Resources

About Us

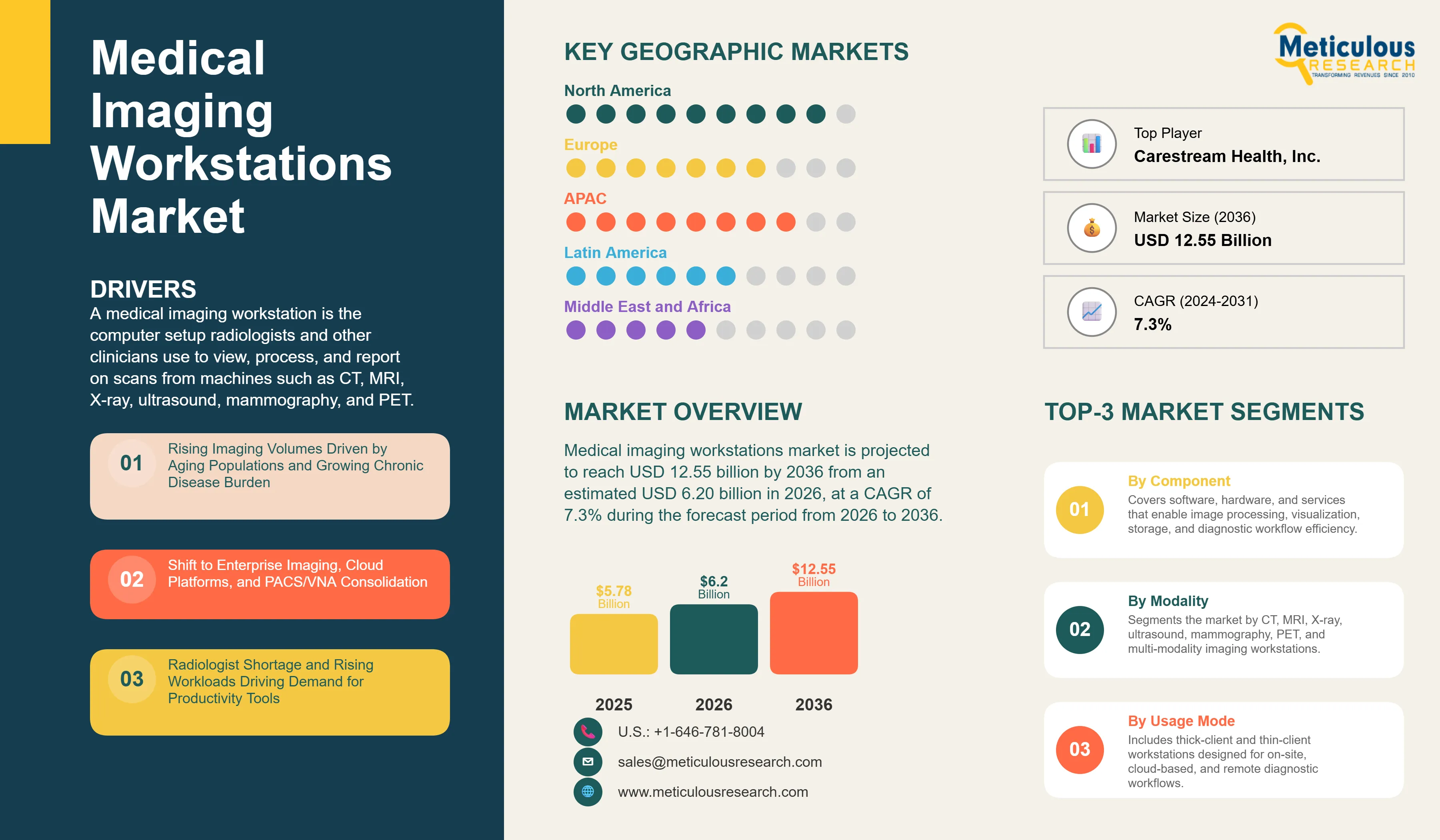

The global medical imaging workstations market is projected to reach USD 12.55 billion by 2036 from an estimated USD 6.20 billion in 2026, at a CAGR of 7.3% during the forecast period from 2026 to 2036.

Click here to: Get Free Sample Pages

Click here to: Get Free Sample Pages

A medical imaging workstation is the computer setup radiologists and other clinicians use to view, process, and report on scans from machines such as CT, MRI, X-ray, ultrasound, mammography, and PET. It brings together diagnostic display monitors, processing hardware, and visualization software, and it connects to the hospital's picture archiving and communication system (PACS) so that images and reports flow through one place. In practice, the workstation is where a scan becomes a diagnosis, which makes it a core part of any imaging department.

