Resources

About Us

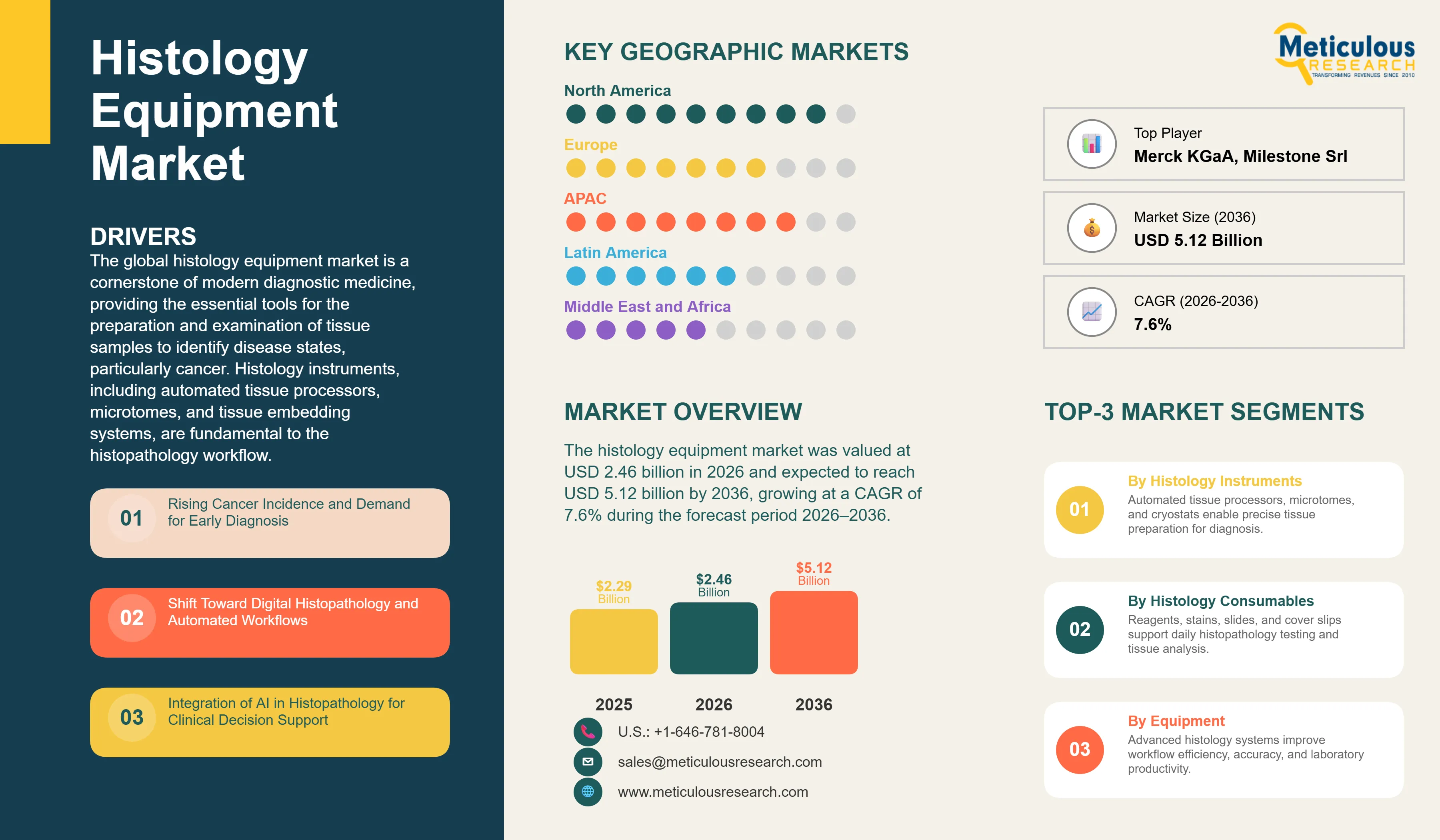

The global histology equipment market was valued at USD 2.46 billion in 2026. This market is expected to reach USD 5.12 billion by 2036, growing at a CAGR of 7.6% during the forecast period 2026–2036.

