Resources

About Us

Diaphragm Pumps Market Size, Share & Trends Analysis, by Product Type (Air-Operated Double Diaphragm, Electrically Operated Diaphragm, Hydraulically Actuated Diaphragm), Construction Material, Diaphragm Material, End Use Industry, and Geography — Global Opportunity Analysis & Forecast (2026–2036)

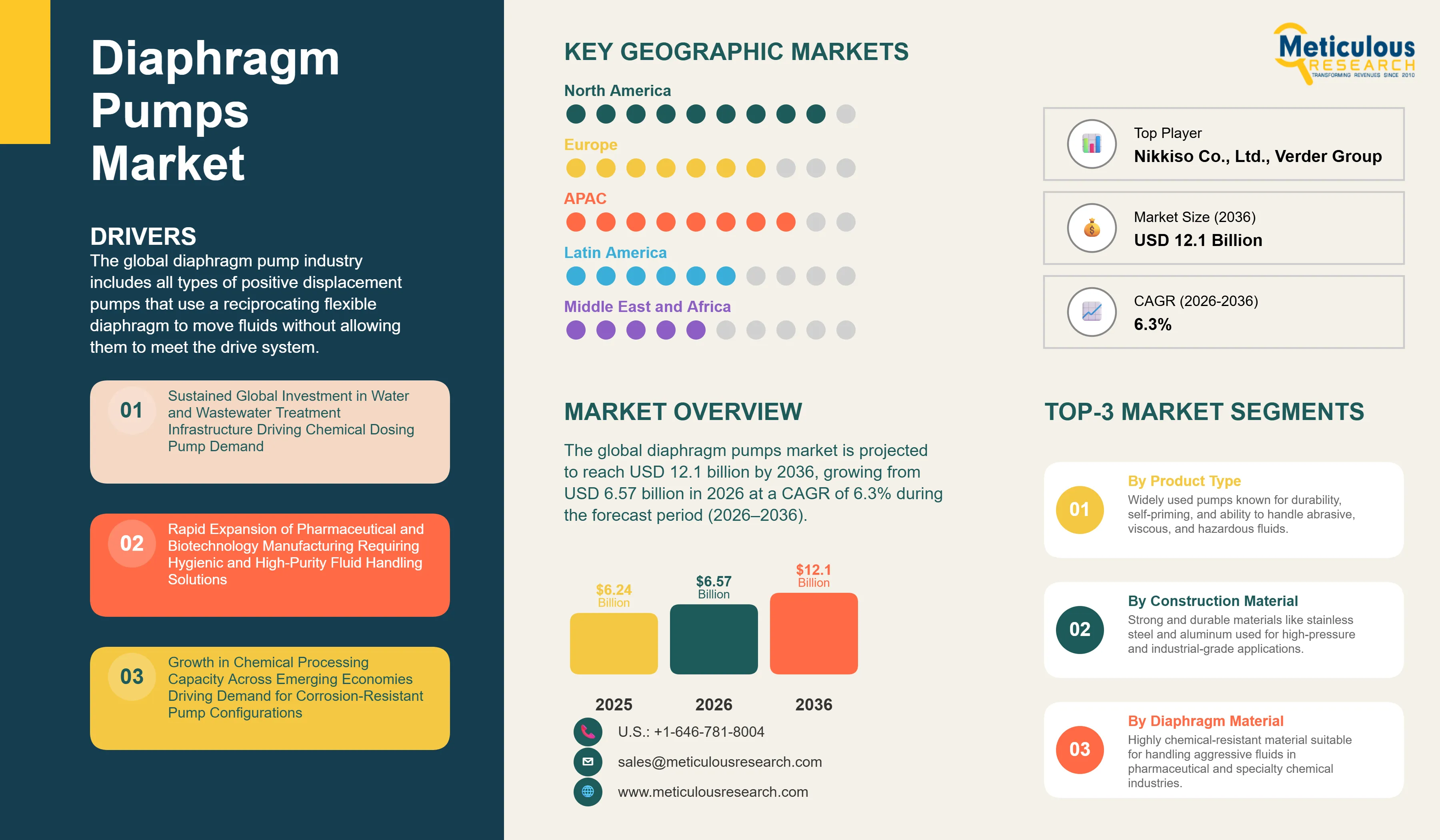

Report ID: MREP - 1041948 Pages: 284 Apr-2026 Formats*: PDF Category: Energy and Power Delivery: 24 to 72 Hours Download Free Sample ReportThe global diaphragm pumps market was valued at USD 6.24 billion in 2025. The market is projected to reach USD 12.1 billion by 2036, growing from USD 6.57 billion in 2026 at a CAGR of 6.3% during the forecast period (2026–2036).