Demand for these workstations follows the demand for imaging itself, and that demand keeps climbing. Populations are getting older, and conditions that call for imaging, above all cancer and heart disease, are becoming more common. The World Health Organization projects that new cancer cases could rise by around 47% between 2020 and 2040, which points to years of growing scan volumes and, with them, a steady need for reading workstations. Oncology and cardiac studies in particular lean on detailed post-processing, so they tend to drive sales of higher-end systems.

How hospitals buy and run these systems is also changing. Many are consolidating separate departmental systems onto a single enterprise imaging platform, and a growing number are moving that platform to the cloud. This shift lets radiologists read from home or across several sites, which has become important as remote work spreads in radiology. It also moves much of the value from the physical box to the software, so visualization software and cloud services now account for a large part of what buyers pay for.

The last big factor is the people using the systems. Radiologists are in short supply in many countries, and caseloads keep rising, so anything that helps a specialist get through more studies without sacrificing accuracy is in demand. This has made workflow speed, easy access to prior studies, and built-in analysis tools central to purchasing decisions. Taken together, rising scan volumes, the move to cloud and enterprise platforms, and pressure on radiologist time set the medical imaging workstations market up for steady growth over the coming decade.

Medical Imaging Workstations Market: Expert Perspectives from Industry Leaders

"Healthcare organizations are moving toward enterprise-wide imaging strategies. Rather than purchasing standalone workstations for individual departments, they are investing in scalable platforms that support collaboration across radiology, cardiology, oncology, and other specialties."

– Vice President, Imaging Informatics Solutions Provider

"Cloud-enabled workstations are becoming an important consideration, particularly for health systems operating across multiple sites. The ability to securely access imaging data from anywhere is now viewed as a strategic advantage rather than an optional feature."

– Healthcare IT Director, Regional Diagnostic Network

"The conversation has shifted from simply improving image quality to improving diagnostic efficiency. Healthcare providers are increasingly looking for workstations that help radiologists prioritize cases, reduce interpretation time, and integrate AI seamlessly into daily workflows."

– Director of Radiology, Multi-Hospital Health System

Rising Imaging Volumes from Aging Populations and Chronic Disease

The key driver of the market is the sheer growth in the number of scans being performed. As people live longer, they need more imaging to detect and monitor age-related conditions, and the rising rates of cancer, heart disease, and other chronic illnesses add to that load. Every one of these studies has to be read on a workstation, so more scans mean more demand for reading systems.

The scale of the trend is significant. The World Health Organization projects that cancer cases could increase by roughly 47% between 2020 and 2040, and cancer follow-up alone generates a large and repeating volume of CT, MRI, and PET studies. Cardiac imaging is on a similar path as heart disease remains a leading cause of death worldwide. Because oncology and cardiac cases rely on careful measurement, comparison with prior scans, and three-dimensional review, they push hospitals toward capable, higher-end workstations rather than basic viewers.

This growth in volume runs across almost every care setting, from large teaching hospitals to community diagnostic centers. As long as populations keep aging and chronic disease keeps rising, the number of studies to be read will keep growing, which gives the workstation market a dependable base of demand.

Move to Enterprise Imaging, Cloud, and PACS/VNA Consolidation

A second strong driver is the way hospitals are reorganizing their imaging systems. For years, radiology, cardiology, and other departments often ran separate archives and viewers. Now health systems are pulling these together into a single enterprise imaging platform built on a shared PACS and vendor-neutral archive, which simplifies access and cuts duplicated infrastructure.

Much of this consolidation is happening in the cloud. Vendors such as Fujifilm, GE HealthCare, Agfa HealthCare, and Sectra have moved their platforms toward cloud-first designs, and hospitals are following because cloud delivery reduces on-site hardware, eases software updates, and lets radiologists read from any location. Agfa HealthCare, for example, signed an agreement in early 2026 to run a multi-state radiology group's reading across 11 sites on a single cloud teleradiology platform. Each of these migrations involves refreshing or replacing the workstations that sit on top of the platform.

Because buyers increasingly want workstations that plug neatly into an enterprise, cloud-ready environment, this shift is steering spending toward software licenses, subscriptions, and services rather than one-off hardware purchases. That change broadens the market and creates recurring revenue for vendors, which supports long-term growth.

