Resources

About Us

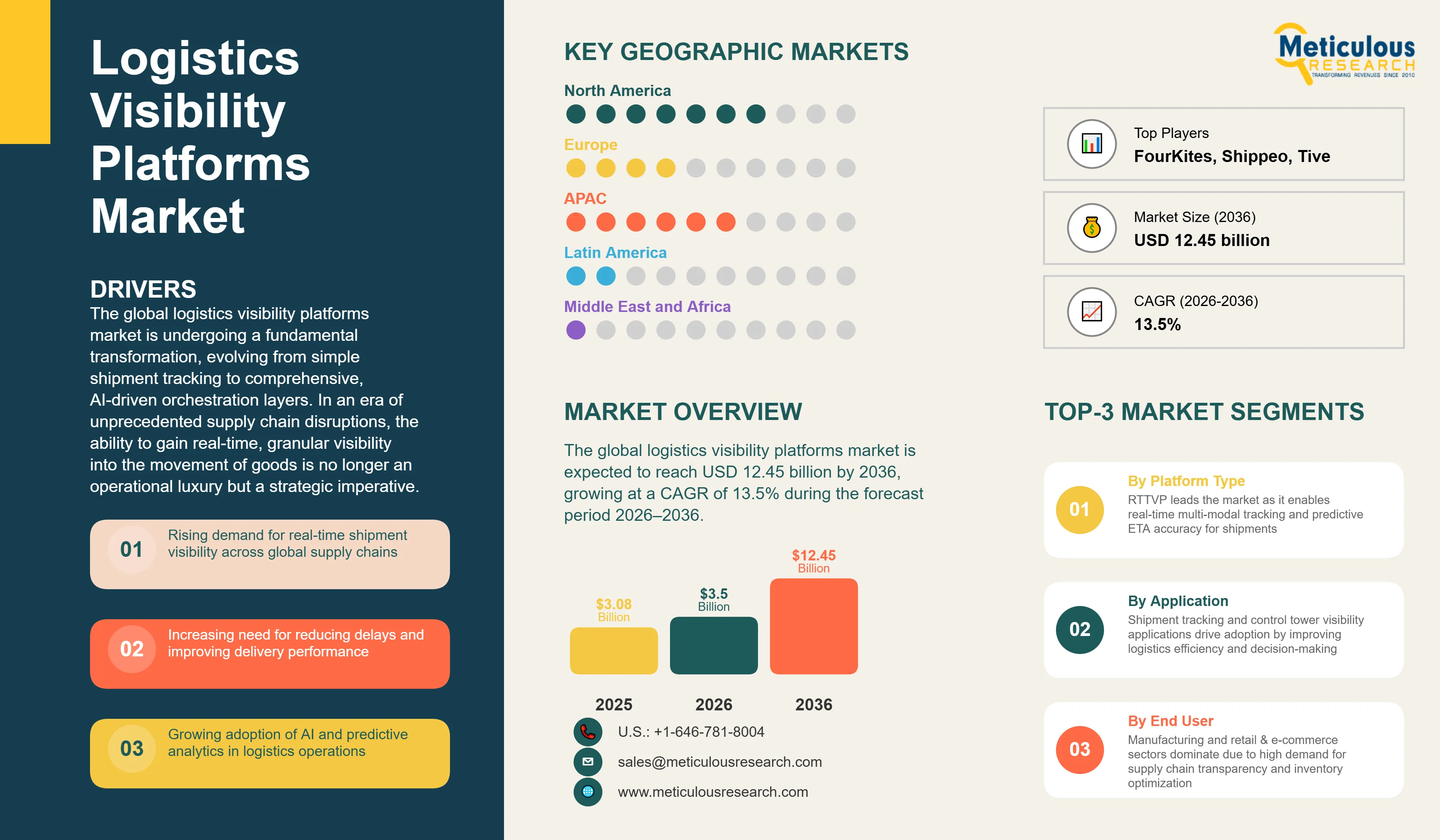

The global logistics visibility platforms market is estimated to be USD 3.50 billion in 2026. This market is expected to reach USD 12.45 billion by 2036, growing at a CAGR of 13.5% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

The global logistics visibility platforms market is undergoing a fundamental transformation, evolving from simple shipment tracking to comprehensive, AI-driven orchestration layers. In an era of unprecedented supply chain disruptions, the ability to gain real-time, granular visibility into the movement of goods is no longer an operational luxury but a strategic imperative. These platforms aggregate data from thousands of carriers, ELD/telematics devices, and port authorities to provide a single 'source of truth' for shippers, carriers, and logistics service providers (LSPs). According to the Digital Container Shipping Association (DCSA), the standardization of data exchange and the adoption of cloud-native visibility platforms are essential for reducing port congestion and improving equipment turnaround times. As logistics networks become increasingly intermodal and complex, these platforms enable stakeholders to move beyond reactive fire-fighting toward proactive risk management, predictive ETA accuracy, and autonomous supply chain orchestration.

Drivers: Eliminating Supply Chain 'Black Holes' and Enhancing Customer Experience

The growth of the global logistics visibility platforms market is propelled by the urgent need for end-to-end transparency across fragmented transport networks and the rising consumer expectation for real-time delivery updates. Shippers are increasingly prioritizing platforms that can provide seamless visibility across all modes of transport—road, ocean, air, and rail—to optimize inventory levels and reduce operational costs associated with delays and manual tracking.

Intensifying Demand for Real-Time Multi-Modal Shipment Transparency

In a globalized economy, shipments often traverse multiple borders and transport modes, creating significant 'visibility gaps' at port terminals and transshipment hubs. Logistics visibility platforms eliminate these black holes by providing a unified view of the shipment's journey. This transparency is critical for industries with high-value or time-sensitive cargo, such as pharmaceuticals and automotive manufacturing, where a lack of visibility can lead to production halts or product spoilage. The ability to receive real-time alerts on delays or deviations allows logistics managers to take proactive corrective actions, driving widespread adoption of these platforms.

Rising Consumer Expectations for 'Amazon-Like' Delivery Visibility

The 'Amazon Effect' has fundamentally altered customer expectations in both B2C and B2B sectors. Customers now demand precise, real-time information on their order status and exact delivery times. For retailers and e-commerce companies, providing this level of visibility is essential for maintaining customer loyalty and reducing the volume of 'where is my order' (WISMO) inquiries. Visibility platforms enable companies to offer branded tracking portals and automated notifications, enhancing the overall customer experience and providing a significant competitive advantage in a crowded market.

Need for Inventory Optimization and Reduction in Safety Stock

High-fidelity logistics visibility allows companies to transition from 'just-in-case' to 'just-in-time' inventory models. By having a precise understanding of when shipments will arrive, manufacturers and retailers can reduce their reliance on safety stock, thereby freeing up working capital and reducing warehousing costs. Visibility platforms provide the data necessary to identify bottlenecks in the supply chain and optimize transit times, leading to more efficient resource allocation and improved financial performance. This economic incentive is a powerful driver for the adoption of advanced visibility solutions.

Restraints: Overcoming Data Fragmentation and Integration Complexities

Despite the clear value proposition, the market faces significant challenges related to the fragmentation of data across thousands of small carriers and the technical complexities of integrating visibility platforms with legacy Enterprise Resource Planning (ERP) and Transportation Management Systems (TMS).

Fragmented Carrier Landscape and Data Quality Inconsistencies

Achieving 100% visibility requires the active participation of a vast and highly fragmented network of carriers, many of whom lack the technical infrastructure to provide real-time data. Data quality remains a persistent issue, with inconsistencies in tracking frequency, location accuracy, and event reporting. For visibility platforms, the ongoing challenge of onboarding small-to-medium-sized carriers and ensuring a standardized, high-quality data stream is a significant barrier to achieving the 'perfect' visibility that shippers demand.

High Complexity and Cost of Integration with Legacy Systems

Logistics visibility platforms must seamlessly integrate with a company's existing TMS, ERP, and WMS systems to provide meaningful insights. For large enterprises with complex, legacy IT architectures, this integration process can be time-consuming, expensive, and technically challenging. The need for custom APIs, data mapping, and cross-functional alignment often leads to prolonged implementation cycles and higher total cost of ownership (TCO), which can restrain the pace of adoption, particularly among mid-market firms with limited IT resources.

Opportunities: Harnessing AI for Self-Healing and Prescriptive Supply Chains

The next frontier for logistics visibility platforms is the move from descriptive to prescriptive and autonomous analytics. By leveraging Artificial Intelligence (AI) and Machine Learning (ML), these platforms can not only identify disruptions but also recommend and eventually execute the best course of action to mitigate them.

AI-Driven Prescriptive Analytics for Autonomous Exception Management

The massive datasets aggregated by visibility platforms provide a rich foundation for AI models to move beyond simple ETA predictions. Future platforms will offer 'prescriptive' insights, suggesting optimal rerouting options or alternative carriers in real-time when a disruption occurs. The development of 'self-healing' supply chains, where the platform can autonomously re-book freight or adjust inventory levels based on predicted delays represents a massive growth opportunity. Vendors that can successfully integrate these advanced agentic AI capabilities will lead the next wave of market expansion.

Expansion into Sustainability and Scope 3 Emissions Tracking

As global sustainability regulations tighten, companies are increasingly required to report on their Scope 3 carbon emissions. Logistics visibility platforms are uniquely positioned to provide this data by calculating the carbon footprint of every shipment based on actual transit data, mode of transport, and carrier efficiency. Integrating robust sustainability reporting and carbon offset modules into visibility platforms offers a significant opportunity to address the growing demand for green logistics and help companies meet their ESG (Environmental, Social, and Governance) goals.

Convergence of Visibility and Execution within Unified Platforms

A major trend in 2026 is the blurring of lines between visibility platforms and execution systems (TMS). Shippers are increasingly seeking unified platforms that allow them to not only track shipments but also book freight, manage payments, and handle exceptions within a single interface. This convergence simplifies the user experience, reduces data silos, and enables faster decision-making. Leading visibility providers are rapidly expanding their capabilities through acquisitions and partnerships to offer more holistic supply chain execution and visibility suites.

Increased Focus on Granular SKU-Level and Order-Level Visibility

The industry is moving beyond 'container-level' visibility toward more granular 'order-level' and 'SKU-level' tracking. Shippers now want to know exactly which orders are in a specific container and their real-time status relative to customer promise dates. This granular visibility requires deep integration with Warehouse Management Systems (WMS) and Order Management Systems (OMS). This trend is particularly strong in the retail and high-tech sectors, where understanding the impact of transit delays on specific customer orders is critical for proactive service management.

Analysis by Deployment Mode

Based on deployment mode, the cloud-based segment is expected to hold the largest share of the global logistics visibility platforms market in 2026. This dominance is driven by the cloud's inherent advantages in scalability, cost-effectiveness, and ease of cross-enterprise collaboration. Cloud-native platforms allow for the seamless aggregation of data from a vast, global network of carriers and data providers without the need for expensive on-premise infrastructure. Furthermore, the cloud-based segment is projected to register the highest CAGR during the forecast period. The continuous push for digital transformation and the increasing preference for SaaS (Software-as-a-Service) models, which offer lower upfront costs and faster time-to-value, are accelerating the shift away from legacy on-premise solutions. The ability of cloud platforms to rapidly deploy AI updates and integrate with other cloud-native supply chain tools makes them the primary engine of market growth.

Analysis by Platform Type

By platform type, thereal-time transportation visibility platforms (RTTVP) segment is expected to hold the largest share in 2026. This leadership is rooted in the immediate and critical need for shippers and carriers to eliminate 'black holes' in their transport networks. RTTVPs provide the foundational 'dot-on-a-map' visibility and predictive ETAs that are essential for daily logistics operations and customer service. However, the end-to-end supply chain visibility (SCV) platforms segment is projected to grow at the fastest CAGR during the forecast period. As companies mature in their visibility journey, their focus is expanding beyond transportation to include visibility into inventory, orders, and manufacturing status. The move toward 'Control Towers' that offer a holistic, cross-functional view of the entire supply chain, enabling more strategic decision-making and prescriptive analytics, is driving the highest growth in this segment.

Analysis by End User

By end user, the manufacturing segment is expected to hold the largest share in 2026. Manufacturers, particularly in the automotive, industrial, and aerospace sectors, operate highly synchronized, global supply chains that rely on just-in-time (JIT) delivery. Any disruption or lack of visibility into the arrival of critical components can lead to expensive production halts and inventory imbalances, making advanced visibility platforms a non-negotiable requirement for operational resilience. However, the retail & e-commerce segment is projected to register the highest CAGR during the forecast period. The 'Amazon Effect' has made real-time tracking a baseline consumer expectation. Retailers are investing aggressively in visibility to manage complex omnichannel fulfillment, improve last-mile delivery performance, and reduce the significant costs associated with customer service inquiries regarding order status. The need to optimize inventory across stores, warehouses, and transit to meet rapid delivery promises is a major driver for this high-growth segment.

Largest Share: North America

North America is expected to dominate the global logistics visibility platforms market in 2026. This leading position is primarily attributed to the region's mature logistics technology ecosystem, high adoption of cloud computing, and the presence of major global retailers and 3PLs that are early adopters of supply chain innovation. The region also serves as the headquarters for many of the world's leading visibility platform providers, fostering a highly competitive and innovative environment. According to the Council of Supply Chain Management Professionals (CSCMP), North American firms lead in logistics IT spending, with a strong focus on enhancing freight visibility to mitigate labor shortages and capacity constraints. The key companies operating in the North America market are project44, FourKites, Descartes Systems Group, Tive, and Roambee Corporation.

Fastest Growing: Asia-Pacific

The Asia-Pacific region is projected to witness the fastest growth in the global logistics visibility platforms market, with a CAGR of 15.8% during the forecast period. This rapid expansion is fueled by the massive digital transformation of logistics sectors in China, India, and Southeast Asia, coupled with the region's role as the world's primary manufacturing hub. Massive investments in 'Smart Port' and 'Smart Airport' initiatives, particularly in China and Singapore, are creating a robust foundation for regional visibility ecosystems. Furthermore, the booming e-commerce sector in India and China is pushing retailers and logistics providers to adopt advanced tracking solutions to meet the demands of a growing middle-class population. The key companies operating in the Asia Pacific market are FarEye, various regional technology integrators, and global players expanding their regional footprints.

The global logistics visibility platforms market is characterized by intense competition and rapid technological evolution. Leading players are aggressively expanding their carrier networks and investing heavily in AI and machine learning to improve ETA accuracy and prescriptive analytics. The market is also seeing significant consolidation as larger visibility providers acquire niche players to expand their multi-modal capabilities (e.g., project44's acquisition of Ocean Insights). Strategic partnerships with TMS and ERP vendors are a key competitive strategy to ensure seamless data integration for end-users. Furthermore, there is a growing focus on 'agentic AI' systems that can not only identify disruptions but also recommend rerouting options, moving the industry closer to the vision of a self-healing, autonomous supply chain.

project44 (US), FourKites (US), Shippeo (France), Descartes Systems Group (Canada), Tive (US), Roambee Corporation (US), FarEye (India), Overhaul (US), Vizion (US), Terminal49 (US), Logixboard (US), Freightos (Israel), BuyCo (France), Ocean Insights (part of project44) (Germany), MarineTraffic (part of Kpler) (Greece), Searoutes (France), Everstream Analytics (US), Resilinc (US), Windward (Israel), Arviem AG (Switzerland).

The global Logistics Visibility Platforms market is estimated to be approximately USD 3.50 billion in 2026, with a projected growth to USD 12.45 billion by 2036, at a CAGR of 13.5%.

Key drivers include the intensifying demand for real-time multi-modal shipment transparency and rising consumer expectations for 'Amazon-like' delivery visibility.

Restraints include the fragmented carrier landscape and data quality inconsistencies, along with the high complexity of integration with legacy ERP and TMS systems.

Opportunities lie in the development of AI-driven prescriptive analytics for autonomous exception management and expansion into Scope 3 sustainability reporting.

The cloud-based segment is expected to hold the largest share due to its scalability and ease of cross-enterprise integration.

End-to-end supply chain visibility (SCV) platforms are expected to grow at the fastest CAGR as companies seek holistic 'Control Tower' solutions.

The manufacturing segment is expected to hold the largest share, necessitated by the requirements of just-in-time (JIT) logistics and inventory optimization.

North America is expected to dominate the market, driven by its mature logistics technology ecosystem and high adoption of cloud-based solutions.

Asia Pacific is projected to witness the fastest growth, fueled by rapid digital transformation and manufacturing expansion in China and India.

Key trends include the convergence of visibility and execution within unified platforms and the shift toward granular SKU-level and order-level visibility.

1. Introduction

1.1. Market Definition

1.2. Market Scope

1.3. Currency & Limitations

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Sources

2.2.1. Secondary Research

2.2.2. Primary Research

2.3. Market Size Estimation

2.3.1. Bottom-up Approach

2.3.2. Top-down Approach

2.4. Assumptions

3. Executive Summary

3.1. Market Snapshot

3.2. Segmental Summary

3.3. Regional Summary

3.4. Competitive Snapshot

4. Market Overview

4.1. Introduction

4.2. Market Dynamics

4.2.1. Drivers

4.2.1.1. Intensifying Demand for Real-Time Multi-Modal Shipment Transparency

4.2.1.2. Rising Consumer Expectations for 'Amazon-Like' Delivery Visibility

4.2.1.3. Need for Inventory Optimization and Reduction in Safety Stock

4.2.2. Restraints

4.2.2.1. Fragmented Carrier Landscape and Data Quality Inconsistencies

4.2.2.2. High Complexity and Cost of Integration with Legacy Systems

4.2.3. Opportunities

4.2.3.1. AI-Driven Prescriptive Analytics for Autonomous Exception Management

4.2.3.2. Expansion into Sustainability and Scope 3 Emissions Tracking

4.2.4. Trends

4.2.4.1. Convergence of Visibility and Execution within Unified Platforms

4.2.4.2. Increased Focus on Granular SKU-Level and Order-Level Visibility

4.3. Porter's Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Logistics Visibility Platforms Market, by Deployment Mode

5.1. Cloud-based

5.2. On-premise

6. Global Logistics Visibility Platforms Market, by Platform Type

6.1. Real-Time Transportation Visibility Platforms (RTTVP)

6.2. End-to-End Supply Chain Visibility (SCV) Platforms

7. Global Logistics Visibility Platforms Market, by End User

7.1. Manufacturing

7.2. Retail & E-commerce

7.3. Food & Beverage

7.4. Pharmaceutical & Healthcare

7.5. Logistics & Transportation (LSPs)

7.6. Others

8. Global Logistics Visibility Platforms Market, by Geography

8.1. North America

8.1.1. U.S.

8.1.2. Canada

8.2. Europe

8.2.1. Germany

8.2.2. U.K.

8.2.3. France

8.2.4. Italy

8.2.5. Spain

8.2.6. Rest of Europe

8.3. Asia Pacific

8.3.1. China

8.3.2. Japan

8.3.3. India

8.3.4. South Korea

8.3.5. Rest of Asia Pacific

8.4. Latin America

8.4.1. Brazil

8.4.2. Argentina

8.4.3. Mexico

8.4.4. Rest of Latin America

8.5. Middle East & Africa

8.5.1. UAE

8.5.2. Saudi Arabia

8.5.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Overview

9.2. Key Growth Strategies

9.3. Competitive Benchmarking

9.4. Competitive Dashboard

9.4.1. Industry Leaders

9.4.2. Market Differentiators

9.4.3. Vanguards

9.4.4. Emerging Companies

9.5. Market Share/Ranking Analysis

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. project44

10.2. FourKites

10.3. Shippeo

10.4. Descartes Systems Group

10.5. Tive

10.6. Roambee Corporation

10.7. FarEye

10.8. Overhaul

10.9. Vizion

10.10. Terminal49

10.11. Logixboard

10.12. Freightos

10.13. BuyCo

10.14. Ocean Insights (part of project44)

10.15. MarineTraffic (part of Kpler)

10.16. Searoutes

10.17. Everstream Analytics

10.18. Resilinc

10.19. Windward

10.20. Arviem AG

11. Appendix

11.1. References

11.2. Disclaimer

12. Key Questions Answered

Published Date: Apr-2026

Published Date: Feb-2026

Published Date: May-2025

Published Date: Jun-2026

Published Date: Jun-2026

Subscribe to get the latest industry updates