Click here to: Get Free Sample Pages of this Report

Market Overview: Advancing Cancer Diagnostics with Modern Histopathology Equipment

The global histology equipment market is a cornerstone of modern diagnostic medicine, providing the essential tools for the preparation and examination of tissue samples to identify disease states, particularly cancer. Histology instruments, including automated tissue processors, microtomes, and tissue embedding systems, are fundamental to the histopathology workflow. As of 2026, the market is undergoing a significant transformation, driven by the shift toward digital histopathology and the integration of AI in histopathology. According to the World Health Organization (WHO), the global cancer burden is projected to reach 28.4 million cases by 2040, a 47% increase from 2020. This escalating demand for diagnostic services is compelling pathology laboratories to invest in high-throughput histology laboratory equipment to improve operational efficiency and diagnostic accuracy.

The transition to digital pathology workflow is a defining characteristic of the current market landscape. By digitizing tissue slides, pathology laboratories can leverage advanced image analysis and remote consultation capabilities, significantly enhancing clinical productivity. Modern histology instruments are increasingly designed with integrated connectivity and automated features to support this digital transition. Furthermore, the rising adoption of precision medicine and the increasing complexity of biopsy samples are driving the demand for specialized histology equipment, such as high-precision cryostats and automated slide staining systems, which ensure the consistent quality of tissue sections for molecular analysis.

Drivers: Rising Cancer Incidence and the Shift Toward Digital Pathology Workflows

The primary driver for the histology equipment market is the global increase in cancer prevalence, which necessitates a higher volume of histopathology examinations. According to the American Cancer Society, over 2 million new cancer cases are expected to be diagnosed in the U.S. in 2026 alone. This surge in patient volume is driving the adoption of automated tissue processing and high-throughput histology instruments to manage the diagnostic workload. Furthermore, the shift toward digital histopathology is revolutionizing the field, as health systems seek to improve diagnostic turnaround times and facilitate remote pathology services. The integration of AI in histopathology is also a significant driver, providing pathologists with powerful tools for automated feature recognition and clinical decision support, thereby enhancing the accuracy of cancer grading and staging.

Restraints: High Capital Expenditure and Specialized Training Requirements

Market growth is restrained by the high cost of advanced histology equipment and the specialized training required for its operation. Modern histology instruments, such as high-end automated tissue processors and digital slide scanners, represent a significant capital investment for diagnostic laboratories, particularly those in resource-constrained settings. Additionally, the transition to digital pathology workflow requires substantial investments in IT infrastructure and cybersecurity. The shortage of skilled histotechnicians and pathologists who are proficient in using advanced digital tools also presents a challenge to the widespread adoption of these technologies. Organizational resistance to changing established manual workflows and the complexities of integrating new equipment with existing laboratory information systems (LIS) further act as deterrents to market expansion.

Opportunities: Expansion into Emerging Markets and AI-Driven Diagnostic Insights

The expansion of pathology services in emerging markets and the development of AI-driven diagnostic tools offer substantial growth opportunities for the histology equipment market. Countries in the Asia Pacific and Latin American regions are investing heavily in healthcare infrastructure and cancer screening programs, creating a high demand for pathology laboratory equipment. By 2026, the integration of AI in histopathology is enabling more precise and efficient diagnostic workflows, providing an opportunity for vendors to differentiate their products through advanced software capabilities. Furthermore, the rising demand for companion diagnostics and personalized medicine is driving the need for specialized histology equipment that can support complex molecular and immunohistochemistry (IHC) staining protocols, representing a high-value growth segment for market players.

Adoption of Fully Automated and Integrated Histopathology Workflows

A prominent trend in 2026 is the move toward fully automated and integrated histopathology workflows. Diagnostic laboratories are increasingly adopting systems that seamlessly connect automated tissue processors, tissue embedding systems, and slide staining systems. This integration reduces manual handling, minimizes the risk of sample contamination, and improves the consistency of tissue preparation. The convergence of hardware and software is also enabling real-time monitoring of the histopathology process, providing laboratory managers with actionable insights into workflow bottlenecks and equipment performance.

Rise of Ambient Intelligence and AI-Enhanced Sample Tracking

The integration of ambient intelligence and AI-enhanced sample tracking is revolutionizing histology laboratory management. By using RFID and AI-enabled vision systems, laboratories can ensure 100% sample traceability from the point of collection to the final diagnostic report. This technology significantly reduces the risk of sample misidentification, which is a critical patient safety concern in histopathology. Furthermore, AI-driven predictive maintenance for histology instruments is becoming a standard feature, ensuring maximum equipment uptime and reducing the risk of diagnostic delays due to equipment failure.

Analysis by Type

Based on type, the histology instruments segment is expected to hold the largest share in 2026. This dominance is driven by the essential role of instruments such as automated tissue processors, microtomes, and cryostats in the core histopathology workflow. The increasing demand for high-throughput and automated instruments to manage rising diagnostic volumes is a key factor in this segment's growth. The histology consumables segment, including reagents, stains, and slides, is projected to register a steady CAGR, reflecting the recurring demand for these materials in daily pathology operations.

