Resources

About Us

Green Logistics Market Size, Share & Trends Analysis by Solution Type (Green Transportation, Green Warehousing), Mode of Transport, Fuel Type (Electric, Hydrogen), Application, and End User - Global Opportunity Analysis & Industry Forecast (2026-2036)

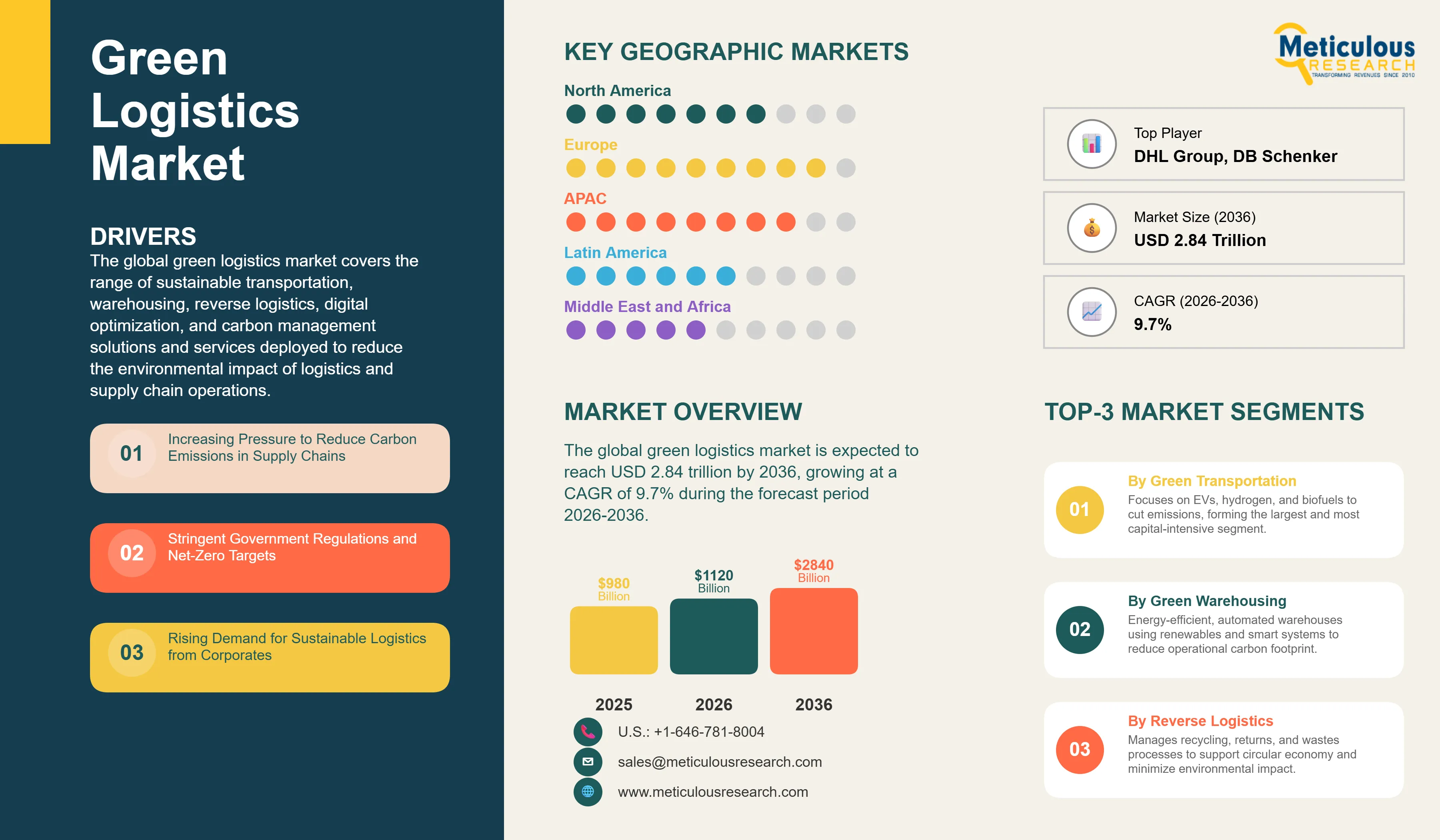

Report ID: MRAUTO - 1041893 Pages: 315 Apr-2026 Formats*: PDF Category: Automotive and Transportation Delivery: 24 to 72 Hours Download Free Sample ReportThe global green logistics market was valued at USD 0.98 trillion in 2025. This market is expected to reach USD 2.84 trillion by 2036 from an estimated USD 1.12 trillion in 2026, growing at a CAGR of 9.7% during the forecast period 2026-2036.

Click here to: Get Free Sample Pages of this Report

Click here to: Get Free Sample Pages of this Report

The global green logistics market covers the range of sustainable transportation, warehousing, reverse logistics, digital optimization, and carbon management solutions and services deployed to reduce the environmental impact of logistics and supply chain operations. This encompasses electric, hydrogen, and biofuel-powered freight transport across road, rail, air, and maritime modes, energy-efficient and renewable energy-powered warehousing facilities, AI and IoT-enabled route optimization and fleet management platforms that reduce fuel consumption and emissions, reverse logistics and circular economy programs, and carbon tracking and offsetting services that enable shippers and logistics operators to measure, manage, and reduce their supply chain emissions footprint.

