Resources

About Us

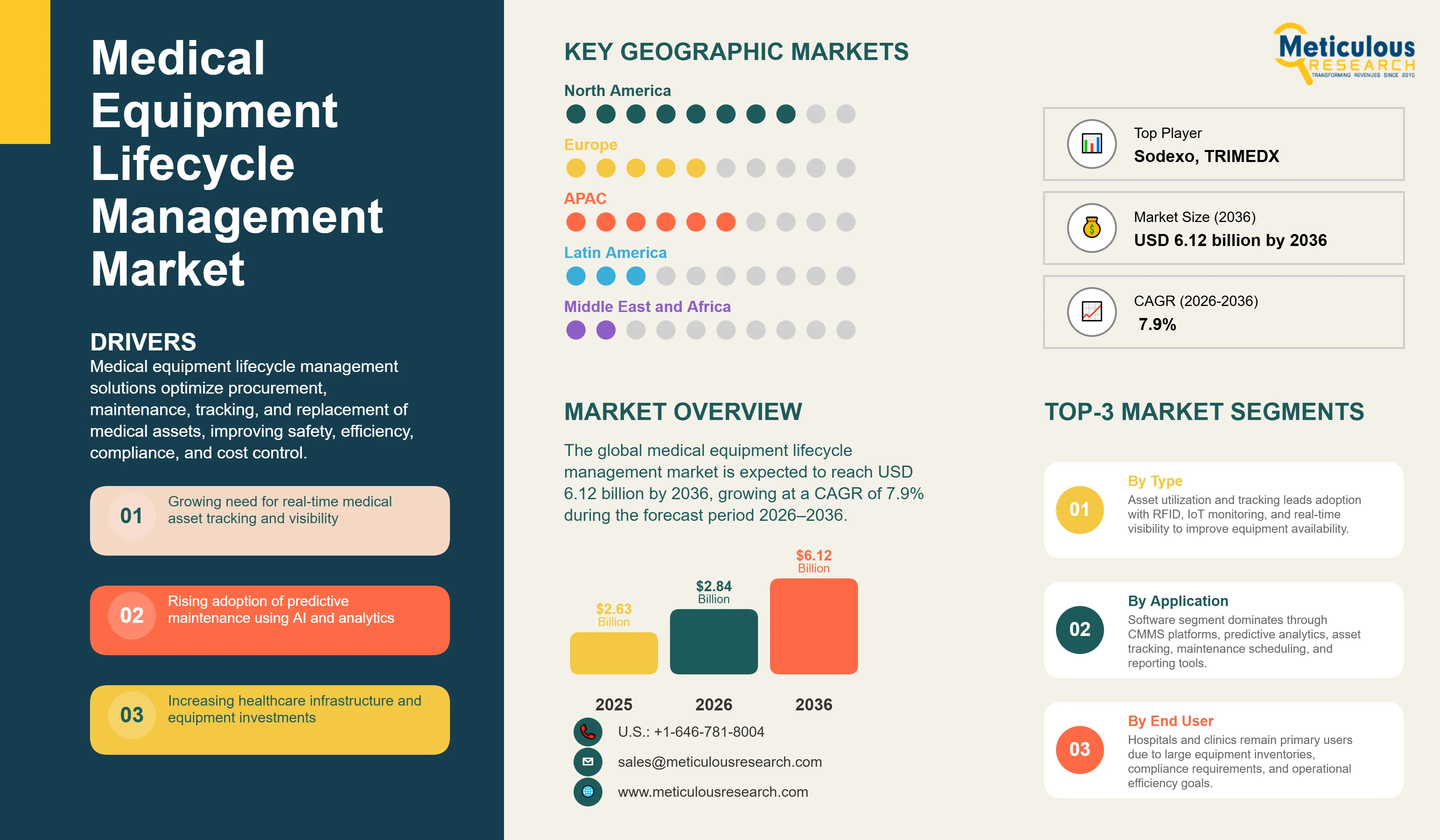

The global medical equipment lifecycle management market is valued at USD 2.84 billion in 2026. This market is expected to reach USD 6.12 billion by 2036, growing at a CAGR of 7.9% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global medical equipment lifecycle management market is a critical segment of the healthcare operations industry, providing the essential infrastructure for managing the end-to-end lifecycle of medical assets, from procurement and maintenance to decommissioning and replacement planning. Healthcare Technology Management (HTM) and Clinical Asset Management solutions, including biomedical equipment management systems and RFID asset tracking tools, enable healthcare organizations to maintain operational integrity and patient safety. As of 2026, the market is undergoing a significant transformation, driven by the global imperative to control healthcare costs and manage increasingly complex medical equipment fleets. The importance of effective lifecycle management is underscored by regulatory and safety requirements surrounding medical devices; for example, the U.S. FDA receives more than 2 million medical device reports annually related to suspected device-associated deaths, injuries, and malfunctions, highlighting the need for robust maintenance, tracking, and performance monitoring systems. Additionally, the World Health Organization (WHO) emphasizes preventive maintenance and systematic equipment management as essential for extending equipment life, reducing failures, and ensuring safe healthcare delivery.

The transition toward integrated and cloud-native HTM platforms is becoming increasingly important for improving operational efficiency and capital equipment planning. Modern lifecycle management solutions leverage advanced analytics, IoT-enabled monitoring, and centralized asset repositories to provide a unified view of equipment performance, utilization, maintenance history, and replacement needs. WHO’s latest guidance on inventory and maintenance management information systems highlights the growing importance of digital platforms for ensuring the availability, traceability, and proper management of medical devices throughout their lifecycle. By integrating computerized maintenance management systems (CMMS) with hospital information systems and other enterprise platforms, healthcare providers can improve asset visibility, streamline maintenance workflows, and support data-driven capital planning. As healthcare systems continue shifting toward value-based care and operational efficiency models, demand is increasing for solutions that can reduce equipment downtime, improve utilization rates, and optimize replacement planning. Market growth is further supported by the adoption of AI-powered asset analytics and predictive maintenance capabilities, which help healthcare organizations proactively identify performance issues, reduce service disruptions, and enhance biomedical equipment reliability and patient safety.

