Resources

About Us

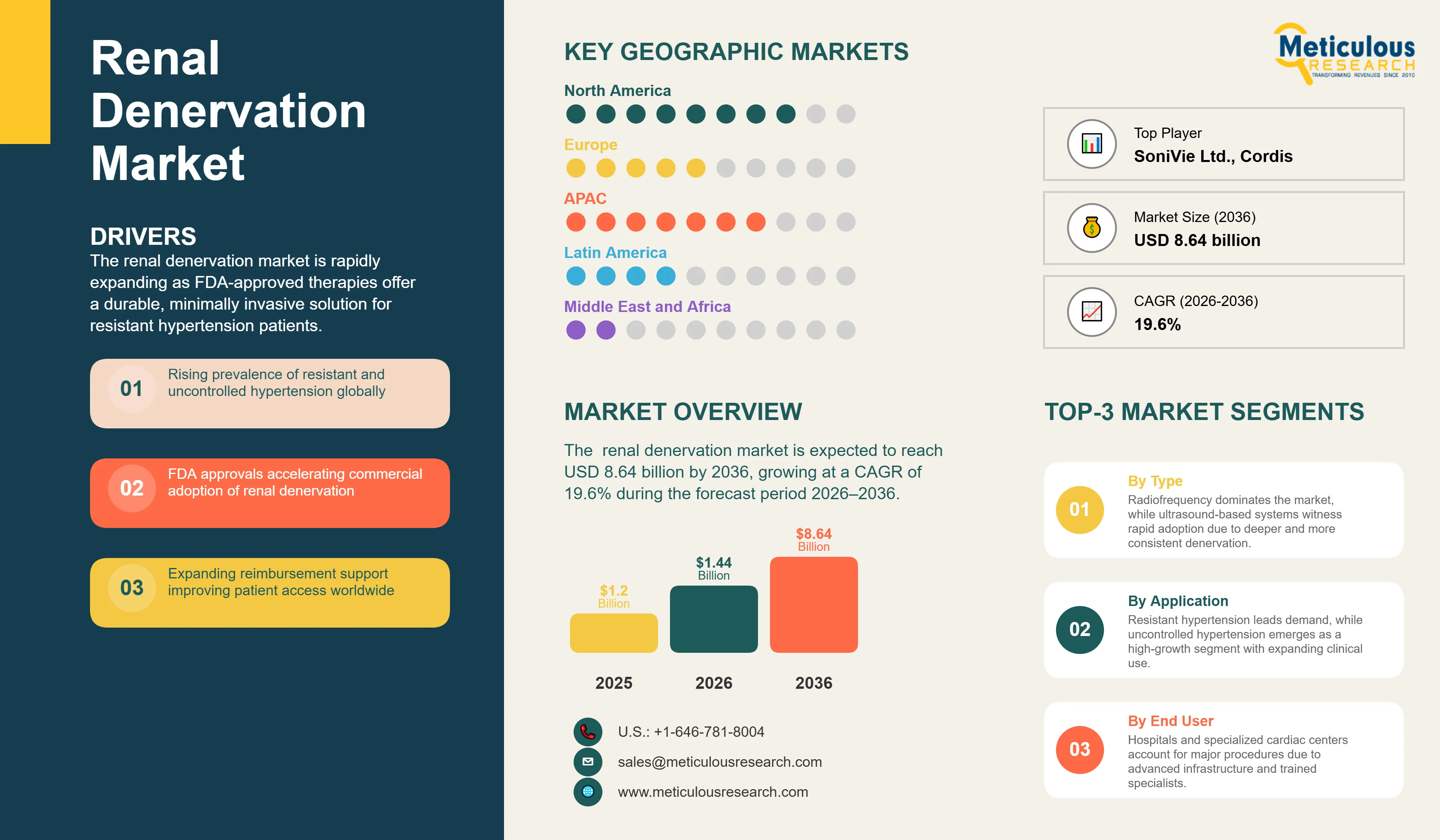

The global renal denervation market was valued at USD 1.44 billion in 2026. This market is expected to reach USD 8.64 billion by 2036, growing at a CAGR of 19.6% during the forecast period 2026–2036.

Market Insights

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global renal denervation market is currently at a historic inflection point, transitioning from a promising research concept to a commercially validated clinical reality. After years of rigorous clinical investigation, the recent FDA approvals of major renal denervation systems have provided a clear pathway for the treatment of resistant hypertension. This device-based therapy, which involves the ablation of sympathetic nerves in the renal arteries, offers a permanent solution for patients who fail to achieve blood pressure control through traditional medication. The market's growth is fundamentally anchored by the global hypertension crisis, with approximately 1.28 billion adults affected worldwide, many of whom suffer from 'pill fatigue' and the long-term cardiovascular risks of uncontrolled blood pressure.

The clinical validation of renal denervation has been strengthened by robust evidence from randomized sham-controlled trials, including the SPYRAL HTN and RADIANCE clinical programs, which have demonstrated significant and durable reductions in ambulatory blood pressure. Ultrasound-based renal denervation has shown reductions of approximately 6–9 mmHg in daytime ambulatory systolic blood pressure compared with sham controls, while radiofrequency-based systems have also demonstrated sustained blood pressure lowering across multiple studies. These reductions are clinically meaningful, as epidemiological evidence indicates that a sustained 5 mmHg decrease in systolic blood pressure may reduce the risk of major cardiovascular events by approximately 10–15%. The market is further benefiting from the establishment of reimbursement pathways and favorable coverage decisions in key markets, particularly the United States, improving patient access to the procedure. In addition, multidisciplinary collaboration among interventional cardiologists, hypertension specialists, nephrologists, and primary care physicians is enhancing patient identification and supporting broader adoption among individuals with resistant or uncontrolled hypertension.

Technological innovation is a primary driver of the market, with a clear shift toward more precise and predictable ablation techniques. While radiofrequency remains the most established technology, ultrasound-based systems are gaining rapid traction due to their ability to provide deeper and more circumferential denervation. The competitive landscape is dominated by Medtronic and ReCor Medical, but the entry of other major medical technology players is expected to further stimulate market growth and innovation. Furthermore, the expansion of indications beyond resistant hypertension into areas like chronic kidney disease and heart failure presents significant long-term growth opportunities. As long-term safety and efficacy data continue to accumulate, renal denervation is poised to become a cornerstone of hypertension management.

Geographically, North America is expected to account for the largest share of the global renal denervation market in 2026, driven by the commercial rollout of FDA-approved renal denervation systems, expanding reimbursement coverage, and increasing physician adoption. Europe continues to represent a significant market due to its longer history of clinical use and supportive hypertension treatment guidelines. Meanwhile, Asia-Pacific is projected to register the fastest growth during the forecast period, supported by the large burden of uncontrolled hypertension, improving healthcare infrastructure, and increasing adoption of advanced interventional therapies in countries such as Japan and China. As clinical evidence, reimbursement support, and physician awareness continue to improve, renal denervation procedure volumes are expected to increase steadily, supporting sustained market expansion through 2036.

The primary driver for the renal denervation market is the recent regulatory clearance and commercial launch of clinically validated systems. FDA approvals have provided the necessary confidence for physicians and payers to adopt the technology. Furthermore, the expansion of reimbursement coverage, including the establishment of specific CPT codes in the U.S., is facilitating patient access. The rising global prevalence of resistant hypertension and the growing patient preference for device-based therapies to reduce the burden of daily medication are also significant drivers.

A major restraint is the need for strict patient selection criteria to ensure procedural success, which can limit the immediate pool of eligible patients. The high initial cost of the procedure and the specialized equipment required also pose challenges, particularly in emerging markets. Furthermore, while short-term data is strong, some physicians remain cautious, awaiting more extensive 5-10 year follow-up data to confirm the long-term sustainability of blood pressure reduction and the overall safety profile of the procedure.