The growth of the global green logistics market is primarily driven by the intensifying corporate and regulatory pressure to decarbonize supply chains as climate commitments translate into binding emission targets and mandatory sustainability reporting obligations. The EU's Corporate Sustainability Reporting Directive requires large European companies and their supply chain partners to disclose detailed Scope 1, 2, and 3 greenhouse gas emissions from 2025 onward, directly compelling shippers and their logistics providers to implement green logistics solutions capable of generating the emission measurement and reduction data required for compliance. The rapid improvement in the commercial competitiveness of electric commercial vehicles, with total cost of ownership parity with diesel counterparts approaching in urban delivery applications as battery costs decline and charging infrastructure expands, is accelerating fleet electrification investment beyond regulatory motivation into financially compelling territory for logistics operators managing large urban delivery fleets.

Two significant opportunities are shaping the market's long-term trajectory. The electrification of logistics fleets at scale, enabled by the rapid expansion of charging infrastructure networks, the improving range and payload capacity of battery electric trucks, and the growing availability of green electricity contracts that allow fleet operators to achieve near-zero operational emissions, represents the largest near-term capital deployment opportunity within the green logistics market. The adoption of AI-based route optimization and fleet management platforms represents a highly accessible and immediately return-generating opportunity that enables logistics operators to reduce fuel consumption by 10 to 20% without fleet replacement investment, generating rapid payback periods that are driving fast adoption across logistics operators of all sizes globally.

|

Parameters |

Details |

|

Market Size by 2036 |

USD 2.84 Trillion |

|

Market Size in 2026 |

USD 1.12 Trillion |

|

Market Size in 2025 |

USD 0.98 Trillion |

|

Revenue Growth Rate (2026-2036) |

CAGR of 9.7% |

|

Dominating Solution Type |

Green Transportation |

|

Fastest Growing Solution Type |

Digital and Optimization Solutions |

|

Dominating Mode of Transport |

Road Transport |

|

Fastest Growing Mode of Transport |

Maritime Shipping |

|

Dominating Fuel Type |

Electric |

|

Fastest Growing Fuel Type |

Hydrogen |

|

Dominating Application |

Retail & E-commerce |

|

Fastest Growing Application |

Pharmaceuticals |

|

Dominating End User |

Third-Party Logistics Providers (3PLs) |

|

Fastest Growing End User |

E-commerce Companies |

|

Dominating Deployment Model |

Outsourced Logistics |

|

Fastest Growing Deployment Model |

In-House Logistics |

|

Dominating Geography |

Europe |

|

Fastest Growing Geography |

Asia-Pacific |

|

Base Year |

2025 |

|

Forecast Period |

2026 to 2036 |

Electrification of Road Freight Fleets at Commercial Scale

The accelerating commercial deployment of battery electric trucks and vans across urban delivery and short-haul freight operations represents the most commercially active transformation underway in the green logistics market. The operational economics of electric last-mile delivery vehicles have reached cost parity with diesel equivalents in several major markets driven by lower energy and maintenance costs offsetting higher vehicle purchase prices, creating a financially self-sustaining adoption dynamic that is driving fleet electrification programs beyond early-mover logistics operators into mainstream adoption across the industry. DHL has committed to electrifying 60% of its global first and last-mile deliveries by 2030, UPS is deploying over 10,000 electric delivery vehicles in the United States and Europe, and Amazon has contracted 100,000 electric delivery vans from Rivian representing the largest electric commercial vehicle order in history.

The heavy truck segment is following the light commercial vehicle electrification trajectory with a lag driven by the greater energy storage requirements of long-haul freight. Tesla's Semi, Freightliner's eCascadia, Volvo FH Electric, and DAF XF Electric are entering commercial deployment in regional freight applications where daily range requirements are compatible with current battery technology. Government incentive programs including the U.S. EPA's Clean Trucks Plan, the EU's CO2 standards for heavy-duty vehicles mandating 90% emission reduction for new trucks by 2040, and national zero-emission truck incentive programs in Norway, the Netherlands, Germany, and California are accelerating the commercial economics of electric freight and expanding the addressable range of fleet electrification programs.

Rise of AI-Powered Route Optimization and Carbon Tracking

The adoption of artificial intelligence and machine learning platforms for logistics route optimization, load planning, fleet management, and carbon emission tracking represents a high-growth technology trend that is delivering immediate sustainability and cost efficiency gains for logistics operators without requiring fleet replacement capital investment. AI route optimization platforms including those offered by Oracle Logistics, SAP Transportation Management, project44, FourKites, and specialized green logistics software providers can reduce fuel consumption by 10 to 25% through dynamic route planning that minimizes empty running, optimizes multi-stop delivery sequencing, and adjusts routing in real time based on traffic, weather, and vehicle load conditions. The direct cost saving from fuel reduction creates compelling financial justification for AI logistics platform adoption independent of sustainability motivations, making this solution category commercially accessible to a broader logistics operator base than capital-intensive fleet electrification programs.

Carbon tracking and scope 3 emission reporting software is experiencing rapid adoption growth driven by the EU CSRD and SEC climate disclosure rule creating mandatory requirements for large companies to report supply chain emissions with increasing precision and external verification quality. Platforms including Pledge, Lune, Bearing, and the sustainability tracking modules embedded within major logistics management systems are enabling shippers to calculate and report the carbon footprint of individual shipments and logistics programs with freight mode, route, and vehicle-specific emission factor granularity. This data infrastructure is becoming a competitive requirement for logistics service providers seeking to retain corporate shippers who must report supply chain emissions and will increasingly direct freight toward providers with the lowest measurable emission intensity.

Hydrogen and Alternative Fuels Gaining Ground in Heavy Freight

The progressive commercialization of hydrogen fuel cell trucks and the expanding adoption of LNG, biomethane, and methanol as transition fuels in heavy freight applications where battery electric vehicles currently face technical limitations is creating important new segments within the green logistics fuel transition. Hydrogen fuel cell trucks offer compelling operational advantages for long-haul freight in terms of range exceeding 800 kilometers on a single fill and rapid refueling times comparable to diesel, addressing the range and payload constraints that limit battery electric truck adoption in long-distance freight corridors. Hyundai's XCIENT Fuel Cell trucks deployed in Switzerland and California, Daimler Truck's collaboration with Volvo on hydrogen fuel cell heavy trucks through the Cellcentric joint venture, and Nikola's commercial hydrogen truck programs are establishing the technology's commercial viability in premium green freight applications.

In maritime shipping, the adoption of LNG as a transition fuel and the accelerating investment in methanol-fueled and ammonia-fueled vessel newbuilds is driving significant decarbonization progress in the highest carbon-intensity transport mode. Maersk's fleet of methanol dual-fuel container ships represents the most commercially visible example of maritime fuel transition at scale, and the IMO's Carbon Intensity Indicator regulations requiring progressive improvement in vessel carbon intensity are creating compliance-driven demand for alternative fuel adoption across the global shipping fleet. Sustainable aviation fuel adoption in air freight is advancing through voluntary corporate sustainability commitments and regulatory mandates including the EU's ReFuelEU Aviation regulation requiring blending of SAF in aviation fuel supplied at EU airports, creating growing demand for SAF-based green air freight services from sustainability-committed shipper customers.

Increasing Pressure to Reduce Carbon Emissions in Supply Chains

The intensifying pressure on corporations to reduce Scope 3 supply chain emissions in response to investor ESG expectations, customer sustainability requirements, and the emerging mandatory climate disclosure regulations being implemented across major economies represents the primary structural demand driver of the green logistics market. Supply chain and logistics activities typically constitute 40 to 70% of corporate Scope 3 emissions for manufacturing and retail companies, making logistics decarbonization a critical component of corporate net-zero transition programs. The Science Based Targets initiative requires companies with validated net-zero commitments to address supply chain emissions in their decarbonization roadmaps, and the growing number of global corporations with validated SBTi net-zero targets is translating directly into procurement pressure on logistics service providers to demonstrate measurable emission reduction performance. This creates a cascading demand effect through the logistics value chain as major shippers including Apple, Amazon, Walmart, and Unilever impose green logistics requirements on their carrier and 3PL relationships.

Stringent Government Regulations and Net-Zero Targets

The legislative framework being built across the European Union, United States, United Kingdom, Japan, South Korea, and China to mandate transport sector decarbonization is creating binding compliance drivers for green logistics adoption that operate independently of voluntary corporate sustainability motivations. The EU's revised CO2 standards for heavy-duty vehicles mandate 45% emission reduction for new trucks sold from 2030 and 90% reduction from 2040 relative to 2019 baselines, effectively phasing out diesel heavy trucks from new registrations on a defined regulatory timeline. The EU Emissions Trading System extension to road transport from 2027 will put a carbon price on transport fuel consumption that increases the operating cost of conventional diesel logistics relative to electric and alternative fuel alternatives. The IMO's 2050 net-zero target for international shipping and the Carbon Intensity Indicator regulations are driving compliance investment across the global shipping industry. These regulatory frameworks create mandatory transition timelines that translate directly into green logistics technology and service procurement demand regardless of upfront cost premiums.

Electrification of Logistics Fleets

The large-scale electrification of commercial vehicle logistics fleets represents the largest single opportunity within the green logistics market, encompassing the procurement of electric delivery vans, medium-duty electric trucks, and heavy-duty electric and fuel cell trucks together with the charging infrastructure, energy management systems, and fleet operations software required to support electrified fleet operations. The total addressable market for logistics fleet electrification globally is estimated in the hundreds of billions of dollars as the hundreds of millions of commercial vehicles operating in logistics applications globally transition to zero-emission alternatives over the coming decade and a half. Battery electric vehicle manufacturers including Tesla, Rivian, BYD, Daimler Truck, Volvo, MAN, Stellantis Pro One, and Ford Pro are competing to supply the electric commercial vehicles and associated software platforms that logistics operators require for fleet transition programs, while energy companies, utilities, and charging network operators are investing in the charging infrastructure and green electricity supply that makes fleet electrification operationally viable at scale.

AI-Based Route Optimization and Efficiency

The deployment of artificial intelligence for logistics network optimization represents a high-return, rapidly scalable opportunity for logistics operators to reduce fuel consumption, carbon emissions, and operating costs simultaneously without requiring the upfront capital investment of fleet electrification programs. AI route optimization platforms that incorporate real-time traffic data, vehicle telematics, weather information, and customer time window constraints into dynamic delivery route planning can reduce total vehicle kilometers traveled by 10 to 20% relative to conventional route planning methodologies, generating proportional reductions in fuel consumption and carbon emissions. The scalability of software-based optimization solutions across existing conventional and green logistics fleets alike makes AI optimization a commercially attractive green logistics investment for operators at all stages of fleet electrification transition, and the improving quality of AI-generated emission reporting data from optimization platforms provides the shipment-level carbon footprint data that corporate sustainability reporting obligations increasingly require from logistics service providers.

By Solution Type: In 2026, Green Transportation to Dominate

Based on solution type, the global green logistics market is segmented into green transportation, green warehousing, reverse logistics, digital and optimization solutions, and carbon management and offsetting services. In 2026, the green transportation segment is expected to account for the largest share of the global green logistics market. The large share of this segment is attributed to transportation's dominant position as the largest source of logistics-related greenhouse gas emissions and therefore the primary focus of regulatory mandates, corporate sustainability investment, and capital deployment across the green logistics landscape. Electric vehicle procurement programs, hydrogen truck pilots, biofuel transition investments, and sustainable aviation and maritime fuel adoption collectively represent the largest component of green logistics capital expenditure, with fleet electrification programs at DHL, UPS, Amazon, Maersk, and major freight carriers generating very large annual investment flows that dominate total green logistics market value.

However, the digital and optimization solutions segment is poised to register the highest CAGR during the forecast period. The high growth of this segment is attributed to the accelerating enterprise adoption of AI route optimization, fleet management, and carbon tracking platforms that deliver immediate and measurable emission and cost reductions at low implementation barriers, the mandatory carbon reporting requirements under EU CSRD and equivalent frameworks creating non-discretionary demand for carbon tracking software across logistics operators and their shipper customers, and the expanding SaaS delivery model of green logistics software that enables rapid scaling across logistics operator customer bases of all sizes.

By Mode of Transport: In 2026, Road Transport to Hold the Largest Share

Based on mode of transport, the global green logistics market is segmented into road transport, rail transport, air freight, and maritime shipping. In 2026, the road transport segment is expected to account for the largest share of the global green logistics market. This dominance reflects road transport's position as the single largest freight mode by volume and value in virtually all regional logistics markets, the concentration of fleet electrification and alternative fuel investment in road transport where the technology maturity of electric vehicles is most advanced, and the direct regulatory pressure on road freight emissions from truck CO2 standards and urban low-emission zone policies that is driving the largest concentration of green logistics regulatory compliance investment.

However, the maritime shipping segment is projected to register the highest CAGR during the forecast period. This growth is driven by the IMO's 2050 net-zero shipping target and the Carbon Intensity Indicator regulations creating binding compliance investment requirements across the global shipping fleet, the very high absolute carbon intensity of ocean shipping that makes maritime decarbonization programs high-priority Scope 3 emission reduction opportunities for global shippers with significant ocean freight volumes, and the large capital investment programs underway at Maersk, CMA CGM, Hapag-Lloyd, and MSC in alternative-fuel vessel newbuilds and fuel transition programs that represent major green logistics market value creation.

By Fuel Type: In 2026, Electric to Hold the Largest Share

Based on fuel type, the global green logistics market is segmented into electric, hydrogen, biofuels, LNG/CNG, and sustainable aviation fuel. In 2026, the electric segment is expected to account for the largest share of the global green logistics market, driven by the commercial maturity and rapid adoption of battery electric vehicles in last-mile and urban delivery logistics, the availability of a broad range of commercially deployed electric van and light commercial vehicle models from multiple manufacturers, and the strongest government incentive support and charging infrastructure investment concentration in battery electric vehicle technology among all green fuel alternatives. The active electric fleet programs of DHL, UPS, FedEx, Amazon, and major urban delivery logistics operators across Europe, North America, and China are generating the largest fuel type segment revenue within the green logistics market.

However, the hydrogen segment is projected to register the highest CAGR during the forecast period. This growth is driven by the advancing commercialization of hydrogen fuel cell heavy trucks for long-haul freight applications, national hydrogen strategy investments in refueling infrastructure in Europe, Japan, South Korea, and the United States, and the maritime sector's growing adoption of hydrogen as a pathway fuel for deep-sea shipping decarbonization where battery electric propulsion is not technically feasible at commercial scale.

By Application: In 2026, Retail & E-commerce to Hold the Largest Share

Based on application, the global green logistics market is segmented into retail and e-commerce, manufacturing, automotive, food and beverage, pharmaceuticals, chemicals, and others. In 2026, the retail and e-commerce segment is expected to account for the largest share of the global green logistics market. This dominance reflects the e-commerce sector's generation of the highest volumes of urban last-mile delivery operations that are most immediately amenable to electric vehicle fleet electrification, the intense consumer-facing sustainability pressure on e-commerce platforms that is driving the largest green logistics capital investment programs among any shipper category, and the strategic green fleet investments of Amazon, Zalando, ASOS, and major retail logistics networks targeting net-zero delivery operations.

However, the pharmaceuticals segment is projected to register the highest CAGR during the forecast period. This growth is driven by the pharmaceutical industry's stringent ESG reporting requirements and investor sustainability expectations that are compelling pharma logistics operators to invest in cold chain decarbonization, the premium logistics service tier in which pharmaceutical shipments operate that supports the pricing of green logistics service premiums, and the growing complexity of pharmaceutical supply chains encompassing temperature-controlled biologics and personalized medicine logistics that are requiring purpose-built green cold chain solutions.

By End User: In 2026, Third-Party Logistics Providers to Hold the Largest Share

Based on end user, the global green logistics market is segmented into third-party logistics providers, freight forwarders, e-commerce companies, and industrial enterprises. In 2026, the third-party logistics providers segment is expected to account for the largest share of the global green logistics market. Third-party logistics providers represent the primary commercial deployers of green logistics solutions, as their business model of operating transportation and warehousing assets on behalf of multiple shipper clients creates both the largest aggregate fleet and facility emission footprints requiring decarbonization and the most direct exposure to shipper sustainability procurement requirements that mandate green logistics performance. DHL Group's GoGreen Plus program, UPS Carbon Neutral shipping service, FedEx's fleet electrification program, Kuehne+Nagel's NetZero carbon neutral logistics offering, and DB Schenker's electrification and alternative fuel programs collectively represent the largest green logistics investment programs in the industry.

However, the e-commerce companies segment is projected to register the highest CAGR during the forecast period. This growth is driven by the extraordinary capital investment programs of Amazon, JD.com, Flipkart, and Coupang in proprietary electric delivery fleet deployment and sustainable logistics infrastructure, the intense consumer and regulatory scrutiny of e-commerce delivery sustainability that is compelling platforms to invest in green logistics at a pace exceeding the 3PL sector, and the direct control that e-commerce companies' proprietary last-mile logistics operations provide over fleet electrification programs that enables faster transition timelines than coordinating green logistics transitions across third-party carrier networks.

By Deployment Model: In 2026, Outsourced Logistics to Hold the Largest Share

Based on deployment model, the global green logistics market is segmented into in-house logistics and outsourced logistics. In 2026, the outsourced logistics segment is expected to account for the largest share of the global green logistics market. The dominant share of outsourced logistics reflects the broad industry practice of manufacturing, retail, and consumer goods companies contracting their transportation and warehousing operations to specialist logistics service providers, concentrating the majority of logistics asset ownership and operation and therefore the primary green logistics investment decision-making within the 3PL and freight carrier sector. The outsourced logistics model allows shippers to access green logistics services and carbon footprint reporting without direct capital investment in green fleet assets, purchasing sustainable logistics capacity as a service from providers who manage the green technology transition investment.

However, the in-house logistics segment is projected to register the highest CAGR during the forecast period. This growth is driven by the strategic insourcing of last-mile delivery operations by major e-commerce platforms seeking direct control over delivery sustainability performance and customer experience, the proprietary electric fleet programs of Amazon Logistics, JD Logistics, and Flipkart that are building large in-house green delivery operations, and the growing preference of sustainability-focused corporations for direct ownership of green logistics assets that enables more verifiable and credible sustainability reporting than purchased third-party green logistics services.

Green Logistics Market by Region: Europe Leading by Share, Asia-Pacific by Growth

Based on geography, the global green logistics market is segmented into Europe, North America, Asia-Pacific, Latin America, and the Middle East and Africa.

In 2026, Europe is expected to account for the largest share of the global green logistics market. The largest share of this region is mainly due to the EU's comprehensive and binding regulatory framework for logistics decarbonization, encompassing the revised CO2 standards for heavy-duty vehicles, the EU Emissions Trading System extension to road transport, the IMO carbon intensity regulations affecting European-registered shipping, and the Corporate Sustainability Reporting Directive creating mandatory supply chain emission reporting requirements that collectively constitute the world's most comprehensive and commercially consequential green logistics regulatory environment. Germany, the Netherlands, Sweden, Norway, and Belgium represent the most advanced European national green logistics markets, with the Netherlands' role as Europe's primary logistics gateway generating very high green freight investment concentration, Sweden and Norway's leading electric truck adoption rates supported by mature charging infrastructure and high carbon taxation, and Germany's large industrial freight market undergoing significant green fleet transition investment driven by strong corporate sustainability programs at BMW, Mercedes-Benz, Volkswagen, and major German logistics operators. DHL Group, DB Schenker, Kuehne+Nagel, and DSV, all with European headquarters and primary operations, are the most active investors in green logistics technology among global logistics companies, reinforcing Europe's market leadership position.

However, the Asia-Pacific green logistics market is expected to grow at the fastest CAGR during the forecast period. The region's rapid growth is driven by China's dominant and accelerating position in electric commercial vehicle production and deployment, with Chinese EV manufacturers including BYD, SAIC, and JAC producing the large majority of global electric trucks and vans and deploying them at scale in Chinese urban logistics operations, China's national carbon neutrality goals driving large-scale green logistics infrastructure investment, and the regulatory and market pressure compelling major Chinese e-commerce operators including JD.com, Cainiao, and SF Express to transition to electric last-mile delivery fleets. India's rapidly growing logistics sector is adopting electric three-wheelers and light commercial vehicles for last-mile delivery at scale, with Mahindra Electric, Tata Motors EV, and international EV brands deploying large urban electric delivery fleets. Japan and South Korea's advanced corporate sustainability programs and hydrogen infrastructure investment are creating important green logistics adoption centers, while Singapore and Australia are establishing themselves as Asia-Pacific green logistics innovation hubs with advanced sustainable port and aviation fuel programs.

North America represents the second-largest regional green logistics market, anchored by large fleet electrification programs at Amazon, UPS, FedEx, and the major U.S. trucking carriers, the EPA's Clean Trucks Plan emission standards driving commercial heavy truck decarbonization, and state-level zero-emission vehicle mandates in California, New York, and other leading states that are establishing binding electric truck adoption timelines. The U.S. Inflation Reduction Act's commercial vehicle tax credits and charging infrastructure grants are accelerating the economic case for electric fleet adoption across U.S. logistics operators of all sizes.

The global green logistics market is moderately consolidated among large integrated logistics service providers that are each deploying multi-billion dollar green transition programs, while remaining highly fragmented across the broader market of regional carriers, specialized green logistics technology providers, and emerging electric freight startups. Competition is focused on the scale and credibility of green fleet transition programs, the quality and granularity of carbon emission reporting capabilities, the geographic coverage of sustainable logistics networks, and the commercial packaging of green logistics services including carbon-neutral shipping options and shipper sustainability reporting tools.

DHL Group leads the green logistics market through its GoGreen Plus program offering insetting-based carbon-neutral shipping, its commitment to net-zero logistics by 2050 with 60% electric first and last-mile delivery by 2030, and the largest active green logistics fleet investment program among global logistics operators. Maersk is the leading actor in maritime green logistics through its methanol dual-fuel vessel fleet and its net-zero by 2040 commitment. UPS and FedEx are the leading North American green logistics operators through their respective electric vehicle programs and carbon-neutral shipping product suites. Kuehne+Nagel, DB Schenker, and DSV are advancing European green logistics programs with strong emission reporting capabilities and alternative fuel procurement frameworks for their road, sea, and air freight networks.

The report provides a comprehensive competitive analysis based on an extensive assessment of leading players' green program scale, technology adoption, geographic presence, and key strategic developments. Some of the key players operating in the global green logistics market include DHL Group (Germany), FedEx Corporation (U.S.), United Parcel Service Inc. (U.S.), A.P. Moller-Maersk A/S (Denmark), DB Schenker (Germany), Kuehne+Nagel International AG (Switzerland), DSV A/S (Denmark), XPO Logistics Inc. (U.S.), CEVA Logistics (France), CMA CGM Group (France), Nippon Express Co. Ltd. (Japan), Schneider National Inc. (U.S.), J.B. Hunt Transport Services Inc. (U.S.), Lineage Logistics (U.S.), and GEODIS (France), among others.

The global green logistics market is expected to reach USD 2.84 trillion by 2036 from an estimated USD 1.12 trillion in 2026, at a CAGR of 9.7% during the forecast period 2026-2036.

In 2026, the green transportation segment is expected to hold the largest share of the global green logistics market, driven by transportation's dominant position as the primary source of logistics carbon emissions and the corresponding concentration of regulatory mandates and capital investment in freight transport decarbonization.

The digital and optimization solutions segment is expected to register the highest CAGR during the forecast period 2026-2036, driven by the accelerating adoption of AI route optimization and carbon tracking platforms delivering immediate emission and cost reductions and the mandatory carbon reporting requirements under EU CSRD creating non-discretionary demand for carbon tracking software.

In 2026, the road transport segment is expected to hold the largest share of the global green logistics market, reflecting road freight's dominant position in logistics volume across all major markets and the concentration of fleet electrification investment and regulation in road transport.

In 2026, the retail and e-commerce segment is expected to hold the largest share of the global green logistics market, driven by e-commerce's generation of the highest urban last-mile delivery volumes and the largest green logistics capital investment programs among all shipper categories.

The growth of this market is primarily driven by the escalating corporate and regulatory pressure to decarbonize supply chains through binding sustainability reporting mandates, progressive transport emission standards, and corporate net-zero commitments that are translating into non-discretionary green logistics investment, and the improving commercial competitiveness of electric commercial vehicles reaching total cost of ownership parity with diesel equivalents in urban delivery applications as battery costs decline and charging infrastructure expands.

Key players are DHL Group (Germany), FedEx Corporation (U.S.), United Parcel Service Inc. (U.S.), A.P. Moller-Maersk A/S (Denmark), DB Schenker (Germany), Kuehne+Nagel International AG (Switzerland), DSV A/S (Denmark), XPO Logistics Inc. (U.S.), CEVA Logistics (France), CMA CGM Group (France), Nippon Express Co. Ltd. (Japan), Schneider National Inc. (U.S.), J.B. Hunt Transport Services Inc. (U.S.), Lineage Logistics (U.S.), and GEODIS (France), among others.

Asia-Pacific is expected to register the highest growth rate in the global green logistics market during the forecast period 2026-2036, driven by China's dominant electric commercial vehicle production and deployment at scale, India's rapidly growing electric last-mile logistics adoption, and the advancing green logistics programs of Japanese, South Korean, and Southeast Asian logistics operators and e-commerce companies.

Published Date: Feb-2026

Published Date: May-2025

Published Date: Jun-2026

Please enter your corporate email id here to view sample report.

Subscribe to get the latest industry updates