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global diaphragm pump industry includes all types of positive displacement pumps that use a reciprocating flexible diaphragm to move fluids without allowing them to meet the drive system. This configuration makes diaphragm pumps especially well-suited for handling corrosive, abrasive, viscous, shear-sensitive, and hazardous liquids in challenging industrial, municipal, and sanitary environments. The market covers air-operated double diaphragm (AODD) pumps, electrically driven diaphragm pumps, hydraulically actuated variants, and motor-driven metering pumps. These systems are manufactured using both metallic and non-metallic materials, with diaphragms typically made from PTFE, rubber elastomers, or thermoplastics.

The growth of the diaphragm pumps industry is primarily driven by expanding demand from the water and wastewater treatment sector, where diaphragm pumps are widely specified for chemical dosing, sludge transfer, and filter press feeding applications. Simultaneously, rapid growth in pharmaceutical and biotechnology manufacturing is creating strong demand for pumps meeting stringent regulatory standards, including FDA 21 CFR and USP Class VI compliance requirements for hygienic fluid transfer. The global expansion of chemical processing facilities, particularly in Asia Pacific and the Middle East, alongside increasing investment in lithium and critical mineral mining operations to support electric vehicle battery supply chains, is further contributing to broad-based demand growth across end use segments.

The transition toward Industry 4.0 and smart manufacturing is reshaping product development priorities across the sector. Leading manufacturers are integrating digital monitoring capabilities, variable frequency drives, and remote diagnostics into pump platforms, enabling customers to reduce unplanned downtime, optimize energy consumption, and extend maintenance intervals. This shift is particularly accelerating adoption of electrically operated diaphragm pumps in process industries that prioritize precise flow control and seamless integration with distributed control systems (DCS) and supervisory control and data acquisition (SCADA) platforms.

Despite strong growth fundamentals, the market faces certain restraints. Diaphragm pumps generally have lower pressure tolerance compared to plunger and centrifugal pumps, which restricts their use in high-pressure applications. In addition, diaphragm wear and the need for regular replacement increase maintenance costs, an important factor in price-sensitive markets. Competition from alternative technologies, such as peristaltic and gear pumps for certain viscous fluid handling needs, also limits adoption in some industry segments.

Significant opportunities are emerging from the rising adoption of single-use and disposable diaphragm pump systems in bioprocessing and pharmaceutical manufacturing, where the elimination of cleaning validation requirements reduces total cost of ownership for drug manufacturers. The growth of decentralized water treatment and industrial fluid management in emerging economies is also opening new addressable markets, while increasingly stringent environmental regulations worldwide are reinforcing the preference for leak-free diaphragm pump designs over alternative technologies with higher fugitive emission profiles.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 12.1 Billion |

|

Market Size in 2026 |

USD 6.57 Billion |

|

Market Size in 2025 |

USD 6.24 Billion |

|

Revenue Growth Rate (2026–2036) |

CAGR of 6.3% |

|

Dominating Product Type |

Air-Operated Double Diaphragm (AODD) Pumps |

|

Fastest Growing Product Type |

Electrically Operated Diaphragm Pumps |

|

Dominating Construction Material |

Metallic |

|

Fastest Growing Construction Material |

Non-metallic |

|

Dominating Diaphragm Material |

Rubber/Elastomeric |

|

Fastest Growing Diaphragm Material |

PTFE |

|

Dominating End Use |

Water and Wastewater Treatment |

|

Fastest Growing End Use |

Pharmaceuticals and Biotechnology |

|

Dominating Geography |

North America |

|

Fastest Growing Geography |

Asia Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Electrification and Digital Integration Redefining Product Development Priorities Across the Diaphragm Pump Industry

The gradual transition from compressed air-driven to electrically operated diaphragm pump configurations is emerging as one of the most consequential shifts in the diaphragm pumps industry. Air-operated double diaphragm pumps have historically dominated the industry due to their inherent simplicity, self-priming capability, and ability to run dry without damage. However, the increasing adoption of electric motor-driven and solenoid-actuated diaphragm pumps is gaining momentum, driven by the high total cost of compressed air infrastructure, energy inefficiency of pneumatic systems, and the inability of pneumatically driven pumps to integrate natively with digital plant automation environments.