Drivers: Optimizing Hospital Operations through Advanced Clinical Asset Management and IoT-Based Monitoring

The primary driver for the medical equipment lifecycle management market is the escalating cost of healthcare and the increasing complexity of medical assets, which require a more efficient and data-driven approach to equipment management. The World Health Organization (WHO) has emphasized that inadequate maintenance and poor management practices can shorten equipment lifespan and reduce the availability of essential technologies, highlighting the importance of structured Healthcare Technology Management (HTM) programs. In addition, the Association for the Advancement of Medical Instrumentation (AAMI) provides standards and best practices aimed at improving equipment performance and asset utilization.

The growing volume of medical equipment and the complexity of asset data are compelling hospitals to modernize their tracking and inventory management infrastructure. According to the U.S. Food and Drug Administration (FDA), more than 2 million medical device reports are submitted annually involving suspected device-related deaths, injuries, and malfunctions, underscoring the need for robust maintenance and performance monitoring systems. Consequently, the shift toward digital health and the increasing demand for real-time equipment monitoring are major market drivers. Government initiatives supporting healthcare digitization and interoperability are further accelerating investments in integrated lifecycle management solutions, while AI-enabled analytics and predictive maintenance technologies are enhancing equipment reliability and operational efficiency.

Restraints: High Implementation Costs and Data Interoperability Challenges

Market growth is restrained by the high cost of implementing comprehensive medical equipment lifecycle management solutions and the technical challenges of achieving seamless data interoperability across disparate device platforms and legacy IT systems. For many mid-sized hospitals, the initial capital investment and ongoing maintenance costs of an advanced asset management platform, such as a cloud-based CMMS or RFID asset tracking system, can be a significant barrier. Additionally, the lack of standardized data protocols between different medical device manufacturers often leads to data silos, making it difficult to achieve a truly unified clinical asset record. Concerns regarding data privacy and cybersecurity in centralized information hubs also act as deterrents to market expansion. Furthermore, the significant organizational change management and specialized training required for successful lifecycle management implementation can lead to slower adoption rates among biomedical engineering staff.

