Resources

About Us

Vessel Sealing Devices Market Size, Share, Trends & Forecast Analysis by Product (Instruments, Generators, Accessories), Energy Type (Bipolar & Advanced Bipolar, Ultrasonic, Hybrid), Usability, Surgery Type (Laparoscopic, Robotic-Assisted, Open), Application, End User, and Geography — Global Forecast to 2036

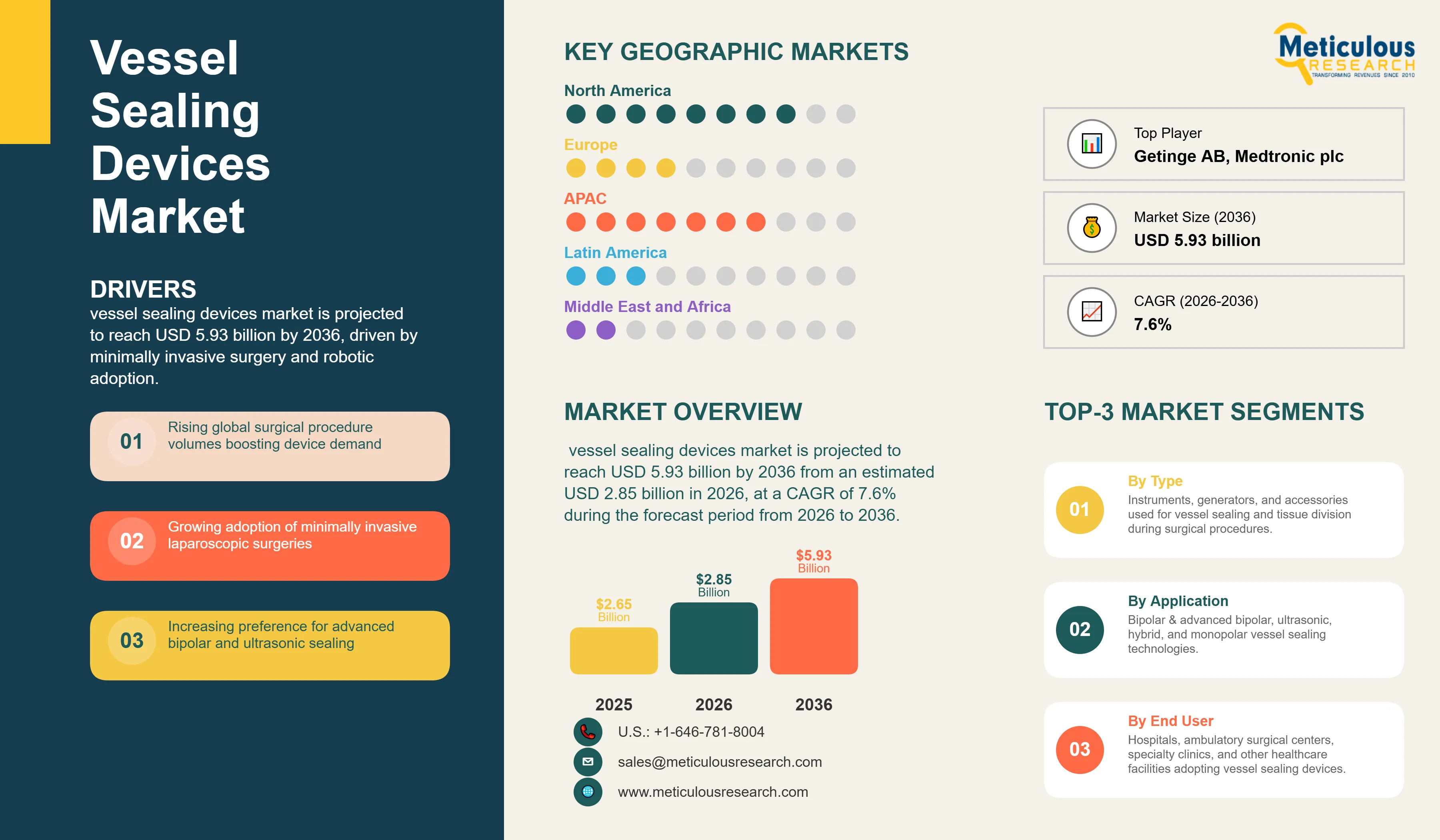

Report ID: MRHC - 1042096 Pages: 251 Jul-2026 Formats*: PDF Category: Healthcare Delivery: 24 to 72 Hours Download Free Sample ReportThe global vessel sealing devices market is projected to reach USD 5.93 billion by 2036 from an estimated USD 2.85 billion in 2026, at a CAGR of 7.6% during the forecast period from 2026 to 2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report Vessel sealing devices are energy-based surgical instruments used to seal and divide blood vessels, tissue bundles, and lymphatics during surgery, replacing conventional sutures, clips, and ties. Using advanced bipolar (radiofrequency) or ultrasonic energy, or a hybrid combination of both, these devices apply controlled heat and pressure to fuse the vessel walls, achieving rapid, reliable hemostasis with reduced blood loss and shorter operative time. A typical vessel sealing system comprises a reusable electrosurgical or ultrasonic generator (capital equipment) and single-use or reusable instruments such as sealer/dividers, dissectors, and shears, together with related accessories. The vessel sealing devices market spans advanced bipolar, ultrasonic, and hybrid energy platforms deployed across laparoscopic, robotic-assisted, and open surgical procedures.

According to Johnson & Johnson MedTech, more than 330 million surgical procedures are performed worldwide each year, while the Lancet Commission on Global Surgery estimates approximately 313 million major operations annually — a large and expanding base of procedures in which controlled hemostasis is essential. As populations age and the burden of cancer, obesity, and chronic disease grows, surgical volumes continue to rise, directly expanding demand for vessel sealing devices.