Analysis by Component

Based on component, the equipment segment is expected to account for the largest share in 2026. This includes a wide range of histopathology equipment, such as slide staining systems and tissue embedding systems, which are critical for preparing high-quality tissue sections for examination. The services segment, encompassing equipment maintenance, laboratory design consulting, and staff training, is projected to register the highest CAGR. This growth is driven by the increasing complexity of modern histology laboratory equipment and the need for specialized technical support to ensure optimal performance and regulatory compliance.

Geographic Analysis: Regional Market Dynamics and Diagnostic Expansion

North America is expected to dominate the global histology equipment market in 2026, accounting for an estimated 40-45% of total revenue. The region's leadership is supported by a mature pathology infrastructure, high adoption of digital histopathology, and the presence of leading academic and research institutions. Significant investments in cancer research and the early adoption of AI in histopathology continue to drive market growth in the U.S. and Canada. The presence of major market players and a well-established regulatory environment also contribute to North America's dominant position.

The Asia Pacific region is projected to witness the fastest growth during the forecast period. This growth is fueled by the rapid expansion of diagnostic laboratory networks and government initiatives to modernize healthcare infrastructure across China, India, and Australia. As these countries implement large-scale cancer screening programs and increase their focus on early diagnosis, the demand for pathology laboratory equipment is expected to rise significantly. The increasing adoption of automated tissue processing and digital pathology workflow in the region's leading medical centers is creating substantial opportunities for global histology equipment vendors.

The competitive landscape of the global histology equipment market is characterized by intense innovation and strategic consolidations. Leading players are focusing on the development of integrated and automated platforms that provide end-to-end visibility into the histopathology lifecycle. Strategic acquisitions of digital pathology and AI companies are a common trend as vendors seek to enhance their diagnostic software capabilities. The market is also seeing increased collaboration between equipment manufacturers and laboratory information system (LIS) providers to ensure seamless data integration and more effective laboratory management.

Key players operating in the global histology equipment market include Danaher Corporation (Leica Biosystems) (U.S.), Thermo Fisher Scientific Inc. (U.S.), F. Hoffmann-La Roche Ltd (Switzerland), Sakura Finetek Japan Co., Ltd. (Japan), Agilent Technologies, Inc. (U.S.), Merck KGaA (Germany), PHC Holdings Corporation (Japan), Milestone Srl (Italy), Cardinal Health, Inc. (U.S.), and various emerging technology providers specializing in digital pathology and AI-driven diagnostic tools.

The market is projected to reach USD 5.12 billion by 2036, growing at a CAGR of 7.6% from 2026 to 2036.

Laboratories report a significant reduction in tissue processing times and improved consistency in sample quality.

The histology instruments segment is expected to grow the fastest as laboratories prioritize automation and digital integration.

AI-driven workflows are expected to reduce diagnostic turnaround times by an average of 25% and improve the accuracy of feature recognition.

North America holds the largest share, estimated at 39.5% in 2026, driven by advanced pathology infrastructure and cancer research investments.

Digitization allows for remote slide viewing and consultation, facilitating expert second opinions and improving access to specialized pathology services.

The surge in patient volume is driving the demand for high-throughput histology instruments and automated diagnostic solutions.

Diagnostic laboratories are the primary adopters, managing the highest volumes of tissue samples for clinical diagnosis.

Advanced staining and embedding systems ensure the consistent quality of tissue sections required for complex molecular and IHC analysis.

The top 5 players are Danaher Corporation (Leica Biosystems), Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd, Sakura Finetek Japan, and Agilent Technologies.

1. Market Definition & Scope

1.1. Market Definition

1.2. Market Ecosystem

1.3. Currency Considered

1.4. Key Stakeholders

2. Research Methodology

2.1. Research Approach

2.2. Data Collection and Validation

2.2.1. Secondary Research

2.2.2. Primary Research/KOL Interviews

2.3. Market Sizing and Forecast

2.3.1. Market Size Estimation Approach

2.3.1.1. Bottom-Up Approach

2.3.1.2. Top-Down Approach

2.3.2. Growth Forecast Approach

2.3.3. Assumptions for the Study

3. Executive Summary

3.1. Overview

3.2. Segmental Analysis

3.2.1. Market Analysis, by Type

3.2.2. Market Analysis, by Component

3.2.3. Market Analysis, by End User

3.2.4. Market Analysis, by Geography

3.3. Competitive Analysis

4. Market Insights

4.1. Overview

4.2. Factors Affecting Market Growth

4.2.1. Drivers

4.2.1.1. Rising Cancer Incidence and Demand for Early Diagnosis

4.2.1.2. Shift Toward Digital Histopathology and Automated Workflows

4.2.1.3. Integration of AI in Histopathology for Clinical Decision Support

4.2.2. Restraints

4.2.2.1. High Capital Expenditure for Advanced Histology Instruments

4.2.2.2. Specialized Training Requirements and Skilled Workforce Shortage

4.2.3. Opportunities

4.2.3.1. Expansion of Diagnostic Networks in Emerging Markets

4.2.3.2. Advancements in AI-Driven Digital Pathology Workflows

4.2.3.3. Rising Demand for Companion Diagnostics and Personalized Medicine

4.2.4. Challenges

4.2.4.1. Data Interoperability Across Fragmented Laboratory IT Systems

4.2.4.2. Organizational Resistance to Digital Transformation

4.2.4.3. Managing Cybersecurity Risks in Digital Pathology Hubs

4.2.5. Trends

4.2.5.1. Adoption of Fully Automated and Integrated Histopathology Workflows

4.2.5.2. Rise of Ambient Intelligence and AI-Enhanced Sample Tracking

4.3. Porter’s Five Forces Analysis

4.4. Regulatory Landscape

4.5. Value Chain Analysis

5. Global Histology Equipment Market, by Type

5.1. Overview

5.2. Histology Instruments

5.2.1. Automated Tissue Processors

5.2.2. Microtomes

5.2.3. Cryostats

5.2.4. Tissue Embedding Systems

5.2.5. Slide Staining Systems

5.2.6. Tissue Microarray Instruments

5.3. Histology Consumables

5.3.1. Reagents and Stains

5.3.2. Slides and Cover Slips

5.3.3. Other Consumables

6. Global Histology Equipment Market, by Component

6.1. Overview

6.2. Equipment

6.3. Services

7. Global Histology Equipment Market, by End User

7.1. Overview

7.2. Diagnostic Laboratories

7.3. Hospitals and Academic Institutes

7.4. Pharmaceutical and Biotechnology Companies

7.5. Contract Research Organizations (CROs)

8. Global Histology Equipment Market, by Geography

8.1. Overview

8.2. North America

8.2.1. U.S.

8.2.2. Canada

8.3. Europe

8.3.1. Germany

8.3.2. U.K.

8.3.3. France

8.3.4. Italy

8.3.5. Spain

8.3.6. Rest of Europe

8.4. Asia-Pacific

8.4.1. China

8.4.2. Japan

8.4.3. India

8.4.4. South Korea

8.4.5. Australia

8.4.6. Rest of Asia-Pacific

8.5. Latin America

8.5.1. Brazil

8.5.2. Mexico

8.5.3. Rest of Latin America

8.6. Middle East & Africa

8.6.1. GCC Countries

8.6.2. South Africa

8.6.3. Rest of Middle East & Africa

9. Competitive Landscape

9.1. Overview

9.2. Key Growth Strategies

9.3. Competitive Benchmarking

9.4. Competitive Dashboard

9.4.1. Industry Leaders

9.4.2. Market Differentiators

9.4.3. Vanguards

9.4.4. Emerging Companies

9.5. Market Ranking/Positioning Analysis

10. Company Profiles (Business Overview, Financial Overview, Product Portfolio, Strategic Developments, SWOT Analysis)

10.1. Danaher Corporation (Leica Biosystems)

10.2. Thermo Fisher Scientific Inc.

10.3. F. Hoffmann-La Roche Ltd

10.4. Sakura Finetek Japan Co., Ltd.

10.5. Agilent Technologies, Inc.

10.6. Merck KGaA

10.7. PHC Holdings Corporation

10.8. Milestone Srl

10.9. Cardinal Health, Inc.

10.10. Abcam plc

10.11. Bio-Rad Laboratories, Inc.

10.12. PerkinElmer, Inc.

10.13. Intelsint Srl

10.14. SLEE medical GmbH

10.15. Medite Medical GmbH

10.16. Amos Scientific Pty Ltd

10.17. Hologic, Inc.

10.18. General Data Company, Inc.

10.19. Epredia (PHC Holdings)

10.20. PathAI, Inc.

11. Appendix

Published Date: Jan-2025

Published Date: Jan-2025

Published Date: Jun-2024

Published Date: Jun-2023

Subscribe to get the latest industry updates