Electrically operated diaphragm pumps offer precise volumetric dosing, variable speed control through frequency inverters, and direct compatibility with process control systems, including DCS, SCADA, and IIoT monitoring platforms. Leading manufacturers including Graco Inc., ProMinent GmbH, and KNF Group have actively expanded their electrically operated pump portfolios with embedded diagnostic capabilities, enabling customers to implement predictive maintenance protocols that reduce unplanned shutdowns. The pharmaceutical, food and beverage, and specialty chemical sectors are particularly driving adoption of smart electric diaphragm pumps, where precise dosing accuracy, process traceability, and regulatory compliance requirements make digital control integration a procurement necessity rather than a convenience feature.

Pharmaceutical and Biotechnology Manufacturing Expansion Creating Sustained Demand for High-Purity Diaphragm Pump Configurations

The global expansion of biologics, biosimilars, and mRNA-based therapeutics manufacturing is generating substantial demand for diaphragm pumps which are designed to meet stringent hygienic and regulatory requirements. Drug manufacturers and contract development and manufacturing organizations (CDMOs) require diaphragm pumps for a wide range of applications including drug substance transfer, buffer and media preparation, chromatography feed, and clean-in-place (CIP) operations, where the leak-free, gentle fluid handling characteristics of diaphragm pumps offer distinct advantages over alternative pump technologies.

Diaphragm pumps made from stainless steel and PVDF that comply with FDA 21 CFR, USP Class VI, and 3-A Sanitary Standards are being increasingly adopted in both high-volume injectable production and oral solid dosage manufacturing. The rise of single-use bioprocessing is further expanding opportunities, as disposable diaphragm pump systems are gaining traction in biologics manufacturing by removing the need for cleaning validation and lowering the risk of cross-contamination in multi-product facilities. Companies such as Verder Group, LEWA GmbH (Nikkiso Group), and IDEX Corporation have broadened their hygienic and pharmaceutical-grade offerings to meet rising demand in this space, which is expected to be among the fastest-growing application areas for diaphragm pumps during the forecast period.

Critical Minerals Mining Expansion Generating New High-Volume Demand for Abrasion-Resistant and Chemically Robust AODD Pump Configurations

The global acceleration of lithium, cobalt, nickel, and copper mining capacity in response to electric vehicle battery supply chain requirements is generating significant demand for diaphragm pumps in mining and minerals processing applications. Air-operated double diaphragm pumps are widely used in mining operations for slurry transfer, tailings management, heap leach acid dosing, dewatering, and solvent extraction applications, where their ability to handle high solids content fluids, operate in remote locations with limited electrical infrastructure, and withstand dry running without damage makes them particularly well suited relative to alternative pump technologies.

The lithium brine extraction operations expanding rapidly in South America's Lithium Triangle and in Australia's hard rock lithium projects require pumps capable of handling highly corrosive brines and process reagents, driving demand for PVDF and polypropylene AODD pumps with PTFE diaphragms. Major pump manufacturers including Ingersoll Rand (ARO brand), IDEX Corporation (Wilden brand), and Yamada Corporation are actively developing pump configurations optimized for the abrasion-resistant and chemical resistance requirements of lithium and battery-grade mineral processing. This trend is expected to contribute meaningfully to diaphragm pump market growth through the forecast period as global critical mineral extraction capacity continues to expand in response to electrification-driven demand growth.