Radiologist Shortage and Rising Workloads

A third driver is the gap between how much imaging needs to be read and how many radiologists are available to read it. In many countries, the supply of radiologists is not keeping pace with rising study volumes, and administrative tasks take up a large share of the working day. This leaves each specialist under real pressure to get through more cases.

Workstations are one of the main ways providers respond. Faster worklists, automatic pairing of current and prior studies, quick access to three-dimensional tools, and viewers that let a radiologist cover several hospitals from one screen all help a scarce specialist do more without added risk. Vendors have leaned into this, positioning their systems as a way to stretch existing staff rather than as a luxury. GE HealthCare's Genesis Radiology Workspace, for instance, is built to let radiologists provide subspecialty reads across multiple sites without traveling between them.

As long as the radiologist shortage persists and caseloads keep climbing, hospitals will keep investing in tools that lift reading productivity. This makes workforce pressure a lasting source of demand and a key reason workstation features now focus so heavily on speed and workflow.

Growth of Cloud-Based Workstations and Emerging Markets

A major opportunity lies in cloud-based, thin-client workstations, which open the market to buyers that older systems left out. Instead of installing a powerful computer at each desk, a thin-client setup streams images from a central server, so a facility can add reading capacity without heavy local hardware or a large IT team. This lowers the cost of entry and fits the way radiology is moving toward remote and distributed reading.

Emerging markets stand to gain the most from this shift. Hospitals across Asia-Pacific, Latin America, and parts of the Middle East and Africa are expanding fast, and many are building imaging capacity from scratch. Rather than install legacy systems, a number of these facilities are going straight to cloud-native platforms, which lets them reach specialist readers who may sit in another city or country. Teleradiology has already shown its value here, cutting patient waiting times where local radiologists are scarce.

Outpatient and diagnostic imaging centers offer a parallel opening. These sites want to keep costs low and avoid running their own data centers, which makes subscription-based, cloud-hosted workstations a good fit. Fujifilm's Synapse One, aimed squarely at outpatient imaging centers, is one example of vendors building for this group. Between emerging markets and outpatient growth, cloud-based delivery gives the workstation market a clear path to expand well beyond its traditional hospital base.

By Component: Software Segment Leads the Medical Imaging Workstations Market in 2026

By component, the market is segmented into software, hardware, and services. The software segment is expected to account for the largest share of the market in 2026, representing approximately 57% of the total market. Software has become the core value driver of modern medical imaging workstations, enabling advanced visualization, image post-processing, AI-assisted image analysis, multi-planar and three-dimensional reconstruction, quantitative measurements, and comparison with prior examinations across multiple imaging modalities. In addition, the growing adoption of subscription-based licensing models, regular software upgrades, and AI-enabled diagnostic applications continues to increase software spending among healthcare providers.

The hardware segment is projected to register the fastest growth during the forecast period. Increasing demand for high-performance workstation processing units equipped with advanced CPUs and GPUs, coupled with the widespread adoption of high-resolution medical-grade displays, including 4K and emerging 8K monitors, is supporting market growth. These hardware advancements improve image rendering speed, visualization quality, and diagnostic accuracy, particularly for complex imaging applications such as oncology, cardiology, and advanced radiology, prompting healthcare providers to modernize their workstation infrastructure.

By Modality: Computed Tomography Leads the Market in 2026

By modality, the market includes CT, MRI, X-ray and radiography, ultrasound, mammography, PET and nuclear medicine, and multi-modality workstations. Computed tomography holds the largest share in 2026, at close to 29%. CT studies are high in volume and demand a lot of post-processing, including vascular analysis, oncology follow-up, and detailed reconstruction, so they rely on capable workstations more than most other modalities.

PET and nuclear medicine workstations are projected to grow the fastest. Rising use of molecular imaging in cancer diagnosis and treatment planning, along with the spread of theranostics, is increasing demand for the specialized processing these studies require.

By Usage Mode: Thick-client Workstations Lead the Market in 2026

By usage mode, the market splits into thick-client workstations and thin-client or web-streaming workstations. Thick-client systems hold the larger share in 2026, at about 41%. They keep processing power and storage on the local machine, which suits heavy tasks such as three-dimensional reconstruction and large multi-modality datasets, and they remain the choice of many academic hospitals and busy reading rooms that need consistent performance.

Thin-client and cloud-based workstations are set to grow the fastest. As hospitals move to enterprise and cloud platforms and as remote reading becomes routine, web-streaming systems that need little local hardware are gaining ground quickly, and many new facilities now start with them by default.

By Application: Diagnostic Imaging Leads the Market in 2026

By application, the market covers diagnostic imaging, clinical review, and advanced visualization. Diagnostic imaging holds the largest share in 2026, at roughly 48%. Reading studies to reach a diagnosis and produce a report is the everyday, core job of the workstation, so it accounts for the bulk of use across radiology departments and imaging centers.

Advanced visualization, covering three-dimensional and four-dimensional imaging, is expected to grow the fastest. As more scans call for detailed multi-planar and volume rendering, particularly in oncology, cardiology, and surgical planning, demand for these tools is rising quickly, and vendors are building them directly into the reading workflow.

By Clinical Specialty: General Radiology Leads the Market in 2026

By clinical specialty, the market spans general radiology, cardiology, oncology, orthopedics, obstetrics and gynecology, mammography, neurology, and other areas. General radiology holds the largest share in 2026, at about 32%. It covers the broadest mix of everyday studies across CT, MRI, X-ray, and ultrasound, which gives it the widest base of workstation use.

Mammography is projected to grow the fastest. Wider breast-screening programs and the shift to digital breast tomosynthesis, which produces large image sets that need dedicated reading tools, are lifting demand for mammography workstations across many markets.

By End User: Hospitals Lead the Market in 2026

By end user, the market is split among hospitals, diagnostic imaging centers, ambulatory care centers, and academic and research institutes. Hospitals hold the largest share in 2026, at close to 43%. They handle high patient volumes and complex cases across many specialties, run the most imaging equipment, and have the budgets to invest in multi-modality workstations tied into their PACS and electronic records.

Diagnostic imaging centers are expected to grow the fastest. As imaging shifts toward outpatient settings and these centers take on more scan volume, their appetite for efficient, often cloud-based workstations is rising, making them the quickest-growing group of buyers.

North America Leads the Market in 2026

By region, the global medical imaging workstations market is split across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America holds the largest share in 2026, at roughly 37%.

North America's lead rests on early adoption of new imaging technology, well-defined reimbursement for advanced procedures, and a deep base of leading vendors, including GE HealthCare, Philips, and Hologic. The United States is the dominant national market, helped by widespread PACS use, a large installed base of scanners, and steady investment in enterprise imaging and AI-assisted reading tools that hospitals can recoup through reimbursed procedures.

Asia-Pacific is expected to record the fastest growth over the forecast period. Ongoing hospital construction, government programs that expand access to diagnostic imaging, and rapidly aging populations across China, India, and Japan are driving demand, and many new facilities are adopting cloud-based systems from the start. Europe remains an important market, supported by national screening programs in countries such as Germany and France and by cross-border image-sharing efforts that encourage interoperable viewers.

Leading companies in the market have grown through new product launches, cloud platform rollouts, partnerships, and acquisitions. Adding advanced visualization and AI-assisted features, moving to cloud-first delivery, and winning enterprise imaging contracts have been the most common ways players strengthen their position.

Prominent companies active in the global medical imaging workstations market include GE HealthCare Technologies Inc. (U.S.), Koninklijke Philips N.V. (Netherlands), Siemens Healthineers AG (Germany), Canon Medical Systems Corporation (Japan), FUJIFILM Holdings Corporation (Japan), Agfa-Gevaert N.V. (Belgium), Carestream Health, Inc. (U.S.), Sectra AB (Sweden), Hologic, Inc. (U.S.), Intelerad Medical Systems Incorporated (Canada), Pro Medicus Limited (Visage Imaging) (Australia), Merative L.P. (U.S.), Esaote S.p.A. (Italy), Barco NV (Belgium), and Novarad Corporation (U.S.).

