Resources

About Us

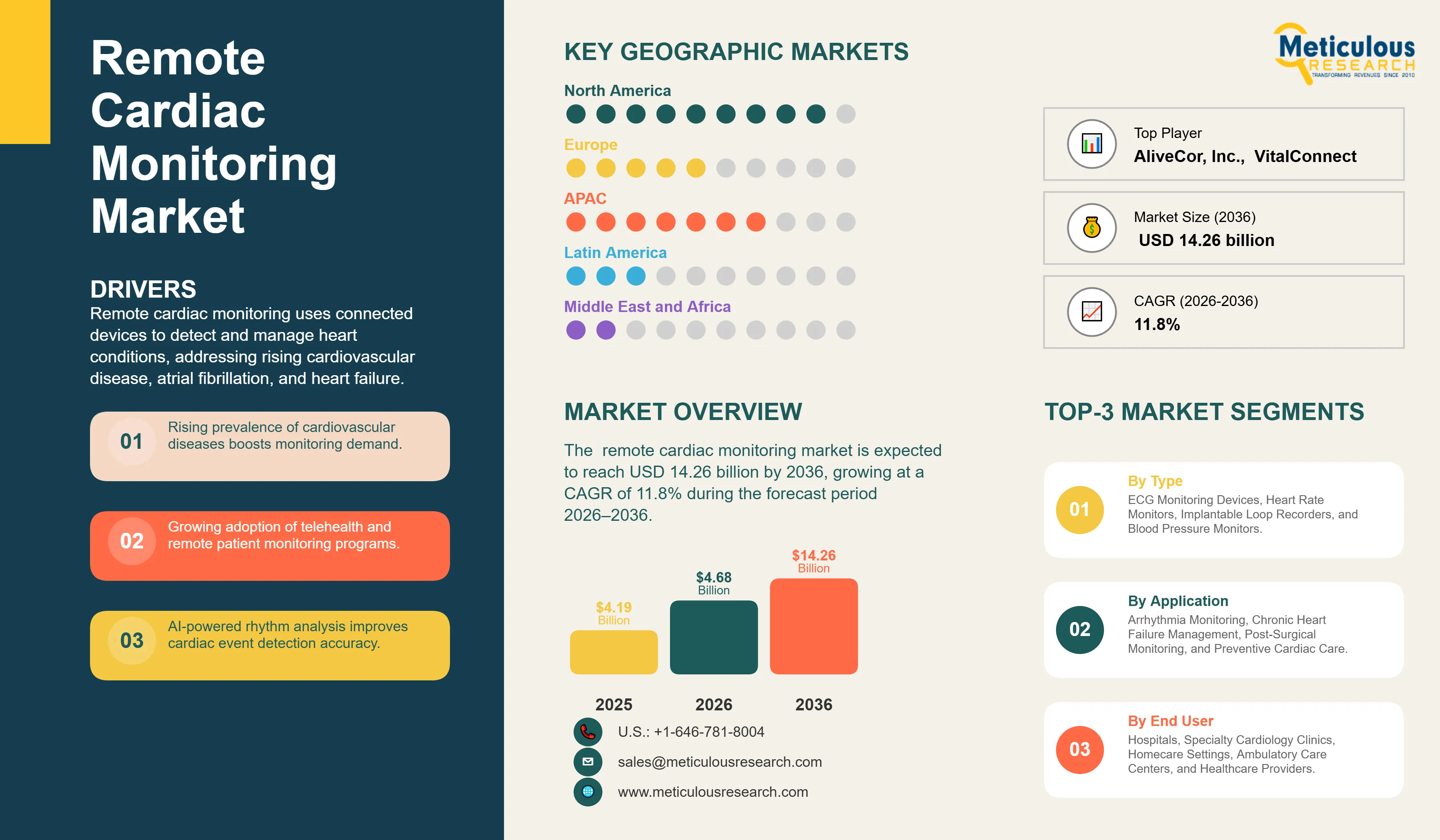

The global remote cardiac monitoring market was valued at USD 4.68 billion in 2026. This market is expected to reach USD 14.26 billion by 2036, growing at a CAGR of 11.8% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this ReportThe market's growth is fundamentally anchored by the convergence of an aging global population, the rising prevalence of chronic cardiac conditions, and the rapid adoption of telehealth services. According to the United Nations, the global population aged 65 years and older is projected to increase from approximately 857 million in 2021 to nearly 1.6 billion by 2050, significantly increasing the incidence of arrhythmias, heart failure, and other age-related cardiovascular disorders. Furthermore, the expansion of remote patient monitoring (RPM) programs has accelerated following the COVID-19 pandemic, as healthcare providers increasingly seek cost-effective solutions that reduce hospital admissions and enable earlier clinical intervention.

