North America, Europe, Latin America, and the Middle East and Africa. In 2026, Asia Pacific is expected to account for the largest share of this market. This dominance is driven by the concentration of the world's largest precision manufacturing industries in Japan, China, South Korea, and Taiwan, encompassing machine tool manufacturing, semiconductor and electronics fabrication, automotive production, and industrial robot manufacturing, all of which are intensive consumers of servo motor and drive systems. Japan is home to Fanuc Corporation and Yaskawa Electric Corporation, two of the world's largest and most technically advanced servo system manufacturers, and the Japanese machine tool and robot manufacturing industries represent the single largest consolidated source of servo procurement globally. China's position as the world's largest industrial manufacturing economy, with its continuing investment in factory automation to offset rising labor costs and address manufacturing quality demands, creates a large and growing domestic demand base for servo systems that is now increasingly supplied by both multinational manufacturers and rapidly maturing domestic suppliers including Inovance Technology, ESTUN Automation, and Shenzhen Megmeet Drive Technology. South Korea and Taiwan similarly generate substantial servo system demand through their electronics, display, and semiconductor equipment manufacturing industries, reinforcing the structural dominance of the Asia Pacific region in global servo market revenue.

However, the North America servo motors and drives market is expected to grow at the fastest rate from 2026 to 2036. This rapid growth is driven by the extraordinary scale of advanced manufacturing capacity investment committed to the region under the U.S. CHIPS and Science Act, which allocated USD 52.7 billion in federal funding for domestic semiconductor manufacturing and research, catalyzing construction of new wafer fabrication facilities across Arizona, Ohio, and Texas that individually represent multi-billion-dollar automation equipment procurement programs. The Inflation Reduction Act's production tax credits and manufacturing incentives for electric vehicle batteries and clean energy components are additionally driving the construction of battery gigafactories and EV powertrain assembly facilities across the southern United States and Midwest, each representing highly automated production environments with intensive servo system content across battery cell manufacturing, module assembly, and end-of-line testing. The broader reshoring of electronics manufacturing, pharmaceutical production, and aerospace component fabrication in response to supply chain resilience priorities is further expanding the regional installed base of automation equipment requiring servo motion systems. The presence of major machine tool builders, contract electronics manufacturers, and automation system integrators in the region provides a structurally supportive supply and service ecosystem that reinforces procurement confidence for servo system investments.

Europe remains a large and technically advanced market for servo motors and drives, underpinned by the world's highest concentration of precision machine tool builders, packaging machinery manufacturers, printing equipment producers, and industrial robot OEMs, concentrated in Germany, Italy, Switzerland, Austria, and Sweden. European manufacturers including Siemens AG, Bosch Rexroth AG, Lenze SE, Beckhoff Automation GmbH, and B&R Industrial Automation GmbH (now part of ABB Ltd.) maintain global competitive leadership in servo system technology and retain dominant positions within European end-user markets through deep application engineering expertise and established machine builder partnerships. The adoption of the EU Machinery Regulation 2023/1230 and the continued enforcement of machinery safety standards is sustaining compliance-driven servo drive specification upgrades across the European machine manufacturing sector.

The global servo motors and drives market is moderately consolidated at the system level, with the leading positions held by large industrial automation conglomerates and specialized motion control manufacturers that compete on the basis of servo system performance specifications, breadth of motor and drive product portfolios, application engineering support capabilities, and the depth of software and digital service offerings accompanying hardware products. Key differentiators in this market include the availability of integrated functional safety functions certified to IEC 61800-5-2 at SIL 2 and PLe levels, support for multiple industrial Ethernet communication protocols within a single drive hardware platform, the availability of high-resolution multi-turn absolute encoder feedback systems, the range of motor frame sizes and power ratings covered within a unified product series, and the quality and usability of commissioning software and motion programming environments.

Large industrial automation companies including Siemens AG and Rockwell Automation, Inc. compete through tightly integrated servo systems that are optimized for deployment within their respective broader automation ecosystems, leveraging tight hardware-software co-engineering and the installed base of their PLCs and CNC controllers to create procurement preference among machine builders already committed to their automation platform. Specialist motion and drive manufacturers including Yaskawa Electric Corporation, Fanuc Corporation, Mitsubishi Electric Corporation, and Panasonic Corporation compete through the depth of servo technology expertise, the breadth of motor and drive product ranges, and the maturity of application software for specific machine types. Regional specialists including Beckhoff Automation GmbH, Lenze SE, and Moog, Inc. maintain strong competitive positions in specific end-use segments including packaging machinery, printing equipment, and aerospace actuation respectively, while Delta Electronics, Inc. and Inovance Technology are expanding their servo portfolios and geographic reach as they transition from regional to global competitive positions.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global servo motors and drives market include Siemens AG (Germany), Fanuc Corporation (Japan), Yaskawa Electric Corporation (Japan), Mitsubishi Electric Corporation (Japan), Rockwell Automation, Inc. (U.S.), ABB Ltd. (Switzerland), Bosch Rexroth AG (Germany), Schneider Electric SE (France), Nidec Corporation (Japan), Parker Hannifin Corporation (U.S.), Beckhoff Automation GmbH & Co. KG (Germany), Delta Electronics, Inc. (Taiwan), Panasonic Corporation (Japan), Moog, Inc. (U.S.), and Lenze SE (Germany), among others.

The global servo motors and drives market is expected to reach USD 29.6 billion by 2036 from an estimated USD 16.1 billion in 2026, at a CAGR of 6.3% during the forecast period 2026–2036.

In 2026, the servo motors segment is expected to hold the largest share of this market, driven by sustained demand for AC permanent magnet synchronous servo motors across machine tool, industrial robot, packaging, and electronics manufacturing applications globally.

The integrated servo systems segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the growing adoption of compact, all-in-one motor-drive-controller platforms among small and mid-size machine builders seeking reduced system complexity, lower panel space requirements, and faster machine commissioning.

In 2026, the rotary servo systems segment is expected to hold the largest share of this market, reflecting the extensive installed base and broad applicability of rotary servo motors across the full spectrum of industrial automation and precision manufacturing equipment.

In 2026, the medium power servo systems segment is expected to hold the largest share of this market, driven by its broad applicability across machine tool axis drives, industrial robot joint actuators in the 6–20 kg payload class, and general-purpose factory automation equipment.

In 2026, the machine tool and industrial machinery segment is expected to hold the largest share of this market, reflecting the historically dense servo motor and drive content across CNC machining centers, turning centers, grinding machines, and laser cutting and forming equipment produced globally.

The growth of this market is primarily driven by the accelerating deployment of industrial robots and the reshoring of advanced manufacturing capacity in semiconductor, electric vehicle, and electronics sectors supported by the U.S. CHIPS and Science Act and equivalent industrial policy instruments globally, the adoption of IEC 61800-5-2 functional safety standards and industrial Ethernet communication protocols compelling servo drive architecture upgrades, the tightening of motor energy efficiency regulations reinforcing adoption of IE4 and IE5 class permanent magnet synchronous servo motors, and the rapid expansion of collaborative robot and integrated servo system applications in light manufacturing, medical devices, and logistics automation.

Key players in the global servo motors and drives market include Siemens AG (Germany), Fanuc Corporation (Japan), Yaskawa Electric Corporation (Japan), Mitsubishi Electric Corporation (Japan), Rockwell Automation, Inc. (U.S.), ABB Ltd. (Switzerland), Bosch Rexroth AG (Germany), Schneider Electric SE (France), Nidec Corporation (Japan), Parker Hannifin Corporation (U.S.), Beckhoff Automation GmbH & Co. KG (Germany), Delta Electronics, Inc. (Taiwan), Panasonic Corporation (Japan), Moog, Inc. (U.S.), and Lenze SE (Germany).

North America is expected to register the highest growth rate in the global servo motors and drives market during the forecast period 2026–2036, driven by the unprecedented scale of advanced manufacturing capacity investment under the U.S. CHIPS and Science Act, the Inflation Reduction Act's electric vehicle and clean energy manufacturing incentives, and the broader reshoring of electronics, pharmaceutical, and aerospace manufacturing capacity across the region.

1. Introduction

1.1 Market Definition and Scope

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Country-/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

3.1 Market Overview

3.2 Market Analysis by Product Type

3.3 Market Analysis by Motion Type

3.4 Market Analysis by Power Rating

3.5 Market Analysis by End-use Industry

3.6 Market Analysis by Geography

4. Market Dynamics

4.1 Overview

4.2 Drivers

4.2.1 Accelerating Industrial Robot Deployments and Factory Automation Investment Across Manufacturing Sectors

4.2.2 Large-Scale Advanced Manufacturing Capacity Buildout in Semiconductor, EV, and Electronics Sectors

4.2.3 Functional Safety Standard Compliance and Industrial Ethernet Protocol Adoption Driving Servo Drive Upgrades

4.2.4 Motor Energy Efficiency Regulations and IE4/IE5 Technology Adoption Creating Replacement Demand

4.3 Restraints

4.3.1 Supply Chain Constraints for Rare Earth Permanent Magnet Materials Affecting Servo Motor Production Costs

4.3.2 Technical Complexity of Multi-Axis Servo System Commissioning and Industrial Communication Protocol Fragmentation

4.4 Opportunities

4.4.1 Collaborative and Mobile Robot Market Expansion Opening New Addressable Markets for Compact Servo Systems

4.4.2 Digital Twin and Model-Based Commissioning Platforms Creating Software-Enabled Growth Opportunities for Servo Manufacturers

4.4.3 Linear Servo Motor Adoption Expanding into Semiconductor, Medical, and High-Speed Packaging Applications

4.5 Challenges

4.5.1 Intensifying Competition from Domestic Chinese Servo Manufacturers Compressing Pricing in Mid-Range Market Segments

4.5.2 Rapid Industrial Communication Protocol Evolution Requiring Continuous Drive Firmware and Hardware Development Investment

4.6 Porter's Five Forces Analysis

5. Servo Motors and Drives Market, by Product Type

5.1 Overview

5.2 Servo Motors

5.2.1 AC Servo Motors

5.2.1.1 Permanent Magnet Synchronous Servo Motors

5.2.1.2 AC Induction Servo Motors

5.2.2 DC Servo Motors

5.2.2.1 Brushed DC Servo Motors

5.2.2.2 Brushless DC Servo Motors

5.2.3 Linear Servo Motors

5.3 Servo Drives

5.3.1 Single-Axis Servo Drives

5.3.2 Multi-Axis Servo Drives

5.4 Integrated Servo Systems

6. Servo Motors and Drives Market, by Motion Type

6.1 Overview

6.2 Rotary Servo Systems

6.3 Linear Servo Systems

7. Servo Motors and Drives Market, by Power Rating

7.1 Overview

7.2 Low Power Servo Systems (Up to 750 W)

7.3 Medium Power Servo Systems (750 W to 7.5 kW)

7.4 High Power Servo Systems (Above 7.5 kW)

8. Servo Motors and Drives Market, by End-use Industry

8.1 Overview

8.2 Machine Tool & Industrial Machinery

8.3 Automotive & Transportation

8.4 Electronics & Semiconductor

8.4.1 Semiconductor Capital Equipment

8.4.2 Electronics Manufacturing & Assembly Equipment

8.5 Food & Beverage Processing

8.6 Packaging & Labeling

8.7 Aerospace & Defense

8.8 Medical Devices & Healthcare

8.9 Robotics & Automation

8.10 Other End-use Industries

9. Servo Motors and Drives Market, by Geography

9.1 Overview

9.2 Asia Pacific

9.2.1 Japan

9.2.2 China

9.2.3 South Korea

9.2.4 Taiwan

9.2.5 India

9.2.6 Southeast Asia

9.2.7 Rest of Asia Pacific

9.3 North America

9.3.1 U.S.

9.3.2 Canada

9.3.3 Mexico

9.4 Europe

9.4.1 Germany

9.4.2 Italy

9.4.3 U.K.

9.4.4 France

9.4.5 Switzerland

9.4.6 Austria

9.4.7 Sweden

9.4.8 Rest of Europe

9.5 Latin America

9.5.1 Brazil

9.5.2 Mexico

9.5.3 Rest of Latin America

9.6 Middle East and Africa

9.6.1 UAE

9.6.2 Saudi Arabia

9.6.3 South Africa

9.6.4 Rest of Middle East and Africa

10. Competitive Landscape

10.1 Overview

10.2 Key Growth Strategies

10.3 Competitive Benchmarking

10.4 Competitive Dashboard

10.4.1 Industry Leaders

10.4.2 Market Differentiators

10.4.3 Vanguards

10.4.4 Emerging Companies

10.5 Market Share/Ranking Analysis (2025)

11. Company Profiles

11.1 Siemens AG

11.2 Fanuc Corporation

11.3 Yaskawa Electric Corporation

11.4 Mitsubishi Electric Corporation

11.5 Rockwell Automation, Inc.

11.6 ABB Ltd.

11.7 Bosch Rexroth AG

11.8 Schneider Electric SE

11.9 Nidec Corporation

11.10 Parker Hannifin Corporation

11.11 Beckhoff Automation GmbH & Co. KG

11.12 Delta Electronics, Inc.

11.13 Panasonic Corporation

11.14 Moog, Inc.

11.15 Lenze SE

11.16 Others

12. Appendix

12.1 Questionnaire

12.2 Available Customization Options

12.3 Related Reports

Published Date: Jul-2025

Subscribe to get the latest industry updates