Resources

About Us

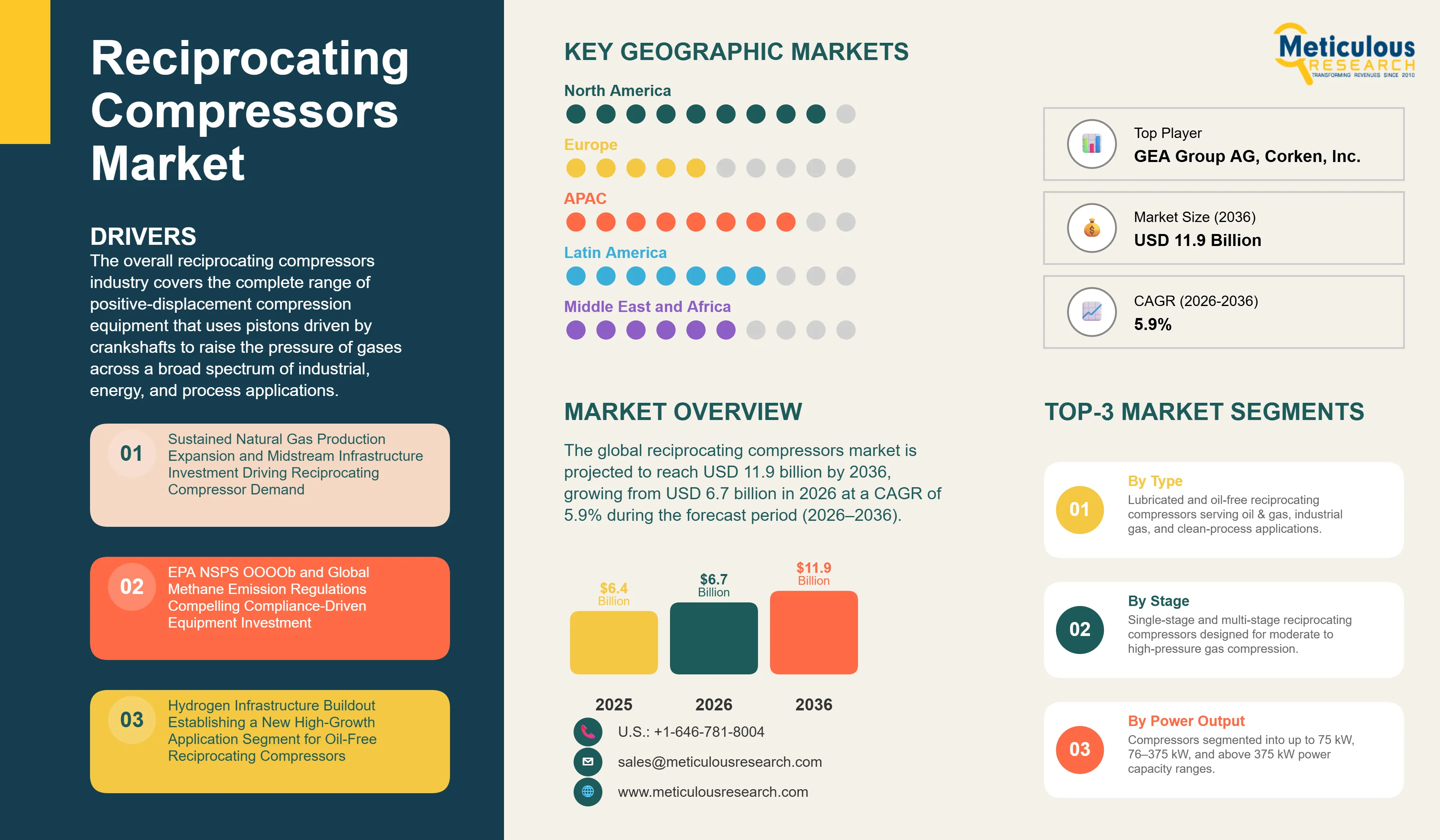

The global reciprocating compressors market was valued at USD 6.4 billion in 2025. The market is projected to reach USD 11.9 billion by 2036, growing from USD 6.7 billion in 2026 at a CAGR of 5.9% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The overall reciprocating compressors industry covers the complete range of positive-displacement compression equipment that uses pistons driven by crankshafts to raise the pressure of gases across a broad spectrum of industrial, energy, and process applications. The market encompasses lubricated and oil-free reciprocating compressors, single-stage and multi-stage configurations, and power outputs ranging from sub-kilowatt units deployed in laboratory and instrumentation applications to large-frame machines exceeding several thousand kilowatts used in high-pressure natural gas gathering, pipeline transmission, gas storage injection, and petrochemical processing. End-use industries served include oil and gas, chemical and petrochemical, industrial gas production, power generation, food and beverage processing, pharmaceutical manufacturing, and general industrial manufacturing.

Reciprocating compressors are distinguished from other compressor technologies by their positive-displacement operating principle, which enables them to achieve higher compression ratios per stage and to handle a wider range of gas compositions, including wet gases, sour gases, hydrogen-rich streams, and process gases with variable molecular weight, compared to rotary and centrifugal compressor designs. This unique capability makes reciprocating compressors the preferred technology for demanding oil and gas applications including gas gathering from high-pressure wellheads, gas reinjection for enhanced oil recovery, pipeline booster compression, and storage reservoir injection and withdrawal cycles where the ability to achieve high discharge pressures reliably over extended continuous-duty operating periods is a primary performance requirement.

The growth of the reciprocating compressors market is primarily driven by the sustained expansion of natural gas production, transportation, and utilization infrastructure globally. According to the U.S. Energy Information Administration, U.S. dry natural gas production reached a record 103.8 billion cubic feet per day in 2023, continuing a multi-year expansion of shale gas output across the Permian Basin, Appalachian Basin, and Haynesville Shale formations that has created sustained demand for reciprocating compression equipment across gathering, processing, and transmission infrastructure. The United States became the world's largest exporter of liquefied natural gas in 2023, further reinforcing demand for high-capacity reciprocating compression in feed gas conditioning, liquefaction pre-treatment, and boil-off gas recompression service at export terminals.

Regulatory developments are reshaping the operational and compliance economics of reciprocating compressor ownership across major industrial markets. In the United States, the U.S. EPA finalized the Standards of Performance for Crude Oil and Natural Gas Facilities at New, Reconstructed, and Modified Sources and Emissions Guidelines for Existing Sources under 40 CFR Parts 60 and 63 in December 2023, commonly referred to as NSPS OOOOb. This regulation directly addresses reciprocating compressor operations by specifying rod packing replacement requirements and emission monitoring obligations for operators of natural gas compression equipment at well sites, gathering and processing facilities, and transmission compressor stations. Complementing this, the methane emissions charge established under the Inflation Reduction Act of 2022, which began applying to reported methane emissions from oil and gas facilities for calendar year 2024, creates a direct financial incentive for operators to minimize fugitive emissions from reciprocating compressor rod packing and valve assemblies, accelerating investment in modern low-emission compressor designs and high-performance sealing materials. In Europe, the European Union Methane Regulation, which entered into force in August 2024 and establishes binding requirements for monitoring, reporting, and reduction of methane emissions from the oil and gas sector, is similarly driving operational scrutiny of compression equipment performance across European upstream and midstream infrastructure.

In addition to regulatory compliance, the emerging role of reciprocating compressors in hydrogen infrastructure is creating a structurally new and rapidly expanding demand segment. The U.S. Department of Energy's allocation of USD 7 billion in October 2023 for seven regional clean hydrogen hubs under the Infrastructure Investment and Jobs Act is generating initial demand for high-pressure hydrogen compression equipment, with reciprocating compressors serving as the technology of choice for compression to pressures above 200 bar, where their ability to handle the unique thermodynamic characteristics of low-molecular-weight hydrogen gas at high compression ratios provides a clear performance advantage over rotary and centrifugal alternatives. Similar hydrogen infrastructure investment is advancing across Europe under the EU Hydrogen Strategy and National Hydrogen Plans and in Japan and South Korea through government-funded hydrogen supply chain development programs, positioning reciprocating compressors as a key enabling technology in the global energy transition.

Despite strong structural demand fundamentals, the reciprocating compressors market faces challenges related to the inherently higher maintenance requirements of piston-based compression equipment compared to rotary alternatives. Reciprocating compressors require planned maintenance of dynamic sealing components including piston rings, rod packing, and suction and discharge valve assemblies, contributing to higher lifecycle maintenance costs and longer planned downtime intervals compared to screw and centrifugal compressors in comparable pressure and flow applications. The availability of technically skilled field service personnel capable of maintaining reciprocating compressor installations in remote oil field environments and processing facilities is becoming an increasingly significant operational constraint for end users as the workforce skilled in this equipment type ages in major industrial markets.

Significant market opportunities are emerging from the growing adoption of digital monitoring and predictive maintenance platforms for reciprocating compressor fleet management, the accelerating demand for high-pressure oil-free reciprocating compressors in hydrogen refueling station infrastructure and industrial gas production, and the sustained investment in natural gas production and transportation infrastructure across Asia Pacific and the Middle East where governments are actively expanding the role of natural gas in their domestic energy mixes as part of transition-period energy policy.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 11.9 Billion |

|

Market Size in 2026 |

USD 6.7 Billion |

|

Market Size in 2025 |

USD 6.4 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 5.9% |

|

Dominating Type |

Lubricated Reciprocating Compressors |

|

Fastest Growing Type |

Oil-Free Reciprocating Compressors |

|

Dominating Stage |

Multi-Stage Reciprocating Compressors |

|

Fastest Growing Stage |

Single-Stage Reciprocating Compressors |

|

Dominating Power Output |

Above 375 kW |

|

Fastest Growing Power Output |

Up to 75 kW |

|

Dominating End-use Industry |

Oil & Gas |

|

Fastest Growing End-use Industry |

Industrial Gas |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

EPA NSPS OOOOb and Global Methane Emission Regulations Driving Compliance-Led Reciprocating Compressor Upgrades

The finalization of U.S. EPA's NSPS OOOOb in December 2023 marks one of the most consequential regulatory developments affecting reciprocating compressor ownership economics in the oil and gas sector in recent years. The regulation introduces updated performance standards and emission control obligations specifically applicable to reciprocating compressors at new and existing crude oil and natural gas facilities, requiring operators to meet defined rod packing emission thresholds and to maintain documented maintenance records demonstrating compliance with equipment servicing obligations. For operators managing large compressor fleets across gathering systems, processing plants, and transmission stations, these requirements translate into structured investment cycles for rod packing replacement, valve maintenance, and in many cases, compressor frame replacement or upgrade to newer models offering superior emission performance and improved sealing system durability.

The Inflation Reduction Act's methane emissions charge, effective for calendar year 2024 reporting periods, further alters the economic calculus of operating aging, poorly sealed reciprocating compression equipment. Facilities emitting methane above established waste emissions thresholds face direct monetary charges per metric ton of excess methane, creating a financial incentive to invest in modern compressor systems equipped with advanced rod packing materials and low-emission design features that reduce fugitive losses during normal operation. Leading manufacturers including Ariel Corporation and Siemens Energy have responded by developing compressor designs and aftermarket sealing upgrades specifically targeted at enabling operators to achieve compliance with these emission performance thresholds.

Beyond North America, Europe's EU Methane Regulation, which entered into force in August 2024, requires operators across the EU oil and gas supply chain to implement leak detection and repair programs and to report methane emissions from compression equipment in accordance with defined methodologies. This is accelerating equipment audit cycles and driving capital investment in newer, more emission-compliant reciprocating compressor installations across European upstream and midstream operations. Taken together, these regulatory developments are transforming reciprocating compressor procurement from periodic capital replacement toward strategically timed compliance-driven investment cycles, broadening addressable demand and creating structured replacement demand for modern low-emission compression equipment across North American and European markets.

Hydrogen Infrastructure Expansion Creating a High-Growth Application Segment for Oil-Free Reciprocating Compressors

The accelerating global buildout of hydrogen production, distribution, and end-use infrastructure is establishing reciprocating compressors, particularly oil-free configurations, as a critical enabling technology in the energy transition. Hydrogen's low molecular weight, high diffusivity, and tendency toward embrittlement of metallic components at high pressures make it one of the most technically demanding gases to compress reliably, and the positive-displacement operating principle and multi-stage design capability of reciprocating compressors make them the best-suited technology for achieving the very high discharge pressures required for hydrogen refueling station cascade storage, pipeline injection, and geological storage applications.

The U.S. DOE's seven regional clean hydrogen hub awards, announced in October 2023 and totaling USD 7 billion in federal funding, are driving initial capital project planning and equipment procurement across a portfolio of projects spanning electrolytic, natural gas reforming with carbon capture, and biomass-based hydrogen production pathways, each of which requires significant reciprocating compression capacity for hydrogen handling at pressure. In parallel, the European Hydrogen Bank's first auction round concluded in 2024, awarding EUR 720 million to green hydrogen production projects across the European Union, providing an additional source of funded demand for oil-free reciprocating compression equipment in electrolytic hydrogen production and downstream compression applications.

Manufacturers including Burckhardt Compression AG, Hofer Hochdrucktechnik GmbH, and Neuman & Esser Group have positioned their oil-free piston compressor platforms specifically for hydrogen service, offering designs that address hydrogen-specific challenges including material compatibility with hydrogen embrittlement, enhanced piston ring seal performance at high pressure, and ATEX-rated electrical configurations for safe operation in hydrogen environments. The demand for oil-free reciprocating compression in hydrogen applications is expected to grow significantly over the forecast period as hydrogen infrastructure moves from pilot and demonstration scale toward commercial deployment across North America, Europe, and Asia Pacific, establishing hydrogen as the fastest-growing application within the broader oil-free reciprocating compressors segment.

Digital Monitoring and Predictive Maintenance Platforms Redefining Reciprocating Compressor Fleet Management

The integration of industrial IoT sensors, connectivity, and advanced analytics into reciprocating compressor monitoring platforms is fundamentally transforming the economics of owning, operating, and maintaining large compression equipment fleets across oil and gas gathering, transmission, and processing applications. Historically, reciprocating compressor maintenance was driven by fixed-interval schedules based on calendar time or operating hours, resulting in either premature component replacement before failure would occur or, in the opposite case, continued operation with degrading components that contributed to unplanned shutdowns, production losses, and increased emission events from worn rod packing and valve assemblies.

