Resources

About Us

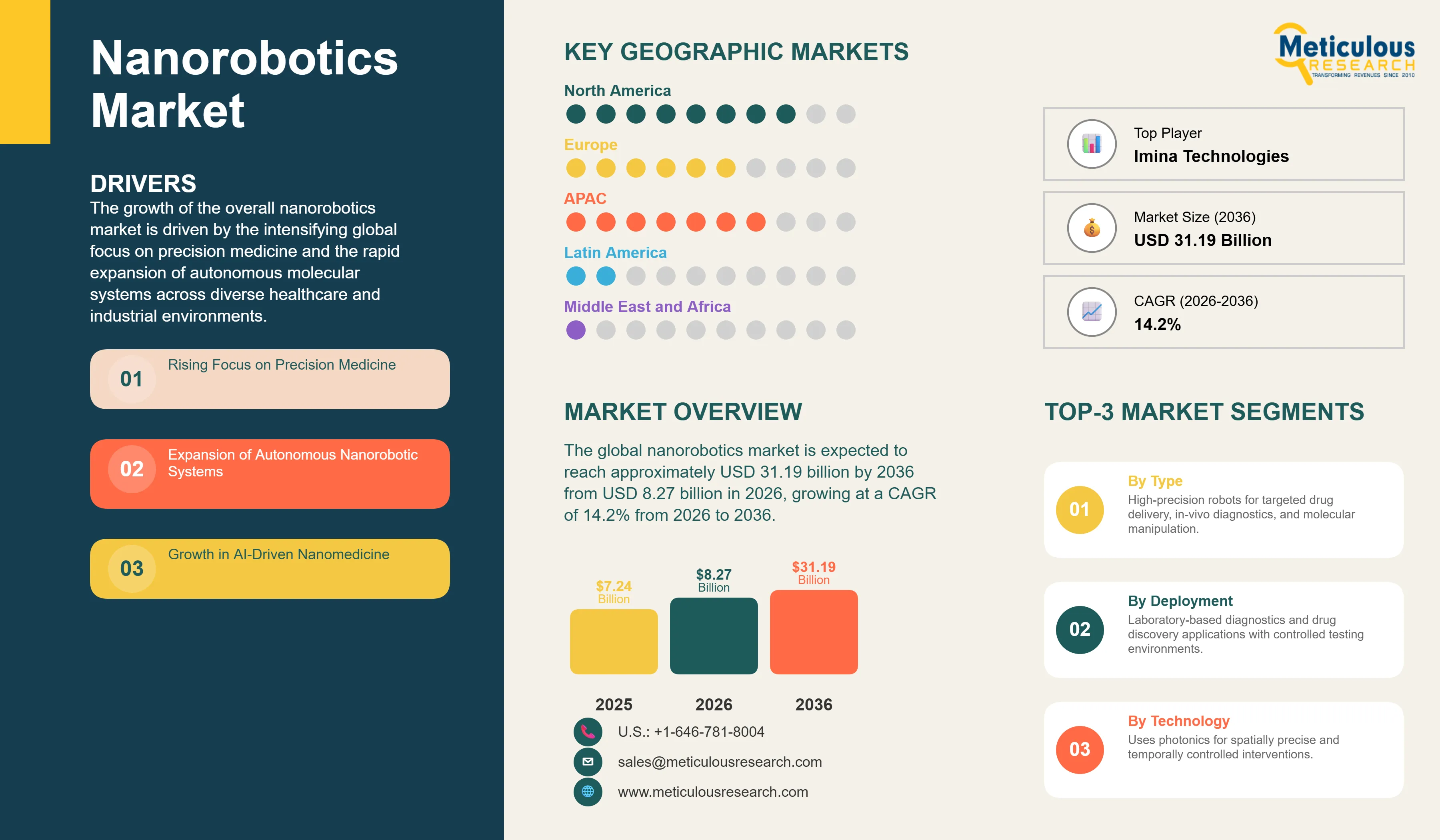

The global nanorobotics market was valued at USD 7.24 billion in 2025. The market is expected to reach approximately USD 31.19 billion by 2036 from USD 8.27 billion in 2026, growing at a CAGR of 14.2% from 2026 to 2036. The growth of the overall nanorobotics market is driven by the intensifying global focus on precision medicine and the rapid expansion of autonomous molecular systems across diverse healthcare and industrial environments. As enterprises seek to integrate more intelligence into their therapeutic and manufacturing frameworks and address the increasing demand for real-time cellular-level intervention and diagnostics, advanced nanorobotic platforms have become essential for maintaining structural integrity and instructional performance. The rapid expansion of AI-driven nanomedicine and the increasing need for high-performance molecular assembly and diagnostics continue to fuel significant growth of this market across all major geographic regions.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