Technological innovation is the primary catalyst for market expansion, particularly the development of medical-grade wearables and non-invasive sensors that offer high patient compliance. Modern remote monitoring platforms now incorporate AI-driven rhythm analysis algorithms capable of filtering massive volumes of continuous data to identify clinically significant events with high precision. These tools have demonstrated a 3x higher detection rate for asymptomatic arrhythmias compared to traditional intermittent clinical ECGs. Furthermore, the integration of remote monitoring data into electronic health records (EHR) is enabling more proactive, data-driven clinical decision-making, reducing the likelihood of emergency hospitalizations and improving long-term patient outcomes. In the United States, Medicare spending on remote patient monitoring has surged by over 20x since 2019, reflecting the rapid mainstreaming of these technologies.

The market is also benefiting from a favorable regulatory and reimbursement landscape, with organizations like the Centers for Medicare & Medicaid Services (CMS) expanding CPT codes for remote physiologic monitoring. While hospitals and specialty clinics remain the primary gatekeepers for diagnostic monitoring, the homecare setting is witnessing the fastest growth as patients and providers seek more convenient and cost-effective long-term management models. The competitive landscape is characterized by intense innovation among medical technology giants such as Medtronic, Abbott, and Boston Scientific, alongside specialized digital health firms like iRhythm and AliveCor. These companies are increasingly focusing on cloud-native architectures and predictive analytics to provide actionable insights at the point of care.

Geographically, North America leads the global market. This dominance is driven by the region's advanced healthcare infrastructure, robust reimbursement for remote services, and a high concentration of leading cardiac technology firms. However, the Asia-Pacific region is projected to witness the fastest growth through 2036. Countries like China and India are rapidly modernizing their diagnostic infrastructure to manage their massive patient populations and the increasing burden of CVDs. As remote cardiac monitoring becomes the standard of care for chronic disease management, the market is poised for sustained growth, reaching over USD 14 billion by the end of the forecast period.

The primary driver for the remote cardiac monitoring market is the rising global prevalence of cardiovascular diseases (CVDs). According to the World Heart Federation (2024), an estimated 20.5 million people died from CVD-related causes in 2021, representing 33% of all global deaths. Furthermore, the rapidly aging global population is significantly increasing the pool of patients at risk for chronic heart failure and arrhythmias. The United Nations (2024) reports that 1 in 6 people worldwide will be over the age of 65 by 2050. Technological advancements in medical-grade wearables and AI-driven rhythm analysis have also made remote monitoring more accessible and reliable, while the expansion of reimbursement codes by payers like CMS is incentivizing providers to adopt these tools in routine clinical workflows.

A major restraint is the concern regarding data security and patient privacy, as the continuous transmission of sensitive cardiac data over public networks presents significant cybersecurity risks. Furthermore, the high capital investment required for sophisticated mobile cardiac telemetry (MCT) and implantable loop recorder (ILR) systems can be a barrier to adoption, particularly in budget-constrained healthcare settings and emerging markets. The American Heart Association (2025) notes that the projected annual cost of CVDs in the U.S. alone will exceed USD 1.1 trillion by 2035, putting immense pressure on healthcare budgets and potentially limiting the rapid rollout of high-cost remote monitoring technologies.

Significant opportunities exist in the development of AI-driven predictive analytics that can use long-term monitoring data to identify early warning signs of acute cardiac events before they occur. This shift from reactive to proactive care has the potential to significantly reduce hospital readmissions and associated costs. The expansion of healthcare modernization in emerging markets, such as China, India, and Brazil, where the burden of CVDs is rising rapidly, presents a massive growth path for manufacturers. Furthermore, the integration of remote cardiac monitoring into broader 'hospital-at-home' models offers high potential for improving the management of complex, multi-morbid patients in a more comfortable and cost-effective environment.