The most important structural driver is the shift toward minimally invasive surgery (MIS). Energy-based vessel sealing is integral to laparoscopic and robotic procedures, where precise, cable-connected sealing replaces manual suturing in confined operative fields. Peer-reviewed U.S. data show minimally invasive approaches rising sharply between 2003 and 2018; for example, laparoscopic appendectomy increased from 38% to 93% and colectomy from 8% to 43% of cases, steadily enlarging the addressable base for advanced sealing instruments. Robotic-assisted surgery has reinforced this trend, creating synergistic demand for compatible, articulating vessel sealing tools and forming a high-growth, premium segment of the market.

Clinical and economic value further support the adoption. Advanced bipolar and ultrasonic devices seal vessels up to 7 mm in diameter, reduce lateral thermal spread, shorten transection time, and lower reliance on multiple single-function instruments — improving operating-room efficiency and patient outcomes. With continued innovation in multifunctional and hybrid energy platforms, expanding robotic integration, and growing surgical demand across emerging markets, the vessel sealing devices market is positioned for steady growth, driven by the clinical imperative for safe, efficient hemostasis.

Rising Volume of Surgical Procedures and Growing Adoption of Minimally Invasive Surgery

The expanding global volume of surgery, coupled with the accelerating shift to minimally invasive surgery, is the foremost driver of the vessel sealing devices market. Vessel sealing devices are used across a broad range of procedures to control bleeding and divide tissue, so demand scales directly with surgical activity. With more than 330 million surgical procedures performed worldwide each year according to Johnson & Johnson MedTech, the underlying demand base is both large and growing.

Minimally invasive surgery amplifies this demand. In laparoscopic and robotic procedures, surgeons operate through small incisions where conventional suturing and clip application are difficult, making energy-based vessel sealing the preferred method for rapid, reliable hemostasis. Peer-reviewed U.S. data demonstrate the scale of the MIS transition, with laparoscopic representation rising across procedures such as appendectomy (38% to 93%) and colectomy (8% to 43%) between 2003 and 2018.