|

Particulars |

Details |

|

Forecast Period |

2026 to 2036 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

CAGR (Value) |

7.3% |

|

Market Size (Value) in 2026 |

USD 6.20 Billion |

|

Market Size (Value) in 2036 |

USD 12.55 Billion |

|

Segments Covered |

By Component - Visualization Software - Display Units - Other Hardware (Controller Cards & Processors) - Services By Modality - CT, MRI, X-ray & Radiography, Ultrasound, Mammography, PET & Nuclear Medicine, Multi-modality By Usage Mode - Thick-client Workstations - Thin-client/Web-streaming (Cloud-based) Workstations By Application - Diagnostic Imaging - Clinical Review - Advanced Visualization (3D/4D Imaging) By Clinical Specialty - General Radiology, Cardiology, Oncology, Orthopedics, Obstetrics & Gynecology, Mammography, Neurology, Others By End User - Hospitals - Diagnostic Imaging Centers - Ambulatory Care Centers - Academic & Research Institutes |

|

Countries Covered |

North America (U.S., Canada), Europe (Germany, U.K., France, Italy, Spain, and Rest of Europe), Asia-Pacific (Japan, China, India, South Korea, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and the Middle East & Africa (Saudi Arabia, UAE, South Africa, and Rest of Middle East & Africa) |

|

Key Companies |

GE HealthCare Technologies Inc. (U.S.), Koninklijke Philips N.V. (Netherlands), Siemens Healthineers AG (Germany), Canon Medical Systems Corporation (Japan), FUJIFILM Holdings Corporation (Japan), Agfa-Gevaert N.V. (Belgium), Carestream Health, Inc. (U.S.), Sectra AB (Sweden), Hologic, Inc. (U.S.), Intelerad Medical Systems Incorporated (Canada), Pro Medicus Limited (Australia), Merative L.P. (U.S.), Esaote S.p.A. (Italy), Barco NV (Belgium), and Novarad Corporation (U.S.). |

The global medical imaging workstations market size is estimated at USD 6.20 billion in 2026.

The market is projected to grow from USD 6.20 billion in 2026 to USD 12.55 billion by 2036, at a CAGR of 7.3%.

The medical imaging workstations market is projected to reach USD 12.55 billion by 2036, at a compound annual growth rate (CAGR) of 7.3% from 2026 to 2036.

Key players in the medical imaging workstations market include GE HealthCare Technologies Inc. (U.S.), Koninklijke Philips N.V. (Netherlands), Siemens Healthineers AG (Germany), Canon Medical Systems Corporation (Japan), FUJIFILM Holdings Corporation (Japan), Sectra AB (Sweden), Pro Medicus Limited (Australia), Carestream Health, Inc. (U.S.), and others.

The move toward cloud-native and subscription-based workstation delivery, and the integration of AI-assisted tools into radiology reading workflows, are prominent trends in the market.

In 2026, visualization software leads by component, CT leads by modality, thick-client workstations lead by usage mode, diagnostic imaging leads by application, general radiology leads by clinical specialty, hospitals lead by end user, and North America leads by region. Display units, PET and nuclear medicine, cloud-based workstations, and mammography are among the fastest-growing segments.

North America holds the largest share of the market in 2026, supported by early technology adoption and strong reimbursement. Asia-Pacific is expected to record the highest growth rate over the forecast period, driven by hospital build-outs and rising scan volumes.

Key drivers include rising imaging volumes from aging populations and chronic disease, the move to enterprise imaging and cloud platforms, and a shortage of radiologists that lifts demand for productivity-enhancing workstations. Together, these are supporting steady adoption across care settings.

1. Introduction

1.1. Market Definition

1.2. Currency & Limitations

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.2. Bottom-Up Approach

2.3.3. Top-Down Approach

2.3.4. Growth Forecast

2.4. Assumptions for the Study

3. Executive Summary

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Rising Imaging Volumes Driven by Aging Populations and Growing Chronic Disease Burden