A key challenge is the management of the massive volume of continuous data generated by remote monitoring devices, which can lead to 'alert fatigue' and administrative overload for clinicians if not properly filtered by efficient AI algorithms. Ensuring the interoperability of diverse monitoring data into disparate electronic health record (EHR) systems is also a critical technical hurdle. Furthermore, manufacturers must navigate complex and evolving regulatory landscapes across different regions and prove the long-term clinical and economic validity of their systems to secure broad adoption and sustained reimbursement.

There is a clear trend toward the adoption of non-invasive, patch-based ECG monitors over traditional Holter monitors. These devices offer significantly higher patient compliance due to their water-resistant, wire-free design and ability to provide continuous monitoring for up to 14 days, leading to higher diagnostic yields for infrequent arrhythmias.

AI is becoming an integral component of remote cardiac monitoring platforms. Sophisticated algorithms are now capable of performing real-time rhythm analysis, automatically identifying and prioritizing life-threatening arrhythmias for clinician review. This trend is significantly reducing the time to diagnosis and allowing for more timely interventions.

Based on product type, the market is segmented into ECG Monitoring Devices, Heart Rate Monitors, Implantable Loop Recorders (ILRs), and Blood Pressure Monitors. In 2026, the ECG Monitoring Devices segment is expected to hold the largest share of the market. This segment includes Holter monitors, patch-based ECGs, and Mobile Cardiac Telemetry (MCT). The dominance is driven by the critical role of continuous ECG tracking in the definitive diagnosis of arrhythmias.

The Patch-based ECGs and Smart Wearables sub-segment is projected to witness the fastest growth, as patients increasingly prefer non-invasive, comfortable monitoring solutions that do not disrupt their daily activities.

Based on application, the market is segmented into Arrhythmia Monitoring, Chronic Heart Failure (CHF) Management, and Post-Surgical Monitoring. In 2026, the Arrhythmia Monitoring segment is expected to hold the largest share of the market. Atrial fibrillation (AFib) is the most common cardiac rhythm disorder, affecting millions globally and requiring long-term tracking to manage stroke risk.

The Chronic Heart Failure (CHF) Management segment is projected to witness the fastest growth during the forecast period, as healthcare systems focus on reducing costly hospital readmissions through proactive fluid status and vital sign tracking.

North America is expected to hold the largest share of the global remote cardiac monitoring market in 2026, accounting for approximately 42% of total revenue. This dominance is due to the region's advanced healthcare infrastructure, favorable reimbursement policies for remote monitoring services, and the presence of major industry players like Medtronic and Abbott. The high prevalence of CVDs in the U.S. also drives significant demand for remote monitoring solutions.

Asia-Pacific is projected to witness the fastest growth during the forecast period. The region is rapidly modernizing its healthcare infrastructure and adopting digital health solutions to manage its massive and aging patient populations. The rising burden of cardiovascular diseases in countries like China and India is the primary growth driver. Key companies operating in the Asia-Pacific market include major global vendors and emerging local medical technology firms.

The global remote cardiac monitoring market is characterized by intense competition between established medical technology giants and specialized digital health firms. Medtronic, Abbott, and Boston Scientific maintain strong positions through their broad portfolios of implantable and wearable monitoring devices, while specialized vendors like iRhythm and AliveCor lead in developing advanced AI-driven software and patch-based solutions. Competition is focused on diagnostic accuracy, patient compliance, and the ability to provide actionable insights through integrated data platforms.

Strategic acquisitions and partnerships are common as companies seek to expand their monitoring capabilities and secure enterprise-wide contracts. Key players in the global market include Medtronic plc, Abbott Laboratories, Boston Scientific Corporation, GE HealthCare, Philips Healthcare, Baxter International (Hillrom), Nihon Kohden Corporation, Biotronik, iRhythm Technologies, BioTelemetry (Philips), Bardy Diagnostics (Baxter), Preventice Solutions (Boston Scientific), AliveCor, VitalConnect, and Cardiac Insight.

The market is projected to reach USD 14,260.4 million by 2036, growing at a CAGR of 11.8% from 2026 to 2036.

Remote monitoring tools demonstrate a 3x higher detection rate for asymptomatic AFib compared to traditional intermittent clinical ECGs.

CVDs account for an estimated 20.5 million deaths annually, representing approximately 33% of all global mortality.

The Asia-Pacific region is projected to witness the fastest growth due to rapid infrastructure modernization and a rising burden of CVDs.

Medicare spending on RPM has surged by more than 20x since 2019, reflecting its integration into standard clinical workflows.

The market is expected to grow at a CAGR of 11.8% during the forecast period 2026–2036

Arrhythmia Monitoring holds the largest share, as it is the most common condition requiring long-term cardiac tracking.

Data security concerns, the high cost of advanced systems, and interoperability issues with EHRs are the primary restraints.

AI filters massive volumes of continuous data to identify and prioritize clinically significant rhythm events for clinician review.

The market is led by Medtronic, Abbott, Boston Scientific, GE HealthCare, and Philips Healthcare.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Process of Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/Interviews with Key Opinion Leaders

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Product Type

3.2.2. Market Analysis, by Component

3.2.3. Market Analysis, by Application

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Rising Global Prevalence of Cardiovascular Diseases (CVDs)

4.2.1.2. Rapidly Aging Global Population and Increased Risk of Arrhythmias

4.2.1.3. Technological Advancements in Medical-Grade Wearables and AI

4.2.1.4. Expansion of Reimbursement Codes for Remote Physiologic Monitoring

4.2.2. Restraints

4.2.2.1. Significant Concerns Regarding Data Security and Patient Privacy

4.2.2.2. High Capital Investment for Sophisticated Monitoring Systems

4.2.3. Opportunities

4.2.3.1. Development of AI-Driven Predictive Analytics for Proactive Care

4.2.3.2. Expansion of Healthcare Modernization in Emerging APAC and LATAM Markets

4.2.3.3. Integration into Comprehensive 'Hospital-at-Home' Care Models

4.2.4. Challenges

4.2.4.1. Managing Data Overload and Alert Fatigue for Clinicians

4.2.4.2. Ensuring Interoperability Across Disparate EHR and IT Systems

4.2.5. Trends

4.2.5.1. Proliferation of Patch-Based ECG Monitors Over Traditional Holters

4.2.5.2. Increasing Integration of AI for Real-Time Clinical Rhythm Analysis

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Remote Cardiac Monitoring Market, by Product Type

5.1. Overview

5.2. ECG Monitoring Devices

5.2.1. Holter Monitors

5.2.2. Patch-based ECGs

5.2.3. Mobile Cardiac Telemetry (MCT)

5.3. Heart Rate Monitors

5.4. Implantable Loop Recorders (ILRs)

5.5. Blood Pressure Monitors

6. Global Remote Cardiac Monitoring Market, by Component

6.1. Overview

6.2. Hardware/Devices

6.3. Software & Platforms

6.4. Services

7. Global Remote Cardiac Monitoring Market, by Application

7.1. Overview

7.2. Arrhythmia Monitoring

7.3. Chronic Heart Failure (CHF) Management

7.4. Post-Surgical Monitoring

8. Global Remote Cardiac Monitoring Market, by End User

8.1. Overview

8.2. Hospitals & Specialty Clinics

8.3. Ambulatory Surgery Centers (ASCs)

8.4. Homecare Settings

9. Global Remote Cardiac Monitoring Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. Australia

9.4.5. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Growth Strategies

10.3. Competitive Dashboard

10.4. Vendor Market Positioning

10.5. Market Share Analysis, 2025

11. Company Profiles

11.1. Medtronic plc

11.2. Abbott Laboratories

11.3. Boston Scientific Corporation

11.4. GE HealthCare Technologies Inc.

11.5. Koninklijke Philips N.V.

11.6. Baxter International Inc. (Hillrom)

11.7. Nihon Kohden Corporation

11.8. Biotronik SE & Co. KG

11.9. iRhythm Technologies, Inc.

11.10. BioTelemetry, Inc. (Philips)

11.11. Bardy Diagnostics, Inc. (Baxter)

11.12. Preventice Solutions (Boston Scientific)

11.13. AliveCor, Inc.

11.14. VitalConnect

11.15. Cardiac Insight, Inc.

12. Appendix

Published Date: Jul-2026

Published Date: Feb-2026

Published Date: Jan-2025

Published Date: Mar-2024

Subscribe to get the latest industry updates