Significant opportunities exist in the expansion of renal denervation into new clinical indications, such as chronic kidney disease, heart failure, and arrhythmias. The integration of AI-driven analytics to identify 'super-responders' through EMR data also presents a major growth path. Furthermore, the development of next-generation chemical-based denervation systems (micro-infusion) could offer a more cost-effective and simplified alternative. The move toward outpatient procedures in Ambulatory Surgical Centers (ASCs) also offers a high potential for market scaling.

A key challenge is overcoming the variable adoption rates among primary care physicians and nephrologists, who are the primary gatekeepers for hypertension patients. Ensuring consistent procedural success across different physician skill levels and anatomical variations is also a persistent challenge. Furthermore, manufacturers must navigate the complex and evolving global regulatory landscapes and prove long-term cost-effectiveness to secure broad reimbursement across all major markets.

The adoption of ultrasound-based renal denervation systems is accelerating following strong evidence from the RADIANCE clinical program and recent regulatory approvals in major markets. In the RADIANCE II trial, ultrasound renal denervation achieved a statistically significant reduction in daytime ambulatory systolic blood pressure compared with sham treatment, supporting its clinical utility in patients with uncontrolled hypertension. The technology's ability to deliver circumferential energy and deeper nerve penetration has strengthened physician confidence and supported adoption in specialized cardiac centers. As hypertension affects an estimated 1.28 billion adults worldwide according to the World Health Organization (WHO), demand for durable device-based treatment options is expected to increase.

Healthcare systems are increasingly favoring minimally invasive therapies that can reduce long-term disease burden and improve patient convenience. Renal denervation is typically performed via a catheter-based approach with short recovery times, supporting its gradual integration into outpatient and ambulatory care settings. The trend is particularly relevant as resistant hypertension affects approximately 10–20% of treated hypertensive patients according to the European Society of Cardiology (ESC), creating demand for scalable treatment alternatives beyond lifelong pharmacotherapy.

Based on technology, the market is segmented into Radiofrequency, Ultrasound, and Micro-infusion. In 2026, the Radiofrequency segment is expected to hold the largest share of the market. This dominance is driven by the extensive clinical history and the massive commercial footprint of Medtronic’s Symplicity platform, which has been the primary focus of early market development.

The Ultrasound-Based segment is projected to witness the fastest growth during the forecast period. The superior depth of denervation and the strong clinical outcomes from the Paradise platform are driving its rapid adoption among interventionalists.

Based on indication, the market is segmented into Resistant Hypertension, Uncontrolled Hypertension, and Others. In 2026, the Resistant Hypertension segment is expected to hold the largest share of the market. This is the primary indication for which current systems are approved and reimbursed, representing the most urgent clinical need.

The Uncontrolled Hypertension segment is projected to witness the fastest growth as indications expand to include patients who may be able to tolerate medication but prefer a device-based solution to reduce their daily pill burden.

North America is expected to hold the largest share of the global renal denervation market in 2026, accounting for approximately 45% of the total revenue. This is due to the rapid commercial launch of FDA-approved systems, a favorable reimbursement landscape with specific CPT codes, and a high concentration of specialized cardiac centers. Key companies operating in the North American market include Medtronic and ReCor Medical.

Asia-Pacific is projected to witness the fastest growth during the forecast period. The region faces a massive hypertension burden, particularly in Japan and China. The recent introduction of ultrasound-based RDN in Japan and the increasing investment in cardiovascular research in China are the primary growth drivers. Key companies operating in the Asia-Pacific market include Otsuka Medical Devices and major global vendors.

The global renal denervation market is highly concentrated, with Medtronic and ReCor Medical currently leading the market following their strategic FDA approvals. However, the landscape is evolving as other major players like Boston Scientific and Otsuka pursue clinical validation for their systems. Competition is centered on clinical data, procedural simplicity, and technical success rates.

Innovation in catheter design focusing on multi-electrode arrays and precision ultrasound is the primary competitive strategy. Companies are also investing in large-scale clinical registries to gather long-term safety and efficacy data. Strategic partnerships with healthcare systems to develop hypertension 'centers of excellence' are also common. Key players in the global renal denervation market include Medtronic plc, ReCor Medical, Inc., Boston Scientific Corporation, Otsuka Medical Devices, Terumo Corporation, Abbott Laboratories, Ablative Solutions, and MicroPort Scientific Corporation.

The market is projected to reach USD 8.64 billion by 2036, growing at a CAGR of 19.6% from 2026 to 2036.

Ultrasound-based renal denervation is the fastest-growing technology due to its depth and precision.

The primary indications are resistant hypertension and uncontrolled hypertension

The Asia-Pacific region is projected to witness the fastest growth due to its high hypertension burden

A sustained 5 mmHg reduction in systolic blood pressure is associated with an approximately 10–15% reduction in major cardiovascular events.

The market is expected to grow at a CAGR of 19.6% during the forecast period 2026–2036.

ReCor Medical currently leads the ultrasound-based segment with its Paradise system.

The need for strict patient selection and the high initial procedure cost are the main restraints.

It offers a permanent solution to reduce blood pressure and can decrease the burden of daily medication.

The market is led by Medtronic, ReCor Medical, Boston Scientific, and Otsuka.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Product

3.2.2. Market Analysis, by Technology

3.2.3. Market Analysis, by Indication

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. FDA Approvals of Medtronic Symplicity and ReCor Paradise Systems

4.2.1.2. Expansion of Reimbursement Coverage and Specific CPT Codes

4.2.1.3. Patient Preference for Device-Based Therapy to Reduce Pill Burden

4.2.2. Restraints

4.2.2.1. Need for Strict Patient Selection Criteria for Procedural Success

4.2.2.2. High Initial Procedure Costs and Specialized Infrastructure

4.2.3. Opportunities

4.2.3.1. Expansion into New Indications like CKD, Heart Failure, and Arrhythmias

4.2.3.2. Integration with AI-Driven Patient Identification and Analytics

4.2.4. Challenges

4.2.4.1. Variable Adoption Rates Among Primary Care Physicians and Nephrologists

4.2.4.2. Requirement for Long-Term Efficacy and Safety Follow-Up Data

4.2.5. Trends

4.2.5.1. Rapid Adoption of Ultrasound-Based Denervation Technology

4.2.5.2. Shift Toward Outpatient Procedures in Ambulatory Surgical Centers (ASCs)

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Renal Denervation Market, by Product

5.1. Overview

5.2. Renal Denervation Catheters

5.3. Generator Systems

5.4. Accessories

6. Global Renal Denervation Market, by Technology

6.1. Overview

6.2. Radiofrequency (RF) Based

6.3. Ultrasound Based

6.4. Micro-infusion Based

7. Global Renal Denervation Market, by Indication

7.1. Overview

7.2. Resistant Hypertension

7.3. Uncontrolled Hypertension

7.4. Chronic Kidney Disease (CKD)

7.5. Others

8. Global Renal Denervation Market, by End User

8.1. Overview

8.2. Hospitals & Cardiac Centers

8.3. Ambulatory Surgical Centers (ASCs)

8.4. Academic & Research Institutes

9. Global Renal Denervation Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. Japan

9.4.2. China

9.4.3. India

9.4.4. Australia

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Dashboard

10.4. Vendor Market Positioning

10.5. Market Share Analysis, 2025

11. Company Profiles

11.1. Medtronic plc

11.2. ReCor Medical, Inc.

11.3. Boston Scientific Corporation

11.4. Otsuka Medical Devices Co., Ltd.

11.5. Terumo Corporation

11.6. Abbott Laboratories

11.7. Ablative Solutions, Inc.

11.8. Mercator MedSystems, Inc.

11.9. Johnson & Johnson MedTech (including Biosense Webster)

11.10. Kona Medical, Inc.

11.11. SoniVie Ltd.

11.12. Symple Surgical Inc.

11.13. MicroPort Scientific Corporation

11.14. CardioSonic Ltd.

11.15. Cordis

12. Appendix

Published Date: Apr-2026

Subscribe to get the latest industry updates