Opportunities: Advancing AI-Powered Predictive Maintenance and Capital Equipment Planning

The integration of artificial intelligence (AI) and machine learning (ML) into lifecycle management platforms offers substantial growth opportunities. AI-powered tools can analyze complex equipment performance data and clinical evidence to identify potential failure risks, facilitating more proactive preventive maintenance management. By 2026, AI-driven predictive maintenance is being used to forecast the risk of equipment downtime, enabling proactive intervention and improving patient safety. Furthermore, the shift toward cloud-native (SaaS) CMMS for healthcare platforms provides organizations with superior scalability, flexibility, and lower upfront costs. Cloud-based solutions also facilitate real-time data sharing among global biomedical engineering teams, supporting multi-disciplinary collaboration. The development of advanced equipment replacement planning modules, which use predictive analytics to optimize capital equipment budgets, represents a high-value growth opportunity for market players.

Evolution toward Holistic and AI-Powered Healthcare Technology Management (HTM)

A defining trend in 2026 is the evolution of lifecycle management from siloed tracking tools into holistic, AI-powered Healthcare Technology Management (HTM) platforms. These systems consolidate data across procurement, maintenance, and utilization to provide a unified view of equipment performance and asset health. The World Health Organization (WHO) estimates that 50–80% of medical equipment in low- and middle-income countries is partially or completely unusable due to inadequate maintenance and management, underscoring the importance of comprehensive HTM programs. In parallel, the Association for the Advancement of Medical Instrumentation (AAMI) continues to promote digital HTM frameworks and predictive maintenance strategies to improve equipment reliability and operational efficiency. AI-enabled automation is increasingly being deployed to streamline maintenance scheduling, documentation, and service workflows, supporting a shift toward proactive enterprise-wide asset management.

Integration of RFID Asset Tracking and IoT-Based Equipment Monitoring

The integration of RFID asset tracking and IoT-based equipment monitoring into lifecycle management platforms is gaining significant traction. According to the U.S. Food and Drug Administration (FDA), more than 2 million medical device reports involving suspected device-related malfunctions, injuries, and deaths are submitted annually, reinforcing the need for continuous equipment monitoring and traceability. Furthermore, the World Health Organization highlights inventory management systems and real-time asset tracking as essential elements of effective medical equipment management. IoT-enabled connected equipment modules are increasingly being used to improve asset visibility, accelerate maintenance response times, and enhance equipment utilization, while regulatory requirements and growing emphasis on patient safety continue to drive adoption of intelligent tracking technologies.

Asset Utilization and Tracking

The asset utilization and tracking segment is expected to hold the largest share in 2026. This dominance is driven by the foundational role of these platforms in managing and tracking mobile medical equipment across diverse hospital settings. Hospitals are increasingly adopting RFID asset tracking and IoT-based monitoring to achieve 100% asset visibility and reduce equipment loss. By optimizing asset utilization management, healthcare organizations can significantly reduce capital expenditure on redundant equipment and improve clinical productivity.

Preventive Maintenance Management

The preventive maintenance management segment is projected to register the highest CAGR. This growth is fueled by the increasing demand for structured interpretation and AI-driven documentation of equipment performance. Modern medical equipment maintenance workflows are shifting from reactive to proactive, with hospitals leveraging predictive maintenance to identify potential failure risks before they impact patient care. This segment's expansion is critical for ensuring equipment safety and regulatory compliance with standards such as ISO and The Joint Commission.

Equipment Replacement Planning

The equipment replacement planning segment is a high-value growth area, as hospitals seek to optimize their capital equipment planning and budgeting. By using advanced analytics to assess equipment performance and total cost of ownership (TCO), healthcare organizations can make data-driven decisions on when to replace or upgrade medical assets. This strategic approach ensures that hospitals maintain a modern and efficient equipment fleet while maximizing their return on investment (ROI).