As aging populations and the rising burden of cancer, obesity, and chronic disease drive higher surgical volumes, and as MIS continues to displace open surgery across specialties, the addressable market for vessel sealing devices continues to expand. This combination of growing procedure counts and increasing MIS penetration underpins the sustained growth of the vessel sealing devices market.

Increasing Preference for Advanced Energy-Based Vessel Sealing Over Conventional Hemostasis

A clear clinical shift from conventional hemostasis — sutures, clips, and ties — toward advanced energy-based vessel sealing is a powerful growth driver. Advanced bipolar and ultrasonic devices deliver faster, more consistent sealing with reduced blood loss, shorter operative time, and fewer instrument exchanges, translating into measurable operating-room efficiency and improved patient outcomes.

These devices reliably seal vessels up to 7 mm in diameter and combine multiple functions — sealing, dividing, grasping, and dissecting — in a single instrument, reducing procedural complexity. Leading platforms such as Medtronic's LigaSure advanced bipolar system, Ethicon's Harmonic ultrasonic devices, and Olympus's POWERSEAL and THUNDERBEAT lines have established these technologies as standards of care across general, gynecologic, colorectal, bariatric, urologic, and thoracic surgery.

As surgeons increasingly train on and adopt these energy modalities, brand familiarity and demonstrated clinical benefits drive repeat purchasing and displacement of conventional techniques. This ongoing preference for advanced, efficient, multifunctional vessel sealing directly expands the market and shifts revenue toward higher-value energy-based devices and their recurring disposable instruments.

Expanding Adoption of Robotic-Assisted Surgery Boosting Demand for Compatible Instruments

The rapid expansion of robotic-assisted surgery is a significant driver of the vessel sealing devices market, creating synergistic demand for compatible, articulating sealing instruments. As robotic platforms scale across urology, gynecology, general surgery, and thoracic care, manufacturers are integrating vessel sealing directly into the robotic ecosystem.

This integration is now a strategic focus for the largest players. Intuitive Surgical offers robotic vessel sealing instruments for its da Vinci platform, while Medtronic has advanced a LigaSure vessel sealer for its Hugo robotic-assisted surgery system. Robotic-compatible sealing instruments command premium pricing and generate recurring per-procedure revenue, forming a high-growth segment within the broader market.

Because each robotic procedure typically consumes dedicated single-use sealing instruments, the expanding installed base of surgical robots translates into durable, recurring demand for vessel sealing devices. As robotic surgery adoption accelerates globally, robotic-compatible vessel sealing represents one of the market's most attractive and fastest-growing opportunities.

Growth Potential Across Ambulatory Surgical Centers and Emerging Markets

The expansion of vessel sealing device adoption into ambulatory surgical centers (ASCs) and emerging markets represents one of the most significant growth opportunities, broadening demand beyond large tertiary hospitals. As a growing share of surgical volume migrates to lower-cost outpatient settings, ASCs are increasingly investing in energy-based sealing systems to perform efficient, same-day minimally invasive procedures.

Ambulatory surgical centers are already the fastest-growing end-user setting for vessel sealing devices, driven by the shift of general, gynecologic, and urologic procedures to outpatient care and by the operating-room efficiency these devices provide. Manufacturers are responding with compact generators and streamlined single-use instruments suited to ASC workflows and economics.

Emerging markets offer a parallel opportunity. Rising surgical demand across Asia-Pacific, Latin America, and the Middle East & Africa — supported by expanding hospital infrastructure and government healthcare investment — is opening large, underserved populations to advanced vessel sealing technology. To address affordability, manufacturers are introducing cost-efficient and reusable device options and building regional distribution and surgeon-training programs, positioning ASC expansion and emerging-market penetration as durable engines of vessel sealing devices market growth.

By Product: The Instruments Segment Dominates the Vessel Sealing Devices Market in 2026

Based on product, the vessel sealing devices market is segmented into instruments, generators, and accessories. In 2026, the instruments segment accounts for the largest share of 61.5% of the global vessel sealing devices market. The large share of this segment is primarily attributed to the high-volume, recurring nature of single-use and limited-use instruments — sealer/dividers, dissectors, and shears — which are consumed on a per-procedure basis and scale directly with surgical activity.