Nanorobotics systems represent critical microscopic frameworks used to provide automated molecular and cellular manipulation while allowing for real-time progress tracking and intervention. These systems include nano-manipulators for research, bio-nanorobots for medical applications, and magnetically guided robots for targeted therapy, which are designed to operate in complex biological environments. The market is defined by high-precision modules such as AI-driven drug delivery systems and computer vision-based diagnostic tools, which significantly enhance therapeutic agility and mechanical durability in complex medical applications. These systems are indispensable for clinicians and researchers seeking to optimize their treatment protocols and achieve breakthrough medical outcomes.

The market includes a diverse range of solutions, ranging from simple diagnostic tools for basic cellular analysis to complex multilayer systems for high-performance drug delivery and professional research services. These systems are increasingly integrated with advanced components such as biocompatible materials and AI-powered navigation to provide services such as targeted cancer therapy and improved diagnostic accuracy. The ability to provide stable, high-precision results while minimizing side effects has made advanced nanorobotics technology the choice for industries where patient outcomes and scalability are paramount.

The global healthcare sector is pushing hard to modernize treatment capabilities, aiming to meet AI-driven automation and hyper-connected healthcare targets. This drive has increased the adoption of high-density nanorobotic platforms, with advanced data analytics techniques helping to stabilize treatment outcomes for ultra-fine biological architectures. At the same time, the rapid growth in the personalized medicine and professional diagnostics markets is increasing the need for high-reliability, clinically-proven therapeutic solutions.

Manufacturers across the nanorobotics industry are rapidly shifting to data-optimized architectures, moving well beyond traditional passive nanoparticles toward high-speed, low-latency autonomous systems. Imina Technologies’ latest nano-manipulators deliver significantly higher precision for semiconductor research, while SmarAct’s recent updates have slashed operational complexity in laboratory trials. The real game-changer comes with “smart” nanorobots featuring integrated AI capabilities that maintain peak performance even in volatile biological environments. These advancements make high-precision cellular intervention practical and cost-effective for everyone from academic researchers to global pharmaceutical conglomerates chasing therapeutic excellence and lower system complexity.

Innovation in bio-hybrid nanorobots is rapidly driving the nanorobotics market, as these devices become more interactive and multi-functional. Suppliers are now designing units that combine the structural integrity of synthetic nanomaterials with the versatility of living cells in a single assembly, saving valuable development time and simplifying clinical translation. These systems often involve advanced biocompatible materials and time-release drug technology capable of handling ultra-fine interactive flows without compromising system security or clinical reliability.

At the same time, growing focus on personalized medicine is pushing manufacturers to develop solutions tailored to individual patient needs. These systems help reduce side effects through targeted drug delivery and the use of adaptive biological substrates. By combining high-density data delivery with robust therapeutic performance, these new designs support both technological advancement and patient-centric care, strengthening the resilience of the broader healthcare value chain.

|

Parameter |

Details |

|

Market Size by 2036 |

USD 31.19 Billion |

|

Market Size in 2026 |

USD 8.27 Billion |

|

Market Size in 2025 |

USD 7.24 Billion |

|

Market Growth Rate (2026-2036) |

CAGR of 14.2% |

|

Dominating Region |

North America |

|

Fastest Growing Region |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

|

Segments Covered |

Type, Deployment, Technology, Application, End-User, and Region |

|

Regions Covered |

North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa |

A key driver of the nanorobotics market is the rapid movement of the global healthcare industry toward data-backed, highly functional digital infrastructure. Global demand for seamless remote diagnostics, effective therapeutic support, and patient-monitoring systems has created significant incentives for the adoption of nanorobotics products. The trend toward “autonomous” therapies and the integration of AI into daily clinical practice drive organizations toward scalable solutions that nanorobotics technology can uniquely provide. It is estimated that as healthcare adoption of automated routines rises and diagnostic tools become more decentralized through 2036, the need for robust, effective management platforms increases significantly; therefore, software modules and cloud-based delivery, with their ability to ensure high-density data delivery, are considered a crucial enabler of modern medical design strategies.

The rapid growth of the personalized medicine market and green manufacturing technologies provides great opportunities for the nanorobotics market. Indeed, the global surge in demand for targeted therapies for cancer and other chronic diseases has created a compelling demand for systems that can replace traditional systemic treatments and integrate seamlessly into digital healthcare models. These applications require high reliability, data transparency, and the ability to handle high-volume patient environments, all attributes that are met with advanced nanorobotic solutions. The ESG market is set to expand significantly through 2036, with nanorobotics products poised for an expanding share as manufacturers seek to maximize resource loyalty and minimize environmental waste. Furthermore, the increasing demand for AI-driven diagnostics and virtual clinical trials is stimulating demand for modular software solutions that provide high-speed results and design flexibility.

The nanorobotic systems segment accounts for a significant portion of the overall nanorobotics market in 2026. This is mainly attributed to the versatile use of this technology in supporting real-time diagnostics and complex therapeutic interventions within extremely diverse environments, such as in the bloodstream and within individual cells. These systems offer the most comprehensive way to ensure therapeutic integrity across diverse high-frequency applications. The healthcare and research sectors alone consume a large share of nanorobotic systems production, with major projects in North America and Europe demonstrating the technology’s capability to handle high-density data requirements. However, the software & control systems segment is expected to grow at a rapid CAGR during the forecast period, driven by the growing need for robust implementation in smart hospitals, clinical procedures, and advanced research systems.

Based on application, the healthcare segment holds the largest share of the overall market in 2026. This is primarily due to the massive volume of targeted drug delivery projects and the rigorous performance standards required for modern medical networks. Current large-scale clinical trials are increasingly specifying high-density management platforms to ensure compliance with global performance standards and clinician expectations for faster, visible results.

The molecular manufacturing segment is expected to witness steady growth during the forecast period. The shift toward secure asset data management and the complexity of specialized research suites are pushing the requirement for advanced active systems that can handle varied data types and mechanical stresses while ensuring absolute reliability for safety-critical medical systems.

The in-vivo deployment segment commands a significant share of the global nanorobotics market in 2026. This dominance stems from its superior therapeutic efficacy, direct patient benefit, and transformative potential in treating complex diseases. Large-scale clinical applications in targeted cancer therapy, cardiovascular interventions, and neurological treatments drive demand, with advanced platforms from suppliers like Thermo Fisher Scientific and Imina Technologies enabling reliable performance in complex biological environments.

The in-vitro and ex-vivo deployment segments are poised for steady growth through 2036, fueled by expanding applications in drug discovery, diagnostics, and research applications. Manufacturers face mounting pressure to optimize costs for high-volume laboratory and research applications, where standardized nanorobotic modules provide a cost-effective alternative for basic research and diagnostic connectivity.

Magnetic actuation technology holds the largest share of the global nanorobotics market in 2026, driven by its proven efficacy in precise navigation and control within biological systems. This technology enables real-time steering and positioning, making it the preferred choice for targeted drug delivery and minimally invasive surgical applications. Leading manufacturers continue to refine magnetic field generation systems to achieve unprecedented precision and safety standards.

Biohybrid and biological propulsion technologies are experiencing the fastest growth during the forecast period, driven by their natural integration with biological systems and reduced toxicity profiles. These innovative approaches combine living cells or biological motors with synthetic nanomaterials, offering superior biocompatibility and therapeutic potential. Acoustic and ultrasound propulsion technologies are emerging as complementary solutions, particularly for applications requiring non-invasive activation and control.

Optical and light-driven actuation represents a rapidly growing segment, enabled by advances in photonics and biocompatible materials. This technology offers unique advantages in terms of spatial precision and temporal control, making it increasingly attractive for complex surgical and diagnostic applications. The convergence of multiple propulsion technologies is creating hybrid systems that leverage the strengths of each approach, further expanding market opportunities.

The hospitals & clinical centers segment commands the largest share of the global nanorobotics market in 2026. This dominance stems from its superior patient management capacity, data consistency, and excellent clinical properties, making it the technology of choice for high-performance medical systems. Large-scale operations in oncology, cardiology, and high-end diagnostics drive demand, with advanced platforms from suppliers like Thermo Fisher Scientific and ZEISS Group enabling reliable performance in extreme environments.

However, the pharmaceutical & biotechnology companies segment is poised for steady growth through 2036, fueled by expanding applications in commercial drug discovery and simple delivery formulations. Manufacturers face mounting pressure to optimize costs for high-volume, less demanding applications, where standardized nanorobotic modules provide a cost-effective alternative for basic research connectivity.

North America holds the largest share of the global nanorobotics market in 2026. The largest share of this region is primarily attributed to the massive investments in healthcare innovation and the presence of the world’s largest research hubs, particularly in the United States and Canada. The US alone accounts for a significant portion of global nanorobotics production, with its position as a leading exporter of high-end medical technology driving sustained growth. The presence of leading manufacturers like Thermo Fisher Scientific and Bruker Corporation and a well-developed healthcare supply chain provides a robust market for both standard and high-density nanorobotic solutions.

Asia-Pacific and Europe together account for a substantial share of the global nanorobotics market. The growth of these markets is mainly driven by the need for technological modernization in the professional, luxury, and commercial medical sectors. The demand for advanced nanorobotic systems in Asia-Pacific is mainly due to its large-scale government funding and the presence of innovators like JEOL Ltd. and Hitachi High-Tech Corporation.

In Europe, the leadership in medical engineering and the push for safety innovation are driving the adoption of high-reliability medical products. Countries like Germany, the UK, and Switzerland are at the forefront, with significant focus on integrating smart nanorobotic solutions into daily routines and advanced medical treatments to ensure the highest levels of performance and reliability.

The companies such as JEOL Ltd. (Japan), Thermo Fisher Scientific Inc. (US), Bruker Corporation (Germany), and Hitachi High-Tech Corporation (Japan) lead the global nanorobotics market with a comprehensive range of manipulation and imaging solutions, particularly for large-scale research and high-speed industrial applications. Meanwhile, players including ZEISS Group (Germany), Oxford Instruments (UK), and Imina Technologies (Switzerland) focus on specialized mass-market and high-density formulations targeting the professional and commercial sectors. Emerging manufacturers and integrated players such as SmarAct GmbH (Germany), Stereotaxis, Inc. (US), and Ginkgo Bioworks (US) are strengthening the market through innovations in medical technology and modular software platforms.

The global nanorobotics market is expected to grow from USD 8.27 billion in 2026 to USD 31.19 billion by 2036.

The global nanorobotics market is projected to grow at a CAGR of 14.2% from 2026 to 2036.

Nanorobotic systems are expected to dominate the market in 2026 due to their superior ability to support real-time diagnostics and adaptive therapies. However, software & control systems are projected to be the fastest-growing segment owing to their increasing adoption in smart hospitals, professional services, and advanced research where high active delivery is required.

Autonomous Systems and AI-driven Navigation are transforming the nanorobotics landscape by demanding higher data integrity, lower latency, and improved therapeutic repair. These technologies drive the adoption of advanced materials like biocompatible platforms and AI-compliant modules, enabling nanorobotics manufacturers to support the complex formulations and high-frequency requirements of next-generation medical products.

North America holds the largest share of the global nanorobotics market in 2026. The largest share of this region is primarily attributed to the massive investments in healthcare innovation and the presence of the world’s largest research hubs in the United States and Canada. Asia-Pacific and Europe together account for a substantial share, driven by high-end applications in professional and luxury medical.

The leading companies include JEOL Ltd. (Japan), Thermo Fisher Scientific Inc. (US), Bruker Corporation (Germany), Hitachi High-Tech Corporation (Japan), and ZEISS Group (Germany).

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Research Methodology

1.4. Assumptions & Limitations

2. Executive Summary

3. Market Overview

3.1. Introduction

3.2. Market Dynamics

3.2.1. Drivers

3.2.2. Restraints

3.2.3. Opportunities

3.2.4. Challenges

3.3. Market Trends

4. Global Nanorobotics Market, by Type

4.1. Introduction

4.2. Nano-manipulators

4.2.1. Atomic Force Microscopes (AFM)

4.2.2. Scanning Tunneling Microscopes (STM)

4.2.3. Others

4.3. Nanorobotic Systems

4.3.1. Bio-nanorobots

4.3.2. Magnetically Guided Nanorobots

4.3.3. Electromechanical Nanobots

4.3.4. Others

4.4. Software & Control Systems

5. Global Nanorobotics Market, by Deployment

5.1. Introduction

5.2. In-vivo Deployment

5.2.1. Targeted Drug Delivery

5.2.2. Surgical Interventions

5.2.3. Diagnostic Imaging

5.2.4. Tissue Engineering & Repair

5.2.5. Other In-vivo Applications

5.3. In-vitro/Ex-vivo Deployment

5.3.1. Laboratory Research

5.3.2. Drug Discovery

5.3.3. Diagnostics & Testing

5.3.4. Other In-vitro Applications

6. Global Nanorobotics Market, by Technology

6.1. Introduction

6.2. Magnetic Actuation

6.2.1. Electromagnetic Field Systems

6.2.2. Permanent Magnet Systems

6.2.3. Hybrid Magnetic Systems

6.3. Biohybrid/Biological Propulsion

6.3.1. Cell-based Propulsion

6.3.2. Biological Motor Systems

6.3.3. Hybrid Bio-synthetic Systems

6.4. Acoustic/Ultrasound Propulsion

6.4.1. Ultrasonic Actuation

6.4.2. Acoustic Streaming

6.4.3. Resonance-based Systems

6.5. Optical/Light-driven Actuation

6.5.1. Photonic Propulsion

6.5.2. Optogenetic Control

6.5.3. Plasmonic Systems

6.6. Other Technologies

7. Global Nanorobotics Market, by Application

7.1. Introduction

7.2. Healthcare

7.2.1. Drug Delivery

7.2.2. Diagnostics & Imaging

7.2.3. Nanosurgery & Tissue Repair

7.2.4. Dental Applications

7.2.5. Other Healthcare Applications

7.3. Molecular Manufacturing

7.4. Research & Development

7.5. Environmental Monitoring

7.6. Industrial & Electronics

8. Global Nanorobotics Market, by End-User

8.1. Introduction

8.2. Hospitals & Clinical Centers

8.3. Pharmaceutical & Biotechnology Companies

8.4. Academic & Research Institutes

8.5. Medical Device OEMs

8.6. Industrial Manufacturers

8.7. Other End-Users

9. Global Nanorobotics Market, by Geography

9.1. Introduction

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Switzerland

9.3.7. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. South Korea

9.4.5. Australia & New Zealand

9.4.6. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Argentina

9.5.4. Chile

9.5.5. Colombia

9.5.6. Rest of Latin America

9.6. Middle East & Africa

9.6.1. GCC Countries

9.6.1.1. Saudi Arabia

9.6.1.2. UAE

9.6.1.3. Qatar

9.6.1.4. Rest of GCC

9.6.2. South Africa

9.6.3. Israel

9.6.4. Egypt

9.6.5. Nigeria

9.6.6. Rest of Middle East & Africa

10. Competitive Landscape

10.1. Introduction

10.2. Key Player Strategies

10.3. Competitive Dashboard

10.3.1. Industry Leader

10.3.2. Market Differentiators

10.3.3. Vanguards

10.3.4. Emerging Companies

10.4. Market Share Analysis, By Key Player

11. Company Profiles

11.1. JEOL Ltd. (Japan)

11.2. Thermo Fisher Scientific Inc. (US)

11.3. Bruker Corporation (Germany)

11.4. Hitachi High-Tech Corporation (Japan)

11.5. ZEISS Group (Germany)

11.6. Oxford Instruments (UK)

11.7. Imina Technologies (Switzerland)

11.8. SmarAct GmbH (Germany)

11.9. Stereotaxis, Inc. (US)

11.10. Ginkgo Bioworks (US)

11.11. EV Group (Austria)

12. Appendix

12.1. Questionnaire

12.2. Available Customization

Published Date: Jul-2026

Published Date: Jul-2026

Published Date: Jul-2026

Published Date: Jul-2026

Published Date: Jul-2026

Subscribe to get the latest industry updates