4.2.1.2. Shift to Enterprise Imaging, Cloud Platforms, and PACS/VNA Consolidation

4.2.1.3. Radiologist Shortage and Rising Workloads Driving Demand for Productivity Tools

4.2.2. Restraints

4.2.2.1. High Cost of Advanced Workstations Limiting Adoption in Budget-Constrained Settings

4.2.3. Opportunities

4.2.3.1. Growth of Cloud-Based and Thin-Client Workstations Widening Access

4.2.3.2. Expanding Opportunities Across Emerging Markets and Outpatient Imaging Centers

4.2.4. Challenges

4.2.4.1. Interoperability and Integration with Legacy Systems Expected to Remain a Major Challenge

4.3. Key Trends

4.3.1. Move Toward Cloud-Native and Subscription-Based Workstation Delivery

4.3.2. Integration of AI-Assisted Tools into Radiology Reading Workflows

4.4. Vendor Selection Criteria/Factors Influencing Purchase Decisions

4.5. Use Cases

4.6. Porter's Five Forces Analysis

4.6.1. Bargaining Power of Buyers: Moderate to High

4.6.2. Bargaining Power of Suppliers: Moderate

4.6.3. Threat of Substitutes: Low to Moderate

4.6.4. Threat of New Entrants: Moderate

4.6.5. Degree of Competition: High

4.7. Value Chain Analysis

4.8. Pricing Analysis

4.9. Technology Analysis

4.10. PESTEL Analysis

5. Medical Imaging Workstations Market Assessment—By Component

5.1. Overview

5.2. Software

5.2.1. Visualization & Post-processing Software

5.2.2. Image Analysis & AI-enabled Software

5.3. Hardware

5.3.1. Workstation Processing Units

5.3.2. Medical-grade Displays & Monitors

5.4. Services

5.4.1. Installation & Integration Services

5.4.2. Maintenance & Support Services

6. Medical Imaging Workstations Market Assessment—By Modality

6.1. Overview

6.2. Computed Tomography (CT)

6.3. Magnetic Resonance Imaging (MRI)

6.4. X-ray & Digital Radiography

6.5. Ultrasound

6.6. Mammography

6.7. PET & Nuclear Medicine

6.8. Multi-modality

7. Medical Imaging Workstations Market Assessment—By Usage Mode

7.1. Overview

7.2. Thick-client Workstations

7.3. Thin-client/Web-based Workstations

8. Medical Imaging Workstations Market Assessment—By Application

8.1. Overview

8.2. Primary Diagnosis

8.3. Clinical Review & Reporting

8.4. Advanced Visualization & 3D/4D Post-processing

8.5. Surgical Planning & Image-guided Procedures

9. Medical Imaging Workstations Market Assessment—By Clinical Specialty

9.1. Overview

9.2. General Radiology

9.3. Cardiology

9.4. Oncology

9.5. Orthopedics

9.6. Obstetrics & Gynecology

9.7. Breast Imaging

9.8. Neurology

9.9. Other Clinical Specialties

10. Medical Imaging Workstations Market Assessment—By End User

10.1. Overview

10.2. Hospitals

10.3. Diagnostic Imaging Centers

10.4. Ambulatory Care Centers

10.5. Academic & Research Institutes

11. Medical Imaging Workstations Market Assessment—By Geography

11.1. Overview

11.2. North America

11.2.1. United States

11.2.2. Canada

11.3. Europe

11.3.1. Germany

11.3.2. United Kingdom

11.3.3. France

11.3.4. Italy

11.3.5. Spain

11.3.6. Rest of Europe

11.4. Asia Pacific

11.4.1. Japan

11.4.2. China

11.4.3. India

11.4.4. South Korea

11.4.5. Australia & New Zealand

11.4.6. Rest of Asia Pacific

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Rest of Latin America

11.6. Middle East & Africa

11.6.1. Saudi Arabia

11.6.2. United Arab Emirates

11.6.3. South Africa

11.6.4. Rest of Middle East & Africa

12. Competitive Landscape

12.1. Introduction

12.2. Key Growth Strategies

12.3. Competitive Benchmarking

12.4. Competitive Dashboard

12.4.1. Industry Leaders

12.4.2. Market Differentiators

12.4.3. Vanguards

12.4.4. Emerging Companies

12.5. Market Share/Position Analysis

13. Company Profiles (Company Overview, Financial Overview, Product Portfolio, Strategic Developments)

13.1. GE HealthCare Technologies Inc. (U.S.)

13.2. Koninklijke Philips N.V. (Netherlands)

13.3. Siemens Healthineers AG (Germany)

13.4. Canon Medical Systems Corporation (Japan)

13.5. FUJIFILM Holdings Corporation (Japan)

13.6. Agfa-Gevaert N.V. (Belgium)

13.7. Carestream Health, Inc. (U.S.)

13.8. Sectra AB (Sweden)

13.9. Hologic, Inc. (U.S.)

13.10. Intelerad Medical Systems Incorporated (Canada)

13.11. Pro Medicus Limited (Visage Imaging) (Australia)

13.12. Merative L.P. (U.S.)

13.13. Esaote S.p.A. (Italy)

13.14. Barco NV (Belgium)

13.15. Novarad Corporation (U.S.)

14. Appendix

14.1. Available Customization

14.2. Related Reports

Published Date: Jun-2026

Published Date: Jan-2025

Published Date: May-2024

Subscribe to get the latest industry updates