Because instruments represent the recurring-revenue core of the vessel sealing business, and because leading manufacturers continually launch new instrument designs, the segment maintains its dominant position across surgical specialties.

However, the generators segment is projected to record a strong CAGR during the forecast period, driven by installed-base expansion in ambulatory surgical centers and emerging markets and by demand for advanced, multi-modality energy platforms. Modern generators that support both bipolar and ultrasonic instruments are prompting equipment refresh cycles that reinforce generator demand.

By Energy Type: The Bipolar & Advanced Bipolar Segment Dominates the Market in 2026

Based on energy type, the market is segmented into bipolar & advanced bipolar, ultrasonic, hybrid, and monopolar vessel sealing devices. In 2026, the bipolar & advanced bipolar segment accounts for the largest share of 45.2% of the global vessel sealing devices market. Advanced bipolar devices dominate owing to their reliable sealing of vessels up to 7 mm, reduced thermal spread, and broad adoption across general, gynecologic, colorectal, and thoracic procedures, anchored by established platforms such as LigaSure, ENSEAL, and POWERSEAL.

Their combination of seal reliability, versatility, and strong clinical evidence has made advanced bipolar the workhorse energy modality for vessel sealing across surgical specialties.

However, the ultrasonic segment is projected to record the highest CAGR during the forecast period. Ultrasonic devices offer low smoke generation, minimal lateral thermal damage, precise transection, and simultaneous cutting and coagulation, attributes that are driving rising adoption, particularly in delicate dissection and specialties where thermal precision is critical.

By Usability: The Single-use/Disposable Segment Dominates the Market in 2026

Based on usability, the market is segmented into single-use/disposable and reusable vessel sealing devices. In 2026, the single-use/disposable segment accounts for the largest share of 58.4% of the global vessel sealing devices market. Disposable instruments dominate due to infection-control requirements, consistent per-procedure performance, and the elimination of reprocessing, making them the default choice for high-volume surgical settings.

The recurring, per-procedure nature of disposable sealer/dividers also aligns with manufacturers' consumable-driven business models, reinforcing the segment's leading share.

However, the reusable segment is projected to grow at a notable CAGR during the forecast period, driven by cost-efficiency priorities in high-volume centers and price-sensitive emerging markets. Reusable vessel sealing systems can substantially lower per-procedure cost over their service life, making them increasingly attractive as health systems seek to control surgical expenditure and improve sustainability.

By Surgery Type: The Laparoscopic Surgery Segment Dominates the Market in 2026

Based on surgery type, the market is segmented into laparoscopic surgery, robotic-assisted surgery, and open surgery. In 2026, the laparoscopic surgery segment accounts for the largest share of 54.6% of the global vessel sealing devices market. Laparoscopy dominates because energy-based vessel sealing is essential to minimally invasive procedures, where sealing and dividing tissue through small incisions replaces conventional suturing, and because laparoscopic techniques are now standard across many high-volume specialties.

The clinical benefits of laparoscopy — reduced blood loss, smaller incisions, faster recovery, and lower complication risk — continue to drive its dominance and sustain demand for compatible vessel sealing instruments.

However, the robotic-assisted surgery segment is projected to grow fastest during the forecast period. The rapid expansion of surgical robots and the integration of dedicated, articulating vessel sealing instruments into robotic platforms are creating a premium, high-growth segment, with recurring instrument demand tied to the growing installed base of robotic systems.

By Application: The General Surgery Segment Dominates the Market in 2026

Based on application, the market is segmented into general surgery, gynecological surgery, urological surgery, cardiovascular & thoracic surgery, orthopedic surgery, bariatric surgery, oncology surgery, and other applications. In 2026, the general surgery segment accounted for the largest share of 33.4% of the global vessel sealing devices market. General surgery encompasses the highest volume of procedures — including cholecystectomy, colectomy, appendectomy, and hernia repair — in which vessel sealing is routinely used, giving it the broadest base of device utilization.

The high procedure volume, established laparoscopic and robotic adoption, and broad applicability of vessel sealing across general procedures sustain this segment's leading position.

However, the bariatric surgery segment is projected to record the fastest growth during the forecast period, driven by the rising global prevalence of obesity and the corresponding increase in bariatric procedures. As metabolic and bariatric surgery volumes expand, demand for advanced vessel sealing devices used in these energy-intensive procedures is expected to grow rapidly.

By End User: The Hospitals Segment Dominates the Vessel Sealing Devices Market in 2026

Based on end user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and others. In 2026, the hospitals segment accounts for the largest share of 59.8% of the global vessel sealing devices market. Hospitals dominate because they perform the majority of complex and high-volume surgical procedures, hold the largest installed base of energy generators and robotic systems, and have the resources to invest in advanced surgical energy platforms.

Their central role in complex surgery, together with established procurement and clinical infrastructure, reinforces the hospitals segment's dominant share.

However, the ambulatory surgical centers (ASC) segment is projected to grow fastest during the forecast period. The ongoing migration of surgical volume to lower-cost outpatient settings, combined with the operating-room efficiency that vessel sealing devices provide, is rapidly expanding ASC adoption and making it the highest-growth end-user setting.

North America Dominates the Global Vessel Sealing Devices Market in 2026

Based on geography, the global vessel sealing devices market is segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. In 2025, North America accounted for the largest share of 38.2% of the global vessel sealing devices market.

The large share of North America is attributed to high surgical volumes, advanced healthcare infrastructure, early and widespread adoption of minimally invasive and robotic surgery, and the concentration of leading manufacturers, including Medtronic, Johnson & Johnson (Ethicon), Intuitive Surgical, CONMED, and Applied Medical. The United States represents the dominant national market, supported by strong reimbursement and rapid uptake of advanced surgical energy technologies.

However, the Asia-Pacific is expected to register the fastest CAGR during the forecast period. Expanding surgical capacity, rising healthcare investment, and growing adoption of minimally invasive and robotic surgery across China, India, and Japan are driving demand for vessel sealing devices. Europe remains a significant market, led by Germany, the United Kingdom, and France, supported by well-established healthcare systems and the presence of leading energy-device manufacturers such as B. Braun, Erbe, and KLS Martin.

Major companies in the global vessel sealing devices market have pursued strategies including product launches & enhancements, partnerships & collaborations, acquisitions, and geographic expansion to strengthen their market positions. Product launches and enhancements have accounted for the majority of strategic activity, as leading manufacturers expand their advanced bipolar, ultrasonic, and robotic-compatible portfolios.

Some of the prominent players operating in the global vessel sealing devices market include Medtronic plc (Ireland), Johnson & Johnson (Ethicon) (U.S.), Olympus Corporation (Japan), B. Braun SE (Aesculap AG) (Germany), CONMED Corporation (U.S.), Erbe Elektromedizin GmbH (Germany), Intuitive Surgical, Inc. (U.S.), Hologic, Inc. (Bolder Surgical, LLC) (U.S.), Applied Medical Resources Corporation (U.S.), KLS Martin Group (Germany), BOWA-electronic GmbH & Co. KG (Germany), Getinge AB (Sweden), Stryker Corporation (U.S.), Meril Life Sciences Pvt. Ltd. (India), and Reach Surgical, Inc. (China).

|

Particulars |

Details |

|

Forecast Period |

2026–2036 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

CAGR (Value) |

7.6% |

|

Market Size (Value) in 2026 |

USD 2.85 Billion |

|

Market Size (Value) in 2036 |

USD 5.93 Billion |

|

Segments Covered |

By Product - Instruments (Sealer/Dividers, Dissectors, Shears & Forceps) - Generators - Accessories By Energy Type - Bipolar & Advanced Bipolar Vessel Sealing Devices - Ultrasonic Vessel Sealing Devices - Hybrid (Ultrasonic + Bipolar) Devices - Monopolar Devices By Usability - Single-use/Disposable Devices - Reusable Devices By Surgery Type - Laparoscopic Surgery - Robotic-Assisted Surgery - Open Surgery By Application - General Surgery, Gynecological, Urological, Cardiovascular & Thoracic, Orthopedic, Bariatric, Oncology, Others By End User - Hospitals - Ambulatory Surgical Centers - Specialty Clinics - Others |

|

Countries Covered |

North America (U.S., Canada), Europe (Germany, U.K., France, Italy, Spain, Switzerland, and Rest of Europe), Asia-Pacific (Japan, China, India, South Korea, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and the Middle East & Africa (Saudi Arabia, UAE, South Africa, and Rest of Middle East & Africa) |

|

Key Companies |

Medtronic plc (Ireland), Johnson & Johnson (Ethicon) (U.S.), Olympus Corporation (Japan), B. Braun SE (Aesculap AG) (Germany), CONMED Corporation (U.S.), Erbe Elektromedizin GmbH (Germany), Intuitive Surgical, Inc. (U.S.), Hologic, Inc. (Bolder Surgical, LLC) (U.S.), Applied Medical Resources Corporation (U.S.), KLS Martin Group (Germany), BOWA-electronic GmbH & Co. KG (Germany), Getinge AB (Sweden), Stryker Corporation (U.S.), Meril Life Sciences Pvt. Ltd. (India), and Reach Surgical, Inc. (China). |

The global vessel sealing devices market size is estimated at USD 2.85 billion in 2026.

The market is projected to grow from USD 2.85 billion in 2026 to USD 5.93 billion by 2036, at a CAGR of 7.6%.

The vessel sealing devices market is projected to reach USD 5.93 billion by 2036, at a compound annual growth rate (CAGR) of 7.6% from 2026 to 2036.

Key companies operating in this market include Medtronic plc (Ireland), Johnson & Johnson (Ethicon) (U.S.), Olympus Corporation (Japan), B. Braun SE (Aesculap AG) (Germany), CONMED Corporation (U.S.), Erbe Elektromedizin GmbH (Germany), Intuitive Surgical, Inc. (U.S.), Hologic, Inc. (Bolder Surgical, LLC) (U.S.), Applied Medical Resources Corporation (U.S.), KLS Martin Group (Germany), BOWA-electronic GmbH & Co. KG (Germany), Getinge AB (Sweden), Stryker Corporation (U.S.), Meril Life Sciences Pvt. Ltd. (India), and Reach Surgical, Inc. (China), and others.

The shift toward multifunctional and combined-energy (hybrid) sealing devices, the growing integration of vessel sealing instruments with robotic surgical platforms, and rising demand for reusable, cost-efficient systems are prominent trends in the market.

By product, the instruments segment held the largest share; by energy type, the bipolar & advanced bipolar segment dominated while ultrasonic is expected to grow fastest; by usability, the single-use/disposable segment led; by surgery type, laparoscopic surgery held the largest share while robotic-assisted surgery is expected to grow fastest; by application, general surgery dominated; by end user, the hospitals segment held the largest share; and by geography, North America commanded the largest share in 2026

North America holds the largest share of the vessel sealing devices market in 2026, supported by high surgical volumes and advanced healthcare infrastructure. Asia-Pacific is expected to register the highest growth rate during the forecast period, driven by expanding surgical capacity and rising healthcare investment.

Key drivers include the rising volume of surgical procedures and growing adoption of minimally invasive surgery, increasing preference for advanced energy-based vessel sealing over conventional hemostasis, and expanding adoption of robotic-assisted surgery. These factors are collectively accelerating adoption of vessel sealing devices across care settings.

Published Date: Jan-2025

Published Date: May-2024

Published Date: Feb-2026

Published Date: Jan-2023

Published Date: May-2024

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates