Resources

About Us

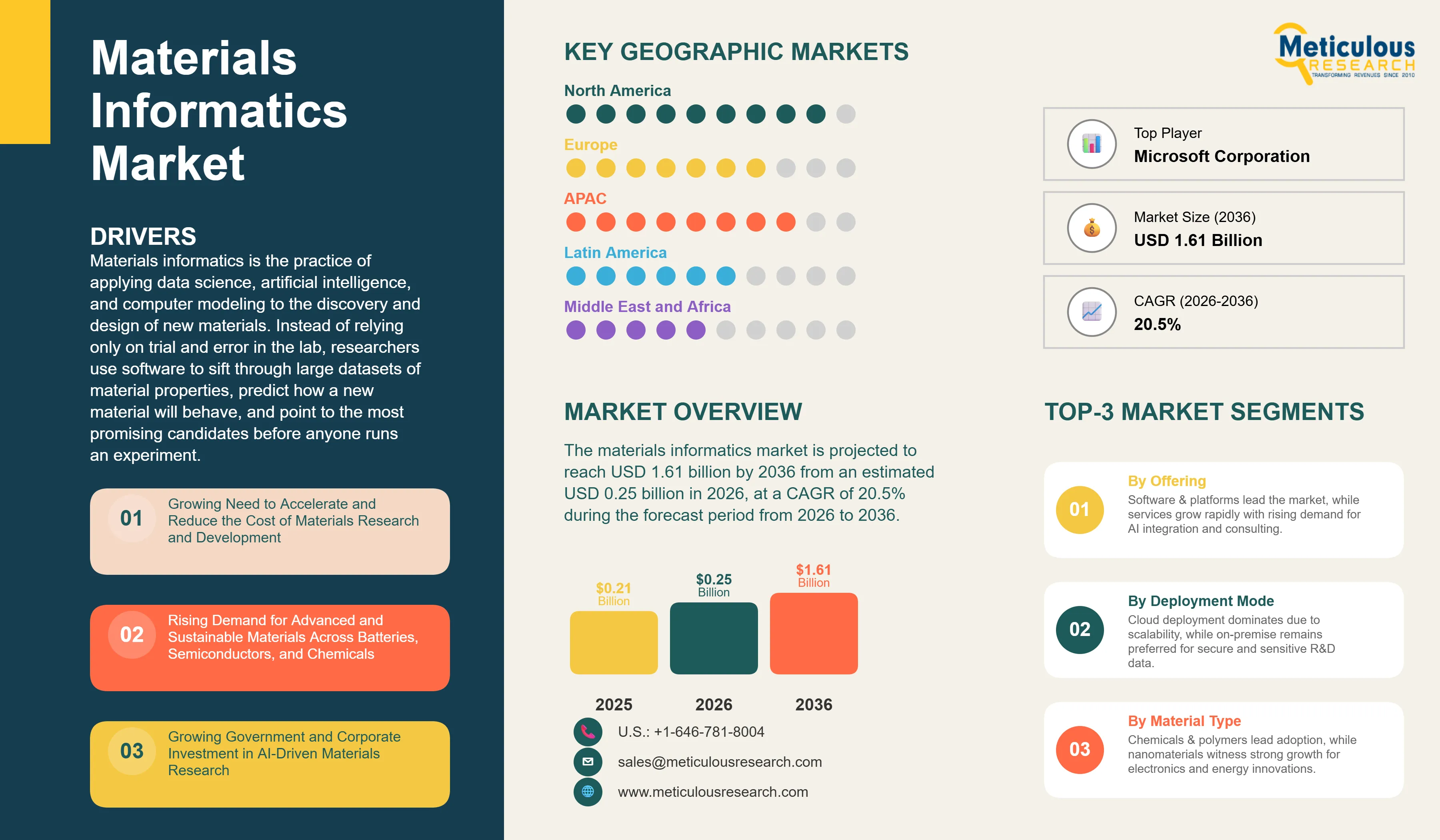

The global materials informatics market is projected to reach USD 1.61 billion by 2036 from an estimated USD 0.25 billion in 2026, at a CAGR of 20.5% during the forecast period from 2026 to 2036.

Click here to: Get Free Sample Pages

Click here to: Get Free Sample Pages

Materials informatics is the practice of applying data science, artificial intelligence, and computer modeling to the discovery and design of new materials. Instead of relying only on trial and error in the lab, researchers use software to sift through large datasets of material properties, predict how a new material will behave, and point to the most promising candidates before anyone runs an experiment. The field brings together materials databases, machine learning models, and simulation tools, and it increasingly connects to automated labs that can test the ideas the software suggests.

The reason this matters is simple economics. Developing a new material the traditional way can take ten to twenty years and a great deal of money, because it means making and testing one candidate at a time. Materials informatics compresses that cycle. By screening thousands of possibilities on a computer and focusing lab work on the best few, companies can move from idea to product far faster and at lower cost. For industries under pressure to innovate quickly, that speed is a real competitive advantage, which is why adoption is spreading.

Demand is being pulled hardest by the race for advanced and sustainable materials. Electric vehicles and grid storage need better batteries, electronics need higher-performing semiconductor materials, and the chemical industry needs greener formulations. Each of these areas involves searching an enormous space of possible compounds, which is exactly the kind of problem AI handles well. Citrine Informatics, for example, has used its platform to identify better battery electrolyte materials and to find solvent blends that outperform older benchmarks in a matter of months rather than years.

The overall materials informatics market is still niche and growing rapidly. Specialists such as Citrine Informatics, Schrödinger, and Materials Zone offer AI platforms built for materials work, while larger companies such as Dassault Systèmes, IBM, Microsoft, and Siemens fold materials informatics into broader research and design software. Governments in the United States, Europe, China, and Japan are funding the field and encouraging open materials data. With R&D costs high, the demand for better materials rising, and AI methods improving fast, the materials informatics market is set for strong growth over the coming decade.

Growing Need to Accelerate and Reduce the Cost of Materials R&D

The strongest driver of the materials informatics market is the growing need to accelerate materials research while reducing development costs. Developing a new material using conventional experimental approaches is typically a lengthy and resource-intensive process, often taking 10–20 years from discovery to commercialization, particularly in industries such as batteries, semiconductors, aerospace, and specialty chemicals. As product life cycles continue to shorten and innovation becomes increasingly critical, organizations are seeking technologies that can significantly reduce research timelines and improve R&D productivity.

Materials informatics addresses this challenge by combining artificial intelligence, machine learning, high-performance computing, and materials data to predict material properties and identify promising candidates before physical testing begins. Instead of relying solely on trial-and-error experimentation, researchers can computationally screen thousands or even millions of potential material compositions, allowing laboratory resources to focus on the most promising candidates. This significantly reduces the number of costly experiments while improving the probability of successful material discovery.

The commercial impact of this approach is becoming increasingly evident. For example, Microsoft Corporation's Azure Quantum Elements combines AI, high-performance computing, and quantum-inspired simulations to accelerate the discovery of advanced battery materials and sustainable chemicals. Similarly, the U.S. Department of Energy's Materials Project, one of the world's largest open materials databases, provides computational data on more than 190,000 materials, enabling researchers worldwide to rapidly identify and evaluate candidate materials using AI-driven workflows. These initiatives demonstrate how computational materials discovery is transforming traditional R&D by reducing development time and enabling faster innovation.

As industries including chemicals, batteries, semiconductors, electronics, aerospace, and advanced manufacturing continue to seek shorter innovation cycles and lower R&D costs, the adoption of materials informatics platforms is expected to accelerate. The ability to reduce experimental effort, optimize research investments, and shorten time-to-market has positioned materials informatics as one of the most important digital technologies for next-generation materials development.

Rising Demand for Advanced and Sustainable Materials

A second major driver of the materials informatics market is the growing demand for advanced and sustainable materials across industries such as electric vehicles, renewable energy, semiconductors, aerospace, chemicals, and electronics. The global transition toward electrification and decarbonization is significantly increasing the need for materials with higher performance, improved durability, lower environmental impact, and greater resource efficiency. For example, the International Energy Agency (IEA) estimates that achieving global clean energy goals will require a four- to six-fold increase in demand for critical minerals by 2040, driven primarily by batteries, electric vehicles, renewable energy technologies, and electricity networks.

Meeting these evolving performance and sustainability requirements requires manufacturers to evaluate an enormous design space of possible material compositions. Traditional trial-and-error experimentation is often too slow and resource-intensive for this purpose. Materials informatics enables researchers to combine artificial intelligence, machine learning, and computational modeling to rapidly screen thousands of candidate materials, identify optimal compositions, and reduce the number of physical experiments required. This capability is increasingly being applied to battery materials, catalysts, lightweight alloys, specialty chemicals, advanced ceramics, and high-performance polymers.

The growing emphasis on sustainability is further accelerating adoption. Manufacturers are under increasing pressure to develop recyclable materials, reduce reliance on critical raw materials, eliminate hazardous substances, and improve energy efficiency throughout the product lifecycle. Regulatory initiatives such as the European Union's Critical Raw Materials Act and growing investments in battery, hydrogen, and semiconductor manufacturing are encouraging organizations to adopt digital tools that accelerate the discovery of next-generation materials while reducing development costs and time-to-market.

As industries continue to prioritize high-performance and environmentally sustainable materials, the need for faster, data-driven materials discovery is expected to increase, supporting the continued growth of the materials informatics market.

Growing Government and Corporate Investment in AI-Driven Materials Research

A third driver is the growing investment in AI-driven materials research from governments, national laboratories, and leading technology companies. Recognizing that advanced materials are critical to clean energy, semiconductors, aerospace, healthcare, and defense, governments across North America, Europe, and Asia-Pacific are accelerating funding for digital materials innovation. For example, the U.S. Department of Energy (DOE) continues to support the Materials Project, one of the world's largest open materials databases, providing researchers access to computational data on more than 190,000 materials to accelerate AI-enabled materials discovery. Similarly, the European Commission continues to fund AI-enabled materials research through Horizon Europe, supporting collaborative projects focused on sustainable materials, battery technologies, and advanced manufacturing.

Corporate investment is also accelerating as companies increasingly integrate AI into materials research and development. In 2024, Microsoft Corporation introduced Azure Quantum Elements, an AI-powered platform for scientific discovery that combines high-performance computing, AI, and quantum-inspired simulations to accelerate the discovery of novel materials for batteries, catalysts, and electronics. Likewise, IBM Corporation continues to expand its AI for Science initiatives, applying foundation models and generative AI to accelerate molecular and materials discovery, while companies such as Schrödinger, Inc., Citrine Informatics, Inc., Materials Zone Ltd., and SandboxAQ, Inc. are partnering with chemical, pharmaceutical, and advanced materials manufacturers to shorten product development cycles through AI-driven materials design.

The continued expansion of publicly available materials databases, high-performance computing infrastructure, and collaborative research programs is reducing barriers to AI adoption while improving data availability and model accuracy. As governments, research institutions, and private enterprises continue investing in AI-enabled materials innovation, organizations across industries are increasingly adopting materials informatics platforms to accelerate research, reduce development costs, and bring new materials to market faster.

By Offering: Software & Platforms Lead the Market in 2026

By offering, the market splits into software and platforms, and services. Software and platforms hold the largest share in 2026, at roughly 72%. The AI platforms that predict material properties, manage data, and run discovery workflows are the core of what companies buy, so licenses and subscriptions make up the bulk of spending.

Services are expected to grow the fastest through 2036. As more organizations adopt these platforms, demand rises for the consulting, data curation, integration, and model validation needed to fit the tools into existing research workflows and to prove they deliver a return, which lifts the services segment.

By Deployment Mode: Cloud Leads the Market in 2026

By deployment mode, the market splits into cloud and on-premise. Cloud holds the largest share in 2026, at around 60%. Cloud platforms give research teams scalable computing, easy access to large datasets, and a way to collaborate across sites, which suits the data-heavy nature of materials work and has made cloud the preferred choice.

Cloud is also the fastest-growing segment of the market, as research moves toward scalable, subscription-based platforms. On-premise deployment remains important for companies with highly sensitive intellectual property or strict data rules, but its share is growing more slowly as cloud adoption widens.

By Material Type: Chemicals & Polymers Lead the Market in 2026

By material type, the materials informatics market covers chemicals and polymers, metals and alloys, composites, semiconductor and electronic materials, nanomaterials, and other materials. Chemicals and polymers hold the largest share in 2026, at roughly 33%. The chemical and polymer industries generate vast amounts of data and run continuous searches for better formulations, so they make the heaviest use of materials informatics.

Nanomaterials are expected to grow the fastest through 2036. Their complex, tunable properties and their use in electronics, energy, and healthcare make them a natural fit for AI-driven design, and rising interest in these materials is driving quick growth in the segment.

By Technique: Machine Learning Leads the Market in 2026

By technique, the market covers machine learning, deep learning, generative models, statistical analysis, and genetic algorithms and other methods. Machine learning holds the largest share in 2026, at about 35%. It is the workhorse of materials informatics, used to predict properties, spot patterns in data, and rank candidates, and its balance of accuracy and practicality keeps it in front.

Generative models are expected to grow the fastest from 2026 to 2036. Their ability to propose entirely new materials that meet a set of targets, rather than only assess known ones, is drawing strong interest, and their adoption is rising quickly as the tools mature.

By Application: Property Prediction Leads the Market in 2026

By application, the materials informatics market covers materials discovery, property prediction, product development and optimization, and synthesis route prediction. Property prediction holds the largest share in 2026, at about 31%. Estimating how a material will behave before making it is the most common and immediately useful task in the field, so it draws the most investment.

Synthesis route prediction is expected to grow the fastest during the forecast period. As companies look not just to design a promising material but to work out how to actually make it, demand for tools that predict practical synthesis routes is rising quickly, which is driving growth in this application.

By End User: Chemicals & Petrochemicals Lead the Market in 2026

By end user, the market covers chemicals and petrochemicals, pharmaceuticals and biotechnology, electronics and semiconductors, energy and batteries, automotive and aerospace, food and consumer goods, and other industries. Chemicals and petrochemicals hold the largest share in 2026, at close to 24%. This sector has the longest history of large-scale R&D, the most data, and a constant need for new formulations, so it leads adoption of materials informatics.

Electronics and semiconductors are expected to grow the fastest. The relentless push for smaller, faster, cooler-running devices calls for a steady stream of new materials, and chipmakers and electronics firms are adopting AI-driven discovery quickly to keep pace, making this the fastest-growing end user.

North America Leads the Global Materials Informatics Market in 2026

By region, the market is split across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America holds the largest share in 2026, at roughly 39%.

North America's lead rests on heavy R&D spending, early adoption of AI and machine learning in materials science, and a deep base of technology providers and research institutions, including Citrine Informatics, Schrödinger, IBM, and Microsoft, along with national laboratories and leading universities. The United States is the dominant national market, supported by strong public and private investment in AI-driven materials research.

Asia-Pacific is expected to record the fastest growth over the forecast period. Large and rising investment in materials science across China, Japan, and South Korea, a strong electronics and battery manufacturing base, and active national research programs are driving demand. Japan's National Institute for Materials Science, for example, has published machine-learning materials maps that predict thousands of new material phases. Europe remains an important market, supported by strong chemical, automotive, and industrial sectors and by vendors such as Dassault Systèmes and Siemens.

Leading companies in the materials informatics market are strengthening their competitive positions through AI platform enhancements, strategic partnerships, product innovations, acquisitions, and the expansion of materials data ecosystems. Key competitive strategies include integrating generative AI and foundation models into materials discovery workflows, expanding computational simulation capabilities, enhancing materials data management platforms, and collaborating with industrial enterprises, research institutions, and cloud technology providers to accelerate materials innovation.

Prominent companies operating in the global materials informatics market include Schrödinger, Inc. (U.S.), Dassault Systèmes SE (BIOVIA) (France), Citrine Informatics, Inc. (U.S.), International Business Machines Corporation (IBM) (U.S.), Microsoft Corporation (U.S.), Materials Zone Ltd. (Israel), SandboxAQ, Inc. (U.S.), Kebotix, Inc. (U.S.), Phaseshift Technologies Inc. (Canada), Mat3ra, Inc. (formerly Exabyte.io) (U.S.), Orbital Materials Ltd. (U.K.), Siemens AG (Germany), Ansys, Inc. (Granta MI) (U.S.), Noble.AI, Inc. (U.S.), and Intellegens Ltd. (U.K.).

|

Particulars |

Details |

|

Forecast Period |

2026 to 2036 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

CAGR (Value) |

20.5% |

|

Market Size (Value) in 2026 |

USD 0.25 Billion |

|

Market Size (Value) in 2036 |

USD 1.61 Billion |

|

Segments Covered |

By Offering - Software & Platforms - Services (Consulting, Integration & Deployment, Support) By Deployment Mode - Cloud - On-premise By Material Type - Chemicals & Polymers, Metals & Alloys, Composites, Semiconductor & Electronic Materials, Nanomaterials, Others By Technique - Machine Learning, Deep Learning, Generative Models, Statistical Analysis, Genetic Algorithm & Others By Application - Materials Discovery, Property Prediction, Product Development & Optimization, Synthesis Route Prediction By End User - Chemicals & Petrochemicals, Pharma & Biotech, Electronics & Semiconductors, Energy & Batteries, Automotive & Aerospace, Food & Consumer Goods, Others |

|

Countries Covered |

North America (U.S., Canada), Europe (Germany, U.K., France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, South Korea, India, Australia, and Rest of Asia-Pacific), Latin America (Brazil, Mexico, and Rest of Latin America), and the Middle East & Africa (Israel, Saudi Arabia, UAE, and Rest of Middle East & Africa) |

|

Key Companies |

Schrödinger, Inc. (U.S.), Dassault Systèmes SE (BIOVIA) (France), Citrine Informatics, Inc. (U.S.), International Business Machines Corporation (U.S.), Microsoft Corporation (U.S.), Materials Zone Ltd. (Israel), Hitachi High-Tech Corporation (Japan), Kebotix, Inc. (U.S.), Phaseshift Technologies Inc. (Canada), Mat3ra, Inc. (U.S.), Enthought, Inc. (U.S.), Siemens AG (Germany), Ansys, Inc. (Granta MI) (U.S.), Noble.AI, Inc. (U.S.), and Intellegens Ltd. (U.K.) |

The global materials informatics market size is estimated at USD 0.25 billion in 2026.

The market is projected to grow from USD 0.25 billion in 2026 to USD 1.61 billion by 2036, at a CAGR of 20.5%.

The materials informatics market is projected to reach USD 1.61 billion by 2036, at a compound annual growth rate (CAGR) of 20.5% from 2026 to 2036.

Key companies in this market include Schrödinger, Inc. (U.S.), Dassault Systèmes SE (BIOVIA) (France), Citrine Informatics, Inc. (U.S.), International Business Machines Corporation (U.S.), Microsoft Corporation (U.S.), Materials Zone Ltd. (Israel), Hitachi High-Tech Corporation (Japan), Kebotix, Inc. (U.S.), Phaseshift Technologies Inc. (Canada), Mat3ra, Inc. (U.S.), Enthought, Inc. (U.S.), Siemens AG (Germany), Ansys, Inc. (Granta MI) (U.S.), Noble.AI, Inc. (U.S.), and Intellegens Ltd. (U.K.), and others.

The rise of generative AI models for materials design, and the integration of materials informatics with lab automation to build closed-loop, self-driving labs, are prominent trends in the market.

In 2026, software and platforms lead by offering, cloud leads by deployment, chemicals and polymers lead by material type, machine learning leads by technique, property prediction leads by application, chemicals and petrochemicals lead by end user, and North America leads by region. Services, nanomaterials, generative models, synthesis route prediction, and electronics and semiconductors are among the fastest-growing segments.

North America holds the largest share of the market in 2026, supported by strong R&D spending and a deep base of technology providers. Asia-Pacific is expected to record the highest growth rate over the forecast period, driven by heavy investment in materials science across China, Japan, and South Korea.

Key drivers include the growing need to accelerate and reduce the cost of materials R&D, rising demand for advanced and sustainable materials across batteries, semiconductors, and chemicals, and growing government and corporate investment in AI-driven materials research. Together, these are supporting rapid adoption across industries.

1. Introduction

1.1. Market Definition

1.2. Currency & Limitations

2. Research Methodology

2.1. Research Approach

2.2. Data Collection & Validation

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Assessment

2.3.1. Market Size Estimation

2.3.2. Bottom-Up Approach

2.3.3. Top-Down Approach

2.3.4. Growth Forecast

2.4. Assumptions for the Study

3. Executive Summary

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Growing Need to Accelerate and Reduce the Cost of Materials Research and Development

4.2.1.2. Rising Demand for Advanced and Sustainable Materials Across Batteries, Semiconductors, and Chemicals

4.2.1.3. Growing Government and Corporate Investment in AI-Driven Materials Research

4.2.2. Restraints

4.2.2.1. Shortage of Skilled Talent and High Cost of Platforms and Services Limiting Adoption

4.2.3. Opportunities

4.2.3.1. Generative AI and Large Language Models Creating New Opportunities in Materials Design

4.2.3.2. Growth in Battery, Semiconductor, and Sustainable Materials Development

4.2.4. Challenges

4.2.4.1. Insufficient Data Volume and Quality Expected to Remain a Major Challenge

4.3. Key Trends

4.3.1. Rise of Generative AI Models for Materials Design

4.3.2. Integration with Lab Automation for Closed-Loop, Self-Driving Labs

4.4. Vendor Selection Criteria/Factors Influencing Purchase Decisions

4.5. Use Cases

4.6. Porter's Five Forces Analysis

4.6.1. Bargaining Power of Buyers: Moderate

4.6.2. Bargaining Power of Suppliers: Moderate

4.6.3. Threat of Substitutes: Low to Moderate

4.6.4. Threat of New Entrants: Moderate

4.6.5. Degree of Competition: High

4.7. Value Chain Analysis

4.8. Pricing Analysis

4.9. Technology Analysis

4.10. PESTEL Analysis

5. Materials Informatics Market Assessment—By Offering

5.1. Overview

5.2. Software & Platforms

5.3. Services

5.3.1. Consulting

5.3.2. Integration & Deployment

5.3.3. Support & Maintenance

6. Materials Informatics Market Assessment—By Deployment Mode

6.1. Overview

6.2. Cloud

6.3. On-premise

7. Materials Informatics Market Assessment—By Material Type

7.1. Overview

7.2. Chemicals & Polymers

7.3. Metals & Alloys

7.4. Composites

7.5. Semiconductor & Electronic Materials

7.6. Nanomaterials

7.7. Other Materials

8. Materials Informatics Market Assessment—By Technique

8.1. Overview

8.2. Machine Learning

8.3. Deep Learning

8.4. Generative Models

8.5. Statistical Analysis

8.6. Genetic Algorithm & Others

9. Materials Informatics Market Assessment—By Application

9.1. Overview

9.2. Materials Discovery

9.3. Property Prediction

9.4. Product Development & Optimization

9.5. Synthesis Route Prediction

10. Materials Informatics Market Assessment—By End User

10.1. Overview

10.2. Chemicals & Petrochemicals

10.3. Pharmaceuticals & Biotechnology

10.4. Electronics & Semiconductors

10.5. Energy & Batteries

10.6. Automotive & Aerospace

10.7. Food & Consumer Goods

10.8. Other End Users

11. Materials Informatics Market Assessment—By Geography

11.1. Overview

11.2. North America

11.2.1. United States

11.2.2. Canada

11.3. Europe

11.3.1. Germany

11.3.2. United Kingdom

11.3.3. France

11.3.4. Italy

11.3.5. Spain

11.3.6. Rest of Europe

11.4. Asia Pacific

11.4.1. China

11.4.2. Japan

11.4.3. South Korea

11.4.4. India

11.4.5. Australia & New Zealand

11.4.6. Rest of Asia Pacific

11.5. Latin America

11.5.1. Brazil

11.5.2. Mexico

11.5.3. Rest of Latin America

11.6. Middle East & Africa

11.6.1. Israel

11.6.2. Saudi Arabia

11.6.3. United Arab Emirates

11.6.4. Rest of Middle East & Africa

12. Competitive Landscape

12.1. Introduction

12.2. Key Growth Strategies

12.3. Competitive Benchmarking

12.4. Competitive Dashboard

12.4.1. Industry Leaders

12.4.2. Market Differentiators

12.4.3. Vanguards

12.4.4. Emerging Companies

12.5. Market Share/Position Analysis

13. Company Profiles (Company Overview, Financial Overview, Product Portfolio, Strategic Developments)

13.1. Schrödinger, Inc. (U.S.)

13.2. Dassault Systèmes SE (BIOVIA) (France)

13.3. Citrine Informatics, Inc. (U.S.)

13.4. International Business Machines Corporation (IBM) (U.S.)

13.5. Microsoft Corporation (U.S.)

13.6. Materials Zone Ltd. (Israel)

13.7. SandboxAQ, Inc. (U.S.)

13.8. Kebotix, Inc. (U.S.)

13.9. Phaseshift Technologies Inc. (Canada)

13.10. Mat3ra, Inc. (formerly Exabyte.io) (U.S.)

13.11. Orbital Materials Ltd. (U.K.)

13.12. Siemens AG (Germany)

13.13. Ansys, Inc. (Granta MI) (U.S.)

13.14. Noble.AI, Inc. (U.S.)

13.15. Intellegens Ltd. (U.K.)

13.16. Others

14. Appendix

14.1. Available Customization

14.2. Related Reports

Published Date: Jul-2026

Published Date: Jun-2026

Published Date: Jun-2026

Published Date: Jun-2026

Subscribe to get the latest industry updates