Software (CMMS, Asset Tracking Software)

The software segment is expected to account for the largest share in 2026. This includes advanced CMMS for healthcare, healthcare asset tracking software, and AI-powered asset management platforms. The increasing reliance on automated tracking, predictive analytics, and real-time data visualization is driving the demand for sophisticated software solutions. Vendors are focusing on developing integrated platforms that provide end-to-end visibility into the medical equipment lifecycle.

Services (Integration, Maintenance, Calibration)

The services segment is projected to exhibit a steady CAGR, reflecting the ongoing need for technical expertise in equipment integration, calibration management, and medical equipment maintenance. As medical equipment becomes more complex, healthcare organizations are increasingly outsourcing their HTM and biomedical engineering services to specialized vendors. This trend allows hospitals to focus on their core mission of patient care while ensuring that their equipment fleet is managed by experts.

North America is expected to dominate the global medical equipment lifecycle management market in 2026, accounting for an estimated 41.5% of total revenue. The region's leadership is supported by a large installed base of medical devices, mature healthcare IT infrastructure, and substantial investments in digital transformation. According to the U.S. Centers for Medicare & Medicaid Services (CMS), national health expenditures reached USD 4.9 trillion in 2023, reflecting continued investment in healthcare infrastructure and operational efficiency. Strong regulatory oversight and accreditation requirements emphasizing equipment safety and clinical quality, together with the presence of leading lifecycle management vendors, further contribute to North America's dominant position.

The Asia Pacific region is projected to witness the fastest growth during the forecast period. This growth is driven by expanding healthcare infrastructure, increasing deployment of advanced medical equipment, and government-led digital health initiatives across China, India, and Japan. Programs such as India's Ayushman Bharat Digital Mission and broader healthcare modernization efforts are accelerating the adoption of integrated asset management systems. In addition, the increasing use of cloud-based platforms and IoT-enabled monitoring solutions is creating substantial opportunities for both global and regional vendors.

The competitive landscape of the global medical equipment lifecycle management market is characterized by intense innovation and strategic consolidations as vendors seek to provide end-to-end healthcare technology management (HTM) platforms. Leading players are differentiating themselves through the sophistication of their AI engines and their ability to provide seamless integration with clinical and hospital management platforms. Strategic acquisitions of niche tracking and analytics companies are a common trend as vendors seek to enhance their diagnostic capabilities. The market is also seeing increased collaboration between vendors and healthcare organizations to ensure seamless equipment management across the product lifecycle.

Key players operating in the global market include GE HealthCare Technologies Inc. (U.S.), Siemens Healthineers AG (Germany), Koninklijke Philips N.V. (Netherlands), Baxter International Inc. (U.S.), TRIMEDX (U.S.), Sodexo (France), Aramark (U.S.), Agiliti Health, Inc. (U.S.), Nuvolo (U.S.), and various emerging technology providers specializing in clinical asset management and AI-driven diagnostic tools.

The market is projected to reach USD 6.12 billion by 2036, growing at a CAGR of 7.9% from 2026 to 2036.

Hospitals report a significant reduction in equipment downtime and an improvement in asset utilization rates.

The preventive maintenance management segment is expected to grow the fastest as hospitals prioritize AI-driven documentation and performance monitoring.

Around 70–75% of new lifecycle management deployments are cloud-based in 2026, driven by demand for scalability, interoperability, and lower infrastructure requirements.

North America holds the largest share, estimated at 41.5% in 2026, driven by high HTM adoption and mature IT infrastructure.

AI enables the prediction of equipment failure and automates routine maintenance scheduling, improving equipment safety and patient safety.

The pressure to reduce capital expenditure is driving the demand for integrated platforms to manage the high volume of medical equipment.

Hospitals and clinics are the primary adopters, managing the highest volumes of diverse medical equipment fleets.

These systems provide the continuous, data-driven equipment management necessary to improve clinical outcomes and reduce the total cost of healthcare operations.

The top 5 players are GE HealthCare, Siemens Healthineers, Koninklijke Philips N.V., Baxter International, and TRIMEDX

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/KOL Interviews

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Type

3.2.2. Market Analysis, by Component

3.2.3. Market Analysis, by Deployment Mode

3.2.4. Market Analysis, by End User

3.2.5. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Optimizing Hospital Operations through Advanced Clinical Asset Management

4.2.1.2. Rising Volume of Medical Equipment and Complexity of Asset Data

4.2.1.3. Integration of AI and IoT for Predictive Maintenance and Performance Monitoring

4.2.2. Restraints

4.2.2.1. High Implementation Costs and Multi-Year ROI Cycles

4.2.2.2. Data Interoperability Challenges Across Fragmented IT Systems

4.2.3. Opportunities

4.2.3.1. Advancing AI-Powered Predictive Maintenance and Capital Equipment Planning

4.2.3.2. Expansion into Emerging Markets and Regional Healthcare Networks

4.2.3.3. Integration of RFID Asset Tracking and Connected Medical Equipment Management

4.2.4. Challenges

4.2.4.1. Managing Cybersecurity Risks in Centralized Asset Management Hubs

4.2.4.2. Addressing Data Sovereignty and Privacy Regulations (GDPR/HIPAA)

4.2.4.3. Organizational Resistance to Workflow Modernization

4.2.5. Trends

4.2.5.1. Evolution toward Holistic and AI-Powered Healthcare Technology Management (HTM)

4.2.5.2. Integration of IoT-Based Equipment Monitoring for Efficient Maintenance

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Medical Equipment Lifecycle Management Market, by Type

5.1. Overview

5.2. Asset Utilization and Tracking

5.3. Preventive Maintenance Management

5.4. Equipment Replacement Planning

5.5. Medical Equipment Inventory Management

6. Global Medical Equipment Lifecycle Management Market, by Component

6.1. Overview

6.2. Software (CMMS, Asset Tracking Software)

6.3. Services (Integration, Maintenance, Calibration)

7. Global Medical Equipment Lifecycle Management Market, by Deployment Mode

7.1. Overview

7.2. Cloud-Based (SaaS) Deployment

7.3. On-Premises Deployment

8. Global Medical Equipment Lifecycle Management Market, by End User

8.1. Overview

8.2. Hospitals and Clinics

8.3. Specialized Care Facilities

8.4. Academic and Research Institutes

8.5. Pharmaceutical and Biotechnology Companies

9. Global Medical Equipment Lifecycle Management Market, by Geography

9.1. Overview

9.2. North America

9.2.1. U.S.

9.2.2. Canada

9.3. Europe

9.3.1. Germany

9.3.2. U.K.

9.3.3. France

9.3.4. Italy

9.3.5. Spain

9.3.6. Rest of Europe

9.4. Asia-Pacific

9.4.1. China

9.4.2. Japan

9.4.3. India

9.4.4. South Korea

9.4.5. Australia

9.4.6. Rest of Asia-Pacific

9.5. Latin America

9.5.1. Brazil

9.5.2. Mexico

9.5.3. Rest of Latin America

9.6. Middle East & Africa

9.6.1. GCC Countries

9.6.2. South Africa

9.6.3. Rest of Middle East & Africa

10. Competitive Landscape

10.1. Overview

10.2. Key Strategic Developments

10.3. Market Share Analysis

10.4. Competitive Benchmarking

11. Company Profiles

11.1. GE HealthCare Technologies Inc.

11.2. Siemens Healthineers AG

11.3. Koninklijke Philips N.V.

11.4. TRIMEDX

11.5. Sodexo

11.6. Agiliti Health, Inc.

11.7. STERIS plc

11.8. Crothall Healthcare

11.9. Nuvolo

11.10. Accruent

11.11. IBM Corporation (Maximo)

11.12. Oracle Corporation

11.13. SAP SE

11.14. ServiceNow, Inc.

11.15. TMA Systems

11.16. Brightly Software, Inc.

11.17. PartsSource Inc.

11.18. Zebra Technologies Corporation

11.19. Fluke Biomedical

11.20. Drägerwerk AG & Co. KGaA

12. Appendix

Published Date: Jun-2026

Published Date: Jan-2026

Published Date: Jun-2024

Subscribe to get the latest industry updates