By Product Type: In 2026, the AODD Pumps Segment to Dominate the Global Diaphragm Pumps Market

Based on product type, the overall diaphragm pumps industry is segmented into air operated double diaphragm pumps, electrically operated diaphragm pumps, hydraulically actuated diaphragm pumps, and other diaphragm pump variants. In 2026, the air-operated double diaphragm pumps segment is expected to account for the largest share of the market. The leading position of this segment is driven by the adaptability of AODD pumps across a wide range of fluid types and industrial applications. They can operate safely in hazardous or explosive environments without requiring electrical connections, tolerate dry running and deadheading without damage, and typically have a lower upfront cost compared to electrically driven or hydraulically actuated alternatives. Their self-priming capability, portability, and well-established service and spare parts networks further reinforce their appeal. As a result, AODD pumps are often the default choice in industries such as chemical processing, paints and coatings, ceramics, and mining, where operating conditions can vary and maintenance resources may be constrained.

However, the electrically operated diaphragm pumps segment is projected to register the highest growth during the forecast period. The strong growth of this segment is driven by the rising demand for precise metering and dosing accuracy in pharmaceutical, water treatment chemical dosing, and food processing applications, growing adoption of energy-efficient pump systems as manufacturing facilities target reductions in compressed air infrastructure costs, and the increasing integration of pump platforms with digital plant management systems requiring electrical control interfaces. Manufacturers are continuously expanding electrically operated pump offerings with advanced flow monitoring, automatic stroke adjustment, and remote diagnostic capabilities that are accelerating penetration of this segment in process-intensive industries.

By Construction Material: In 2026, the Metallic Segment to Hold the Largest Share

Based on construction material, the diaphragm pumps industry is segmented into metallic pumps (aluminum, stainless steel, cast iron, and high-alloy variants) and non-metallic pumps (polypropylene, PVDF, acetal, and other engineered plastic materials). In 2026, the metallic segment is expected to account for the largest share of the total diaphragm pumps market. This growth is attributed to the growing use of aluminum-bodied AODD pumps in general industrial applications due to their combination of mechanical durability, reasonable chemical compatibility, and cost effectiveness, alongside the strong demand for stainless steel diaphragm pumps in hygienic industries where surface finish requirements, steam sterilization compatibility, and corrosion resistance specifications mandate metallic construction. The established installed base of metallic diaphragm pumps across chemical processing, oil and gas, food and beverage, and mining industries continues to drive significant replacement and aftermarket demand for metallic configurations.

However, the non-metallic segment is projected to register the highest groeth during the forecast period. The growth of this segment is driven by the rapid expansion of applications requiring resistance to aggressive acids, alkalis, and oxidizing chemicals that would corrode metallic pump housings, as well as growing demand from the semiconductor and pharmaceutical industries where metallic ion contamination from wetted surfaces is unacceptable. PVDF and polypropylene diaphragm pumps are increasingly specified in chemical dosing systems, semiconductor ultrapure water handling, and pharmaceutical fluid transfer where the combination of broad chemical resistance, low extractables, and compliance with purity standards makes non-metallic construction preferable to metallic alternatives.

By Diaphragm Material: In 2026, the Rubber and Elastomeric Segment to Account for the Largest Share

Based on diaphragm material, the diaphragm pumps industry is segmented into PTFE, rubber and elastomeric materials (including EPDM, neoprene, nitrile, and natural rubber), thermoplastic elastomers (including Santoprene and Hytrel), and other diaphragm materials. In 2026, the rubber and elastomeric diaphragm segment is expected to account for the largest share of the market. This dominant position reflects the cost-effectiveness, mechanical flexibility, and adequate chemical resistance of rubber diaphragms for a broad range of general industrial fluid handling applications, including water-based fluids, mild chemicals, and slurries encountered in water treatment, mining, construction, and manufacturing environments. EPDM diaphragms are particularly widely specified for water-based and alkaline fluid applications due to their good resistance to ozone, weathering, and polar fluids, while neoprene diaphragms serve a wide range of mineral oil and fuel handling applications.

However, the PTFE diaphragm segment is projected to register the highest growth during the forecast period. This high growth is driven by the expanding demand for diaphragm pumps in pharmaceutical, food and beverage, semiconductor, and specialty chemical applications where PTFE diaphragms provide the broadest chemical resistance to concentrated acids, oxidizing agents, and solvents, along with FDA compliance and near-zero extractables characteristics that are essential for high-purity fluid contact applications. The increasing specification of PTFE diaphragms in combination with non-metallic pump housings for corrosive chemical service is further reinforcing this segment's growth trajectory over the forecast period.