Connected monitoring platforms, such as Ariel Corporation's Ariel Connect system and Siemens Energy's REMOTE360 digital service platform, deploy real-time sensors monitoring cylinder pressure and temperature profiles, rod load, vibration signatures, valve performance, and lube oil conditions to continuously evaluate the health of each major compressor component and to predict maintenance needs based on actual operating data rather than fixed schedules. This approach allows operators to identify developing valve failures, worn piston rings, and deteriorating rod packing conditions weeks before they would cause production-impacting failures, enabling maintenance to be planned and executed during scheduled downtime windows at a fraction of the cost of responding to unplanned equipment outages.

The business case for connected compressor monitoring is particularly compelling for operators managing geographically dispersed compression fleets in remote production areas, where dispatching field technicians for unplanned repair events carries significant logistical cost and where NSPS OOOOb compliance obligations require documented evidence of equipment performance and maintenance activity. Burckhardt Compression's PROGNOST Systems intelligent condition monitoring platform and Hoerbiger's digital valve monitoring solutions similarly demonstrate the growing commitment of major reciprocating compressor suppliers to providing integrated equipment, monitoring software, and lifecycle service offerings that shift customer engagement from transactional equipment sales toward performance-based service contracts. This trend is generating new recurring revenue streams for compressor manufacturers while improving customer loyalty and reducing total cost of ownership for end users managing high-utilization compression assets.

By Type: In 2026, the Lubricated Reciprocating Compressors Segment to Dominate the Global Reciprocating Compressors Market

Based on type, the reciprocating compressors industry is segmented into lubricated reciprocating compressors and oil-free reciprocating compressors. In 2026, the lubricated reciprocating compressors segment is expected to account for the largest share of this market. The leading position of this segment reflects the overwhelming prevalence of lubricated reciprocating compressors across the oil and gas sector, which represents the largest end-use industry in the global market by revenue. Lubricated reciprocating compressors are designed with cylinder lubrication systems that introduce controlled quantities of lubricating oil into the compression cylinder, providing superior piston ring and packing seal life, reduced metal-to-metal wear, and the mechanical durability required for continuous-duty, high-pressure service in demanding environments including sour gas, wet gas, and high-molecular-weight hydrocarbon streams. Manufacturers including Ariel Corporation, Exterran Corporation, and Siemens Energy have developed extensive product portfolios of lubricated reciprocating compressors spanning a broad range of frame sizes and pressure ratings to serve oil and gas gathering, transmission, storage, and processing applications.

However, the oil-free reciprocating compressors segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by its expanding adoption across pharmaceutical manufacturing, food and beverage processing, industrial gas production, and hydrogen compression applications where any level of lubricant carryover into the compressed gas stream is incompatible with product purity requirements, regulatory standards, or downstream process chemistry. The growing hydrogen infrastructure investment noted in the key trends section is a particularly significant driver of oil-free reciprocating compressor demand, as hydrogen applications require complete absence of hydrocarbon contamination at the very high compression pressures that oil-free reciprocating designs are uniquely capable of achieving. Leading manufacturers including Burckhardt Compression AG and Neuman & Esser Group are investing in advanced non-lubricated piston ring and rider ring material technologies, including polytetrafluoroethylene and carbon-filled polymer compounds, to extend the service intervals of oil-free reciprocating compressors in demanding high-pressure applications and to broaden their competitive reach against alternative non-lubricated compressor technologies in industrial gas markets.

By Stage: In 2026, the Multi-Stage Reciprocating Compressors Segment to Hold the Largest Share

Based on stage, the reciprocating compressors industry is segmented into single-stage and multi-stage reciprocating compressors. In 2026, the multi-stage reciprocating compressors segment is expected to account for the largest share of this market. This reflects the technical requirements of the oil and gas sector applications that dominate the global market by revenue, where suction pressures, discharge pressure requirements, and gas throughput volumes make multi-stage compression with interstage cooling essential for achieving thermodynamically efficient operation and for managing discharge temperatures within safe operating limits. Pipeline transmission compressor stations, gas storage injection facilities, and gas processing plants each typically require multi-stage reciprocating compression frames capable of handling high inlet flow rates and achieving discharge pressures in the range of 100 to 1,000 bar or above, applications for which no single-stage reciprocating configuration can provide a cost-effective solution.

However, the single-stage reciprocating compressors segment is projected to register the highest growth during the forecast period. The growth of this segment is driven by the expanding adoption of single-stage reciprocating units in light industrial manufacturing environments, food and beverage processing facilities, pharmaceutical production applications, and small-scale natural gas compression installations where moderate pressure ratios and flow rates make single-stage configurations the most cost-effective option. The ongoing growth of small and mid-size enterprise manufacturing across Asia Pacific and Latin America is generating broad-based demand for entry-level reciprocating compressor capacity, and the increasing availability of compact, low-noise single-stage oil-free reciprocating compressors from manufacturers including Atlas Copco AB and Ingersoll Rand Inc. is improving accessibility for operators in these segments who previously relied on alternative compressor technologies for moderate-pressure process air and gas supply requirements.

By Power Output: In 2026, the Above 375 kW Segment to Account for the Largest Share

Based on power output, the reciprocating compressors industry is segmented into up to 75 kW, 76 kW to 375 kW, and above 375 kW. In 2026, the above 375 kW segment is expected to account for the largest share of this market by revenue, driven by the dominance of large-frame reciprocating compressors in oil and gas gathering, pipeline transmission, gas storage, and petrochemical processing applications that constitute the highest-value portion of the global market. These large-frame units, which include Ariel Corporation's JGT, JGM, and JGQ compressor frame families and Siemens Energy's Dresser-Rand DATUM and HHE-VG product lines, are typically configured as custom-engineered packages with gas coolers, scrubbers, controls, and supporting auxiliary systems, representing multi-million-dollar capital investments per installation unit and generating significant aftermarket parts and service revenue over their extended operating lives.

However, the up to 75 kW segment is projected to register the highest growth during the forecast period. The high growth of this segment reflects the rapid expansion of demand for small-capacity oil-free reciprocating compressors in pharmaceutical manufacturing, food and beverage processing, laboratory and analytical instrumentation, and small-scale industrial applications across emerging markets in Asia Pacific and Latin America where manufacturing capacity in these sectors is growing rapidly. The increasing adoption of compact, low-maintenance oil-free reciprocating compressors by small and mid-size enterprises that previously used rotary vane or small screw compressors is also contributing to growth in this power output range, as operators in regulated industries seek oil-free compressed air and gas supply solutions that offer superior pressure capability and lower lifecycle cost than alternative technologies at comparable capacity.

By End-Use Industry: In 2026, the Oil & Gas Segment to Hold the Largest Share

Based on end-use industry, the reciprocating compressors industry is segmented into oil and gas, chemical and petrochemical, industrial gas, power generation, food and beverage processing, pharmaceutical and healthcare, and other end-use industries. In 2026, the oil and gas segment is expected to account by far for the largest share of this market, reflecting the foundational role of reciprocating compression equipment across all phases of oil and gas production, processing, and transportation. In the upstream sector, reciprocating compressors are deployed for gas gathering at wellheads and production facilities, gas lift injection for artificial lift of producing wells, and vapor recovery at tank batteries and production facilities. In the midstream sector, reciprocating compressor stations provide the primary compression capacity for natural gas gathering lines, processing plant feed gas compression, and transmission pipeline booster stations. In the downstream sector, reciprocating compressors handle hydrogen-rich recycle gas, process gas compression in refinery hydrotreating and hydrocracking units, and refrigerant gas compression in ethylene and other petrochemical process plants. OSHA's Process Safety Management standard and EPA's Risk Management Program, which apply to oil and gas processing facilities handling covered hazardous substances, sustain structured compliance-driven maintenance and equipment replacement investment within this segment across North American and European markets.

However, the industrial gas segment is projected to register the highest growth during the forecast period. The high growth of this segment is driven by the accelerating demand for high-pressure compression of hydrogen, oxygen, nitrogen, and specialty gases for energy transition applications and expanding industrial end uses. Hydrogen, in particular, is emerging as the fastest-growing application within the industrial gas end-use segment, with investment in electrolytic hydrogen production facilities, hydrogen pipeline infrastructure, and high-pressure hydrogen refueling stations driving demand for oil-free multi-stage reciprocating compressors capable of achieving the discharge pressures required for cascade storage at hydrogen vehicle refueling stations and for pipeline injection and geological storage. Traditional industrial gas production for established applications including nitrogen generation for inerting and purging, oxygen compression for steel and glass production, and specialty gas filling operations are additionally sustaining baseline demand growth aligned with global manufacturing expansion.

Based on geography, the overall reciprocating compressors market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of this market. The dominant position of North America reflects the region's unmatched scale of natural gas production and midstream infrastructure, sustained by record-level shale gas and associated gas output from the Permian Basin, Appalachian Basin, and other major producing regions that collectively require thousands of reciprocating compression units across gathering, processing, and transmission operations. The United States' position as the world's largest LNG exporter as of 2023 has additionally reinforced demand for high-capacity reciprocating compression in feed gas pre-treatment and liquefaction support applications at Gulf Coast export terminals. The regulatory environment established by EPA NSPS OOOOb and the IRA methane charge is compelling structured equipment replacement and compliance upgrade investment across the region's large installed base of oil and gas compression equipment. The presence of leading manufacturers including Ariel Corporation, Exterran Corporation, Ingersoll Rand Inc., and Sundyne Corporation ensures a deep local supply base and comprehensive aftermarket parts and service infrastructure that supports procurement confidence among North American industrial buyers.

However, the Asia Pacific reciprocating compressors market is expected to grow at the fastest rate from 2026 to 2036. The rapid growth of this market is driven by the sustained expansion of natural gas production and distribution infrastructure across China, India, and Southeast Asia, where government policy actively supports the development of domestic gas supply chains as a cleaner-burning transition fuel. According to the National Bureau of Statistics of China, China's natural gas production grew to approximately 232 billion cubic meters in 2023, reflecting continued investment in domestic gas exploration and production that supports demand for reciprocating compression across upstream and gathering infrastructure. India's Petroleum and Natural Gas Regulatory Board is overseeing the expansion of the national gas pipeline network toward an interconnected national gas grid, requiring significant new compression capacity at pipeline stations and terminal facilities. The rapid growth of petrochemical manufacturing across Southeast Asia, supported by substantial foreign direct investment into refinery and chemical complex expansion in countries including Vietnam, Indonesia, and Malaysia, is creating growing demand for process gas reciprocating compressors across refinery hydrogen, ethylene, and specialty chemical applications. Additionally, the expansion of industrial gas production capacity across the region to serve growing manufacturing industries is sustaining structural demand for oil-free reciprocating compression in oxygen, nitrogen, and hydrogen production applications.

Europe is a large, technologically mature market for reciprocating compressors, supported by a strong regulatory framework encompassing the EU Methane Regulation, the Industrial Emissions Directive, and national occupational health and environmental standards that collectively drive sustained compliance-led investment across the region's oil and gas, petrochemical, and industrial manufacturing sectors. European manufacturers including Burckhardt Compression AG, Neuman & Esser Group, GEA Group AG, and Hoerbiger Holding AG maintain strong market positions across European and global markets, supported by deep application engineering capabilities and established aftermarket service networks. The growing emphasis on hydrogen infrastructure development under the EU Hydrogen Strategy is creating a new, high-value demand segment for European oil-free reciprocating compressor manufacturers with established capabilities in hydrogen service compressor design and certification.

The Middle East and Africa market is an important and growing segment for large-frame lubricated reciprocating compressors serving oil and gas production, gas reinjection for reservoir pressure maintenance, and gas gathering across the region's extensive hydrocarbon production infrastructure. National oil companies and international oil company operators in Saudi Arabia, the UAE, Qatar, and Kuwait continue to invest in compression capacity to support production plateau maintenance and upstream gas management objectives. Latin America represents a steady-growth market driven by oil and gas production activities in Brazil, Argentina, and other producing countries, as well as growing petrochemical manufacturing capacity supported by regional energy resource development.

The global reciprocating compressors market is moderately consolidated at the large-frame oil and gas segment level, where a small number of manufacturers with deep application engineering expertise and established API 618 compliance capabilities compete for high-value capital projects, and more fragmented in the smaller-capacity industrial and oil-free segments where a broader range of domestic and regional manufacturers serve local markets. Key competitive differentiators include the breadth of compressor frame sizes and configurations available for specific end-use applications, the strength of aftermarket parts and service capabilities, API 618 and API 11P design compliance for oil and gas service, ATEX and NEC explosion-proof certification for hazardous area installation, the availability of integrated package engineering including gas coolers, scrubbers, and control systems, and the depth of application-specific engineering expertise for demanding services including hydrogen, sour gas, and high-molecular-weight hydrocarbon streams.

Large diversified industrial machinery manufacturers such as Siemens Energy AG and Atlas Copco AB compete through comprehensive product portfolios spanning multiple compressor technologies, strong global service networks, and advanced digital monitoring and performance management platforms. Specialty reciprocating compressor manufacturers including Ariel Corporation and Burckhardt Compression AG compete through unmatched application depth in their respective primary markets, with Ariel holding a commanding position in North American separable gas compressor applications and Burckhardt Compression recognized globally for its oil-free piston compressor and diaphragm compressor capabilities in high-pressure and clean-service applications. Regional and application-focused manufacturers including Exterran Corporation, Neuman & Esser Group, Kobelco Compressors Corporation, and Mitsubishi Heavy Industries Compressor Corporation maintain competitive positions in their respective primary markets through customized engineering and integrated compression system capabilities.

The report provides a comprehensive competitive analysis based on assessment of key players' product portfolios, geographic presence, and strategic initiatives undertaken over the past several years.

Some of the key players operating in the global reciprocating compressors market include Ariel Corporation (U.S.), Siemens Energy AG (Germany), Burckhardt Compression AG (Switzerland), Atlas Copco AB (Sweden), Ingersoll Rand Inc. (U.S.), Chart Industries, Inc. (U.S.), Exterran Corporation (U.S.), Kobelco Compressors Corporation (Japan), Mitsubishi Heavy Industries Compressor Corporation (Japan), GEA Group AG (Germany), Sundyne Corporation (U.S.), Neuman & Esser Group (Germany), Corken, Inc. (U.S.), Hitachi Industrial Equipment Systems Co., Ltd. (Japan), and Shenyang Yuanda Compressor Co., Ltd. (China), among others.

The global reciprocating compressors market is expected to reach USD 11.9 billion by 2036 from an estimated USD 6.7 billion in 2026, at a CAGR of 5.9% during the forecast period 2026–2036.

In 2026, the lubricated reciprocating compressors segment is expected to hold the largest share of this market, driven by its dominant deployment across oil and gas, petrochemical, and heavy industrial applications where its robust design and high-pressure capability make it the technology of choice for continuous-duty service.

The oil-free reciprocating compressors segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by its accelerating adoption in pharmaceutical manufacturing, food and beverage processing, industrial gas production, and hydrogen compression infrastructure where hydrocarbon-free compressed gas is a mandatory operating requirement.

In 2026, the multi-stage reciprocating compressors segment is expected to hold the largest share of this market, reflecting its essential role in high-pressure oil and gas gathering, pipeline transmission, gas storage, and petrochemical processing applications that constitute the highest-value portion of the global market.

In 2026, the above 375 kW segment is expected to hold the largest share of this market, driven by the prevalence of large-frame reciprocating compressors in oil and gas and petrochemical applications where high-capacity, high-pressure compression equipment represents the primary capital investment category.

In 2026, the oil and gas segment is expected to hold the largest share of this market, reflecting the foundational role of reciprocating compression equipment across upstream production, midstream gathering and transmission, and downstream refining and petrochemical processing operations globally.

The growth of this market is primarily driven by sustained natural gas production and midstream infrastructure expansion in North America and Asia Pacific, the tightening of methane emission regulations including U.S. EPA NSPS OOOOb and the EU Methane Regulation compelling compliance-driven equipment investment, the emergence of hydrogen infrastructure as a new high-growth application segment for oil-free reciprocating compressors, the integration of digital monitoring and predictive maintenance platforms that improve fleet management economics, and the rapid growth of industrial gas and petrochemical manufacturing capacity across Asia Pacific.

Key players in the global reciprocating compressors market include Ariel Corporation (U.S.), Siemens Energy AG (Germany), Burckhardt Compression AG (Switzerland), Atlas Copco AB (Sweden), Ingersoll Rand Inc. (U.S.), Chart Industries, Inc. (U.S.), Exterran Corporation (U.S.), Kobelco Compressors Corporation (Japan), Mitsubishi Heavy Industries Compressor Corporation (Japan), GEA Group AG (Germany), Sundyne Corporation (U.S.), Neuman & Esser Group (Germany), Corken, Inc. (U.S.), Hitachi Industrial Equipment Systems Co., Ltd. (Japan), and Shenyang Yuanda Compressor Co., Ltd. (China).

Asia Pacific is expected to register the highest growth rate in the global reciprocating compressors market during the forecast period 2026–2036, driven by accelerating natural gas infrastructure expansion, growing petrochemical and industrial manufacturing capacity, and increasing government investment in clean energy and hydrogen infrastructure across the region.

1. Introduction

1.1 Market Definition and Scope

1.2 Market Ecosystem

1.3 Currency and Limitations

1.3.1 Currency

1.3.2 Limitations

1.4 Key Stakeholders

2. Research Methodology

2.1 Research Approach

2.2 Data Collection & Validation Process

2.2.1 Secondary Research

2.2.2 Primary Research & Validation

2.2.2.1 Primary Interviews with Experts

2.2.2.2 Country/Region-Level Analysis

2.3 Market Estimation

2.3.1 Bottom-Up Approach

2.3.2 Top-Down Approach

2.4 Data Triangulation

2.5 Assumptions for the Study

3. Executive Summary

3.1 Market Overview

3.2 Market Analysis by Type

3.3 Market Analysis by Stage

3.4 Market Analysis by Power Output

3.5 Market Analysis by End-Use Industry

3.6 Market Analysis by Geography

4. Market Dynamics

4.1 Overview

4.2 Drivers

4.2.1 Sustained Natural Gas Production Expansion and Midstream Infrastructure Investment Driving Reciprocating Compressor Demand

4.2.2 EPA NSPS OOOOb and Global Methane Emission Regulations Compelling Compliance-Driven Equipment Investment

4.2.3 Hydrogen Infrastructure Buildout Establishing a New High-Growth Application Segment for Oil-Free Reciprocating Compressors

4.2.4 Rapid Industrialization and Energy Infrastructure Expansion Across Asia Pacific Generating Structural Demand Growth

4.3 Restraints

4.3.1 Higher Lifecycle Maintenance Requirements and Total Cost of Ownership Relative to Rotary Compressor Alternatives

4.3.2 Availability of Technically Skilled Service Personnel Constraining Fleet Management Capabilities in Remote and Emerging Markets

4.4 Opportunities

4.4.1 Digital Monitoring and Predictive Maintenance Platforms Creating New Service Revenue Streams and Improving Equipment Economics

4.4.2 Growing Oil-Free Reciprocating Compressor Adoption in Pharmaceutical, Food Processing, and Hydrogen Compression Applications

4.4.3 Large-Scale Gas Storage and Pipeline Infrastructure Expansion in Asia Pacific and the Middle East Driving Capital Equipment Demand

4.5 Challenges

4.5.1 Increasing Competition from High-Speed Rotary and Screw Compressor Technologies in Moderate-Pressure Industrial Applications

4.5.2 Material Compatibility and Sealing Technology Requirements for Hydrogen and Sour Gas Service Complicating Equipment Specification

4.6 Porter's Five Forces Analysis

5. Reciprocating Compressors Market, by Type

5.1 Overview

5.2 Lubricated Reciprocating Compressors

5.2.1 Trunk Piston Lubricated Compressors

5.2.2 Crosshead Lubricated Compressors

5.3 Oil-Free Reciprocating Compressors

5.3.1 Non-Lubricated Piston Compressors

5.3.2 Diaphragm Compressors

6. Reciprocating Compressors Market, by Stage

6.1 Overview

6.2 Single-Stage Reciprocating Compressors

6.3 Multi-Stage Reciprocating Compressors

6.3.1 Two-Stage Reciprocating Compressors

6.3.2 Three-Stage and Above Reciprocating Compressors

7. Reciprocating Compressors Market, by Power Output

7.1 Overview

7.2 Up to 75 kW

7.3 76 kW to 375 kW

7.4 Above 375 kW

8. Reciprocating Compressors Market, by End-Use Industry

8.1 Overview

8.2 Oil & Gas

8.2.1 Upstream (Gas Gathering & Production)

8.2.2 Midstream (Pipeline Transmission & Gas Storage)

8.2.3 Downstream (Refining & Petrochemical Processing)

8.3 Chemical & Petrochemical

8.4 Industrial Gas

8.4.1 Hydrogen Compression

8.4.2 Oxygen & Nitrogen Compression

8.4.3 Other Industrial Gas Compression

8.5 Power Generation

8.6 Food & Beverage Processing

8.7 Pharmaceutical & Healthcare

8.8 Other End-Use Industries

9. Reciprocating Compressors Market, by Geography

9.1 Overview

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.3 Europe

9.3.1 Germany

9.3.2 U.K.

9.3.3 France

9.3.4 Italy

9.3.5 Netherlands

9.3.6 Norway

9.3.7 Rest of Europe

9.4 Asia Pacific

9.4.1 China

9.4.2 Japan

9.4.3 India

9.4.4 South Korea

9.4.5 Australia

9.4.6 Southeast Asia

9.4.7 Rest of Asia Pacific

9.5 Latin America

9.5.1 Brazil

9.5.2 Argentina

9.5.3 Rest of Latin America

9.6 Middle East and Africa

9.6.1 Saudi Arabia

9.6.2 UAE

9.6.3 Qatar

9.6.4 South Africa

9.6.5 Rest of Middle East and Africa

10. Competitive Landscape

10.1 Overview

10.2 Key Growth Strategies

10.3 Competitive Benchmarking

10.4 Competitive Dashboard

10.4.1 Industry Leaders

10.4.2 Market Differentiators

10.4.3 Vanguards

10.4.4 Emerging Companies

10.5 Market Share/Ranking Analysis (2025)

11. Company Profiles

11.1 Ariel Corporation

11.2 Siemens Energy AG

11.3 Burckhardt Compression AG

11.4 Atlas Copco AB

11.5 Ingersoll Rand Inc.

11.6 Chart Industries, Inc.

11.7 Exterran Corporation

11.8 Kobelco Compressors Corporation

11.9 Mitsubishi Heavy Industries Compressor Corporation

11.10 GEA Group AG

11.11 Sundyne Corporation

11.12 Neuman & Esser Group

11.13 Corken, Inc.

11.14 Hitachi Industrial Equipment Systems Co., Ltd.

11.15 Shenyang Yuanda Compressor Co., Ltd.

11.16 Others

12. Appendix

12.1 Questionnaire

12.2 Available Customization Options

12.3 Related Reports

Published Date: Jan-2026

Published Date: Jan-2026

Published Date: Jul-2025

Subscribe to get the latest industry updates