By End Use: In 2026, the Water and Wastewater Treatment Segment to Hold the Largest Share

Based on end use, the diaphragm pumps industry is segmented into water and wastewater treatment, chemical processing, pharmaceuticals and biotechnology, food and beverage, oil and gas, mining and minerals processing, paints, coatings, and inks, and other end uses. In 2026, the water and wastewater treatment segment is expected to account for the largest share of this market. This growth is driven by the extensive deployment of diaphragm pumps in chemical dosing applications including chlorination, pH adjustment, coagulation, and disinfection byproduct control across municipal water treatment plants, industrial effluent treatment systems, and desalination facilities worldwide. The sustained global investment in water infrastructure modernization, particularly in the United States under the Infrastructure Investment and Jobs Act, as well as large-scale water treatment capacity expansion programs across the Middle East and Asia Pacific, is maintaining strong volume demand for diaphragm metering pumps in this segment.

However, the pharmaceuticals and biotechnology segment is projected to register the highest growth during the forecast period. The strong growth of this segment is driven by the accelerating global expansion of biologics and biosimilars manufacturing capacity, the rapid scaling of mRNA vaccine production infrastructure established during and following the COVID-19 pandemic, and the growing adoption of continuous manufacturing approaches in pharmaceutical production that require precise, validated fluid transfer solutions. The preference for diaphragm pumps in aseptic processing, sterile fill-finish operations, and cell culture media preparation is reinforcing their position as the technology of choice for pharmaceutical fluid handling applications requiring strict adherence to regulatory compliance and cross-contamination prevention requirements.

Based on geography, the diaphragm pumps industry is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. In 2026, North America is expected to account for the largest share of this market. This leading position is attributed to the large installed base of diaphragm pumps across the United States chemical processing industry, concentrated along the Gulf Coast chemical corridor, the presence of major diaphragm pump manufacturers including Graco Inc., IDEX Corporation (operating the Wilden and Warren Rupp brands), and Ingersoll Rand (ARO Fluid Products), significant investment in water infrastructure modernization under federal funding programs, and strong demand from the pharmaceutical and biotechnology manufacturing industries concentrated in the northeastern United States and Puerto Rico. The oil and gas sector in the Permian Basin and other shale production regions continues to drive meaningful demand for AODD pumps in production fluid handling, chemical injection, and produced water management applications.

However, the Asia Pacific diaphragm pumps market is expected to grow at the fastest CAGR from 2026 to 2036. The rapid growth of this market is driven by the massive ongoing expansion of chemical manufacturing capacity across China, India, South Korea, and Southeast Asia; large-scale government investment in water supply and wastewater treatment infrastructure, including India's Jal Jeevan Mission and China's national water infrastructure programs; the emergence of India as a global pharmaceutical manufacturing hub with growing demand for hygienic and sterile pump solutions; and the accelerating expansion of lithium and critical mineral mining in Australia and Indonesia creating new demand for abrasion and chemical-resistant diaphragm pump configurations. Domestic pump manufacturers in China, including Shenyang Pump and INOXPA China operations, are intensifying competitive pressure on international manufacturers, while multinational players are simultaneously expanding their local manufacturing and service capabilities to serve rapidly growing regional demand.

The global diaphragm pumps industry is consolidated, featuring a combination of large, diversified industrial players with established pump brands and specialized manufacturers competing across product types, material construction, and application-specific niches. Competition is driven by factors such as compatibility of diaphragms and wetted materials with different fluid chemistries, the range of pump configurations available to meet varied application needs, the strength of global distribution and service networks, compliance with industry-specific regulatory standards, and the ability to provide application engineering expertise and integrated pump system solutions.

Large diversified industrial companies such as Graco Inc., IDEX Corporation, Ingersoll Rand plc (through its ARO Fluid Products brand), and Dover Corporation (through its Pump Solutions Group) compete through broad product portfolios covering multiple diaphragm pump configurations, global manufacturing operations, and well-established distributor networks with strong brand recognition across key end use industries. These players benefit from significant aftermarket revenue streams from diaphragm replacement parts and service consumables that provide recurring revenue alongside new equipment sales.

European and Japanese specialty pump manufacturers including LEWA GmbH and IWAKI Co., Ltd. (both part of Nikkiso Co., Ltd.), KNF Group, ProMinent GmbH, Verder Group, and Tapflo Group compete through application expertise, high-precision metering capabilities, and strong positions in the pharmaceutical, chemical, and water treatment segments. The market is also influenced by the growing adoption of smart and connected pump platforms, which is driving investment in digital product development capabilities across both large and specialist manufacturers.

The report provides a comprehensive competitive analysis based on an assessment of key players' product portfolios, geographic presence, regulatory certifications, and strategic initiatives undertaken over the past few years.

Some of the key players operating in the global diaphragm pumps industry include Graco Inc. (U.S.), IDEX Corporation (U.S.), Ingersoll Rand plc (U.S.), Dover Corporation (U.S.), Yamada Corporation (Japan), Nikkiso Co., Ltd. (Japan), KNF Group (Germany), ProMinent GmbH (Germany), Verder Group (Netherlands), Tapflo Group (Sweden), Flowserve Corporation (U.S.), FLUX-GERÄTE GmbH (Germany), Lutz-JESCO GmbH (Germany), Grundfos Holding A/S (Denmark), and PSG, a Dover Company (U.S.), among others.

The global diaphragm pumps market is expected to reach USD 12.1 billion by 2036 from an estimated USD 6.57 billion in 2026, at a CAGR of 6.3% during the forecast period 2026–2036.

In 2026, the air-operated double diaphragm (AODD) pumps segment is expected to hold the largest share of this market, driven by the broad application compatibility, operational simplicity, and cost effectiveness of AODD pump configurations across general industrial end use segments.

The electrically operated diaphragm pumps segment is expected to register the highest CAGR during the forecast period 2026–2036, driven by the accelerating adoption of smart pump technologies integrating with industrial automation and IIoT platforms, alongside growing demand for precise metering and dosing accuracy in pharmaceutical and chemical processing applications.

In 2026, the metallic segment is expected to hold the largest share of this market, reflecting the widespread deployment of aluminum-bodied and stainless steel diaphragm pumps across general industrial, chemical processing, and hygienic manufacturing applications.

In 2026, the rubber and elastomeric segment is expected to hold the largest share of this market, reflecting the widespread specification of EPDM, neoprene, and nitrile diaphragms across high-volume industrial fluid handling applications in water treatment, mining, and general manufacturing.

In 2026, the water and wastewater treatment segment is expected to hold the largest share of the overall diaphragm pumps market, supported by sustained global investment in water treatment infrastructure and the widespread use of diaphragm metering pumps in chemical dosing applications at municipal and industrial water treatment facilities.

The growth of this market is primarily driven by expanding investment in water and wastewater treatment infrastructure globally, rapid growth in pharmaceutical and biotechnology manufacturing requiring hygienic fluid handling solutions, broad demand from the chemical processing industry for corrosion and abrasion-resistant pumping solutions, and the accelerating expansion of critical mineral mining operations supporting global electric vehicle battery supply chains.

Key players in the global diaphragm pumps market include Graco Inc. (U.S.), IDEX Corporation (U.S.), Ingersoll Rand plc (U.S.), Dover Corporation (U.S.), Yamada Corporation (Japan), Nikkiso Co., Ltd. (Japan), KNF Group (Germany), ProMinent GmbH (Germany), Verder Group (Netherlands), Tapflo Group (Sweden), Flowserve Corporation (U.S.), FLUX-GERÄTE GmbH (Germany), Lutz-JESCO GmbH (Germany), Grundfos Holding A/S

(Denmark), and PSG, a Dover Company (U.S.).

Asia Pacific is expected to register the highest growth rate in the global diaphragm pumps industry during the forecast period 2026–2036, driven by the rapid expansion of chemical manufacturing, pharmaceutical production, water treatment infrastructure investment, and critical mineral mining activities across China, India, Australia, and Southeast Asia.

Published Date: Oct-2025

Published Date: Sep-2025

Published Date: Jul-2025

Published Date: Jan-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates